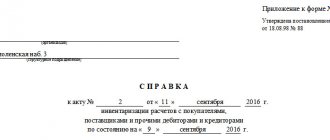

Carrying out an inventory of payments refers to one of the stages of the mandatory inventory of property and liabilities, carried out before drawing up annual reports in accordance with the requirements of paragraph 2 of Article 12 of Law 129-FZ “On Accounting”.

Taking into account the increasingly stringent requirements for the accuracy and reliability of financial statements, all significant reporting indicators are subject to close attention.

For many companies, such indicators include the amount of settlements with debtors and creditors, as well as the amount of estimated values (reserves) that regulate the amount of receivables in case of doubtfulness.

In order to exercise internal control over receivables and payables, as well as the reliability of their reflection in the annual financial statements, organizations need to: