20.11.2020

After capitalization, materials are transferred for use in production, for management purposes, for capital construction, for use in the socio-cultural sphere. Accounting for such transactions is not easy.

Firstly, a huge nomenclature appears. Secondly, prices are constantly changing. There are many other factors. Therefore, accounting for materials that are transferred to their destination requires the use of special methods.

Each company has the right to independently determine the method of accounting and writing off materials as costs. The chosen method must be recorded in the company’s accounting policy (both for accounting and taxation).

Let's look at three common methods:

- write-off of costs at average cost;

- write-off at unit cost of inventory;

- FIFO method.

Deferred expenses: what exactly do we reflect on the balance sheet?

Accounting should reflect the value of assets - funds over which an organization gains control as a result of its activities, in anticipation of financial or other benefits. This is how this term is clarified by the Concept of Accounting of the Russian Federation, adopted by the Methodological Council on Accounting under the Ministry of Finance of the Russian Federation, by the Presidential Council of the IPB RF on December 29, 1997.

When is an inventory of deferred expenses ?

The cost of an asset is made up of the funds spent on its acquisition, creation, introduction into production, etc. All these costs fall on the balance sheet in the reporting period when they were documented (recognized), even if they were not actually paid at that time (clause 18 of PBU 10/99 “Organizational expenses”).

Question: How are the costs of insuring property (including leased and rented property) reflected in accounting and tax accounting if the insurance premium is qualified by the organization as a deferred expense? View answer

However, the law allows for certain assets to be prescribed in accounting regulations the conditions under which certain costs for them are reflected and written off according to rules other than the general ones. Nevertheless, they are included in the cost of assets in the same way, it’s just that this inclusion will not take place at the time of payment, but later. Naturally, they cannot be reflected on the balance sheet at the time of payment, because the profit from their investment will appear in other accounting periods and must be written off gradually and evenly over the entire life of such an asset. Therefore, these costs are classified as deferred expenses .

DEFINITION: RBP is expenses incurred in one reporting period and included in the cost of assets in subsequent periods of the organization's business, necessary to make a profit in the future. Their difference from other company costs exists solely in accounting.

Conveniences of BPO for accountants

In many cases, it is more expedient to defer certain types of expenses to future periods than to recognize them in the current period. Accountants love this type of accounting for several reasons, sometimes deliberately using it not entirely correctly, because it is convenient.

- Is it possible to reflect expenses for voluntary medical insurance as part of deferred expenses?

- There is no need to be afraid of large sums in current expenses . For example, a company purchased expensive equipment or made costly repairs. Even if this money can be written off immediately, this will worsen the reporting, because the profit, if it eventually turns out, cannot be shown immediately.

- BPOs allow you to “hide” losses. Even justified financial losses are unpleasant signals for tax inspectors who select “victims” for an on-site audit. Therefore, accountants sometimes resort to lesser violations by reflecting “unprofitable” items of current expenses on this account, although this is incorrect.

- It is easier to combine accounting with tax accounting. There are situations that can affect discrepancies in these types of accounting, for example, a fixed asset was sold before its service life expired, resulting in a loss. It cannot be written off immediately, because there is still a certain time before the end of its useful life, during which the resulting loss must be reflected. It is easier to enter funds from the sale of fixed assets not into “Other income and expenses”, but into “RBP” and write them off simultaneously with tax accounting, although this is not entirely legal.

- Simple write-off. If the accounting policy allows for a uniform write-off of funds to the BPO, this can be introduced as an automatic function, which reduces the accountant’s work and reduces the possibility of errors.

IMPORTANT! For the purpose of reasonable classification and prevention of accounting violations of the RBP, the Ministry of Finance has provided for a clear identification of this type of expense.

How to distinguish RBP from other expenses

Working in a particular industry, an accountant takes into account the specific specifics of the organization's expenses. Taking into account the nuances, he can determine the criteria by which certain expenses should be included in the BPR. These criteria are recorded in the accounting policies.

The first step is to properly separate regular expenses from assets, which by definition are BPOs.

Signs of an asset:

- Accountability and control of the organization.

- Focus on future benefits:

- use separately or together with other assets to carry out the main activities of the organization;

- exchange for another asset;

- used to satisfy an obligation;

- distributed among business owners.

The second step is to allocate deferred expenses among assets according to the definitions given in the accounting policies. Examples of RBP - investments made before the profit from them can be capitalized, and therefore reflected in the reporting period:

- costs for planning and preparation of construction work;

- purchasing licensed software;

- funds spent on product certification, licensing, obtaining a patent;

- purchasing voluntary insurance policies (medical, property, transport);

- funds for promotions that are still ongoing;

- finances for the launch of new capacities, development of equipment;

- land reclamation costs;

- funds spent out of season (for seasonal production);

- expenses for moving branches to other locations;

- money for vehicle inspections;

- bank guarantee fee;

- payment of rent;

- other expenses that are written off gradually.

IMPORTANT! The first two points of classifying assets as RBP are determined by PBU, and the rest are supplemented by the Tax Code of the Russian Federation.

Advance payments issued, including subscriptions to periodicals, as well as amounts paid as vacation pay, are not included in the RBP

What is remarkable about the FIFO method?

The FIFO (first in - first out) method is based on the assumption that the use of an enterprise’s material resources is carried out over a period of time in the sequence in which they are acquired (i.e., received by the enterprise). Thus, the resources that entered production first must be valued on the basis of the cost of those that were acquired first in time, taking into account the cost of those inventories that are listed at the beginning of the period.

This method is suitable for:

- wholesale companies;

- industrial enterprises;

- logistics companies.

But for trading, the FIFO method is not suitable, since it does not allow creating an accurate estimate of the cost of individual types of goods.

When costs are written off using this method, each newly received batch of material must be reflected in accounting as a separate category, regardless of whether the same materials are already in accounting.

In other words, this method is based on the assumption that those materials that were in the batch that arrived at the warehouse earlier than others were released for production purposes.

In the event that the amount of material contained in the 1st batch is less than the amount of material consumed, the material of the 2nd batch should be written off, etc.

There are two ways to calculate the price of materials that have been written off for production purposes.

- Standard. Incoming and outgoing materials are calculated, and unused materials are taken into account once at the end of the month.

- Modified. Calculations are carried out in reverse order. First, the balance of materials at a certain point in time is determined at the price of the most recent acquisition, and then the cost of inventories written off for production is calculated.

The standard FIFO calculation model is quite labor-intensive in cases where materials are purchased frequently during the month.

Cost restrictions

Not any costs are accepted for reduction, but only those directly named in Art. 346.16 Tax Code of the Russian Federation. In particular, it is allowed to write off as expenses under the simplified tax system:

- cost of goods and materials, stationery;

- labor and travel expenses;

- insurance premiums;

- expenses for the acquisition and repair of fixed assets;

- rental payments;

- R&D expenses;

- costs for notary, legal, accounting and auditing services;

- interest on loans and borrowings;

- fare;

- KKM maintenance;

- amounts spent on property protection and fire safety;

- expenses for communication services, postal services;

- tax payments, with the exception of VAT charged to counterparties and the single tax under the simplified tax system.

In 2021, the list of expenses was supplemented (Federal Law No. 121-FZ dated April 22, 2020) - from January 1, 2020, you can take into account expenses for disinfection of premises, purchase of equipment, special clothing, and other personal/collective protective equipment in connection with the implementation of sanitary -hygienic requirements of the authorities to combat coronavirus (clause 39, clause 1, article 346.16 of the Tax Code of the Russian Federation).

Conditions for writing off expenses: simplified tax system “income minus expenses”

The procedure for recognizing costs during “simplification” is described in Art. 346.17 Tax Code of the Russian Federation. A necessary condition for any operation is actual payment of expenses. Some types of expenses have additional requirements. Let's take a closer look at them.

By fixed assets

The cost of fixed assets acquired during the period of application of the simplified system is included in expenses under the simplified tax system from the moment they are put into operation (clause 3 of article 346.16 of the Tax Code of the Russian Federation). The company can expense the cost of such OS until the end of the year in which it was purchased. Write-offs occur in equal shares based on the number of reporting periods remaining until the end of the year. For example, the company will completely write off fixed assets worth RUB 110,000 purchased in July 2021 in the third and fourth quarters of 2021 (RUB 55,000 for each quarter).

If the fixed assets were acquired before the transition from a different taxation system, accounting is carried out at the residual value of the object as of the date of the change of regime. At the same time, the write-off of expenses under the simplified tax system “income minus expenses” depends on the useful life of the property:

- less than 3 years - during the first year of operation;

- from 3 to 15 years – half of the cost is written off in the first year, 30% in the 2nd year of operation, 20% in the 3rd year of use;

- 15 years or more - in equal shares over 10 years.

Costs are distributed in equal shares over the write-off period.

Example

The cafe has been applying the simplified tax system of 15% since the beginning of 2021. In October 2021, the cafe purchased a dishwasher. Its residual value as of January 1, 2020 was 120,000 rubles. The service life of the equipment is 6 years. How will accounting write off acquisition costs:

- in 2021, expenses will take into account 50% of the residual value of the dishwasher (RUB 60,000), i.e. 15,000 rubles each. in each quarter (RUB 120,000 x 50% / 4 quarters);

- for 2021, 36,000 rubles will be written off, 9,000 rubles each. for the quarter (RUB 120,000 x 30% / Q4);

- in 2022, the cost of the operating system will be written off completely - the annual amount of expenses will be 24,000 rubles, quarterly - 6,000 rubles. (RUB 120,000 x 20% / Q4).

In the case of the sale of fixed assets within the first 3 years from the date of accounting for expenses (for fixed assets with a service life of 15 years or more when sold within the first 10 years), the tax base for past periods before the date of sale is adjusted, the amount of accrued depreciation is included in expenses excluded. The cost of fixed assets is included in the costs on the day of sale of the object. An additional amount of tax and penalties will be paid.

Write-off of goods purchased for sale

To account for the cost of goods, it is important not only the date of their receipt and payment to the supplier, but also the moment of their sale, since the costs of purchasing goods are written off as they are sold to customers (clause 2, clause 2, article 346.17 of the Tax Code of the Russian Federation).

That is, writing off expenses of the simplified tax system is possible provided that:

- the goods have been received;

- settlement with the supplier has been made;

- the goods are sold to the buyer.

Transport and other costs associated with the sale of goods are taken into account after actual payment.

The company chooses the method of accounting for goods (FIFO, average cost, per unit cost) independently. Acceptance for accounting occurs without taking into account VAT paid to the supplier.

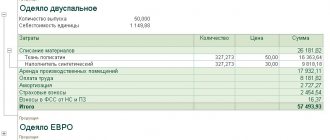

How to write off materials at average cost

Most companies use average cost to release materials into production.

Here's a short algorithm:

- Reflect the adopted method in the accounting policy. Please note the required criteria.

- the average cost write-off method must be applied to all types and/or groups of inventory defined by the policy;

- the principle of sequence of application must be observed.

- The following parameters must be met:

- operational analytics should make it possible to clearly identify types and groups of inventory items;

- the procedure for capitalization and actual release into production should make it possible to accurately determine the amount of accepted or written off inventories in established units of measurement;

- Accounting accounts must promptly reflect the cost of each batch of inventory.

- weighted assessment - cost calculation is made for a specified period (usually a month); Moreover, during the period, the write-off of raw materials and materials for production occurs only in quantitative terms;

- rolling estimate - the average cost is determined for each batch of inventory released into production; in this case, accounting is carried out in two dimensions at once - quantitative and cost based on the average cost.

The average cost is determined for each type of material, calculating it by dividing the total cost of a given type of material by their quantity.

General formula for calculating average cost (ACst):

СSt = Total cost of the type (group) of inventory / Quantity of inventory by type (in the group).