A situation often arises that, for various reasons, you did not have time to make changes to the Accounting Policies before the beginning of the year. Or they deliberately didn’t. I wanted to think about it better, remember all the changes - and modify it later. But it is important to take into account that with continuous numbering of orders for conducting financial and economic activities, the order approving changes to the accounting policy for 2021 must be dated exactly 2021.

What is accounting policy

Accounting policy is a document establishing methods and methods for conducting tax and accounting of a company.

Deviation from the approved version is possible only if changes are made in a timely manner. All accounting entities formulate the policy independently.

That is, all legal entities write accounting policies for taxes and accounting. For individual entrepreneurs, the task is simpler: if they don’t do accounting, then they don’t need an accounting policy, but they still have to create a tax policy.

And more useful for an accountant

How not to be responsible for someone else's mistake

On July 26, 2021, an addition was made to the accounting law that all employees of the organization are required to comply with the requirements of the chief accountant (or the person responsible for accounting) regarding the execution and submission of primary accounting documents.

The accountant must submit a request to eliminate the identified violation or the need to submit certain information to the accounting department in writing to the employee.

In the accounting policy for 2021, the accountant should use this opportunity: fix this condition, approve the form (form) of the chief accountant’s written request to the employee, prescribe the procedure for issuing such requirements, the deadlines for their implementation, responsibility and other conditions.

All documents and information go to the accounting department!

In 2021, to be honest, I was surprised by the negative judicial practice, which confirmed the legality of holding an accountant liable for failure to record primary documents on new objects and operations that he did not even know about. True, the decision of the Krasnoyarsk Regional Court No. 7Р-116/2019 dated March 14, 2019 concerns a budgetary organization, but every accountant should take precautions.

To do this, it is worthwhile to prescribe in the accounting policy - in addition to the company's existing document flow regulations - the procedure for the company's employees to notify the chief accountant of all transactions with new accounting objects: forms of accounting documents, deadlines for their submission and responsibility.

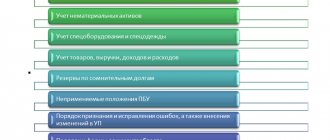

About the closed list of accounting registers

In the accounting policy, it is advisable to approve a closed list of accounting registers for accounting. Which can be - at your discretion - concise and short. And consist, for example, of the general ledger, sales ledger, purchase ledger and balance sheets for accounting accounts (list them).

This can be a great help in not having to submit a ton of documents for the unlimited demands of the tax authorities.

Taking into account the provisions of the accounting policy, tax authorities can request only those accounting and tax registers that are maintained in the prescribed manner. This is what the state tax policy regulator, the Ministry of Finance, thinks so (letter dated May 11, 2010 No. 03-02-07/1-228).

You should not indicate in your accounting policy a link only to the accounting program: 1C or other software packages. You understand that a great variety of accounting forms and transcripts can be generated and downloaded from the database according to any requests of the inspectors. Save your time.

Innovations in PBU

Please note the updated versions of PBU 13/2000, PBU 16/02 and PBU 18/02 and the FSBU standard 25/2018 “Lease Accounting”.

FAS 25/2018 comes into force in 2022, but if the company decides to apply it ahead of schedule from 2021, this should be stated in the accounting policy for accounting.

About the annual report

Pay attention to the new accounting forms. And according to the order of the Ministry of Finance dated April 19, 2021 No. 61n.

Lines about the audit of the annual reports have been added to the balance sheet - if the audit of the annual report is mandatory for the company, a check mark is placed and information about the auditor is indicated.

In the balance sheet and financial results report, you cannot indicate data in millions of rubles, but only in thousands of rubles.

Updated financial reporting forms are applied starting with reporting for 2021. But the company has the right to decide to use them earlier, consolidating changes in accounting policies.

Starting from 2021, annual reports do not need to be submitted to Rosstat. If this condition was specified in the accounting policy, it should be excluded in the new edition.

When can you make changes?

According to the approved policy, the company operates from year to year. The legislator does not allow changes to be made at will. It is allowed to edit the document in clause 10 of PBU 1/2008 only in the following cases.

- Changes in legislation . Everything is simple here - the UE cannot contradict the law. Therefore, if changes have occurred in the field of accounting, for example, a new act has come into force, then change the company’s policy in a timely manner.

- The company has developed a new way of accounting . An important point is that changes made to the policy should improve the quality of information about the company’s activities.

- Working conditions have changed . This could be a change in the main activity, merger, acquisition, division of the company, and so on.

Amendments to the policy occur on the basis of an order signed by the head of the organization. The order is written in free form.

Get acquainted with a sample accounting policy for LLCs and individual entrepreneurs on UTII and OSNO in the cloud service for small businesses Kontur.Accounting!

Get free access for 14 days

Rules for accounting and payment of taxes for separate divisions

If a company has created several separate divisions located in one region, then the accounting policy establishes the procedure for paying taxes to the regional budget from two possible options:

- Each department independently.

- Centrally - through the parent company or through a responsible division.

The accounting policy lists the separate divisions to which the right of representation is delegated, indicating the taxes in respect of which the specified division will perform duties - submit tax returns and pay taxes.

If, from January 1, 2021, such a procedure was prescribed in the accounting policy and you do not plan to change it, there is no need to make changes. But with regard to the centralized payment of personal income tax and insurance premiums, there are innovations that need to be included in the accounting policy for 2020.

Innovations from 2021:

- From January 1, 2021, it is officially allowed to submit 2-NDFL and 6-NDFL reports and transfer personal income tax in a single payment for all separate divisions located within the same municipality (within one OKTMO).

- From January 1, 2021, the company has the right to grant the authority to transfer insurance premiums only to those separate divisions that have a bank account.

Don’t forget to notify the tax authority about the centralized procedure for paying taxes, submitting reports and choosing a responsible department. Please note that regarding the centralization of personal income tax, only the selected inspectorate should be notified - the rest of the Federal Tax Service will receive information automatically. Each Federal Tax Service is notified regarding insurance premiums, in which the “separate” ones are registered. Messages are sent either about the vesting or deprivation of powers of the corresponding separate unit.

From what period do the changes take effect?

The changes are effective from the beginning of the reporting year. If the editing is caused by a change in accounting legislation, the changes take effect from the date of entry into force of the relevant law.

If the changes had a significant impact on the company's finances, account for them retrospectively. We will have to evaluate what the result would have been if the company had applied the new accounting policies from the beginning of its operations. In practice, retrospective accounting is an adjustment of retained earnings and other balance sheet items to the earliest date in the financial statements if this can be done reliably. If reliability cannot be ensured, apply the new accounting policies from the date the amendments are introduced.

Results

Current changes to the accounting policy for 2020-2021 can be made due to amendments to legislation that came into force during the year, as well as when the organization has new or substantially different types of activities from previously existing ones. Such changes are approved by order (instruction) of the manager, supplementing the accounting policy.

In addition, from 2021, changes will need to be made to the accounting policy if the previously used accounting algorithms have been adjusted by law since the beginning of the year or the organization independently decided to change the accounting rules applied.

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

How to reflect changes in accounting policies in accounting statements

Reflect all significant changes in the financial statements. To do this, write an explanatory note. Clause 21 PBU 1/2008 contains a list of information that needs to be reflected:

- reason for change;

- nature of changes;

- how changes are reflected in the reporting;

- the amount of adjustments as a result of changes in the CP.

If the policy has been revised due to legal requirements, then the consequences must be disclosed as specified in the relevant law.

How PBU 1/2008 details the process of making changes

PBU 1/2008 “Accounting policies of the organization” (approved by order of the Ministry of Finance of the Russian Federation dated October 6, 2008 No. 106n) explains the algorithms for making changes to the accounting policies in an expanded format - the regulation has a separate chapter for this, establishing:

- reasons for introducing changes (clause 10) - they fully correspond to those listed in art. 8 of Law No. 402-FZ;

- the requirement to justify the changes made (clause 11);

- registration requirements - changes are approved by order or directive of the manager;

- requirement for the date of amendments (clause 12) - it coincides with that specified in clause 7 of Art. 8 of Law No. 402-FZ;

- the requirement for a monetary assessment of the consequences of changes (clause 13) - it refers to changes that can significantly affect the financial position of the organization, the results of its activities and (or) cash flows;

- the need to reflect in accounting the consequences of changes in accounting policies (clauses 14, 15) in one of the specified ways: prospectively or retrospectively;

- scheme for describing in reporting the consequences of applying changes - changes that have had or are capable of having a significant impact on the financial performance of the organization are subject to separate disclosure.

In addition to the above requirements, Ch. III PBU 1/2008 contains important clarifications:

- about which accounting innovations are not considered changes - approval of accounting methods for facts of economic activity that appeared in the organization’s activities for the first time or differ in essence from those that took place previously (paragraph 5, clause 10);

- about when all changes can be reflected in the reporting prospectively - if the organization organizes accounting using simplified methods (clause 15.1).

For information about who is allowed to use simplified accounting, read the article “Features of accounting in small enterprises .

The considered requirements describe algorithms for changing accounting policies. However, they also need to be properly formalized. This is done by drawing up an order that supplements or changes the accounting policy.

What is the difference between addition and change?

When you make changes, you change the order in which you take into account those facts of life that already existed before. This entails changes in financial results, income, expenses and, therefore, the need for recalculation in retrospect.

Additions arise only for those transactions that you have not performed before. For example, the emergence of a new type of activity in addition to the old one. In this case, simply write down new provisions. There is no need to recalculate balance sheet items and determine the impact of adjustments on past dates.

When maintaining accounting and tax records, adhere to the developed accounting policies. This will help you defend your position in a dispute with the Federal Tax Service. In order not to deviate from your policy, use the cloud service Kontur.Accounting. The program can work with different methods of accounting and tax accounting. We give all newcomers a free trial period for 14 days.

If you switch to a different tax regime from the beginning of the year, you need to draw up a new accounting policy

When changing the object of taxation according to the "simplified" tax system - from "Income" to "Income minus expenses" and vice versa - the change must be made to the accounting policy for 2021.

In the event of a transition from UTII to “simplified” taxation, the accounting policy must specify the accepted methods and accounting procedures for the new taxation procedure - the simplified taxation system.

Innovation from 2021:

From January 1, 2021, sellers of three groups of goods subject to mandatory labeling will lose the right to use UTII and PSN: medicines, shoes, clothing and other products made from natural fur.

In return for UTII, small companies and individual entrepreneurs will consider the option of switching to the simplified tax system.

To switch to the simplified tax system, the current accounting policy will have to be revised. And it’s important: no later than December 31, 2021, do not forget to notify the tax authority by sending an application to switch to the simplified tax system using form No. 26-1. Otherwise, in 2021 you will have to pay taxes according to the general taxation system.

If part of the business is transferred to UTII or the opportunity to receive targeted financing opens up, the accounting policy needs to detail the procedure for maintaining separate accounting.

There are still many tax innovations that will come into effect on January 1, 2021. Eg:

- the obligation to restore VAT during reorganization if the successor applies a special regime or begins to use the received property, goods, work, services in non-VAT taxable activities;

- the obligation to use electronic forms of salary reporting 6-NDFL, 2-NDFL, calculation of insurance premiums for companies with a staff of 10 people or more;

- new deadlines and formats for submitting tax reports;

- deadlines for payment of advance payments for transport and land taxes established at the federal level, and others.

All these innovations are unambiguous norms for execution that do not allow for choice of actions or alternative judgments. Therefore, it is necessary to take them into account in the work, but it is not necessary to include them in the accounting policy.

Please note other provisions of existing accounting policies. It is possible that some of the elements have lost their relevance, while others do not take into account the changes that have occurred in the structure of the company or the peculiarities of doing business. Some accounting methods require simplification, while others require replacement to achieve optimal results.

This may concern:

- working chart of accounts;

- inventory procedure;

- methods for valuing assets and liabilities;

- list of direct expenses;

- methods of maintaining separate accounting, if such an obligation is provided;

- benefits for which you have the right to apply and other solutions for organizing accounting.

If you create reserves in accounting and tax accounting, do not forget to take inventory of them as of December 31, 2021. From January 1, 2021, you can refuse to form reserves for tax purposes by reflecting the decision made in your accounting policies.

In this issue, we discussed in detail the transition to a new inventory accounting standard from 01/01/2021. And as required by clause 10 of PBU 1/2008 “Accounting Policies”, it is necessary to make changes to the accounting policy, reflecting innovations and selected accounting methods reserves that will be used next year. I hope that during the New Year holidays everyone will work on the accounting policy, although it must be approved for 2021 before the end of 2021. What to consider?

We propose to begin by eliminating references to normative acts that have lost force and inserting the new FSBU 5/2019:

— PBU 5/01 (approved by order of the Ministry of Finance dated 06/09/2001 No. 44n);

— Guidelines for accounting of oil and gas production facilities (approved by order of the Ministry of Finance dated December 28, 2001 No. 119n);

— Guidelines for accounting of special tools, special devices, special equipment and special clothing” (approved by order of the Ministry of Finance dated December 26, 2002 No. 135n).

Next, you must decide on the method of transition to the new standard: prospective or retrospective (clause 47 of FSBU 5/2019) and also fix the specified method of transition.

In the accounting policy, it will be necessary to adjust the composition of inventories, the rules for their assessment upon recognition and subsequent assessment, taking into account the changes. For convenience, information to be reflected in the accounting policy in connection with the entry into force of the new FAS 5/2019 is presented in the table:

Table 1

| No. | Changes to the new FSBU that must be disclosed in the UP | The acceptable options that are most suitable for your accounting are reflected in the accounting policy | Link to regulations |

| 1 | Stationery and office supplies, other materials for administrative needs with a shelf life of no more than 12 months | 1) Do not take into account as assets; costs associated with their acquisition are included in the expenses of the period (account 26) in which they were incurred. Such assets include: - stationery; - etc. | clause 2 FSBU 5/2019, clause 7 PBU 1/2008 |

| 2) For internal control purposes, take into account as assets (account 10) with subsequent attribution to expenses. | |||

| 2 | Consequences of changes in accounting policies in connection with the start of application of FAS 5/2019 | 1) Promising 2) Retrospectively | clause 47 FSBU 5/2019 |

| 3 | Accounting for low-value fixed assets and special clothing (special equipment) for over 12 months | 1) Take into account expenses at a time, organize off-balance sheet accounting for control | clause 5 PBU 6/01, clause 5 FSBU 6/2020 (if a decision is made on its early application), PBU 1/2008 |

| 2) Take into account as part of fixed assets, calculate depreciation based on the useful life | clause 3 FSBU 5/2019 | ||

| 4 | Accounting for workwear (special equipment), service life up to 12 months | 1) Take into account as part of inventories and write off as expenses at the time of release into operation. | clause 3 FSBU 5/2019 |

| 5 | Accounting for expensive spare parts | 1) If spare parts are used in repair work that is carried out every 3 years, reflect it as part of non-current assets. | clause 3 FSBU 5/2019, Appendix to Letter dated January 29, 2014 No. 07-04-18/01 |

| 2) If spare parts are used in repair work once a year or more often, count them as part of inventories (account 10) regardless of their cost. | |||

| 3) If spare parts are used in repair work that is carried out every 3 years, reflect them as part of inventories (account 10), because such assets cannot perform independent functions and do not correspond to the concept of “inventory item of fixed assets”. | clause 6 PBU 6/01 | ||

| 4) If spare parts improve the quality characteristics of the vehicle/equipment, then it is allowed to reflect them as a modernization of a fixed asset with attribution to the increase in the cost of the item being repaired. | clauses 26, 27 PBU 6/01 | ||

| 6 | Accounting for building materials | 1) If an object is being built, which is subsequently accounted for as a fixed asset, then construction materials should be taken into account as part of non-current assets (account 08 with a separate analytical account). Reflect such assets in the balance sheet in the line “Other non-current assets”. | clause 3 FSBU 5/2019, Appendix to Letter dated January 29, 2014 No. 07-04-18/01 |

| 2) If an object is being built that is intended for sale/transfer, then construction materials are taken into account as part of inventories, because the constructed facility will be used during one operating cycle. | clause 3 FSBU 5/2019 | ||

| 7 | Accounting for parts, spare parts or scrap metal received from write-off/disassembly/liquidation | 1) If in relation to the received (extracted) materials a decision has been made to sell and the sale of similar material assets is not part of the organization’s normal operating cycle, upon termination of a certain type of activity, reflect it as long-term assets for sale. In the balance sheet, reflect it as part of the line “Other current assets”. | clause 10.1 PBU 16/02, Information message of the Ministry of Finance of Russia dated 07/09/2019 No. IS-accounting-19 |

| 2) Parts, spare parts or scrap metal received from write-off/disassembly/liquidation, used further for the repair of other equipment, for their sale, should be reflected as part of inventories. In the balance sheet, reflect it as part of the “Inventories” line | clause 16 FSBU 5/2019 | ||

| 8 | Valuation of finished goods and work in progress upon recognition | 1) Administrative expenses (not directly related to production) should not be included in the actual cost of work in progress and finished products. Use the Direct Costing cost accounting method. Reflect administrative expenses by writing off directly to the debit of subaccount 90-8 “Administrative expenses” from credit 26 of account. | clause 18 FSBU 5/2019 |

| 2) The cost does not include excess consumption of raw materials, losses from defects and downtime, violations of labor and technological discipline. Such costs should be written off immediately to the cost of sales of the reporting period (Dt 90 Kt 28). The cost does not include storage costs; such costs should be reflected in current production costs or sales costs (except for storage costs that are directly related to the production process) | clause 26 FSBU 5/2019 | ||

| 9. | Method for assessing finished products and work in progress upon recognition | Select one of the assessment methods: | clause 24, FSBU 5/2019 |

| 1) Approve the valuation method at full cost. | |||

| 2) Approve the valuation method at standard cost using account 40 “Product output”. The difference between the actual cost and the cost of planned (standard) costs should be included in the cost of sales in the reporting period in which this difference is identified. | |||

| 3) Approve the method of assessment based on the amount of direct costs without taking into account indirect ones. Direct costs include: - raw materials and materials, - wages of main production workers and deductions from it, — depreciation of fixed assets. Indirect costs include general production costs (account 25). | |||

| 4) Measure own-produced agricultural, forestry and fishery products, as well as commodities at initial recognition and subsequent valuation at fair value | Clause 19 FSBU 5/2019, IFRS 13 “Fair value measurement”) | ||

| 10. | Valuation of goods in retail trade | 1) Purchased goods are valued at their selling price with separate consideration of markups. | clause 20 FSBU 5/2019 |

| 2) Purchased goods should be valued at actual cost. | |||

| 3) The costs of procurement and delivery of goods should be included in sales expenses (account 44). | clause 21 FSBU 5/2019 | ||

| 4) Costs of procurement and delivery of goods are included in the cost of goods sold. | |||

| 11. | Valuation of inventories after recognition | 1) When determining the valuation of inventories at the reporting date in the case of using the net sales indicator of inventories, use their estimated price minus the estimated costs of production, preparation for sale and sale of inventories - this is a value equal to the share of inventories of the estimated price at which the organization can sell similar inventories as of the reporting date or the price at which similar inventories can be purchased as of the reporting date (the lower of these values). | clauses 28, 29 FSBU 5/2019 |

| 12. | Valuation when releasing inventories into production | Select one of the assessment methods: | clause 36 FSBU 5/2019 |

| 1) at the cost of each unit; | |||

| 2) at the average cost, determined at regular intervals (specify the interval: month, quarter, etc.) or as each new batch of inventory arrives | |||

| 3) at the cost of the first units received in time (FIFO method) | |||

| 13. | Provision for impairment of inventories | Every year, when conducting an inventory of inventories, evaluate them and create a reserve (account 14), which is equal to the amount of excess of the actual cost of inventories over their net selling value. The creation of a reserve should be reflected: Dt 90-2 Kt 14, restoration of the reserve: Dt 14 Kt 90-2. | clause 30-32 FSBU 5/2019 |

| Valuate inventories at the reporting date at cost (applicable if the organization uses simplified accounting methods, as well as non-profit organizations). |

All other innovations according to FAS 5/2019 are mandatory for use (unless, of course, you are a micro-enterprise) without the right to choose one of the methods fixed in the accounting policy. Therefore, you do not need to rewrite the entire new inventory standard into your accounting policy; all provisions are defined in this regulatory act. We include in our accounting policy only one of the accounting options proposed by the FSB.

To change the accounting policy, you need an order from the manager (clause 8 of PBU 1/2008). Changed accounting methods can be applied only from the beginning of the new year (clause 10, PBU 1/2008).

| Order on amendments to the accounting policies of Rassvet JSC ORDER on changes to accounting policies 28.12.2020 | № 309 |

- The following changes should be made to the accounting policy for accounting purposes, approved on December 27, 2019:

1) references to the Guidelines for accounting for workwear and equipment (No. 119n and No. 135n), PBU 5/01 should be removed according to the text. Lost power. For inventory accounting, provide links to FSBU 5/2019.

2) determine a promising method of transition to FSBU 5/2019.

3) the inventory intended for administrative needs, written off at a time as expenses, includes: stationery and office supplies, office equipment (clause 16 of the Accounting Policy).

4) construction materials intended for the construction of industrial buildings subsequently used in the organization’s activities should be reflected in a separate analytical account to subaccount 08-3, reflected in the balance sheet as part of the line “Other non-current assets” (clause 17 of the Accounting Policy).

5) determine the method for determining the cost of finished products based on direct costs. Direct costs include:…….. (clause 20 of the Accounting Policy).

6) do not include administrative expenses in the cost of finished products, use the “Direct Costing” method, write off account 26 “General expenses” to subaccount 90-8 “Administrative expenses” (clause 30 of the Accounting Policy).

6) etc...

The change in accounting policy will apply from 01/01/2021.

General Director Sergeev A.A. signature

Be sure to write in great detail about accounting for insurance premiums.

This is not true, but something will still have to be written down in the accounting policy. Undoubtedly, the most important change of 2021 is that insurance premiums will now be administered by the Federal Tax Service instead of the Pension Fund and the Social Insurance Fund. We are talking about two federal laws dated July 3, 2016: No. 243-FZ and No. 250-FZ.

Read also “Limits and base for insurance premiums for 2021”

The only thing that must be written down in the accounting policy is to approve the form of an individual accounting card for the amounts of accrued payments and other remunerations and the amounts of accrued insurance premiums. Now everyone uses the card form given in the joint letter of the Pension Fund of Russia, the Federal Insurance Fund of Russia dated December 9, 2014 No. AD-30-26/16030, 17-03-10/08/47380. The Tax Service does not plan to develop a form of the card. They say that this is a regular tax register, which each company can maintain in its own way. That is, everything is similar to personal income tax - once there was a form 1-NDFL, then it was canceled and taxpayers began to use a new register, using 1-NDFL as a basis.

Clause 4 of Article 431 of the Tax Code of the Russian Federation obliges to keep records of the amounts of accrued payments of insurance premiums and other remunerations, the amounts of insurance premiums related to them in relation to each individual recipient of payments. Therefore, it is necessary to supplement the accounting policy by issuing an order.

Read also “The accounting policies of organizations are being prepared for changes”

Sample order to make additions to the accounting policy for accounting and taxation purposes

You can take as a basis the same register that was recommended by the Pension Fund and the Social Insurance Fund. During inspections, tax officials, if necessary, will also require accounting cards from companies. For absence - a fine of 200 rubles for each register (Article 126 of the Tax Code of the Russian Federation).

One more thing. If your company does not practice types of work that affect the length of service for early retirement and are subject to pension contributions at additional rates, the card can be reduced. Leave only the sections about payments and insurance coverage.