Each business representative, choosing a tax regime at the beginning of his entrepreneurial journey, or changing it in the process of work, focuses primarily on the expected amount of tax payments. The main interest is to save as much as possible on taxes, but not least of all is the simplicity and clarity of the tax system. That is why the simplified taxation system is in great demand among Russian businessmen - it is quite understandable even for a non-specialist. Despite the fact that it has some subtleties and nuances, most businessmen choose it as the main mode. In this article we will talk about how to calculate tax income minus expenses using a simplified taxation system.

Tax base for the simplified tax system

1. For the simplified tax system “income”, the tax base for determining the tax is income. 2. For the simplified tax system “income reduced by the amount of expenses”, the tax base is the monetary expression of income reduced by the amount of expenses.

For both options, the procedure for determining and the composition of income is the same; income under the simplified tax system is recognized as:

- income from sales, i.e., proceeds from the sale of goods, works and services of own production and previously acquired, and proceeds from the sale of property rights;

- non-operating income specified in Art. 250 of the Tax Code of the Russian Federation, such as property received free of charge, income in the form of interest on loan agreements, credit, bank account, securities, positive exchange rate and amount differences, etc.

Expenses recognized under the simplified system are given in Art. 346.16 Tax Code of the Russian Federation. The list of expenses is quite long. If necessary, you can familiarize yourself with it directly in the Tax Code of the Russian Federation.

Articles 346.15 to 346.17 of the Tax Code of the Russian Federation specify the procedure for determining and recognizing income and expenses under the simplified tax system.

How to calculate the simplified tax system in 2017 - innovations

Having dealt with the example of calculating the simplified tax system - income for 2021, it is necessary to clarify whether there have been any changes in its algorithm in 2021. This year has not brought any special innovations in terms of calculating both the tax itself and the tax base. However, we note that some new conditions have been introduced for the use of the special simplified tax regime, such as increasing the limits on income received. When deciding to switch to a simplified system and when applying this regime, you need to carefully monitor so as not to “fly” beyond the restrictive framework.

Formula for calculating the simplified tax system

1. For the simplified tax system “income”: Income X Tax rate. 2. For the simplified tax system “income minus expenses”: (Income minus expenses) X Tax rate.

These are the general formulas used to calculate the simplified tax system in 2020. These formulas do not take into account the following important details:

1. Recognition and accounting of expenses for calculating the tax base on the simplified tax system Income minus expenses:

In order for expenses under the simplified tax system “income minus expenses” to be confirmed, it is necessary to formalize them in accordance with the law. Otherwise, the tax authority will not take them into account when calculating the simplified tax system.

To confirm expenses, the following documents must be completed:

- payment document (receipt, account statement, payment order, cash receipt);

- a document confirming the transfer of goods or the provision of services and performance of work (invoice for the transfer of goods or an act for services and work).

2. Reducing the single tax on the simplified tax system due to paid insurance premiums:

- under the simplified tax system, “income” can be reduced by the single tax itself (advance payment);

- under the simplified tax system “income minus expenses”, insurance premiums can be taken into account when calculating the tax base (included in expenses).

EXAMPLE 1

Initial data:

1. LLC "Salut". 2. The amount of income is 270,000 rubles. 3. The amount of expenses supported by documents is 225,000 rubles:

- employee salary - 60,000 rubles;

- mandatory insurance premiums - 21,300 rubles;

- advertising expenses - 20,000 rubles;

- expenses for stationery - 5,000 rubles;

- expenses for postal and telephone services - 2,000 rubles;

- expenses for maintaining official transport - 19,000 rubles;

- expenses for renting premises - 50,000 rubles;

- expenses for paying the cost of goods purchased for further sale, reduced by the amount of VAT on paid goods purchased by the taxpayer and subject to inclusion in expenses - 47,000 rubles.

Task 1.

How to calculate an advance payment under the simplified tax system “income”, with a tax rate of 6%.

Answer:

270,000 (income) X 6% = 16,200 rubles.

The advance payment is subject to reduction by the amount of insurance premiums paid, but not more than 50% of the calculated advance payment:

16,200 - 21,300 = 16,200×50% = 8,100 rubles.

We get 16,200 - 8,100 = 8,100 amount of the advance payment of the simplified tax system, income payable.

Task 2.

How to calculate an advance payment under the simplified tax system “income minus expenses” at a tax rate of 15%.

Answer:

(27,000 - 225,000) X 15% = 6,750 rubles.

In this case, the advance payment is not subject to reduction by the insurance premiums paid, since the amount of insurance premiums is already taken into account in expenses.

CONCLUSION:

In comparative examples with the same initial data, the simplified taxation system “income minus expenses” is more optimal. But this only happens if the entrepreneur has large expenses.

In what case is it beneficial to use it?

As a preferential treatment, this system is beneficial for most companies. However, when comparing two types of simplified tax system, it must be taken into account that each of them has positive and negative sides.

STS 15 income minus expenses is beneficial in situations where a business entity has a sufficient amount of costs, which it has the right to take into account when calculating tax.

When a taxpayer has a low level of expenses, then it is most profitable for him to use the simplified tax system for income. As a rule, this situation arises among organizations providing services. If an enterprise is engaged in production or trade, then a system with a rate of 15% is more preferable for it.

Attention! Current practice shows that the simplified tax system of 6% is best used when the share of expenses in the revenue received does not exceed 60%.

Deadline for payment of the simplified tax system

Despite the fact that, according to the Tax Code of the Russian Federation, the tax period for calculating tax on the simplified tax system is a calendar year, the obligation to pay this tax arises quarterly. The calculation is carried out on a cumulative basis: 1st quarter, half-year, nine months of the calendar year, calendar year.

Deadlines for payment of advance payments for single tax:

- based on the results of the first quarter - April 25;

- based on the results of the half year - July 25;

- based on the results of nine months - October 25;

- at the end of the year - until March 31 for organizations; until 30.04 for individual entrepreneurs. When calculating the simplified tax system at the end of the year, advance payments paid are taken into account.

Briefly about the tax regime

Often firms and individual entrepreneurs strive to work in a “simplified” way, especially at the dawn of a business. This is due to the fact that using the simplified tax system you do not need to pay:

- for private entrepreneurs - personal income tax;

- firms, offices and other enterprises – a profitable fee;

- companies not exporting – VAT;

- property tax (excluding objects for which the financial base is determined by cadastral value).

The payer himself can decide to work under the simplified tax system, that is, this system is considered voluntary. When registering an individual entrepreneur or LLC, you must attach an application to the package of documents for the tax service, expressing your desire to work in a “simplified” manner. Existing companies can also change the regime to the simplified tax system, but there are restrictions. Companies cannot do this:

- with an income of more than 58 million 805 thousand rubles;

- having more than 150 million rubles of fixed assets;

- which employ more than one hundred employees;

- having more than 25% share of participation of third-party companies.

According to the law, it is permissible to switch from regime to regime once a year - from January 1. The transfer application must be prepared no earlier than October 1, since the funds earned are recorded over the past nine months.

In addition to the single tax, other tax fees are also paid: contributions to the Pension Fund of the Russian Federation and the Compulsory Medical Insurance Fund, social insurance, property, water and land taxes, excise taxes, state duties and VAT for exporting companies.

Examples of calculations of advance payments and single tax on the simplified tax system

How to calculate the simplified tax system “Income” with examples of calculation for the 1st quarter is described above.

The calculation of the advance payment based on the results of the half-year is similar to the calculations for the 1st quarter. Then you need to multiply the tax base obtained based on the results of 6 months (from January to June inclusive) by the tax rate, and from this amount subtract the advance payment already paid for the first quarter. In the case of the simplified tax system “income”, the amount received must be reduced by insurance premiums (but not more than 50%). The resulting balance will be an advance payment for the six months.

We do the same when calculating the advance payment of the simplified tax system “income minus expenses”, except for reducing the advance payment due to insurance premiums.

At the end of the year, the single tax is calculated as follows:

- We multiply the tax base for the entire year by the tax rate. From the resulting amount we subtract all three advance payments. The resulting difference is the annual simplified tax system.

How to calculate simplified tax in 2021 (example)

It is best to learn how to calculate the 6% simplified tax system based on a practical example.

Example

Having chosen trading activity as the main direction, Altair LLC uses a simplified system of settlements with the budget with the object of the simplified tax system “income”. For 2021, she managed to receive income in the amount of 3,560,000 rubles. By month they were:

| No. | Month | Amount of income, thousand rubles. |

| 1 | January | 300 |

| 2 | February | 290 |

| 3 | March | 259 |

| 4 | April | 315 |

| 5 | May | 341 |

| 6 | June | 309 |

| 7 | July | 289 |

| 8 | August | 330 |

| 9 | September | 323 |

| 10 | October | 296 |

| 11 | November | 302 |

| 12 | December | 206 |

As a result, the income amounted to:

- for the 1st quarter - 849,000 rubles;

- for the six months - 1,814,000 rubles;

- for 9 months - 2,756,000 rubles;

- for a calendar year - RUB 3,560,000.

Amounts paid for hired workers to extra-budgetary funds were:

- for the 1st quarter - 22,000 rubles;

- for half a year - 41,000 rubles;

- for 9 months - 65,000 rubles;

- for the whole year - 89,000 rubles.

In addition, the company paid sick leave in the second quarter in the amount of RUB 19,000. The organization is subject to the obligation to pay a trade fee, the amounts of which are:

- for the 1st quarter - 8,000 rubles;

- for half a year - 17,000 rubles;

- for 9 months - 24,000 rubles;

- for the whole year - 38,000 rubles.

Tax calculation simplified tax system Income 6%:

Example 3

Initial data:

1. Individual entrepreneur with no employees. 2. Taxation system of the simplified tax system “income”. 3. Tax rate 6%. 4. Income:

- 1st quarter - 150,000;

- half-year - 350,000;

- nine months - 550,000;

- twelve months - 800,000.

Payment of fixed insurance contributions for oneself was made in equal parts, based on the fact that fixed contributions for 2019 are determined within the following limits: for pension insurance 29,354 rubles; for medical insurance 6,884 rubles. Payments were made within the following terms:

- until March 31 - 9059.50 rubles;

- until June 30 - 9059.50 rubles;

- until September 30 - 9059.50 rubles;

- until December 31 - 9059.50 rubles.

Example of calculating the simplified tax system Income:

Advance payment of the simplified tax system for the 1st quarter:

150,000 × 6% - 9059.50 = - 59.50 rubles, therefore, there is no need to pay an advance payment for the 1st quarter of 2021;

Advance payment of the simplified tax system for the six months:

(350,000×6%) - (9059.50 + 9059.50) = 2881 rubles.

Advance payment of the simplified tax system for nine months:

550,000 × 6% - (9059.50 + 9059.50+ 9059.50) - (2881) = 2941.00 rubles.

Payment of simplified tax system for the year:

800,000 × 6% - (9059.50 + 9059.50+ 9059.50+ 9059.50) - (2881+ 2941.00) = 5940 rubles.

If the amount of tax payable was in kopecks, then it would be necessary to round the resulting amount: a tax amount of less than 50 kopecks is discarded, and a tax amount of 50 kopecks or more is rounded to the full ruble.

Since the individual entrepreneur received an annual income of 500,000 rubles and thereby exceeded 300,000 rubles, he is obliged to pay an additional 1% of the excess amount to the Pension Fund. Such a payment must be made before July 1 of the year following the reporting year, but can be made in the current year, thereby immediately reducing the advance payments by the amount paid.

Example 4:

The initial data are the same as in example 3. i.e. at the end of nine months, the income amounted to 550,000 rubles.

(550,000 - 300,000) X 1% = 2,500.00 rubles.

If the individual entrepreneur pays this amount before September 30, then the advance payment for 9 months will be:

550,000 × 6% - (9059.50 + 9059.50 + 9059.50) - (2941.00 + 2500.00) = 380.50 rubles. In this case, the amount of the advance payment must be rounded and paid 381 rubles.

The advance payment will be reduced by 2,500 rubles due to an additional contribution to the Pension Fund in the amount of 1% of the difference in excess income and 300,000 rubles.

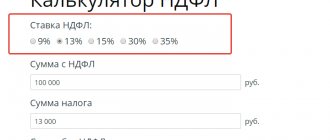

The simplified taxation system rate is the main advantage

The differentiated rate is considered a big advantage of the “simplified” system. This is a kind of additional bonus provided in a preferential tax regime. The base rate is fifteen percent. But local authorities have the authority to reduce it to five percent. Thus, for 2021, representatives of the regional board reduced rates in 71 settlements.

At the local level, a decision on the rate for the simplified tax system is made every year until it comes into force. You can find out what rate is in effect in a particular region of Russia from the local administration or tax service. We emphasize that the reduced rate is not a special benefit that requires confirmation - its application is the same for all entrepreneurs working under the simplified tax system in the region.

Important point! For 2017-2021, for the subjects of Crimea, the rate can be reduced to three percent. The laws of the constituent entities of Russia also state that individual entrepreneurs engaged in scientific or socially significant work, or providing household services for the population, can count on a zero rate. At the same time, there are a number of obligations: the share of profitability from activities for which a 0% rate is applied must be at least seventy percent. An individual entrepreneur can apply a zero rate from the moment of registration until December 31 of the same year.

Example of calculating the simplified tax system Income minus expenses 15%

The procedure for calculating advance payments and tax under the simplified tax system “Income minus expenses” is similar to the previous example, except for the following points:

- expenses must be justified in accordance with Article 346.17 of the Tax Code of the Russian Federation;

- Expenses are recognized on a cash basis, except for expenses when paying for the cost of goods. Such expenses are taken into account as goods are sold (clause 2.2 of Article 346.17 of the Tax Code of the Russian Federation);

- on the last day of the reporting period, expenses for the acquisition of fixed assets are recorded.

- the simplified tax system tax is not reduced by insurance premiums, since they are taken into account in expenses;

- when calculating the additional 1% contribution to the Pension Fund, the tax base is only income, expenses are not taken into account;

- the obligation to pay a minimum income of 1% in the event of a loss or in the case when the accrued tax of the simplified tax system for the year is less than the minimum.

- The tax base at the end of the reporting period is subject to reduction by losses received in previous periods.

Who can apply

The application of a preferential tax system assumes that it is available only to those business entities that meet the criteria for its application established by the Tax Code of the Russian Federation:

- The main criterion for using the simplified tax system is the average number of employees of a business entity, which cannot exceed 100 people.

- In addition, the amount of income received per year is taken into account. To switch to the simplified tax system, the entity’s revenue for 9 months should not exceed 112.5 million rubles. A taxpayer loses the right to preferential treatment if his annual income exceeds 150 million rubles.

- The residual value of fixed assets is also taken into account, which should not exceed 150 million rubles, the share in the authorized capital of the simplified entity per legal entity cannot be more than 25%, and the organization should not have branches.

Attention! If they do not comply with them, the subject loses the right to preferential treatment. That is, the simplified tax system for income is available to entrepreneurs and organizations classified as small businesses.

This might also be useful:

- What taxes does the individual entrepreneur pay?

- simplified tax system for individual entrepreneurs in 2021

- Tax system: what to choose?

- Tax calendar for 2021

- What reporting must an individual entrepreneur submit?

- Fixed payments for individual entrepreneurs in 2021 for themselves

Is the information useful? Tell your friends and colleagues

Dear readers! The materials on the TBis.ru website are devoted to typical ways to resolve tax and legal issues, but each case is unique.

If you want to find out how to solve your specific issue, please contact the online consultant form. It's fast and free!