- home

- Reference

- Insurance premiums

Every officially employed person has the right to annual leave. It is fully paid for by the employer, so the citizen receives money three days before the start of the vacation in connection with going on vacation.

Vacation pay, like regular earnings, is subject to personal income tax and insurance contributions. This takes into account special rules and regulations that the company’s accountant should be aware of.

Rules for calculating insurance premiums from vacation payments

The employee's annual leave period (standard - 28 days) is paid in full based on the average daily earnings for the last 12 calendar months.

From each accrual, the employer makes contributions to various authorities. Income tax on vacation pay is withheld directly from labor remuneration and transferred to the Federal Tax Service. All other contributions are paid from the company’s funds in the following proportions of income:

- for the formation of pension provision – 22%;

- for social insurance – 2.9%;

- for compulsory health insurance – 5.1%;

- insurance for injuries and occupational diseases – from 0.2%.

In addition to annual paid leave, other types of leave are also subject to payment of contributions. But there are exceptions.

When is it necessary to pay personal income tax on vacation pay?

In 6-NDFL, this tax must be included in full for the month in which the payment was made. Example of retention Example conditions: The employee is entitled to regular leave from March 27 to April 15, 2021 inclusive (20 calendar days).

Articles on the topic (click to view)

- Fine for late payment of vacation pay

- What to do with unused vacation

- What to do if your employer does not pay vacation pay

- How long after employment is vacation allowed?

- Is maternity leave taken into account when calculating pensions?

- Accounting for compensation for unused vacation

- Dismissal while on maternity leave

- Date of actual receipt of income - .

- Personal income tax withholding date - .

- The transfer deadline is (since the last day of March is Saturday).

Useful video About the deadlines for paying personal income tax and insurance contributions from vacation pay, see the video: Conclusions The employer is required to withhold 13 percent of the tax from accrued vacation pay and pay it to the tax office.

What are the fees?

Are vacation pay taxable? Since vacation pay is part of earnings, the employer must include it in the calculation base and when calculating insurance premiums . If he evades this duty, he will be subject to penalties.

Expert opinion

Polyakov Pyotr Borisovich

Lawyer with 6 years of experience. Specialization: civil law. More than 3 years of experience in drafting contracts.

The amount of vacation pay will be: 1365.2 rubles. x 14 = 38225.6 rub. 13% of this amount is 4969.3 rubles, which must be transferred to pay personal income tax.

You will learn about the deadlines for personal income tax payment in the following video:

Contributions to the Pension Fund, FFOMS and Social Insurance Fund

Is the holiday subject to insurance contributions?

Along with income tax, the employer is required to pay insurance contributions to the following organizations:

- Pension Fund.

- Social Insurance Fund.

- Compulsory health insurance fund.

Funds must be paid by the 15th of the following month . If the vacation is taken out in August, contributions from vacation pay are transferred until mid-September.

How are insurance premiums calculated from vacation pay?

At the legislative level, regulation of the mechanism for calculating and subsequent payment of insurance premiums is carried out in chapters. 34 NK.

In accordance with paragraph 1 of stat.

420 taxable objects include various types of payments to individuals within the framework of existing labor and civil law relationships. Vacation pay is subject to insurance contributions in the general manner, since it is provided to personnel under the terms of concluded employment contracts.

Amounts not subject to insurance premiums

Insurance premiums are required to be calculated on the following types of vacation pay:

- Annual basic rest - this type of leave is entitled to all employees without exception. The total duration is 28 days (calendar) per year, the right to rest for newly hired specialists arises after six months of employment with the employer (stat. 115, 122 of the Labor Code).

- Additional basic rest - such periods are issued and paid to the employee for employment in certain working conditions. For example, for working in harmful or dangerous production, at irregular hours, etc. (stat. 116, 321 TC).

- Other vacations - the employer, at its discretion, has the right to establish other types of vacation for employees that are not specified in labor legislation. The exact regulations should be approved by the company’s LNA.

This is important to know: How many days before the vacation is the application written?

There is no requirement to charge insurance premiums on the following types of vacation pay:

- Medical leave for referral to sanatorium-resort institutions - such leave is granted to employees who have a work-related injury or occupational disease (Clause 1, Article 8 of Law No. 125-FZ).

Insurance premiums for vacation pay and compensation - examples of calculations

Let's look at how the above regulatory rules work in practice. Let’s assume that the manager of a trading company, S.V. Krivonosov, goes on annual leave with a total duration of 28 days (calendar) from April 2 to April 29, 2021. Let’s calculate the amount of vacation payments and accrued contributions by type of insurance:

- For the billing period, the accountant will take the period from 04/01/17 to 03/31/18. The period was worked by the employee in full, there are no excluded days.

- The total amount of earnings during this time is RUB 570,000.00.

- Let's determine the employee's earnings for one day - SDZ = 570,000.00 / 12 / 29.3 = 1621.16 rubles.

- Let's calculate the amount of vacation payments - OTP = 1621.16 rubles. x 28 days = 45,392.48 rub.

We will calculate insurance premiums taking into account the fact that the company applies general (not preferential) rates. The calculation of deductions was carried out in terms of pension, social and medical insurance, as well as “injuries”. Wiring – typical:

- Contributions from vacation payments to OPS were accrued - 45,392.48 rubles. x 22% = 9986.35 rubles, wiring - D 44 K 69.2.

- Contributions from vacation payments to OSS were accrued - 45,392.48 rubles. x 2.9% = 1316.38 rubles, wiring - D 44 K 69.1.

- Contributions from vacation payments for compulsory medical insurance were accrued - 45,392.48 rubles. x 5.1% = 2315.02 rubles, wiring - D 44 K 69.3.

- Contributions to NS and PZ from vacation pay were accrued - 45,392.48 rubles. x 0.2% (tariff assigned by the territorial branch of the Fund) = 90.78 rubles, posting - D 44 K 69.11.

How to calculate compensation if the employee did not take the leave required by the Labor Code? Let us assume that S.V. Krivonosov did not have time to use his vacation and quits on April 2. According to the norms of stat. 127 of the Labor Code, he is entitled to compensation payments for all unused days, that is, for 2021 and January-March 2021. In our example, this is 35 days. (28 days + 3 months x 2.33 days) The calculation is carried out according to the general rules for calculating vacation payments:

- Compensation amount = 35 days. x 1621.16 rub. (average daily earnings) = 56,740.60 rubles.

Note! When working less than 15 days. such a month is not taken into account, over 15 is taken into account. Insurance premiums are determined using the algorithm above.

Other deductions from vacation pay

In addition to income tax, contributions to the Pension Fund, Social Insurance Fund and Federal Compulsory Medical Insurance Fund are subject to accrual on vacation pay amounts. Insurance contributions from vacation pay are calculated in the month in which vacation pay is calculated and are payable no later than the 15th day of the month following the month of their accrual. For example, if an employee goes on vacation from May 1 and vacation pay is accrued in April, contributions must be paid no later than May 15. The amounts of insurance contributions to the Social Insurance Fund regarding insurance against accidents at work are subject to transfer simultaneously with the payment of wages in the month in which vacation pay is accrued. Insurance premiums from vacation pay in 2015 are calculated at the following rates (with the exception of preferential and increased rates):

Types of vacations not subject to insurance contributions

Vacation pay is not subject to insurance premiums in the following cases:

- additional rest for liquidators of the accident at the Chernobyl nuclear power plant or those affected by its consequences;

- leave for sanatorium-resort treatment in health institutions due to the consequences of injury or occupational disease;

- social leaves provided to women in connection with the birth of children - sick leave for pregnancy and childbirth (maternity leave) and time to care for a child up to one and a half or three years.

According to the provisions of Art. 422 of the Tax Code, accruals for the described periods are classified as social security payments. According to the legislation of the Russian Federation, in this case, contributions from vacation pay are not paid.

From incentive payments

Are premiums subject to insurance contributions? In general, yes, because they relate to payments under an employment contract (this is an incentive remuneration, as a rule, based on the results of consideration of labor results) and, in accordance with Art. 420 of the Tax Code of the Russian Federation are subject to taxation of the payments under discussion. Thus, since these are deductions made within the framework of an employment agreement, and they are not indicated in the list of non-taxable payments (Article 422 of the Tax Code of the Russian Federation), payments to the Funds must be transferred from them.

There are premiums that are not subject to insurance premiums. This is evidenced by judicial practice. Arbitration courts, in terms of deductions for incentive payments, interpret Article 422 of the Tax Code of the Russian Federation in this way: payments in connection with insurance are transferred if premiums are paid under an employment contract. Their size depends on labor achievements, in other cases - not.

What premiums are not subject to insurance premiums? For example, those issued in connection with a company anniversary or a national holiday in the same amount for all employees. There is a subtle nuance: if the size is different, it still turns out that the payment depends on labor achievements. Even if incentive payments are not provided for in a contract, collective agreement, or the provisions of local regulations, they are paid in connection with the performance of job duties, the source of their formation is not important. Therefore, they are also subject to a premium at the expense of net profit; insurance premiums must be deducted from them in the general manner.

Due dates for payment of contributions

The company is obliged to transfer contributions from the funds issued to the employee no later than the fifteenth day of the month following the one in which the employee was given the remuneration. This rule is spelled out in paragraph 7 of Art. 6.1 of the Tax Code of the Russian Federation.

Working conditions regulated by the Labor Code and Tax Code of the Russian Federation oblige employers to comply with the specified period. Responsibility for its violation is expressed in the form of a penalty for each day of delay and a fine equal to 20% of the amounts subject to deduction.

The company also faces liability if an accounting error was made that led to an incorrect calculation of the amounts payable. For such a violation, fines of 5-10 thousand rubles are provided. for the head of the enterprise and the chief accountant.

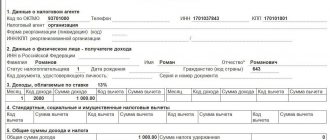

An example of calculating insurance contributions for vacation pay for an annual 28-day rest period in the amount of 30 thousand rubles:

IMPORTANT! Contributions must be made in separate payments to the appropriate funds within the period prescribed by law.

Accrual rules

Employees of any company go on vacation based on a special schedule that is formed at the beginning of the year. It is allowed to postpone periods at the initiative of the employer or employees.

Vacation payments are transferred to the citizen three days before the start of the rest period. Insurance premiums must be calculated in the same month as vacation pay, which is confirmed by the provisions of Art. 421 and 424 NK.

If a citizen resigns, but has unused rest days, he is assigned special compensation. Its size depends on average earnings and remaining days. Personal income tax and insurance premiums are additionally paid from this amount. The calculation procedure is carried out on a general basis.

If the employer, for various reasons, does not remit taxes on time, this leads to the accrual of penalties, and if arrears are discovered, then during desk or on-site inspections a fine is imposed, which is equal to 20% of the unpaid contribution.

If an accountant makes mistakes during calculations, he and the director of the company will be held administratively liable. It is presented in the form of a fine from 5 to 10 thousand rubles.

Are they charged according to law?

Every officially working citizen of Russia is supposed to be given annual paid leave.

Expert opinion

Polyakov Pyotr Borisovich

Lawyer with 6 years of experience. Specialization: civil law. More than 3 years of experience in drafting contracts.

The Labor Code of the Russian Federation also enshrines the right to additional leave, which is given due to dangerous working conditions, irregular working hours or the special nature of the work.

Important! The Russian Tax Code states that insurance contributions are subject to vacations of any kind, including paid annual and additional ones.

An exception is maternity and child care leave; benefits paid on these grounds are not subject to contributions.

Insurance premiums must be transferred:

- for pensions at a rate of 22%;

- for social (disability and maternity) at a rate of 2.9%;

- in medical - 5.1%;

- for social protection from occupational diseases - from 0.2%.

The first three are accrued for payment to the Federal Tax Service, the last - to the Social Insurance Fund.

There are some exceptions in the form of non-taxable holiday periods.

The following holidays are not subject to contributions:

- To undergo medical treatment in resort organizations for workers who have work-related injuries or occupational diseases. Such vacation is considered paid. Moreover, the employer is obliged to reimburse the costs of travel and treatment. This is stated in Law No. 125-FZ, paragraph 1, article 8.

- Victims of radiation as a result of the Chernobyl disaster. Budget funds are used for such payments.

Due to the fact that such payments for the above types of paid vacation are made at the expense of social insurance, vacation pay contributions are not accrued.

We also recommend reading: Is vacation compensation subject to insurance contributions?

When to pay in 2021?

Almost all insurance contributions must be paid to the Federal Tax Service budget, except for injuries.

Important! The payment deadline, according to Article 431 of the Tax Code of the Russian Federation, is until the 15th day of the next month in which vacation pay is accrued.

If the 15th is a weekend or non-working day, then the deadline is considered to be the nearest working day. This procedure is established by clause 7 of Art. 6.1 Tax Code of the Russian Federation.

This is important to know: sample vacation compensation order 2021

In 2021, the terms and conditions for paying contributions for injuries to the Social Insurance Fund are the same as to the tax office. The payment procedure is prescribed in clause 4 of article 22 of Federal Law No. 125 dated.

If you do not pay your dues on time, then the tax office will charge penalties. If arrears are identified during an audit, the organization is also imposed a fine of 20% of the debt amount.

How to pay insurance premiums to a budget organization

So, based on Art. 431 of the Tax Code of the Russian Federation, we can affirmatively state that disputes about how insurance premiums are paid (with or without kopecks in 2021) are absolutely groundless. Paragraph 5 of this article gives a comprehensive answer: we pay in rubles if the amount is “round”, and in rubles and kopecks if the amount is a fraction.

After the repeal of Law No. 212-FZ dated July 24, 2009, most policyholders have questions about how to transfer insurance premiums in 2021. Now the procedure for calculation, payment, terms and rates is regulated by the new 34th chapter of the Tax Code. The changes affected compulsory pension and medical coverage (CPS, compulsory medical insurance), as well as contributions in case of temporary disability and in connection with maternity (VNiM).

Vacation pay for employees engaged in hazardous work is subject to additional tariff contributions

Additional tariffs for insurance contributions for compulsory pension insurance apply to payments and other remuneration in favor of individuals employed in the types of work specified in paragraphs 1 - 18 of part 1 of Article 30 of the Federal Law of December 28, 2013 N 400-FZ “On Insurance Pensions”.

At the same time, the mentioned insurance premiums at additional tariffs, as well as insurance premiums at the main tariffs, are charged in the generally established manner on all payments and remunerations in favor of the employee, recognized as the object of taxation, with the exception of the amounts specified in Article 422 of the Tax Code.

An employee who holds a position in a job with harmful, difficult and dangerous working conditions, but is absent from work due to being on annual paid leave, educational leave, maternity leave, parental leave until the child reaches the age of 1, 5 years, due to temporary disability, etc., continues to be considered employed in the above jobs.

This is important to know: Are days off on vacation paid?

Thus, payments in favor of the above-mentioned employee holding a position at work with harmful, difficult and dangerous working conditions, accrued in the month the employee is on the mentioned vacations or during a period of temporary disability, are fully subject to insurance premiums in the generally established manner, including for OPS at additional rates.

General provisions

It is very important for the employer to determine which compensation, social or incentive payments these payments are calculated for. Several points will be discussed here.

There are several types of vacation pay. According to the law, each of them requires its own calculation procedure.

An equally important question: is the premium subject to insurance contributions? By definition, this is an incentive payment for work. Therefore, the discussed deductions must be paid from it. However, there are exceptions, which we have already discussed.

Are they accrued?

Expert opinion

Polyakov Pyotr Borisovich

Lawyer with 6 years of experience. Specialization: civil law. More than 3 years of experience in drafting contracts.

Regardless of the chosen taxation system used at the enterprise, insurance contributions for compulsory medical, pension and social insurance are charged on the entire amount of vacation pay (Article 420 of the Tax Code of the Russian Federation).

In addition, deductions for accidents and occupational diseases are calculated on the amount issued (125-FZ of July 24, 1998).

The Tax Code indicates the need to tax any type of employee rest, with the exception of maternity leave, and rest accompanied by treatment in sanatorium-resort institutions. Payment under these circumstances is made from the funds of the Social Insurance Fund; contributions are not charged.

When and how to pay in 2019?

The transfer must be made no later than the 15th day of the month following the month of accrual of vacation pay (Article 431 of the Tax Code of the Russian Federation, clause 3).

If the payment day coincides with a weekend or holiday, the payment order should be issued on the next business day following the transfer deadline.

For this type of tax burden, the day of payment of vacation pay or the date the employee starts rest does not matter.

The payment procedure is influenced by which company accrues them. If a separate division independently calculates payments, then the transfer of insurance premiums is carried out at its own location. If all actions are carried out by the head office, then it pays this type of deductions (Article 431 of the Tax Code of the Russian Federation, clause 11).

How holiday pay is assessed - example

Initial data:

Employee Klekovkina M.A. Irregular working hours are established. The collective agreement gives her additional leave of 8 days.

Nuances of granting leave

Before we talk about what insurance premiums are charged on vacation pay, and whether they are charged at all, it is necessary to note how these paid days off from work are generally provided. Everyone knows that vacation is called annual calendar leave, but rarely does anyone think that it is so called because it is given only once a year. This also happens because enterprises often divide workers’ rest into several periods, usually two weeks or so.

Back to contents

Duration of calendar rest

In general cases, the law recommends the number of vacation days is twenty-eight, but if a manager wants to reward his employees, for example, with thirty days, this is not prohibited. In addition, a certain category of employees, for example, workers in the education sector, can rest much longer - due to the specifics of the profession and the structure of the work process. It must be remembered that, according to labor legislation, at least one part of the vacation must be at least two weeks - such a period is considered sufficient for proper rest.

Back to contents

Procedure for granting leave

To earn the right to paid holidays, you must first work a certain number of working days. As mentioned above, rest is considered annual, but for the first time you can take a break from your company and colleagues already six months after your first working day. Of course, this must be agreed upon with superiors and colleagues - usually organizations have already drawn up a vacation schedule for the whole year in January, and they are not very willing to change it. This is due to the accrual and issuance of funds for employees.

Back to contents

Is it possible to pay insurance premiums from vacation pay earlier?

The employer calculates mandatory payments for contributions based on the results of each calendar month based on the amounts accrued in favor of the employee (Part 3, Article 15 of Law No. 212-FZ of July 24, 2009). And he pays them to the Pension Fund of the Russian Federation, the Social Insurance Fund and the Federal Compulsory Medical Insurance Fund no later than the 15th day of the month following the month of accrual (Part 5, Article 15 of the Law of July 24, 2009 N 212-FZ).

- payment for leave for sanatorium-resort treatment provided if an employee has an accident or receives an occupational disease (clause 1, part 1, article 9 of the Law of July 24, 2009 N 212-FZ, subclause 3, clause 1, article 8 Law of July 24, 1998 N 125-FZ, Letter of the Ministry of Labor dated October 27, 2015 N 17-3/B-524).

Leave compensation upon dismissal, insurance premiums

In addition to basic income, there is a category of compensation payments that are not subject to insurance premiums. So, at the time of dismissal, the employee is entitled to severance payments. And if the amount is within 3 average earnings of the applicant, then no tax is paid. For employees of enterprises in the Far North and equivalent regions, the amount of non-taxable benefits was increased to 6 average monthly earnings. This possibility is mentioned in Art. 9 of Law No. 212-FZ of July 24, 2009

For any type of dismissal, the employer must compensate the citizen for unused vacation days. But, there is also a situation in which you cannot count on repayment of vacation payments. This is the case when he does not resign of his own free will, but is eliminated under an article for guilty actions.

Is it possible to transfer insurance premiums in the middle of the month?

Withhold personal income tax on income paid in kind or in the form of material benefits from any monetary remuneration paid to an employee. That is, in this case, the date of payment of income and the date of tax withholding may differ. In this case, the withheld tax amount cannot exceed 50 percent of the amount of monetary remuneration.

The tax agent’s obligation to transfer personal income tax to the budget can be considered to have arisen if the following conditions are simultaneously met: – wages for the past month have been accrued (the management of the organization has approved the payroll for the payment of wages); – the amount of personal income tax subject to withholding from the income of each employee has been determined (accounting entries related to the withholding of personal income tax have been made, and accounts payable have been generated in account 68 subaccount “Personal Income Tax Payments”).