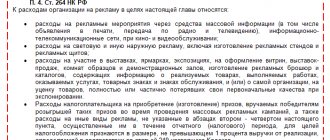

Companies whose main activity is the production of agricultural products pay the unified agricultural tax (USAT) to the budget. In addition to the basic tax, agricultural producers pay income tax, and such enterprises are required to apply a zero rate for this tax. We propose to understand how income tax is paid for agricultural producers who receive income from activities related to the sale of produced products.

Main changes for AU

Firstly, the income tax rate remains at 0% for organizations engaged in educational and (or) medical activities, as well as for organizations providing social services to citizens. Secondly, a 0% rate is provided for the income tax of museums, theaters and libraries.

Important: all institutions that have switched to using a 0% rate are not exempt from taxpayer obligations. In accordance with the requirements of paragraph 2 of Art. 289 of the Tax Code of the Russian Federation, taxpayers are required to maintain tax records and submit a tax return after the expiration of the tax period (calendar year).

When calculating the share, not all income is taken into account

To determine the status, the total revenue from the sale of products, works and services is compared with the revenue from the sale of its own agricultural products and processed products.

Other income is not taken into account when calculating the share. In particular, the income of an agricultural enterprise from the sale of a share in the authorized capital of another company is not taken into account. This was pointed out by financiers in a letter from the Russian Ministry of Finance dated December 3, 2009 No. 03-11-06/1/51. The situation is similar with the implementation of land lease rights. Also, when calculating the share, non-operating income is not taken into account, the list of which is established in Article 250 of the Tax Code of the Russian Federation. For example, income from leasing property (including land plots) for rent (sublease), if such income is not defined by the taxpayer himself as income from sales (letter of the Ministry of Finance of Russia dated June 5, 2012 No. 03-11-06/1/12). Income in the form of interest received under loan agreements, bank accounts, bank deposits, as well as securities (letter of the Ministry of Finance of Russia dated October 24, 2011 No. 03-11-06/1/17) is also not taken into account. Income in the form of gratuitously received property (work, services) or property rights is not taken into account.