When an employee is sent on a business trip, the employer guarantees not only the preservation of his job and average earnings, but also reimbursement of expenses associated with the business trip, which include daily allowances. Per diem can be defined as the employer's financing of additional daily expenses of an employee associated with temporary residence in another location. According to the Tax Code, personal income tax is not withheld from daily allowances if they are paid within the limits established by Article 217 of the Tax Code of the Russian Federation. And according to what standards should daily allowances be subject to insurance premiums? To understand this issue, we should consider the current provisions of the law, as well as the upcoming changes in the new year.

When daily allowances in excess of the norm are subject to insurance contributions, what are these norms for employers, and also what new is expected in 2017 in connection with the entry into force of new provisions of tax legislation regarding the taxation of daily allowances for business trips in Russia and abroad - about all this in our article.

Determining limits

So, the current legislation does not establish a maximum size of SR. However, officials have determined a certain limit, above which daily allowances in excess of the norm are subject to insurance premiums (2018).

IMPORTANT!

The daily allowance for business trips is set for each company individually. The management of the organization sets limits based on their financial capabilities.

Article 217 of the Tax Code establishes that excess daily allowances are subject to insurance contributions (2018). Also, personal income tax will have to be withheld from amounts exceeding the limit. The limits are set as follows:

- for trips within Russia - 700 rubles per day;

- for foreign business trips - 2500 rubles per day.

In other words, if an institution has established large values for this type of expense, then the amount exceeding the limit is subject to taxation (personal income tax and personal income tax). Please note that this limit only applies to taxation. The company has the right to establish a CP greater than specified in Art. 217 Tax Code of the Russian Federation.

Using a specific example, we will determine whether daily allowances are subject to personal income tax and insurance premiums.

Primerov Ivan Andreevich was sent to Moscow for 10 calendar days. 43,000 rubles were allocated for travel expenses, including:

- 5000 rub. - to pay for travel;

- 18,000 rub. — for rental housing (payment for a hotel room);

- 20,000 rub. - SR (2000 rubles per day, therefore, daily allowances over 700 rubles, insurance premiums will have to be charged).

Amounts allocated for travel and accommodation are not subject to taxes. But above-limit daily allowances are subject to insurance premiums. Let's do the calculation:

- We determine the amount of excess (2000 rubles – 700 rubles) × 10 days. = 13,000 rub.

- We calculate personal income tax: 13,000 × 13% = 1,690 rubles.

- We determine the amount of SV: 13,000 × 30.2% (OPS - 22%, compulsory medical insurance - 5.1%, VNIM - 2.9%, NS and PZ - 0.2%) = 3926 rubles.

Consequently, Examples will receive 41,310 (5000 + 18,000 + (20,000 – 1690)) rubles. And the company’s expenses will amount to 46,926 (43,000 + 3926) rubles.

IMPORTANT!

The SR limit that the company has established should be fixed by a separate order or special order of the company management. It is also permissible to stipulate in a local document the key rules for sending specialists on business trips.

Please note that one-day business trips and daily allowances (insurance contributions) are no exception. You will still have to withhold personal income tax on the excess and pay the contribution tax to the budget.

Use of personal transport by a business traveler

An employee can also go on a business trip in his own car. In order not to impose contributions on compensation related to the exploitation of an employee’s property, several conditions must be met (letter of the Ministry of Finance dated March 28, 2019 No. 03-15-06/21254):

- The types of expenses subject to compensation are prescribed in the collective agreement, for example: for the purchase of fuels and lubricants, repair of a vehicle during a business trip.

- The employee agrees with the employer on the fact of going on a business trip in a personal car.

- Expenses are supported by documents.

Useful information about compensation:

- for unused vacation without dismissal;

- personal car without personal income tax and contributions;

- rental housing for an employee;

- delay of wages.

How are daily personal income tax and insurance premiums assessed?

The taxation procedure for SRs exceeding those established in Art. 217 of the Tax Code of the Russian Federation, the general one applies. For personal income tax, the rate is set at 13%. Let us remind you that not the entire amount is taxed, but only the difference exceeding the permissible limit.

The amount of insurance coverage is determined individually. This means that if a company has benefits and applies reduced rates for SV, then in order to tax daily allowances above the norm, insurance premiums for 2021 will be calculated at reduced rates. We described in more detail what benefits are valid in 2021 in a special article “Who is entitled to reduced SV tariffs in 2021”.

For example, a company operates in the field of IT technologies and has the right to reduced insurance rates:

- OPS - 8%;

- Compulsory medical insurance - 4%;

- VNiM - 2%;

- NS and PZ - 0.2%.

According to the conditions of the example given above, the company will pay to the budget not 3,926 rubles (13,000 × 30.2%), but only 1,846 rubles (13,000 × 14.2% (8% + 4% + 2% + 0.2% Therefore, insurance premiums for excess daily allowances are calculated and paid at preferential rates if the company has a legal right to them.

note

In 2021, insurance premiums must continue to be accrued for payments under employment agreements and civil contracts. This is regulated by Article 420 of the Tax Code of the Russian Federation. But quite often the question arises: are daily allowances subject to insurance premiums?

Payments that are not subject to contributions have not changed in 2021. They are recorded in Article 422 of the Tax Code. At the same time, in 2021, daily allowances for the Social Insurance Fund for industrial injuries are not subject to insurance premiums. Any amount of such daily allowance is free from such contributions.

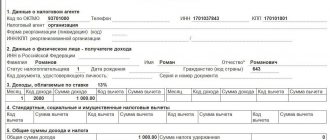

Daily allowances based on insurance premiums 2021

Many accountants wonder whether per diem is correctly reflected in the calculation of insurance premiums? Tax officials gave an official explanation that not only SR, but also all amounts of travel expenses should be included in the calculation of SV.

So, when filling out the report, indicate the entire amount that was accrued to the posted employee. Don't forget to include travel, accommodation and other expenses. Enter travel expenses in line 030 of subsection number 1.1 of Appendix No. 1 to Section No. 1 of the SV report.

The amount that is not subject to taxation is indicated in line 040 of subsection 1.1, Appendix No. 1 of the first section.

Therefore, line 050 will indicate the taxable difference.

Lines 030, 040 and 050 of subsection 1.2 of Appendix No. 1 of the first section should be completed in the same way. And also lines 020 and 030 of Appendix No. 2 to the first section. Such recommendations are presented in the Letter of the Federal Tax Service dated 08.08.2017 No. GD-4-11/15569.

The information will also have to be detailed in the third section of the DAM. Namely, in part 3.2.1 of the third section, reflect the daily allowance in the report on insurance premiums as follows:

Additional services on the train

The cost of travel to and from the business trip may include the cost of service. For example, when purchasing a ticket for a luxury carriage on long-distance trains (clause 33 of the Rules for the provision of services, approved by Decree of the Government of the Russian Federation dated March 2, 2005 No. 111).

The composition of the range of services is determined by the carrier. In each train, taking into account the schedule and the duration of the passengers' stay on the route, it may vary. Paid services include: provision of guaranteed food, printed materials, sets of sanitary and hygienic items (Order of the Ministry of Transport dated July 9, 2007 No. 89).

Compensation for the cost of paid services included in the ticket price is not included in the contribution base, since the cost of such services forms the single cost of travel on the train (letter of the Ministry of Finance dated 08/07/2017 No. 03-04-06/50386).

Let's sum it up

So, we have identified the following important points:

- The CP limit is set by the organization independently.

- The norms must be enshrined in the order.

- If the CP per day exceeds 700 rubles. for trips around Russia and 2500 rubles. per day for business trips abroad, then amounts exceeding the daily allowance for business trips are subject to insurance contributions.

- All travel expenses should be included in reporting, namely in the DAM.

Please note that if a company does not include travel expenses in the DAM report, then tax authorities do not have the right to issue a fine. However, this only applies to non-taxable amounts. It should also be noted that if the company has not included non-taxable business trips in the DAM, then it is advisable to provide an adjusting report. But if the adjustment is not provided, then the tax authorities cannot fine the company, since the tax base is not underestimated.

The concept of “per diem”

In situations where a company employee goes on a business trip in Russia or abroad, the employer undertakes to pay him a certain monetary remuneration, which is calculated per day - these are the so-called daily allowances. At the same time, there are only 3 main situations in which the employer is obliged to pay per diem. Firstly, these are business trips themselves. Secondly, business trips of employees in situations where the work is traveling in nature or occurs directly on the road. And thirdly, during expeditionary type work or in field conditions.

To study the issue more accurately, let’s look at how the law interprets business trips. A business trip is a business trip, the terms and conditions of which are determined by the employer. In this case, the place where the work will be carried out must be remote from the established one.

Per diems are not part of the housing payment when working remotely and are taken into account as additional expenses for the employee’s daily needs. As a rule, the further away the remote work location is, the greater the amount the employer pays.

Accounting for excess daily allowances. Example

Excessive daily allowances must be reflected in the accounting reports. They should indicate not only direct payments, but also insurance premiums (if any) and personal income tax. In order to consider this issue in detail, consider the following example.

An employee of the company goes on a business trip for 7 days across Russia. His daily allowance is 1,257 rubles, which exceeds the norm. Accordingly, in 7 days he will receive 8,799 rubles. How it will look in the accountant's spreadsheet:

| Number | Debit | Credit | Payment amount | the name of the operation | Execution date |

| 1 | 208.12 | 201.34 | 8799 | Issuance of cash payment from the cash desk for daily expenses | Daily allowance payment date |

| 2 | 401.20 | 208.12 | 8799 | The daily payment is reflected in expenses by the date of approval of the advance report | Date of approval of the advance report |

| 3 | 302.11 | 303.01 | 507 | Withholding personal income tax from the employee’s salary (8799 – 700*7) * 0.13 = 507 | Date of next salary payment |

These rules for indicating expenses and payments made are specified in the Instructions for the Application of Budget Accounting Charts, which was approved by the Russian Ministry of Finance in 2010. According to this instruction, the debit of the corresponding analytical accounting account should be displayed, and the credit of the account for increasing accounts payable for taxes established on the income of an individual.

conclusions

The employer is obliged to pay employees the amounts guaranteed by the legislation of the Russian Federation. Any payments to employees not directly established by the legislation of the Russian Federation or constituent entities of the Russian Federation, for the purpose of their economic justification, must be secured by an internal document of the bank: a collective agreement, an employment contract or other local document approved by the head of the bank.

And, of course, in order to minimize the risks of additional assessment of insurance premiums and personal income tax by supervisory authorities, it is necessary to train (conduct consultations, draw up memos, instructions, etc.) employees in the correct execution of primary documents confirming expenses incurred. First of all, this concerns travel expenses, and especially expenses associated with foreign business trips, where the composition of documents issued to confirm payment may differ significantly from those accepted in Russia.

Sources

- https://nalog-nalog.ru/strahovye_vznosy/nachislenie_strahovyh_vznosov/oblagayutsya_li_komandirovochnye_strahovymi_vznosami/

- https://online-buhuchet.ru/sutochnye-sverx-normy-dokumentalnoe-oformlenie-nalogooblozhenie-straxovye-vznosy/

- https://nalog-nalog.ru/ndfl/uderzhanie_ndfl/platim_ndfl_s_komandirovochnyh_rashodov/

- https://online-buhuchet.ru/oblagayutsya-li-sverxnormativnye-sutochnye-straxovymi-vznosami/

- https://glavbuhx.ru/strahovie-vznosi/vznosi-na-travmatizm/sutochnye-sverh-normy-vznosy-na-travmatizm.html

- https://online-buhuchet.ru/oblagayutsya-li-komandirovochnye-strahovymi-vznosami/

- https://WiseEconomist.ru/poleznoe/82229-straxovye-vznosy-ndfl-vyplate-srednego-zarabotka-komandirovochnyx

The legislative framework

Within the framework of this issue, it makes sense to mention two codes at once - Labor and Tax. Both of them contain general or detailed information about excess daily allowance and how this payment is subject to insurance premiums. The following table will help to clearly consider this issue:

| Code | Information about excess daily allowances |

| Labor Code | 1. According to Art. 168, the employer is obliged to reimburse the employee’s expenses related to living outside his place of permanent residence. 2. The employer can independently determine the amount of daily allowance, fixing it in a local regulation or in a collective agreement. 3. A business trip is work carried out by an employee for a specified period outside the place of work and involving residence in a place remote from his permanent home. If the work officially involves traveling, then such a trip is not considered a business trip. At the same time, while on a business trip, an employee cannot lose the established salary or lose his job: his working conditions must remain the same throughout the entire period of the business trip. |

| tax code | 1. Daily allowances that exceed the norm established by the Government do not make the income tax base smaller (Article 264). 2. Article No. 217 limits the amount of daily allowance paid to an employee, which is not taxed. 3. Compensation payments established by local, regional, district, and federal legislation, the amount of which does not exceed the norms established by law, are completely exempt from taxation (Article 217). 4. Article No. 226 specifies the procedure for withholding personal income tax from daily allowances, which it is recommended that the accountant adhere to. |

In addition, it is important to refer to two decrees of the Government of the Russian Federation that address the issue of daily allowances. The first of them, No. 93, contains information about the rate of daily allowance paid and some of their features. Second, No. 729 includes the amount of reimbursement of travel expenses within budgetary organizations.

Recommendations and answers to pressing questions

Let's consider a number of frequently asked questions that often arise both among company employees and financiers. These questions relate to payments of daily allowance and excess daily allowance, as well as their features:

- When assessing daily income tax with personal income tax, it is recommended to act according to the following algorithm. First, an advance report is received from the employee, then the amount subject to tax is calculated, then personal income tax is calculated and, finally, personal income tax is withheld from the salary.

- To ensure that problems do not arise within the company, as well as during its interaction with organizations such as the Pension Fund or the Social Insurance Fund, it is recommended that the rules for calculating daily allowances and insurance premiums be established in local documents. It is best to fix the rules in a collective labor agreement.

- Not only insurance premiums, but also personal income tax are not charged on the established daily allowance rates. This feature must be taken into account by accountants when working.

To legally work with daily payments in favor of employees, it is necessary to carefully monitor the updating of the current legislative framework, as well as monitor the company’s local documents and their content. At the same time, it is recommended to sometimes consult professional tax employees about documentation, who will help resolve existing shortcomings and avoid problems with various inspections.