Depositing authorized capital into a current account

A financial transaction can be carried out in one or more payments. The purpose of payment should indicate “formation of authorized capital”. A receipt indicating the fact of the event should be attached to the registration package of documentation. It should be noted that after completing the registration procedure, the temporary account to which the transfer was made is transformed into a permanent one.

The authorized capital is deposited by the founders of the company into its current account after the completion of registration activities. The fund must contain a minimum amount in monetary terms, the value of which corresponds to 10,000 rubles. Everything above can be contributed in monetary or property equivalent.

Acquisition of a share in the authorized capital

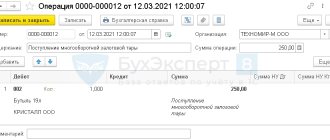

Based on the Instructions for the application of the Chart of Accounts for accounting the financial and economic activities of organizations, approved by Order of the Ministry of Finance of Russia dated October 31, 2000 N 94n, account 81 “Own shares (shares)” is intended to account for the share of a participant acquired by the company upon its exit from the LLC. On the date of receipt of an application from an LLC participant about his withdrawal from the company, the debit of account 81 in correspondence with the credit of account 75 “Settlements with founders” reflects the debt to this participant in the amount of the actual value of his share.

The participants of the company, in whose favor the share in the authorized capital transferred to the company was distributed, received income in kind, subject to personal income tax (clause 1 of article 210, clause 2 of clause 2 of article 211 of the Tax Code of the Russian Federation). The tax base, in accordance with paragraph 1 of Art. 211, art. 41 of the Tax Code of the Russian Federation (see also Letters of the Ministry of Finance of Russia dated December 19, 2007 N 03-04-06-01/444, dated October 25, 2007 N 03-04-06-01/360), is determined based on the actual value of the distributed shares.

Purchase of an enterprise as a property complex

In their economic activities, commercial organizations make various transactions, including purchase and sale transactions, the subject of which may be an entire enterprise with all its property. The procedure and requirements for such transactions are regulated by Art. 559-566 Civil Code of the Russian Federation.

Under the sales agreement, the seller enterprise undertakes to transfer the ownership of the enterprise as a whole as a property complex to the buyer, with the exception of the rights and obligations that the seller does not have the right to transfer to other persons. Such rights and obligations include, for example, licenses and permits to engage in certain activities, the obligation to pay debts to creditors in the event of the latter’s refusal to transfer the debt from the seller to the buyer, the obligation to pay taxes and fees incurred before the transaction (clause 3 of Art. 44 of the Tax Code of the Russian Federation). Let's consider the situation from the perspective of the buyer of the property complex.