Two main approaches to cost planning

In planning the costs of production and sales of products, the classification of costs is of paramount importance:

- into variables (or direct) - the size of which depends on the volume of output and, accordingly, on the volume of sold output. Examples include:

- raw materials and supplies included in a specific type of product;

- wages of production personnel;

- rental and leasing payments for production equipment and premises;

- some taxes included in the cost, such as property tax;

- expenses for maintaining management personnel.

Note! Conditionally fixed costs are often distributed among the cost of finished products. In this case, a dependence arises: the larger the output volume, the smaller the share of indirect costs in the cost of production. The higher will be the enterprise profit indicator obtained from accounting records.

From the above relationship, prerequisites arise for distinguishing two methods of cost planning - based on the principle of maneuvering the values of fixed costs:

- the direct cost method (or the “direct costing” method) - which takes into account only variable costs as part of the production cost (in this case, indirect costs are applied directly to the financial results, without distribution);

- full cost method - which consists of summing up all costs incurred in the cost of production.

Accounting for production costs

To display information about expenses incurred by an enterprise in accounting, several active synthetic accounts are used:

- account 20 – costs associated with the production of products by the main workshops;

- account 21, reflecting the valuation of produced semi-finished products;

- Account 23 accumulates costs broken down by operating auxiliary workshops;

- Account 25 is intended for general production expenses;

- Account 26 indicates the amount of overhead costs.

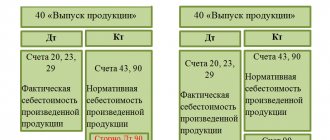

Product defects detected during the production process are included in account 28, and the costs of service facilities are collected in account 29. The costs of selling products are displayed in the debit of account 44. Accumulation of expenses is carried out in the debit of these accounts, write-off to cost is carried out by credit turnover.

Nuances of the partial (direct) cost method

Advantages of the method

Accounting only for direct costs allows for operational analysis and planning in the following areas:

- dependence of cost on production volume;

- the dependence of marginal income on production volume and the impact of margin on the company’s final profit (marginal income or simply margin - a specific indicator for the partial cost method - is the difference between gross revenue from product sales and the direct costs of its production);

- identifying the relationship between the final profit and the amount of direct or indirect costs in relation to established sales prices and assortment;

- determining the break-even point of production projects;

- determining the maximum possible production costs at a given profitability level.

To summarize, we can say that the partial cost method provides extensive information for making management decisions. In particular, it allows you to effectively manage pricing and assortment policies, as well as production volumes of various product groups.

Disadvantages of the method

The main disadvantage is the difficulty in correctly classifying costs into variable and fixed in relation to a specific enterprise. In practice, this can be quite difficult to accomplish. For example, a type of cost such as electricity costs:

- on the one hand, when production volumes change, the final amount of energy consumed will almost always change - that is, according to this criterion, such costs should be classified as variable;

- on the other hand, electricity can be spent on lighting and heating production premises, on the operation of electronic measuring equipment, etc. - that is, the amount of energy consumed for these purposes does not particularly depend on the volume of products currently being produced in these premises, and it would be more logical to classify the costs of this electricity as constant.

Another disadvantage of the direct cost method is considered to be the more complex organization of accounting. Often, the use of the method leads to the parallel existence of financial and management accounting (i.e., it leads to an increase in the costs of maintaining the accounting apparatus). In addition, even if there is no division into financial accounting and management, the preparation of a report on financial results for the period still takes place in several stages (calculation of direct costs, calculation and write-off of indirect costs, classification and attribution to financial results of other expenses that are accounted for separately, etc. .d.).

Analysis of cost dynamics in production costs

This type of analysis involves comparing accounting data for several periods. With regard to costs, the report on financial results is analyzed first. Based on which aspect they want to study in more depth, the analysis of financial results and costs can be:

- Vertical - when the revenue indicator on the financial results report is taken as 100%, and then for each expense item reflected in the report, the percentage of revenue is determined. The analysis allows you to determine how the components of costs change over time and depending on sales volumes.

Example

LLC Metalkonstruktsii from the previous example plans to purchase new equipment on lease. The payment amount per year will be 4,000,000 rubles. The volume of production using existing equipment is 10,000,000 rubles. With the introduction of new equipment, the volume can be increased:

- in the 1st year 1.5 times;

- in the 2nd year 2 times.

The planned indicators (excerpt from the forecast report) will be as follows:

| Report Indicators | This year | 1st year of leasing | 2nd year of leasing | |||

| Absolute indicator (thousand rubles) | Relative rate (%) | Absolute indicator (thousand rubles) | Relative rate (%) | Absolute indicator (thousand rubles) | Relative rate (%) | |

| Revenue | 15 000 | 100 | 22 500 | 100 | 30 000 | 100 |

| Cost price | 10 000 | 66,67 | 15 000 | 66,67 | 19 500 | 65 |

| Leasing payments | — | — | 4 000 | 17,78 | 4 000 | 13,33 |

From this vertical comparison we can see:

- With an increase in the volume of production on new equipment, the share of expenses for leasing payments in revenue will decrease.

- Full utilization of new equipment will lead to a reduction in production costs. However, this will not happen immediately, but only after adapting the technology and reaching maximum utilization of new production capacities.

What can be included in the cost, see the article “What costs does the commercial cost of production include?”

- Horizontal - when the dynamics of each item in the financial results report is monitored over several periods. Horizontal analysis is usually complementary to vertical analysis.

Example (continued)

In a horizontal view, the excerpt from the forecast report of Metallokonstruktsii LLC that we have already discussed will look like this:

| Report Indicators | This year | 1st year of leasing | 2nd year of leasing | |||

| Absolute indicator (thousand rubles) | Relative rate (%) | Absolute indicator (thousand rubles) | Relative rate (%) | Absolute indicator (thousand rubles) | Relative rate (%) | |

| Revenue | 15 000 | 100 | 22 500 | 150 | 30 000 | 200 |

| Cost price | 10 000 | 100 | 15 000 | 150 | 19 500 | 195 |

| Leasing payments | — | — | 4 000 | 100 | 4 000 | 100 |

Interestingly, the conclusions regarding changes in cost as a result of the introduction of new equipment and an increase in output will be approximately the same as in the vertical analysis: using the maximum capacity of the new equipment will lead to a reduction in production costs.

But with regard to changes in the share of leasing payments in the total cost, a horizontal analysis will not show the nuances.

Nuances of the full cost method

Advantages of the method

- The ability to determine how, as production volume increases, the share of fixed costs in production costs decreases.

- The ability to manage the indicator of indirect costs by maneuvering output volumes and, as a result, the ability to influence the profit indicator, which will be reflected in the reporting.

- The full cost method, when applied in practice, insures against a situation where selling prices ultimately do not cover all production costs (which sometimes happens with an unplanned increase in fixed costs when using “direct costing”).

Disadvantages of the method

In contrast to the direct cost method, the method of fully including costs in the cost price can negatively affect management decisions made on its basis.

Example

The enterprise produces the main product A. Additionally, it was decided to launch the production of product B, which is approximately comparable in characteristics to product A. At the same time, when planning and making additions to the accounting policy, such a procedure was formed for the distribution of overhead and management costs that most of them began to relate to product B .

IMPORTANT! The enterprise determines the method of distribution of fixed expenses independently and records it in its accounting policies.

As a result, a situation was artificially created:

Unit cost A = 1000 (direct costs) + 300 (indirect costs) = 1,300.

The company applies a 50% markup. That is, the selling price of unit A = 1300 × 1.5 = 1,950.

Unit cost B = 900 (direct costs) + 600 (indirect costs) = 1500.

Selling price of unit B = 2,250.

Thus, as a result of an incorrectly chosen method of allocating costs by type of product, instead of a working alternative to product A, we received a product with similar characteristics, but 300 rubles more expensive. Will they buy such a product? Unlikely. Most likely, all work on the release of product B will only bring losses to the enterprise.

This example also demonstrates the second negative aspect of the full cost method - the difficulty of effective pricing. In this case, setting the selling price will be a multi-stage process. Thus, in order to avoid getting into trouble with product B, the enterprise managers should have made all the calculations for allocating costs to cost and determining the markup before product B was actually put into production.

The cost of production is all the costs of an enterprise for the production and sale of products.

Cost is a necessary component in determining the profit of an enterprise. The amount of profit depends on the amount of costs for the production of a given type of product and on current selling prices and represents the difference between the price at which the product is sold and the costs of its production, i.e. cost [p.48] Price is the monetary expression of value products. Therefore, it includes all elements of social production costs. This allows all normally operating enterprises to reimburse the costs of production and sales of products and make a profit for the formation of economic incentive funds. The price level depends to a decisive extent on the cost price, i.e. on the enterprise’s expenses for the production and sale of products (at its own share - [p.263] Revenue from the sale of products, works, services is the main source of cash receipts for enterprises, its composition and structure . Gross income, cash savings and profit of enterprises. The economic nature of profit, its types (profit from sales, gross, balance sheet, taxable, net) and factors influencing its value. The role of profit in the development of enterprises, its planning, distribution and use. Costs enterprises for the production and sale of products (works, services). Cost elements included in the cost of products (works, services). Financial planning at enterprises (business plan, estimates). [p.487]

The cost of production, one of the most important qualitative indicators of enterprise performance, represents the costs of enterprises expressed in monetary terms for the production and sale of products. Cost is part of the cost of production. The latter, as is known, in a socialist society consists of the following parts of the value of the consumed means of production, the value created by necessary labor, and the value created by surplus labor. The first two parts of the cost of the product, expressed in monetary terms, are the basis of the cost of production. The cost of surplus product (product for society) in modern conditions of self-financing of enterprises is included in the cost of production in some part. Specifically, this is expressed in the fact that the cost of production includes contributions for social insurance, taxes and fees and other payments. Therefore, and also due to the fact that current prices for means and objects of labor do not always coincide with their value, and wages with the cost of the necessary product, the cost may not quantitatively coincide with the cost of the consumed means of production and the necessary product. [p.295]

The cost of production is the sum of the current costs of the enterprise for the production and sale of products. When comparing options, you should use the full cost, including the cost of transporting products to places of consumption. The comparability of the production cost indicator of different options is very important. [p.85]

Cost is the monetary costs of an enterprise for the production and sale of products; it shows how much the products it produces (or the work performed) cost and includes the following costs [p.249]

The cost of production represents the costs of an enterprise for the production and sale of products and services, expressed in monetary terms. It includes the costs of consumed raw materials, main and auxiliary materials, energy, catalysts, reagents, depreciation of fixed assets and labor. Costs incurred directly at the enterprise for the production of products and services constitute the production cost of production. [p.131]

The cost of production is part of the social costs of production, i.e., the cost representing the monetary costs of an enterprise for the production and sale of products. Value and cost represent a dialectical unity of the whole and the part without cost there is no value and vice versa (Diagram 2). [p.53]

Price is the monetary expression of the cost of a product. Therefore, the price structure includes all elements of social production costs (C + V + t). This price structure allows all normally operating enterprises to reimburse the costs of production and sales of products (C + F) and make a profit for the formation of economic incentive funds. The price level depends to a decisive extent on cost, i.e., on the enterprise’s costs for the production and sale of products (the share of cost in the price of industrial products is 80%, in the wholesale price of oil - more than 50%). Hence, the most important way to reduce prices is to reduce production costs. [p.54]

The long-term lower price limit shows what minimum price can be set to cover the full costs of the enterprise for the production and sale of products. This limit corresponds to the full cost of production. [p.233]

Variable costs are the costs of an enterprise for the production and sale of products, the volume of which varies in proportion to the change in the volume of production. [p.439]

Costs of production and sales of products - the costs of an enterprise for the production and sale of products constitute the full cost of production. [p.439]

The current costs of the enterprise for the production and sale of products constitute the cost of production. In the process of analysis, the cost of commercial products, the cost of a unit of production, and the specific cost of commercial products are studied. Retrospective cost analysis allows us to identify and measure the influence of both external factors that influence the formation of costs and factors caused by changes in organization and production technology. [p.351]

The cost indicator, representing the enterprise's costs for the production and sale of products, belongs to the group of qualitative indicators of economic activity. Reducing costs is the most important source of profit growth. It ensures increased production efficiency and helps improve the quality of production work. Currently, in the conditions of enterprises operating on economic accounting and self-financing, the cost indicator and its analysis should be given special attention. [p.101]

ESTIMATE OF COSTS (costs) - grouping of the enterprise's upcoming planned costs for the production and sale of products (works, services) according to economically homogeneous cost items, taking into account changes in work in progress balances, capital construction costs, etc. for a certain calendar period. [p.204]

Cost of production is the costs of an enterprise expressed in monetary terms for the production and sale of products. There are total and unit costs. Full cost is the total cost of the entire volume of production. Unit cost is the cost per unit of production (cost per unit of production). [p.406]

The cost indicator represents the enterprise's costs expressed in monetary terms for the production and sale of products (works, services). The cost level reflects economic, scientific, technical, social and environmental factors of the enterprise's development. [p.90]

GROSS SALES - the total revenue of an enterprise from sales of products. Includes the equivalent of the enterprise’s material costs for the production and sale of products and gross income (gross income). [p.40]

The cost of production represents the current costs of enterprises expressed in monetary terms for the production and sale of products (works, services). [p.6]

COST, gross costs, the totality of the current costs of an enterprise expressed in monetary form for the production and sale of products, works or services. The main elements in the production of goods are the costs of raw materials, basic materials, energy resources, wages received from outside (main and additional), social insurance contributions, depreciation charges and other expenses. In addition to the listed costs associated directly with the production process, the cost also includes non-production costs for containers, packaging and transportation [p.258]

CLASSIFICATION OF PRODUCTION COSTS - grouping of enterprise costs for production and sales of products. Based on various characteristics, costs are divided into basic and overhead, direct and indirect, semi-fixed and variable. In planning and accounting for product costs, the main role is played by the grouping of expenses by economic elements and by costing items. All costs that are homogeneous in economic content are grouped into elements, regardless of the place where they are produced (workshop, plant management, warehouse, etc.), regardless of the cost object (manufacture of products in the main production or costs in auxiliary and service industries). In planning and accounting on this basis, eight groups (elements) of costs are distinguished: raw materials and basic materials, auxiliary materials, external fuel, external electricity, depreciation of fixed assets, wages, basic and additional, social insurance contributions, other expenses. This grouping is used to develop production cost estimates that reflect the overall [p.104]

COST ESTIMATE - a complete set of enterprise costs for the production and sale of products for a certain calendar period (year, quarter), compiled according to the economic elements of expenses. S. z. compiled according to standard elements: raw materials and basic materials, returnable waste (subtracted) auxiliary materials, fuel and energy from the side, wages, basic and additional contributions to social security, other expenses. S. z. It is calculated by direct summation of individual economic elements and estimates of complex expenses or estimates of individual divisions of enterprises; it excludes secondary accounting of self-made products for one’s own production needs. In N. z. takes into account the costs of changing the balances of work in progress, capital construction, capital re- [p.295]

Statistics, using accounting data, characterize the level of all costs of enterprises for the production and sale of products, called the full cost of production, as well as costs associated with production and called factory, or production, cost, and costs due to the sale of products and representing distribution costs in branches of circulation and non-production expenses in industry. These data are studied both for the enterprise (organization) and industry as a whole, and for the most important groups and types of products. [p.147]

CLASSIFICATION OF PRODUCTION COSTS - grouping of enterprise costs for production and sales of products. According to various criteria, costs are divided into basic and overhead, direct and indirect, semi-fixed and variable. [p.102]

PRODUCT COST—expressed in monetary terms, the current costs of an enterprise for the production and sale of products. S. p. is a synthetic, generalizing indicator that reflects all aspects of the production and economic activities of an enterprise and characterizes the efficiency of its work. Planning, accounting, and analysis of cost accounting are one of the most important conditions for the implementation of effective economic accounting at enterprises. The cost of production includes the cost of consumed means of production (costs of raw materials, semi-finished products, fuel, energy, costs associated with the operation and depreciation of fixed production assets), expenses for remuneration of employees of the enterprise, and social insurance contributions. The structure of industrial costs is characterized by the relationship between individual types of costs and reflects the specific features of each industry. Thus, in the oil industry, the most significant costs are for labor and depreciation of fixed production assets; in the light and food industries, 85-90% are the costs of raw materials and supplies, with a small share of labor costs. As a result of scientific and technological progress in all industries, the share of material costs increases and the share of labor costs decreases. All production costs of an enterprise are determined by production [p.287]

COST ESTIMATE - a complete set of enterprise costs for production and sales. products for a certain calendar period (year, quarter), compiled according to the economic elements of expenses. S. z. compiled according to standard elements: raw materials and basic materials, returnable waste (subtracted) auxiliary [p.293]

The enterprise's costs for the production and sale of products do not cover its entire cost. The full cost of a product is determined by the costs of both materialized and living labor, including labor for society. [p.265]

Cost expresses the cash costs of an enterprise for the production and sale of products; it shows how much it costs the company to manufacture and sell products. [p.218]

The full (self-supporting) cost of the product cx represents the sum of the enterprise’s costs for the production and sale of products. It can be expressed by the formula [p.121]

PROFITABILITY is one of the performance indicators of the main self-supporting units of socialist social production. The economic nature of profitability is determined by the dominant type of production relations. Under capitalism, profit (see capitalist profit) is the main driving force and goal of production. Under socialism, making a profit cannot serve as the goal of production. Here profit (see Profit of socialist enterprises) is an important source of expansion of production, satisfaction of the growing needs of members of society, formation of reserves and insurance stocks. Profitability is determined by the ratio of profit to the enterprise's costs for the production and sale of products and the ratio of profit to the cost of fixed production assets and standardized working capital. In the first case, the degree of efficiency of current production costs is characterized, in the second - the efficiency of using production assets. When determining the profitability of an enterprise, they use the overall profitability indicator as the ratio of balance sheet profit (i.e., profit from pea-[p.369]

The cost of industrial products is the current costs of an enterprise for the production and sale of products, expressed in monetary terms. The cost of production includes the cost of means and labor consumed in the production process (depreciation, cost of raw materials, materials, fuel, energy, etc.), part of the cost of living labor (wages), the cost of purchased products and semi-finished products, costs of production services third party organizations. Many of these costs can be planned and taken into account in kind, i.e. in kilograms, meters, pieces, etc. However, in order to calculate the amount of all expenses of the enterprise, they need to be brought to a single meter, i.e. presented in monetary terms expression. [p.189]

Currently, the production cost plan is not approved by higher authorities. But this does not mean that the cost indicator loses its significance. Not a single enterprise can do without planning and cost analysis if it wants to run its business economically, since reducing the enterprise’s costs for production and sales of products is the main way to increase profits and increase profitability. [p.166]

The use of the product cost indicator in the context of the transition to a market economy is of especially great practical importance. One of the most important tasks of successful management is to increase the economic efficiency of production. Savings in the costs of living and embodied labor for production in monetary terms affects the reduction of production costs. The cost of production is a general indicator that reflects in monetary terms all the costs of enterprises for the production and sale of products. In connection with scientific and technological progress, the level and structure of production costs are changing. In the practice of managing the cost of production, as well as to identify reserves for its reduction, it is necessary to know the composition and share of individual expenses in the cost of production, the nature of their changes in connection with technical progress. The study of the influence of technical progress on the cost of production and its individual components is of great theoretical and practical importance. [p.7]

The enterprise's expenses for the production and sale of products in cash form the cost of production. These are expenses for consumed means of production, wages of collective farmers (workers and employees) with accruals, expenses for servicing production, and others. Cost planning is the main condition for carrying out economic calculations. There are planned and reported production costs, as well as individual and industry costs. [p.231]

D enterprise costs for production and sales of products [p.137]

When manufacturing a particular product or performing a particular job, money is spent on materials, semi-finished products, components, fuel and energy, on wages for workers of various categories, professions and qualifications, on reimbursement of costs, maintenance and operation of equipment, fixtures and tools , for preparation and development of production. The monetary costs of an enterprise for the production and sale of products or the performance of work are called cost. [p.251]

FULL COST - the totality of all enterprise costs for the production and sale of products. [p.546]

The cost of production is the current costs of an enterprise expressed in monetary terms for the production and sale of products. [p.199]

Total cost is the totality in monetary form of all the enterprise’s costs for the production and sale of products. In contrast to factory cost in P. s. non-production expenses are included. P.S. also called k o m m e r ch e-s k o i. [p.104]

Total cost is the totality in monetary form of all the enterprise’s costs for the production and sale of products. In P. s. non-production expenses are included. P.S. also called commercial. [p.134]

The cost of industrial products is the current costs of an enterprise for the production and sale of products, expressed in monetary terms. The cost of production reflects the cost of means and objects of labor consumed in the production process (depreciation, cost of raw materials, materials, fuel, energy, etc.), part of the cost of living labor (wages), the cost of purchased products and semi-finished products, production services third party organizations. [p.272]

Cost is the sum of the enterprise's costs for the production and sale of products, expressed in monetary terms. Although the cost of production is not included in the number of policy indicators, it retains its importance as one of the most important indicators characterizing the organizational and technical level of the enterprise and the quality of its production and economic activities. [p.222]

The cost of industrial products is the current costs of an enterprise for the production and sale of products, expressed in monetary form. The cost reflects the cost of means and objects of labor consumed in the production process (depreciation, cost of raw materials, materials, fuel, energy, etc.), the cost of living labor (wages), the cost of purchased products and semi-finished products, production services of third-party organizations [ 14, p. 193]. The total cost of production reflects the total costs of production resources, while the unit cost (the cost per 1 ruble of production) reflects the efficiency of resource use. Cost is the main pricing and profit-generating factor, therefore cost analysis allows, on the one hand, to give a general assessment of the efficiency of resource use, and on the other, to determine reserves for increasing profits and reducing unit prices. [p.315]

COST (ost) is the monetary expression of the enterprise’s costs for the production and sale of products. C. of products (works, services) includes costs associated with the direct production of products, costs associated with the use of natural raw materials, costs for preparation and development of production, costs associated with the improvement, modernization of technologies and production, costs for servicing the production process, costs for ensuring normal conditions labor and safety costs associated with production management costs of training and retraining of personnel costs of creating insurance funds and reserves costs of paying interest on loans received costs associated with the sale of products depreciation deductions taxes, fees and other mandatory deductions and payments. S. also includes a number of other enterprise costs. [p.213]

Full cost (commercial). The totality of all costs of an enterprise for the production and sale of products, expressed in monetary form. It also includes non-production expenses. [p.186]

Results

Planning costs for production and sales of products is always preceded by the choice of the main planning method. Both methods, traditionally used in production and sales management, have both their pros and cons. Determining a suitable method and its correct application is a subjective expert choice of enterprise management.

Read more about cost classifications from a management perspective: “Classification of costs in management accounting (nuances).”

For more information about variable and fixed costs, see: “What costs does the workshop cost of production include?”

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.