Taxable income

In accordance with the law, the following income of an organization is subject to income tax:

- income received from the sale of goods, works, services. In this case, it does not matter whether these are purchased goods or goods of own production.

- non-operating income, such as:

- profit from previous reporting periods identified in the current reporting year;

- positive amount differences;

- positive exchange rate differences;

- property received free of charge;

- penalties and fines;

- written off accounts payable;

- interest on bills and commercial loans;

- interest received on loans;

- dividends;

- the cost of valuables identified during inventories or received after the liquidation of fixed assets, etc.

VAT

VAT – value added tax – is a form of withdrawal of a share of the cost of a product to the state budget. Implemented and paid at all stages of production.

Formula for calculating VAT tax

The tax is calculated using the following formula:

VAT=Cost*St,

Where:

- Cost – the cost of products sold (with excise taxes, but excluding VAT).

- St – tax rate (0%, 10%, 18%).

VAT calculation examples

sells 1 thousand Christmas tree decorations at a price of 10 rubles per piece. The tax rate is 18%, and the tax is not taken into account in the price tag. It is necessary to calculate VAT and the final cost of the product (including tax).

- First of all, the cost is determined without VAT (NB): 1,000*10= 10,000 rubles.

- VAT is calculated from the amount received: 10,000*0.18= 1,800 rubles.

- The amount including VAT is revealed: 10,000+1,800= 11,800 rubles.

- The final amount can be determined immediately: 10,000*1.18=11,800 rubles.

Example of VAT calculation

In accordance with the calculations performed, the following indicators must be indicated in the settlement documents:

- cost without VAT – 10 thousand rubles;

- VAT at the rate of 18% - 1,800 rubles;

- cost including VAT – 11.8 thousand rubles.

So, every tax agent must understand that the terms of tax payment are considered binding, since regulatory authorities monitor the accounting system of any organization. If violations are detected, penalties will be imposed on the guilty person, which will subsequently negatively affect the reputation of the entire company.

Tax-free income

The list of income not subject to income tax is given in Article 251 of the Tax Code of the Russian Federation and is final.

Not subject to taxation:

- prepayment made for goods when the accrual method is used;

- borrowed funds received;

- the value of property contributed as a contribution to the authorized capital;

- the value of property or funds received by the organization in connection with the fulfillment of obligations under the agency agreement, with the exception of the intermediary’s own remuneration;

- grants and targeted funding;

- the cost of inseparable improvements to fixed assets provided under a free use agreement;

- the cost of inseparable improvements to the leased property made by the lessee.

Also, property received free of charge is not subject to taxation:

- from an individual, provided that the person’s share in the authorized capital of the organization is more than 50%;

- from a legal entity, provided that its share in the authorized capital of the recipient is more than 50%;

- from another organization, provided that the recipient’s share in its authorized capital is more than 50%.

If the listed property was transferred for use or ownership to third parties during the year, income tax must be paid in accordance with the general procedure.

What may be subject to taxation

In Russia, contributions to the budget are paid by individuals and legal entities - subjects of taxation. To understand whether you need to calculate and pay taxes, try to evaluate your income, assets or activities you engage in. These are sources or objects of tax obligations:

- the population working under employment contracts pays personal income tax, enterprises pay a tax on profits;

- property contributions are levied on the real estate of individuals and organizations, transport, and land;

- taxable activities: mining, exploitation of water bodies. The tax on gambling business, trade tax and excise taxes are calculated separately;

- a special group made industry contributions to the budget for the use of subsoil, animals and aquatic biological resources;

- Entrepreneurs or LLCs have the right to choose one or more special tax regimes. This is UTII (single tax on imputed income), simplified taxation system (simplified taxation system), unified agricultural tax (unified agricultural tax) or patent. The fee system allows you to apply these modes and calculate taxes in parallel to each other.

If a taxpayer is registered as an individual entrepreneur, this does not cancel his obligation to make mandatory tax payments as an individual. These are property taxes, personal transport taxes, personal income tax and land taxes.

Organizational expenses subject to deduction

- Employee remuneration costs. This group includes:

- wages;

- bonuses;

- compensation;

- additional payments;

- one-time payments for length of service;

- labor costs for employees working under civil contracts;

- insurance payments, both under compulsory and voluntary insurance contracts;

- labor costs for periods of forced temporary downtime;

- accruals for staff reductions or company reorganization;

- funds reserved for the upcoming payment of benefits for length of service and vacation pay;

- employee costs for paying interest on loans for the purchase and construction of housing, etc.

- Material costs

- Depreciation of fixed assets

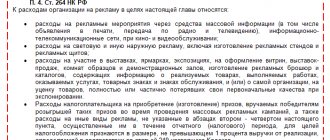

- Other costs associated with sales and production. Such as:

- rent;

- Third-party company services;

- advertising;

- compensation for the use of personal transport;

- travel and entertainment expenses;

- personnel training;

- insurance;

- rights to use programs and databases for computer equipment.

- Non-operating expenses, which include:

- interest on loans and credits;

- interest on securities;

- legal costs and arbitration fees;

- fines, penalties, penalties for violated terms of contracts;

- shortages of material assets identified during inventories, in the absence of culprits;

- negative exchange rate difference;

- expenses incurred in connection with the formation of a reserve for doubtful debts;

- losses from previous years that were identified in the current tax period;

- written off accounts receivable;

- losses due to force majeure.

Types and Types of Tax Rates

The standard classification of tax rates is carried out on certain grounds. Thus, according to the degree of burden for the taxpayer, the following types of tax payments are distinguished:

1. Basic NS. This concept does not provide for the classification of the taxpayer into any specific group, which gives him the opportunity to enjoy tax benefits and other preferences;

2. An increased tax rate is established in relation to taxpayers whose activities can be characterized as such, which gives the state the right to levy an increased tax from the payer;

3. Reduced NS. The use of this type of tax rate allows the taxpayer to enjoy tax benefits and preferences, up to the use of zero tax.

According to the method of establishment, tax rates can be:

1. Absolute.

The absolute tax rate is a fixed value determined for each specific object of taxation separately;

2. Relative.

The size of the relative tax directly depends on the size of the taxable object and is calculated in proportion to it.

According to the jurisdiction of approval, tax rates are divided into the following:

- federal;

- regional;

- local.

Expenses that are not tax deductible

Expenses that are not subject to tax deduction are listed in Article 270 of the Tax Code of the Russian Federation.

Such expenses include:

- contributions of founders to the authorized capital;

- taxes and payments for exceeding limits on emissions of pollutants into the environment;

- penalties and fines transferred to the state budget, as well as state extra-budgetary funds;

- payments and remuneration to members of the board of directors;

- contributions to the reserve in case of depreciation of investments in securities. The exception is the contributions of professional participants in the securities market;

- losses incurred in the process of servicing production and farming. This list includes objects of both socio-cultural and housing and communal services;

- prepayment made for the goods, in case of using the accrual method;

- property and funds transferred under loans and loan agreements;

- voluntary membership fees to public organizations;

- the value of property transferred free of charge. This also includes the cost of transferring such property;

- fee for notary registration when the amount of such fee exceeds the established tariffs;

- the amount of revaluation of securities at market value in case of a negative difference;

- bonuses paid from earmarked proceeds or special-purpose funds;

- partial or full repayment of loans provided to employees for housing;

- lump sum payments for retirement , as well as pension supplements;

- payment for vacations not provided for by current legislation, but provided for by the collective agreement;

- vacation and treatment vouchers for employees;

- visiting cultural and sporting events;

- n subscription to literature not used for production purposes;

- payment for travel from home to the place of work and back, if such payment is not provided for by the provisions of the collective agreement or technological features of production;

- preferential or free meals in cases where it is not provided for by the provisions of the collective agreement or current legislation;

- payment for personal consumption goods and similar expenses made in favor of the employee.

Section on document restoration - how to restore a pension insurance certificate.

In the news (here) about how to restore a lost driver's license.

How to register an inheritance for a house? https://urist.club/inheritance/coming_into/kak-oformit-nasledstvo.html

What is important to consider when calculating tax

Employees of the fiscal department themselves determine the amount of payment when calculating taxes: transport, land, and property of individuals. In these cases, tax notices are sent to payers by mail or via electronic resources.

The employer is the tax agent. He calculates and pays the monthly contribution to the budget from the income for the employee. All other tax payers calculate it themselves.

When making calculations, it is important to take into account the order of calculation and payment. When independently calculating the tax amount, a declaration is first submitted to the inspectorate, where the payer must calculate the tax. Payment occurs later.

It is equally important to meet deadlines. In case of late payment, a penalty will be charged. Unpaid contributions to the budget are collected in the form of a fine of 20% of the tax amount. The payer is also punished if the tax is calculated with inaccuracies. If errors in calculations are recognized as intentional, the amount of the fine increases to 40% - Art. 12 of the Tax Code of the Russian Federation.

The tax payment amount is calculated for a specific period of time—the tax period. Typically this is a calendar year, but can be a month or a quarter.

Sources:

Taxes of the Russian Federation

Information about tax rates and benefits

tax code

Profit tax amount

The tax rate for income tax for organizations under current legislation is 20%. Of this, 2% goes to the federal budget, and 18% goes to the regional budget.

This tax rate applies to residents of the Russian Federation.

For foreign organizations, if they do not have a permanent establishment in the Russian Federation, the amount of income tax is 20% on all income and 10% on the use or delivery of vehicles for international transport.

Tax base object for various taxes

Taxes can be levied according to various algorithms - in some, cost indicators are taken as a basis, in others, it is necessary to focus on the number of objects of taxation or their physical characteristics.

The taxable base is displayed separately for each tax, and each tax has its own object of taxation (Clause 1, Article 38 of the Tax Code of the Russian Federation). What can act as an object of tax collection:

- sale of goods or services;

- sale of owned property;

- income or profit;

- vehicles;

- another circumstance that may have a qualitative or cost characteristic.

The tax base is defined as the value expression of the object of taxation, but there are exceptions to this rule. A non-standard algorithm for calculating the amount of taxation is inherent, for example, in transport tax - the object is cars and other vehicles, but the basis for calculations is not their price, but engine power. The cost factor has an indirect effect - for expensive cars, special increasing factors are introduced into the calculation formula.

Example of calculation procedure

Manufacturing organization X took out a loan of 1 million rubles in the current reporting period, and made an initial payment of 400 thousand rubles.

Amounts on loans and advance contributions in this case are not subject to taxation.

In the first quarter of the year, the organization received revenue of 1,770 thousand rubles, including VAT of 270 thousand rubles.

Production costs amounted to 560 thousand rubles. Staff salaries are 350 thousand rubles.

Insurance contributions from wages - 91 thousand rubles. Depreciation of equipment - 60 thousand rubles.

Interest on a loan issued to another company and taken into account for tax purposes for the first quarter amounted to 25 thousand rubles. We also take into account last year’s tax loss, which amounted to 120 thousand rubles.

Total expenses for the first quarter of the year: 767,700 rubles.

Taxable profit for the first quarter of the year: 612,300 rubles.

1,770,000 (revenue) - 270,000 (VAT) - 767,700 (expenses) - 120,000 (tax loss for last year) = 612,300 rubles.

The amount of income tax will be: 122,460 rubles.

612,300 (profit) x 20% (tax rate) = 122,460 rubles.

the amount of tax going to the federal budget: 612,300 x 2% = 12,246 rubles.

the amount of tax going to the regional budget: 612,300 x 18% = 110,214 rubles.

The procedure for submitting a declaration, paying tax and advance payments

The reporting period for income tax is 1 year. But if all economic entities begin to contribute amounts only after its expiration, then the budget will be replenished unevenly. Therefore, advance tax payments have been introduced. They can be:

- Quarterly. In this case, income tax is calculated for 3, 6, 9 months, taking into account the amounts paid for the previous period. According to Article 286 of the Tax Code of the Russian Federation, all payers contribute them. The exception is budgetary cultural institutions and organizations that use monthly payments based on actual profits.

- Quarterly, broken down by month. A legal entity is required to use this type of payment if it received revenue of more than 15 million rubles in each of the previous four quarters. The algorithm for calculating the amount of the monthly payment is that the tax for previous quarters is determined on an accrual basis, starting from January 1 of the reporting year. Its size is adjusted based on the results of the reporting quarter, depending on the profit received. Budgetary and non-profit organizations are exempt from payments.

- Monthly based on the actual profit received. This option can be used by any company. In this case, the tax amount is determined monthly on an accrual basis from the beginning of the year. When paying it, the amounts transferred for previous months are taken into account.

At the end of each reporting period, the organization must submit a declaration. Its sample, recommended form and filling rules are approved by the Order of the Federal Tax Service of Russia.

The document should be submitted to the tax office:

- at the location of the organization;

- at the location of each separate division.

In the case where subsidiaries are located on the territory of one subject of the Federation, then the tax can be paid to the regional budget through any of them, and which one is determined by the organization itself.

If the number of employees of an organization exceeds 100 people, then the declaration is accepted by the tax authority only in electronic form.

All organizations are required to submit their annual declaration no later than March 28 of the year following the previous one. The deadlines for the reporting periods depend on the option of transferring “profitable” advances:

- If monthly, based on actual profit, the declaration is submitted by the 28th of each month. In this case, the reporting periods are 1, 2, 3 months, etc. until the end of the calendar year.

- If you report quarterly, you will have to report on the results of 3, 6 and 9 months. The declaration must be submitted by the 28th day of the month following the reporting quarter, that is, by April 28, July 28, October 28.

Penalties and fines are provided for failure to meet the deadlines for making advance payments and filing declarations.

How is income tax calculated?

First you need to calculate the tax base, which is calculated as the difference between the organization's total income, expressed in cash or in kind (OD), and its total expenses (OR). That is, the tax base is the total profit of the enterprise minus expenses for the reporting period.

Total income is the sum of income received as a result of the main and secondary activities of a given organization. Simply put, this is the total profit.

The total expense consists of advertising costs, labor costs, depreciation, production costs, as well as fines, debts, etc.

Also, to calculate income tax, you need to know the tax rate (TS) as a percentage, which since 2015 has been 20%, with rare exceptions (but cannot be lower than 12.5%).

Algorithm for calculating income tax (IP): NP= (OD-OR)*NS/100

The amount obtained as a result of these calculations will be the amount of tax that must be paid.

Basic rates

Calculate income tax at the rate for 2021 for taxpayers under the general tax regime - 20% of the obtained financial result of the activity. Until 2021, organizations contributed 18% to the regional budget and 2% to the federal budget. From the end of 2021, a different breakdown by budget level came into force (Order of the Federal Tax Service of the Russian Federation No. ММВ-7-3 / [email protected] dated 10/19/2016). Now taxpayers transfer 17% to the regional budget and 3% to the federal treasury. Local governments have the opportunity to reduce the tax rate transferred to the treasury of a particular region, but the regional rate should not be less than 13.5%, and the minimum overall rate should not be less than 16.5%.

Let's look at an example of how to calculate income tax for the general tax rate. Each region has established minimum values for certain types of taxpayers. For example, in Moscow, a reduction in the tax burden to 13.5% is confirmed by the Federal Tax Service for enterprises that employ people with disabilities, produce vehicles, or represent special economic zones, technopolises and industrial parks. In St. Petersburg, only those payers who work in the territory of the special economic zone pay a simplified regional contribution of 13.5%.

Some categories of taxpayers pay fees at special rates, the accrued amounts of which are sent exclusively to the federal budget. Special rates apply to the following categories of payers for certain types of income:

- foreign companies that do not have a Russian representative office, producing hydrocarbons and controlled foreign companies - 20%;

- foreign companies without a representative office in Russia pay a tax on income from the rental of vehicles and for international transport - 10%;

- Russian enterprises from dividends of foreign and Russian companies and from dividends from shares on depositary receipts - 13%;

- foreign companies receiving dividends from Russian enterprises and owners of yield on state and municipal securities - 15%;

- companies receiving income from interest on municipal securities and other income, according to paragraphs. 2 clause 4 art. 284 of the Tax Code of the Russian Federation - 9%.

Medical and educational institutions, residents of special economic zones and free economic zones in Crimea and the city of Sevastopol, organizations participating in regional investment projects and operating in the territory of rapid socio-economic development are exempt from paying the fee.

Declaration and period code

A tax return when calculating income tax is a document filled out by the taxpayer, which reflects information about his main activity, namely:

- the organization's income and expenses;

- tax deductions (refunds) and benefits;

- total tax amount;

- information about objects subject to taxation;

- other data serving as the basis for calculating tax.

A tax return is submitted by each taxpayer for each tax separately. For each tax, the legislation sets its own deadlines for submitting the declaration.

When filling out a tax return, you must indicate the tax period code. The period can be one calendar month, quarter, year or other period of time.

- codes 01-12 correspond to twelve months (01 – for January, etc.);

- codes 21-24 - four quarters;

- code 51 indicates the first quarter upon liquidation of the enterprise; 54 – second quarter; 55 – third; 56 – fourth;

- codes 71-82 correspond to twelve months and are also indicated when liquidating an organization (71 for January, 72 for February, etc.).

Error in calculation: how to fix

If an error was made in the taxpayer's accounting when calculating the amount of the taxable amount, it must be corrected. Officials have provided two options for correcting errors:

- The period of the error is determined. In this case, the taxpayer makes accounting corrections precisely in the calculation (tax) period for which the inaccuracy was made. Then he submits adjustment reports to the Federal Tax Service and pays the amounts of the identified debt or asks to offset the overpayment against future payments.

- The period of the error cannot be determined. In such circumstances, corrections are made in the settlement (tax) period in which this inaccuracy was discovered. In this case, prepare an explanatory note to the Federal Tax Service to warn inspectors in advance and avoid penalties.

There is no specific deadline for submitting adjustments to the Federal Tax Service. However, there is no need to hesitate. Submit the corrected report immediately upon discovery of an error before the office or on-site inspection of the inspectorate. Otherwise, tax authorities will impose fines.

Calculation methods

There are two methods for calculating income tax:

- Basically, the accrual method is used. When maintaining tax accounting using this method, all income (expenses) are reflected in the reporting period when they were incurred, regardless of the actual date of receipt of funds. That is, revenue is recognized based on shipment and presentation of settlement documents.

- In some cases, the use of the cash method is permitted, according to which income and expenses are recognized based on the actual accrual of funds.

Determination of the tax base

The tax system operates in Russia according to the rules laid down in the Tax Code of the Russian Federation. All taxpayers are required to make tax payments within a strictly specified time frame and in compliance with the principle of complete repayment of debts. The amount of the tax base acts as a structural element of any tax. The taxable amount can be presented in different forms:

- cost measurement of the object;

- physical characteristics of the subject of taxation;

- different meaning.

The tax base is a cost expression of the object of taxation, from which the final value of taxpayers' obligations to budgets of different levels is derived.

The tax base of an organization for various types of payments is calculated based on the results of tax periods. The basis for deriving this parameter is the accounting and tax registers. If an error was made during the calculation process, it is eliminated by adjusting the tax base for the period in which the error occurred, and not in the current interval.

Taxable amounts can be withdrawn in two ways:

- Cash method - in this case, income and expense transactions actually performed by the taxpayer in the period under review are taken into account.

- The accrual method, when the emphasis is placed on the date the right to a property asset arises or on the moment the liability arises.

Physical indicators and basic UTII profitability

Next, let's take a closer look at the above indicators.

The values of basic profitability and physical indicator are determined for each specific type of business activity and approved by the norms of Article 346.29 of the Tax Code of the Russian Federation.

| Types of business activities | Physical indicators | Basic income per month (rubles) |

| 1 | 2 | 3 |

| Provision of household services | Number of employees, including individual entrepreneurs | 7 500 |

| Provision of veterinary services | Number of employees, including individual entrepreneurs | 7 500 |

| Providing repair, maintenance and washing services for motor vehicles | Number of employees, including individual entrepreneurs | 12 000 |

| Provision of services for the provision of temporary possession (for use) of parking spaces for motor vehicles, as well as for the storage of motor vehicles in paid parking lots | Total parking area (in square meters) | 50 |

| Provision of motor transport services for the transportation of goods | Number of vehicles used to transport goods | 6 000 |

| Provision of motor transport services for the transportation of passengers | Number of seats | 1 500 |

| Retail trade carried out through stationary retail chain facilities with trading floors | Sales area (in square meters) | 1 800 |

| Retail trade carried out through facilities of a stationary retail chain that do not have sales floors, as well as through facilities of a non-stationary retail chain, the area of the retail space in which does not exceed 5 square meters | Number of retail places | 9 000 |

| Retail trade carried out through stationary retail chain facilities that do not have trading floors, as well as through non-stationary retail chain facilities with a retail space exceeding 5 square meters | Area of retail space (in square meters) | 1 800 |

| Delivery and distribution retail trade | Number of employees, including individual entrepreneurs | 4 500 |

| Sales of goods using vending machines | Number of vending machines | 4 500 |

| Provision of public catering services through a public catering facility with a customer service hall | Area of the visitor service hall (in square meters) | 1 000 |

| Provision of public catering services through a public catering facility that does not have a customer service hall | Number of employees, including individual entrepreneurs | 4 500 |

| Distribution of outdoor advertising using advertising structures (except for advertising structures with automatic image changes and electronic displays) | Area intended for printing (in square meters) | 3 000 |

| Distribution of outdoor advertising using advertising structures with automatic image changes | Exposure surface area (in square meters) | 4 000 |

| Distribution of outdoor advertising using electronic signs | Light emitting surface area (in square meters) | 5 000 |

| Advertising using external and internal surfaces of vehicles | Number of vehicles used for advertising | 10 000 |

| Provision of temporary accommodation and accommodation services | Total area of premises for temporary accommodation and living (in square meters) | 1 000 |

| Provision of services for the transfer for temporary possession and (or) use of retail spaces located in facilities of a stationary retail chain that do not have trading floors, facilities of a non-stationary retail chain, as well as public catering facilities that do not have customer service halls, if the area of each they do not exceed 5 square meters | Number of trading places, non-stationary retail chain facilities, and public catering facilities transferred for temporary possession and (or) use | 6 000 |

| Provision of services for the transfer for temporary possession and (or) use of retail spaces located in facilities of a stationary retail chain that do not have trading floors, facilities of a non-stationary retail chain, as well as public catering facilities that do not have customer service halls, if the area of each exceeds 5 square meters | Area of a retail space, a non-stationary retail chain facility, or a public catering facility transferred for temporary possession and (or) use (in square meters) | 1 200 |

| Provision of services for the transfer of temporary possession and (or) use of land plots for the placement of stationary and non-stationary retail chain facilities, as well as public catering facilities, if the area of the land plot does not exceed 10 square meters | Number of land plots transferred for temporary possession and (or) use | 10 000 |

| Provision of services for the transfer of temporary possession and (or) use of land plots for the placement of stationary and non-stationary retail chain facilities, as well as public catering facilities, if the area of the land plot exceeds 10 square meters | Area of land transferred for temporary possession and (or) use (in square meters) | 1 000 |

Correction factors K1 and K2

Coefficients K1 and K2 allow you to adjust the basic profitability taking into account the influence of various external conditions (factors) on the amount of income received.

K1 is a deflator coefficient established by federal legislation for the calendar year. It is determined annually by the Ministry of Economic Development of Russia and published no later than November 20 of the year in which deflator coefficients are established. Its value corresponds to the indexation of consumer prices for various categories of goods and services.

UTII Coefficient K1 for 2021 is 1.915

K2 – adjustment coefficient of basic profitability, established by local legislation and taking into account the totality of features of doing business (list of goods, services, other features).