Business lawyer > Accounting > Primary documents > Letter to the tax office about lack of activity: sample for the tax office and pension and social insurance funds

During a period of unstable economic conditions, each enterprise may need to temporarily suspend its activities in order to avoid increasing costs that bring losses to the company. In this case, the legal a person must notify regulatory authorities of his lack of commercial activity in order to avoid the accrual of taxes and mandatory payments. Otherwise, they will turn into the company’s debt and will entail the imposition of penalties on it.

Sequence of actions and comments to them

Step No. 1. We decide to stop the business.

The verdict on suspension of activities is made by the board of directors or other highest management body of the company. For example, the director has the right to make the appropriate decision alone. But only if the company’s charter vests him with such powers.

Step No. 2. We issue a directive or order from the manager.

The decision made should be documented. An order or other form of order to suspend activities is issued.

Step No. 3. We cancel the contractual documentation.

We terminate or cancel contracts, agreements and agreements under which such operations are permissible.

Step No. 4. Fulfillment of accepted obligations.

All accepted obligations that cannot be waived will have to be fulfilled. If no operations were carried out under concluded agreements and transactions, then termination of the agreements is permitted.

Step No. 5. Release of employees from their positions.

Complete the procedure in accordance with the provisions of Articles 180 and 157 of the Labor Code of the Russian Federation.

Step No. 6. We notify controllers about the suspension of business.

Send appropriate letters to the controlling ministries and departments.

IMPORTANT!

If you do not send an explanation to the tax office on time about the lack of activity, then controllers will have additional questions. For example, inspectors can initiate an on-site inspection if they notice a decrease in the amounts of taxes and deductions paid.

General provisions

Any company must submit financial statements and tax returns. Even in the absence of business transactions. Mandatory accounting and reflection of the company's financial condition in reporting are determined by Art. Law “On Accounting” dated December 6, 2011 No. 402-FZ. And the obligation of taxpayers to fill out declarations and calculations is established in Art. Tax Code of the Russian Federation.

Therefore, no one relieves the company management of the responsibility for filing reports during the period of suspension.

Algorithm for suspending activities

The decision to freeze a business is made based on a number of factors and reasons. The key problem is the crisis state and financial instability of the economic entity. There is no need to completely liquidate the company. It is enough to suspend activities for a certain time to resolve all the accumulated issues.

But the owner’s decision to freeze the business is not enough. It is required to notify the controllers: compose a letter and send it to all regulatory authorities (Federal Tax Service, Pension Fund of the Russian Federation, Social Insurance Fund, Rosstat, and so on).

It is important to follow the procedure when stopping activities.

What is a zero balance LLC

An LLC has to deal with the concept of a zero balance when preparing annual reports for the Federal Tax Service. Filling out reports is mandatory, since for violation of this paragraph of the Tax Code of the Russian Federation (Tax Code of the Russian Federation), an administrative fine is imposed on both the enterprise and its manager (director).

An LLC cannot have a zero balance. The concept of balance sheet includes not only a certain amount of money or property taken on lease or credit, but also the authorized capital of the company, which is contributed upon opening. It must be declared with an entry in line 1150. Loan funds and property leased or on other terms are also subject to declaration.

According to the Tax Code of the Russian Federation, organizations are required to submit reports on activities no later than March 31 of the year following the reporting year. For example, the organization was founded on 02/01/2017. Reports are due March 31, 2021. Cash is declared on line 1250.

Letters to the Pension Fund and Social Security

You will have to send information to the Pension Fund and the Social Insurance Fund, even if the company does not have a single employee. For example, if a company has stopped its activities and there is only one founder. Moreover, an employment contract has not been concluded with the founder.

IMPORTANT!

You will have to submit a monthly SZV-M if the company has a single director. Explanations for filling out are in the Letter of the Ministry of Labor dated March 16, 2018 No. 17-4/10/B-1846.

In the notification, be sure to indicate:

- Period and reasons for which activities were suspended.

- Number of employees with whom employment contracts have been concluded.

- Passport and personal data of employees.

- The grounds on which wages to employees are not accrued or paid.

- Reasons why the company did not pay insurance premiums and deductions.

The certificate is issued in any form. The signature of the manager or other authorized representative is required. Submit information electronically, by mail or in person on paper.

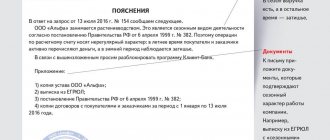

How to notify the Federal Tax Service

Sending a notification to the tax office is the most important step. Fiscal controllers closely monitor any changes in the tax burden of the subject. And if there is a significant decrease in the amount of tax deductions, on-site inspections are initiated. To avoid meeting with auditors, you will have to write a letter.

There are no uniform instructions for registration, as well as a unified notification form. The document is drawn up in any form, but taking into account the mandatory requirements:

- Please indicate the name of the territorial branch of the Federal Tax Service in full. Write down the job title and full name. head of the receiving service department.

- Full name of the applicant - company or entrepreneur. Contact details and mandatory identification codes - TIN, KPP, OGRN and OKVED.

- Title of the document. This could be a “letter on suspension of financial and economic activities” or “certificate of absence of employees in the organization.” Depending on the essence of the explanations sent to the Federal Tax Service.

- The text part of the appeal must disclose the current situation, circumstances and reasons why the entity’s activities are temporarily suspended.

- Evidence base. List all the supporting documents that confirm the fact of business suspension: orders from the manager, copies of additional agreements to termination contracts, release of employees from their positions, etc. Attach copies of documents to the letter.

- Date of document preparation, signature of the head of the company. It is not necessary to put a stamp on the letter. But if the company’s charter provides for the use of an imprint on documentation, then a stamp will have to be affixed.

IMPORTANT!

Be sure to indicate the period of time during which the activities of the economic entity were suspended. If necessary, confirm the facts with documents. Separately indicate taxes, fees and contributions for which there is no tax base for calculation.

The signature of the chief accountant is not required. A sample letter to the tax office regarding the absence of employees and tax objects is certified only by the manager. But the chief accountant’s signature is affixed if such a position is provided for in the company’s staffing table.

What happens if the letter is not written and not poisoned?

Advance notification to the fiscal authorities and social funds will prevent possible questions in connection with the reduction or absence of assessments for certain types of taxes. If such notification is not received, regulatory authorities have grounds to conduct unscheduled inspections to determine the reasons for the decrease in revenue.

Penalties for lack of notification are not provided for in the Tax Code of the Russian Federation and other laws, if the company continues to submit reports on time (even zero) and pay mandatory contributions.

IP on OSNO

If no activity was carried out, the individual entrepreneur submits documents with zero indicators within the following deadlines: VAT report - every quarter by the 25th day of the month following the reporting quarter, and 3-NDFL - once a year until April 30 of the year following the reporting one.

VAT declaration

The zero declaration is submitted within the same time frame as a regular VAT report. Dashes must be entered in the columns; the tax office will not accept reports with zeros.

Declaration 3-NDFL

When conducting non-income-generating activities, expenses may be reflected in the 3-NDFL declaration. Actual and documented expenses are taken into account and subsequently transferred to the next period.

Letter about lack of activity in the Social Insurance Fund

In addition to sending a letter to the tax office and the Pension Fund of the Russian Federation, the FSS will also need to notify the lack of activity. When writing a letter, you will need to indicate the following:

- name of the FSS body;

- name, details and contact details of the organization;

- information about the lack of activity, as well as the calculation and payment of social insurance contributions.

Important! This document is needed so that the Social Insurance Fund is informed that the organization did not work for a specific period of time. There is also no special form provided for this document, so the company has the right to develop it independently. The certificate should be accompanied by a bank statement confirming the fact that there were no funds in the account for a certain period of time.

Does an individual entrepreneur need to submit reports if there is no activity?

Even if an individual entrepreneur does not carry out activities, at the end of the reporting period it is necessary to submit tax reports.

When the activity does not bring profit, the individual entrepreneur still continues to submit declarations, but with zero indicators. Zero declarations are submitted to OSNO, simplified tax system and unified agricultural tax. Individual entrepreneurs do not submit reports only on UTII, since in this mode a zero declaration is not drawn up.

Does an individual entrepreneur need to file reports if there is no income?

In business activities, it may be that during the reporting period no income was received, but expenses were incurred. Justified expenses include documented expenses aimed directly at running the business.

Then, at the end of the year, a loss from business activity is generated - we show it in the reporting. This situation may occur for individual entrepreneurs using a general system and a simplified system. When preparing a UTII return, tax is calculated based on possible income based on physical indicators.

Reasons for writing a letter of absence of activity

Throughout their business activities, companies may encounter various financial problems. In this case, companies suspend their activities and send a message to certain authorities about the lack of commercial activity. The notification is drawn up in the form of a letter along with reporting and sent to the Pension Fund and the tax office to the Social Insurance Fund. The most common reasons for issuing this notice include the following:

- economic crisis;

- suspension of activities;

- Liquidation of company.

The letter is drawn up as a certificate, the form of which is not provided for by law. This document is of a notification nature, informing government authorities that the company does not have commercial, financial and economic activities . Such a certificate is submitted along with monthly documentation. In the absence of this letter, the tax office has the right to forcibly liquidate the company (Read also article ⇒ Zero reporting of the simplified tax system).

Important! A certificate of absence of company activity is submitted to the Federal Tax Service, Social Insurance Fund and the Pension Fund of the Russian Federation. In some cases, a certificate may be required by other authorities, for example, the prosecutor's office when conducting scheduled inspections. In this case, at the oral request of the prosecutor's office, the company is obliged to provide this document.

When should I write and submit?

There is no statutory deadline for submitting such an explanation. The information is sent to regulatory authorities along with reporting for the period when the company suspended its activities. The explanation is drawn up anew each time, since the period for which reporting is provided changes. There is no penalty for failure to provide a certificate of suspension of operation. An exception is the provision of information to the employment center. Federal Law No. 1032-1 of April 19, 1991 requires information about the suspension of proceedings to be provided within three days after the decision is made.

Single simplified declaration

Instead of several zero tax reports, an LLC can send to the Federal Tax Service a single simplified declaration in the form KND 1151085. But enterprises are allowed to use this form only if the following conditions are simultaneously met (clause 2 of Article 80 of the Tax Code of the Russian Federation):

- During the reporting period, no business transactions were carried out on the organization's current accounts or cash register, i.e. there was no movement of money;

- the company did not have taxable objects.

The document replaces several company declarations at once.

How to send a notification

There are different ways to submit information to the inspectorate. For example, provide a package of documents in person. Be sure to take your passport and documents confirming the authority of the manager with you. An official representative can also submit papers; in this case, a power of attorney is required.

It is allowed to notify the Federal Tax Service by mail. Send the documentation by registered mail. Be sure to fill out an inventory of investments. This receipt confirms that you sent information to the inspectorate in a timely manner.

You can send a letter electronically. For example, via secure communication channels or using an account in the taxpayer’s personal account. In any case, special cryptographic protection tools will be required. This is an enhanced qualified digital signature.

Answers to common questions

Question: Is there a fine for failure to notify the tax authority of the lack of activity?

Answer: No, there is no penalty for failure to notify. But the company will also have to submit reports and pay mandatory fees.

Question: How can you confirm that the company did not conduct financial and economic activities?

Answer: To do this, you will need to obtain a statement from the bank confirming that there are no movements on the current account. This will confirm that there were no movements on the account with the participation of the company.

Information to Rosstat and other departments

You will also have to notify the territorial statistics office. Send a standard letter indicating the reasons and period for which the activity is suspended. If a company is required to submit narrow-profile reporting forms to Rosstat, then it will have to prepare additional forms.

IMPORTANT!

Don't forget to send similar notifications to all regulatory authorities, depending on the type of business you choose. For example, write a sample letter to Rosprirodnadzor about the lack of activity, if previously the company had to report to Rosprirodnadzor.

Reporting to statistics is allowed on paper or electronically. It is possible to send documents by mail. Let us remind you that for failure to provide statistical reporting, administrative liability is provided in the form of fines of up to 70,000 rubles (150,000 for a repeated violation). It is important to notify Rosstat in advance to avoid sanctions from controllers.