Cash discipline is another area of business responsibility that requires detailed study and compliance. The rules for using cash register equipment (hereinafter referred to as CCT) oblige sellers to issue cash receipts or strictly reporting forms (hereinafter referred to as CC and BSO) each time buyers pay for goods or services. At the same time, you can often encounter situations where a sales receipt is also issued along with them. If the CoC and BSO are mandatory documents, then the sales receipt is only complementary. So is there a need to provide both of these documents? And what exactly is the difference between them? Let's try to figure it out.

What are sales and cash receipts: the difference

A cash receipt (CR) is a document printed on a cash register, intended for the initial accounting of the purchase of goods. It is an attachment to the commodity.

A sales receipt (PR) is a fixed version of confirmation of a purchase made from a seller. Owners of companies subject to a single tax on imputed income are exempt from installing a cash register. In this case, it is allowed to issue a sales receipt without a cash receipt. There are nuances that must be taken into account when issuing a payment form. Let's talk about them further.

S - Business online magazine

NGS.BUSINESS is a business online magazine from Novosibirsk. Daily fresh news from the world of business, economics and finance, expert comments. Thanks to the site, you can find out currency quotes and choose a profitable deposit among the offers of Novosibirsk banks, find advertisements for the purchase and sale of ready-made businesses, choose a mortgage, a car loan, and also discuss business ideas and questions with readers on the business forum.

Network publication "NGS.NEWS" (18+) Registered by the Federal Service for Supervision of Communications, Information Technologies and Mass Communications (Roskomnadzor) Certificate of registration of mass media EL No. FS 77 - 70959 dated 09/13/2021 Founder: LLC "Network of Urban portals" Editorial office: LLC "Network of City Portals" Editor-in-Chief: Agafonov Alexander Sergeevich Editorial office address: 630099, Novosibirsk region, Novosibirsk, st. Lenina, 12., 6th floor, telephone Editorial office email address

Requirements for sales and cash receipts

Today there are no established rules for what a sales receipt without a cash receipt should look like. Each owner has the right to decide for himself how the payslip will be drawn up. It is important to remember that the sales receipt or cash register is considered valid. Let's look at what is written on each check:

| Sales receipt | Cash receipt |

|

|

Data from checks must be clear, printed using thermal paper, on which information is not stored for a long time (Article 4.7, 54-FZ). According to accounting standards, the PM contains a transcript of the cash register, because Not in all cases the latest version of the forms contains the necessary information about the purchase.

What is the difference between an invoice and a delivery note?

The consignment note has a certain structure - a document header, a tabular part and a place for stamps and signatures. The header contains information about the shipper and consignee, and the place of delivery. The header also contains the number and date of the document and information about the document on the basis of which the delivery is made. The tabular part contains information about the supplied product - name, quantity, price and other data.

An invoice is a document that accompanies the transfer of inventory from one person to another. A consignment note is one of the varieties of this document. With its help, goods are shipped from the supplier, received and processed at the recipient's warehouse or retail outlet.

Design rules

If the enterprise does not have a cash register, the entrepreneur issues a form confirming the receipt of money for a product or service, if the buyer requests it. In such cases, a sales receipt is issued without a cash receipt. For a sheet to be considered valid, it must be compiled correctly.

So, a sales receipt for an individual entrepreneur without a cash receipt contains:

- Company details. The absence of any one point is grounds to consider the sheet invalid. There are cases when entrepreneurs place advertising on the back and front sides of the form. Such an action is not prohibited by law. But when registering, you should remember that advertising should not cover the details.

- List of products. The name of each new item or service is entered on a separate line. For example, if a buyer purchases office supplies, each new item (pen, pencil, notepad, etc.) will need to be indicated in the deed. It is wrong to describe “office supplies” in general terms.

- Total purchase amount. The information is written in a specially designated column. This rule is mandatory, and it does not depend on the number of goods purchased. To be on the safe side, you can make a double entry: in numbers and in words.

- Cross out the remaining empty lines so that no one can add additional products in the future. This is done in cases where the number of lines in the form is greater than the number of goods purchased.

The procedure for issuing PM requires care during registration. This entails high demands on both the entrepreneur and his employees making cash payments.

New list of documents for the advance report in 2021

If an employee used railway transport (train) with an electronic ticket, then he must go through electronic registration. There will be a note about this on the ticket “Electronic registration completed.” If there is no mark, expenses cannot be accepted.

Introductory information about the expense report

If the seller refuses to issue a check after July 1, 2021, then you need to take from him a payment receipt, which must contain the required details, including a signature (clause 2.1, 3 of Article 2 of the Federal Law of May 22, 2003 No. 54 -FZ).

According to Article 14.5 of the Code of the Russian Federation on Administrative Offenses, refusal to issue a document at the request of the buyer (client) in the case provided for by federal law entails a warning or the imposition of an administrative fine. For citizens, the fine will be from 1.5 to 2 thousand rubles, for officials - from 3 to 4 thousand rubles, for legal entities - from 30 to 40 thousand rubles.

The cash receipt must be given to the buyer or client at the time of the purchase and sale transaction - the transfer of the fiscal document is confirmation of the completion of this transaction. A cash receipt is necessary for the buyer or client in case he wants to return the purchased product or replace it.

Storage of documents: procedure and terms

However, the law states that businessmen are obliged to ensure the safety of archival documents during their storage period (Part 1 of Article 17 of the Law “On Archival Affairs in the Russian Federation” dated October 22, 2004 No. 125-FZ) - otherwise they may be punished under Art. 13.20 or 13.25 Code of Administrative Offenses of the Russian Federation.

Once the archiving period has expired, stored documents can be disposed of: burned or cut using special equipment. However, be extremely careful not to accidentally destroy data that is still valid or requires storage.

Have the retention periods for invoices changed since October 1, 2017? How to organize the storage of electronic invoices? Is it necessary to keep copies? Where should documents be kept? Let's figure it out.

Documents on specific issues and activities

However, in addition to this, amendments were also made to the rules that relate to the storage of invoices. Let's tell you more about them.

In addition, the TTN (Form No. 1-T) is a document intended to record the movement of inventory items and payments for their transportation by road. Therefore, if the buyer simultaneously acts as a customer for the transportation of goods, he must have a consignment note (form No. 1-T) (letter of the Federal Tax Service of Russia dated August 18, 2009

No. ШС-20-3/1195).

If an organization has a small volume of documents, then storage is carried out by the organization, and the documents are usually stored in the accounting department. If the organization has a significant document flow, then it makes sense to create an archive as an independent structural unit.

If the cargo is delivered by a transport organization (road transport), a TTN is issued in Form No. 1-T. When transporting using its own vehicles, the seller also issues a consignment note. This document can serve as the basis for reflecting received goods in the buyer’s accounting.

In September 2012, the company acquired inventory items intended for further sale. For this transaction, the seller issued a delivery note and issued an invoice dated September 18, 2012. Payment was made through the bank. We will determine the storage period for documents.

Expert opinion

Makarov Igor Tarasovich

Legal consultant with 8 years of experience. Specialization: criminal law. Extensive experience in document examination.

Such periods end in the corresponding month and day of the last year of the term. Upon direct reading of the provisions of this article, it turns out that the period of storage of a document begins from the day following the day of its preparation.

Personal files and cards of employees, employment contracts with employees, documents on dismissal and hiring must be kept for 75 years.

Let's look at an example. IP Ryabinin K.

N. decided to stop commercial activities.

Since the landlords urgently demanded to vacate the premises, the businessman transported all the documents to his home and placed them in the free space in the utility room. Invoices took up a considerable volume, since the sale of goods was carried out in small batches to numerous counterparties.

Failure to comply with these requirements for storing documents in the event of their loss may subject the organization to liability for tax offenses. Based on clause 6.8 of the Regulations, in the event of loss or destruction of documents, the head of the organization must appoint by order a commission to investigate the reasons for the loss of documents.

How long are accounting documents kept? On average 5 years, but the duration of storage depends on the type of document. The exact deadlines are indicated in the Tax Code and the new order of the Federal Archive, which came into force on 02/18/2020.

Based on the legislative acts mentioned above, organize the storage of accounting documents in the organization.

We will tell you about the latest news and publications. Read us anywhere. Always be aware of the main thing!

Store electronic documents in Diadoc - it's safer than on your personal computer. All documents are stored in several copies on different servers, which makes it impossible to lose information. Try Diadoc for free with the “Unlimited for 2 months” promotion.

Primary accounting documents, accounting registers and financial statements, if they are not specified in the List of storage periods, are stored for five years (Clause 1, Article 17 of the Federal Law of November 21, 1996 No. 129-FZ).

Storage periods for invoices at an enterprise What is the storage period for invoices when transporting goods in a legal entity, such as a Limited Liability Company? Question No. 2. Are TTNs generally required if, for example, waybills are already being issued?3. Question No. 3.

What is it used for?

The turnover of goods and materials in the process of their movement and sale is certified by documents. This is precisely why such a shipping document (along with others) is used. For the seller it reflects expenditure transactions, and for the buyer it reflects incoming transactions.

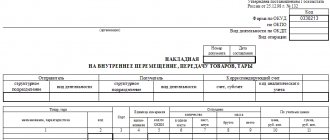

This documentation shows that the products were released, and also serves as the basis for accounting actions: writing off surplus from warehouses, accounting for units sold. The main purpose is to record the movement of inventory items within a business entity (between workshops and departments), as well as during sales to contractors. Correctly completed RP confirms the specificity of gross expenses when calculating taxes.

Such paper serves as a basis for carrying out transactions under a cooperation agreement. But it does not reflect the payment made, since it does not contain information about depositing money into the cash register or transferring it to the supplier’s account. In this regard, it is interesting how the invoice differs from the goods invoice.