From January 1, 2021, a new taxation system for residential real estate , this includes an apartment, house, cottage, and land plot. If previously the tax was calculated according to the BTI method, then from this year the tax is calculated based on the market, cadastral value based on the address .

Now ordinary citizens will have to give ten times more personal money to the state. If there is no money to pay the tax, the authorities suggest selling the apartment and looking for a more affordable option or renting housing. Of course, the adoption of this law caused excitement among ordinary citizens, because how should pensioners and low-income citizens of the Russian Federation pay the cadastral tax?

How to use the calculator

The easiest way to get an answer to the question of how to calculate an organization’s property tax in 2021 is to use an online calculator. It's easy to work with.

Step 1: Enter your tax rate. For budgetary organizations - 2%.

Step 2. Indicate in rubles the residual value of fixed assets at the beginning of each month and on the last day of the year. A separate field is provided for each digit. In total, you need to enter 13 values (two of them are December).

Step 3. When everything is ready, click on the Calculate button. The results will be displayed in the table below.

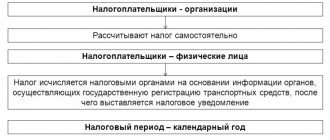

Official notice of tax assessments.

According to changes in the Tax Code of the Russian Federation, which entered into force in June 2021, personal liability increases for persons who have a personal account (personal account) on the Tax Service website. From now on, the tax department is allowed to inform individuals only through this online service, without sending paper notifications. Thus, property owners must independently control the receipt of notifications about tax assessments in their own account, without waiting for a written notice. If it is more convenient for the owner of a personal account to receive a notice in paper form, he must independently send the corresponding request to the Federal Tax Service.

Features of taxation

The calculation of the property tax of organizations, as well as the general requirements for the specified obligation to pay tax, are defined in Chapter. 30 Tax Code of the Russian Federation. The tax is recognized as regional, that is, the authority to determine the rates, terms and procedure for payment and additional benefits has been transferred to the constituent entities of the Russian Federation. Tax rates and the procedure for applying differentiating coefficients are approved by regional legislative acts.

Payers are legal entities that own (on balance, for temporary use) movable or immovable fixed assets that are recognized as an object of taxation. Budgetary institutions do not have preferential benefits. Lists of objects that are not subject to taxation and preferential categories of institutions are presented in detail in Art. 374 and 381 of the Tax Code of the Russian Federation.

The trade tax must be paid by organizations and individual entrepreneurs who conduct trading activities in Moscow through a trading facility. The payer of the fee is registered on the basis of a notification in Form N TS-1 submitted by him to the tax authority. Deadline for filing a notification (Clause 6, Article 6.1, Article 412, Clause 2, Article 416 of the Tax Code of the Russian Federation): • for initial registration - five working days from the day you started trading through a retail outlet; • if there is a change in the characteristics of trading activities that affect the amount of the fee (for example, the appearance of a new object) - five working days from the date of such change. A service for searching for trade items for which notifications on the trade fee have not been submitted or the notifications contain inaccurate information will help: either register the listed trade item, or correct the inaccurate information before drawing up an act by the Department and avoid a fine. Attention! The data in the list is updated monthly! If your property is included in the list, it means, according to the Department of Economic Policy and Development of the City of Moscow, that you are engaged in trading activities and have not submitted a notification on the trade tax to the tax authorities or have submitted a notification with errors. If a trade item included in the list has not been registered with the tax authority , then you can independently submit a notification to the tax authority within 20 calendar days before the relevant act is issued by the Department. In this case, you will need to pay the amount of the trade fee and penalties, without paying a fine. If you do not agree with the inclusion of an object in the list , then you must, within 20 calendar days from the date of its publication, send an appeal to the Department with a request to remove the object from the list. If the deadline of 20 days is missed, the Department, within five working days, will draw up an act on identifying a new object subject to trade tax or an act on identifying inaccurate information regarding the object subject to trade tax. The reports are sent to the tax authorities and the person using the facility for trade. Based on the act, the trade tax payer is registered and a demand for payment of the trade tax, penalties and fines is issued.

About fines If the deadline for submitting a notification to the tax authorities is violated, the fine will be 200 rubles.

If the notification is not submitted and the Department’s act is drawn up, then the fine will be 10% of the income for the period in which the activity was carried out without filing a notification, but not less than 40 thousand rubles. Also, the payer of the trade fee will lose the right to reduce other taxes by the amount of the trade fee. Go to calculation

Calculation of property tax for legal entities in 2021

This issue is regulated by clause 4 of Art. 376 Tax Code of the Russian Federation. To determine the tax base for an obligation regarding the organization’s property, the criteria of PBU 6/01 and the All-Russian Classifier of Fixed Assets (hereinafter referred to as OKOF) are used. Order of Rosstandart No. 458 dated April 21, 2016 regulates the transition of fixed assets to a new classifier. The document contains a detailed and clarified description of codes and decryptions.

Calculate property taxes in 2021 in a new way. Before drawing up a declaration or intermediate (advance) calculation, update the OKOF, and when calculating the tax base, exclude the objects that are listed in clause 4 of Art. 374 and Art. 381 of the Tax Code of the Russian Federation, that is, those that are excluded from the base:

- fixed assets classified in the first or second group of the updated classifier;

- land objects and environmental management objects;

- movable fixed assets acquired after January 1, 2013 (except for property that was taken into account as a result of the reorganization or liquidation of legal entities, and property of interdependent persons, in accordance with the conditions of clause 2 of Article 105.1 of the Tax Code of the Russian Federation);

- Fund objects not accepted for balance, in accordance with accounting requirements.

State employees calculate and transfer taxes to the appropriate budget at the average annual cost. But there are exceptions! They are determined individually, so they are clarified only by the tax office.

Formula for calculating property tax for individuals during the transition period

The 4th transition period will continue in 2021. Therefore, experts have identified a more detailed formula to ensure an imperceptible increase in tax revenues - and a soft, smooth transition to the new taxation system for Russians.

Now every Russian can pay taxes in advance

In 2018-2020 the following scheme will be in effect:

| Н= (N- Ninv) x K + Ninv =(N- Ninv x Kdef x Sinv) x K + (Ninv x Kdef x Sinv) Where N = (Ncad - W) x C = (Ncad - U x Sw) x C = (Ncad - Ncad./S x Sw) x C

|

To make the calculation, you should:

- Calculate the specific cadastral value of the object - divide the cadastral value by the taxable area ( U = Ncad/S).

- Calculate the deduction that is possible and required by law for a Russian citizen ( W = x Sw ).

- Calculate the tax amount based on the cadastral value. To do this, it is necessary to subtract from the cadastral value the deduction calculated in paragraph 2 ( N = Ncad. - W ).

- Calculate the tax fee based on the inventory price of the property ( Ninv = (Ninv x Kdef x Sinv).

- And finally. calculate the final amount of tax to be paid by the citizen ( H = (N- Ninv) x K + Ninv).

Of course, this formula is the best, as it takes into account all the important indicators that affect the amount of tax collection.

How to calculate property tax

There is no need to carry out tax calculations yourself, because the Federal Tax Service inspectorate does this personally and, after the calculation, sends the document to the property owner. This document will indicate the amount required to be paid in the form of a tax fee.

On January 1, 2015, Chapter number 32 of the Tax Code of the Russian Federation came into force, which introduced new procedures for calculating property taxes. Now the cadastral value of the property comes first, according to which the calculation will be made. Previously, this was the inventory value. The cadastral value is considered to be as close as possible to the market value, so this decision was made.

Important! Some regions of the country have not yet complied with the instructions, that is, the cadastral value has not been officially approved, for which a special act had to be drawn up and sent for publication. Therefore, in these regions in 2021, the tax will be calculated according to the old rules.

Note: the situation will change only by 2021. This is exactly the deadline the state has set for the entire territory of our country.

How to calculate tax from cadastral value

There is a special scheme for this:

Nk = (Cadastral value - Tax deduction) * Share size * Tax rate

More details:

Cadastral value. Taken from the official state real estate cadastre as of January 1 of each year. If the object is new, it will be registered at the time of delivery. If you need to find out this cost, the Rosreestr branch for the territory where the property is located will be able to help.

Tax deduction. There are several options based on the type of property.

- Apartment - a deduction can reduce the calculation by 20 square meters.

- If the property is a room, then 10 square meters.

- A residential building gives the right to deduct 50 square meters from the calculations.

When a residential building is taxable property (a single complex of real estate with residential premises), the deduction will be equal to one million rubles.

Note: managers of Moscow, St. Petersburg and Sevastopol have been given the opportunity to increase these deductions

If the cadastral value after deduction is less than zero, then it is equal to zero.

Tax calculation example

Ivan Ivanovich owns an apartment with an area of 50 square meters. According to the cadastre, it is estimated at 3 million rubles. The price per square is 60 thousand.

Tax deduction, if calculated: 60,000 * 20 squares = 1,200,000 rubles.

This means that in order to calculate the tax, Ivan Ivanovich will use only 1 million 800 thousand rubles as the cadastral value.

Share size. Often property is divided between several owners according to certain shares. In accordance with the share, the tax will be calculated for a specific property owner separately.

Tax rate. This indicator is individual for each specific subject of the Russian Federation. To find out, you need to go to the Federal Tax Service website. In a special section there will be decrees and indicators.

Also, the tax rate depends on the type of property.

- Residential buildings (even those whose construction has not yet been completed), residential apartments and rooms have a rate of 0.1%. This also includes garages, places for vehicles, outbuildings smaller than 50 square meters, which are located on the ground. plots for personal farming or personal construction.

- Rate 2%. This indicator is used when calculating the tax for shopping centers, administrative and business buildings, office and retail buildings and public catering and consumer services buildings. And also those buildings whose cost according to the cadastre is more than 300 million rubles.

- The 0.5% rate applies to other objects that do not fit the previous two sections.

Example for calculation:

Let's assume that Ivan Ivanovich owns half of the apartment, the size of which is 50 square meters. As in the previous example, the tax deduction will be 1 million 200 thousand rubles. The tax rate for this type will be 0.1%. Applying the already known formula, Ivan Ivanovich will obtain the following result:

(3 million (cad. cost) - 1 million 200 thousand (deduction)) * 0.5 (share) * 0.1 percent (rate) = 900 rubles.

Calculation based on the inventory value of property

The formula is:

Ni = Inventory value * Share size * Tax rate

The owner of the property can check the inventory value at the BTI branch to which the property belongs.

The tax rate has its own variations here too. Again, it varies for different subjects. Details can be found in this section of the official website of the Federal Tax Service.

There are certain limits to this rate:

- If the investment value is up to 300 thousand rubles. inclusive, then a rate of 0.1% is applied.

- If the cost is from 300 thousand to 500 thousand rubles, then the rate will be from 0.1 to 0.3 percent.

- If the cost is more than 500 thousand rubles, then the maximum rate will be 2 percent.

Important! The municipal government has the right to set a differentiated tax rate.

Example of calculation based on inventory value:

Ivan Ivanovich owns half of the apartment. He found out that the investment value of the entire apartment is 200 thousand rubles. The rate for such property will be 0.1 percent. This means, based on the formula, he will have to pay 100 rubles. (200 thousand * 0.5 share * 0.1% rate).

As we can see, the tax values for the two methods vary greatly. And since the cadastral method will soon be the only one, the government decided to extend the increase in the tax burden for 4 years. Therefore, until 2021, in those areas of the country where a new calculation method is being introduced, it is recommended to use the following formula for the first four years:

H = (Hk - Ni) * K + Ni

Nk and Ni, as you already understood, this is the cadastral and inventory value of the property.

K - reduction factor. It is thanks to him that the tax increase will be 20% slower. It is equal to 0.2 in the first year after the introduction of new rules, 0.4 further, 0.6 and 0.8 in the 3rd and fourth years, respectively.

In the fifth year, the calculation will have to switch to the cadastral version completely.

Important! This rule is applicable only in cases where the tax calculated based on the cadastral value differs significantly from that calculated based on the inventory value.

How to pay property tax

One of the most convenient options at the moment is the special service of the official tax service portal “Payment of taxes for individuals” https://service.nalog.ru/payment/tax-fl.html.

You will need:

- Correctly fill out the fields with the details (TIN must be filled out for those who plan to pay by bank transfer).

- Select the type of tax you want to pay, indicate the address of the property and the type of payment (payment of tax or payment of tax penalties).

- Specify the payment amount.

- Select which option will be used to pay the tax. If you want to pay in cash, the program will give you a ready-made receipt, which you can use to pay at the bank (to do this, click “Generate PD”). If your option is cashless payment, then you will need to select the credit institution through which the payment will be made, after which you will be taken to the payment page.

Tax payment deadlines

In 2021, the deadline is the same for everyone - no later than December 1, 2017. If the deadlines are ignored, a penalty will be charged for each day of delay. The amount of the penalty is one three-hundredth of the refinancing rate of the central bank.

Moreover, the tax office has the right to notify his employer of problems with the taxpayer. In this case, the arrears will be collected from wages. And the violator will also receive the status of a travel ban. That is, it will be impossible to leave the Russian Federation.

In addition, there is no fine for individuals.

How to make approximate calculations yourself?

You can independently calculate the tax that will have to be paid after the end of the transition period.

To do this, you need to know the cadastral price of your home and the size of the total area. This information can be obtained in the form of a request on the Rosreestr website.

Moreover, if the apartment is located in an ordinary, not elite building, then the minimum rate of 0.1% will apply. For prestigious housing, a maximum rate of 2% is used.

You can find out how to find out the cadastral price of your property in this detailed article. You may also find it helpful to learn how this value is calculated and how to challenge it to reduce your tax.

Payment procedure:

- At the first stage, it is necessary to determine the price of 1 m² from the cadastral valuation.

- Then you should calculate the area on which the tax will be charged. When living in an apartment, the total area should be reduced by 20 m². If the calculation is made for a room, the reduction will be 10 m².

- The resulting values from previous calculations are multiplied and adjusted by the tax rate.

If the property is in shared ownership, then each owner will have to pay his or her share of the charges.