Every person who is registered in the Russian Federation and owns a vehicle needs to be well acquainted with the rules written down in the Tax Code for paying the transport tax. No matter how conscientious a payer he is, any person may encounter unforeseen circumstances, which causes a delay in payment. In this case, penalties, fines and interest will be charged. They must be transferred to specific numbers.

- Who does the transport tax apply to?

- What are the criteria taken into account for its accrual?

- 18210604011022100110 KBK what tax?

KBK for payment of penalties on transport tax for individuals

| PENALIES, INTEREST, FINES | KBK | |

| Penalties, interest, fines on transport tax for individuals | penalties | 182 1 06 04012 02 2100 110 |

| interest | 182 1 06 04012 02 2200 110 | |

| fines | 182 1 06 04012 02 3000 110 | |

FILES

KBK 2021

Order of the Ministry of Finance of Russia dated June 8, 2020 No. 99n approved the following codes of the budget classification of the Russian Federation for 2021:

| Payment | Tax | Penalty | Fine |

Pension contributions to the Federal Tax Service from employee salaries | |||

| Contributions to compulsory pension insurance | 182 1 02 02010 06 1010 160 | 182 1 02 02010 06 2110 160 | 182 1 02 02010 06 3010 160 |

Contributions to compulsory social insurance from employee salaries to the Federal Tax Service | |||

| Contributions to compulsory social insurance in case of temporary disability and in connection with maternity | 182 1 02 02090 07 1010 160 | 182 1 02 02090 07 2110 160 | 182 1 02 02090 07 3010 160 |

Contributions to compulsory health insurance from employee salaries to the Federal Tax Service | |||

| Contributions for compulsory health insurance of the working population | 182 1 02 02101 08 1013 160 | 182 1 02 02101 08 2013 160 | 182 1 02 02101 08 3013 160 |

Contributions for injuries to the Social Insurance Fund | |||

| Contributions for injuries to the Social Insurance Fund | 393 1 0200 160 | 393 1 0200 160 | 393 1 0200 160 |

Insurance premiums for individual entrepreneurs for themselves | |||

| In the Pension Fund of the Russian Federation (fixed payment and payment from income 1% - a single BCC) | 182 1 0210 160 | 182 1 0210 160 | 182 1 0210 160 |

| In FFOMS | 182 1 0213 160 | 182 1 0213 160 | 182 1 0213 160 |

Personal income tax (NDFL) on employee salaries | |||

| Personal income tax on income the source of which is a tax agent, with the exception of income in respect of which tax is calculated and paid in accordance with Articles 227, 227.1 and 228 of the Tax Code of the Russian Federation (Salaries / Vacation pay / Dividends and other payments to employees) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

Personal income tax on income the source of which is a tax agent exceeding 5 million rubles | 182 1 0100 110 | ||

| Personal income tax on income received by citizens registered as: – entrepreneurs; – private notaries; – other persons engaged in private practice in accordance with Article 227 of the Tax Code of the Russian Federation | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Personal income tax on income received by citizens in accordance with Article 228 of the Tax Code of the Russian Federation | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Personal income tax in the form of fixed advance payments on income received by non-residents employed by citizens on the basis of a patent in accordance with Article 227.1 of the Tax Code of the Russian Federation | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

Value added tax (VAT) | |||

| VAT on goods (work, services) sold in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| VAT on goods imported into Russia (from the Republics of Belarus and Kazakhstan) | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| VAT on goods imported into Russia (payment administrator - Federal Customs Service of Russia) | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

Income tax | |||

| Income tax credited to the federal budget | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Profit tax credited to the budgets of constituent entities of the Russian Federation | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Income tax upon implementation of production sharing agreements concluded before the entry into force of Law No. 225-FZ of December 30, 1995 and which do not provide for special tax rates for crediting the specified tax to the federal budget and the budgets of constituent entities of the Russian Federation | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Income tax on the income of foreign organizations not related to activities in Russia through a permanent establishment, with the exception of income received in the form of dividends and interest on state and municipal securities | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Corporate income tax on income in the form of profits of controlled foreign companies | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Income tax on income received by Russian organizations in the form of dividends from Russian organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Income tax on income received by foreign organizations in the form of dividends from Russian organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Income tax on income received by Russian organizations in the form of dividends from foreign organizations | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| Income tax on income received in the form of interest on state and municipal securities | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

Excise taxes | |||

| Excise taxes on ethyl alcohol from food raw materials (except for distillates of wine, grape, fruit, cognac, Calvados, whiskey), produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on ethyl alcohol from non-food raw materials produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on ethyl alcohol from food raw materials (wine, grape, fruit, cognac, calvados, whiskey distillates) produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on alcohol-containing products produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on tobacco products produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on motor gasoline produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on straight-run gasoline produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on passenger cars and motorcycles produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on diesel fuel produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on motor oils for diesel and (or) carburetor (injection) engines produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on wines, fruit wines, sparkling wines (champagnes), wine drinks made without the addition of rectified ethyl alcohol produced from food raw materials, and (or) alcoholized grape or other fruit must, and (or) wine distillate, and (or) fruit distillate produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on beer produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on alcoholic products with a volume fraction of ethyl alcohol over 9 percent (except for beer, wines, fruit wines, sparkling wines (champagnes), wine drinks produced without the addition of rectified ethyl alcohol produced from food raw materials, and (or) alcoholized grape or other fruit must, and (or) wine distillate, and (or) fruit distillate) produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on alcoholic products with a volume fraction of ethyl alcohol up to 9 percent inclusive (except for beer, wines, fruit wines, sparkling wines (champagne), wine drinks made without the addition of rectified ethyl alcohol produced from food raw materials, and (or) alcoholized grape or other fruit must, and (or) wine distillate, and (or) fruit distillate) produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| Excise taxes on alcoholic products with a volume fraction of ethyl alcohol over 9 percent (except for beer, wines, fruit wines, sparkling wines (champagnes), wine drinks produced without the addition of rectified ethyl alcohol produced from food raw materials, and (or) alcoholized grape or other fruit must, and (or) wine distillate, and (or) fruit distillate), imported into the territory of Russia | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| Excise taxes on household heating fuel produced from diesel fractions of direct distillation and (or) secondary origin, boiling in the temperature range from 280 to 360 degrees Celsius, produced in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

Organizational property tax | |||

| Tax on property of organizations not included in the Unified Gas Supply System | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Tax on property of organizations included in the Unified Gas Supply System | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

Land tax | |||

| Land tax levied on taxable objects located within the boundaries of intra-city municipalities of federal cities of Moscow and St. Petersburg | 182 1 06 06 031 03 1000 110 | 182 1 06 06 031 03 2100 110 | 182 1 06 06 031 03 3000 110 |

| Land tax levied on taxable objects located within the boundaries of urban districts | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Land tax levied on taxable objects located within the boundaries of inter-settlement territories | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Land tax levied on taxable objects located within the boundaries of rural settlements | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Land tax for plots within the boundaries of urban settlements | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Land tax for plots within the boundaries of urban districts with intra-city division | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Land tax for plots within the boundaries of intracity districts | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

Transport tax | |||

| Transport tax for organizations | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| Transport tax for individuals | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

Single tax simplified taxation system (STS) | |||

| Single tax with simplified income | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Single tax simplified from the difference between income and expenses | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Minimum tax | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

Unified tax on imputed income (UTII) | |||

| UTII | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| UTII (for tax periods expired before January 1, 2011) | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Unified Agricultural Tax (USAT) | |||

| Unified agricultural tax | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

| Unified Agricultural Tax (for tax periods expired before January 1, 2011) | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

Water tax | |||

| Water tax | 182 1 0700 110 | 182 1 0700 110 | 182 1 0700 110 |

Trade fee | |||

| Trade tax in federal cities | 182 1 0500 110 | 182 1 0500 110 | 182 1 0500 110 |

KBK 2021 for insurance premiums according to lists of professions

| Payment | Old codes | New KBK |

| Penalty | ||

| List 1, tariff depends on special assessment | 182 1 0210 160 | 182 1 0200 160 |

| List 1, the tariff does not depend on the special rating | 182 1 0210 160 | |

| List 2, tariff depends on special rating | 182 1 0210 160 | 182 1 0200 160 |

| List 2, the tariff does not depend on the special rating | 182 1 0210 160 | |

| Fines | ||

| List 1, tariff depends on special assessment | 182 1 0210 160 | 182 1 0200 160 |

| List 1, the tariff does not depend on the special rating | 182 1 0210 160 | |

| List 2, tariff depends on special rating | 182 1 0210 160 | 182 1 0200 160 |

| List 2, the tariff does not depend on the special rating | 182 1 0210 160 | |

Fines and mandatory payments

| Payment | KBK |

| Income from the provision of paid services | |

| Fee for providing information contained in the Unified State Register of Taxpayers | 182 1 1300 130 |

| Fee for providing information contained in the Unified State Register of Taxpayers (when applying through multifunctional centers) | 182 1 1300 130 |

| Fee for providing information and documents contained in the Unified State Register of Legal Entities and in the Unified State Register of Individual Entrepreneurs | 182 1 1300 130 |

| Fee for providing information and documents contained in the Unified State Register of Legal Entities and the Unified State Register of Individual Entrepreneurs (when applying through multifunctional centers) | 182 1 1300 130 |

| Fee for providing information from the register of disqualified persons | 182 1 1300 130 |

| Fee for providing information from the register of disqualified persons (when applying through multifunctional centers) | 182 1 1300 130 |

| Government duty | |

| State duty on cases considered in arbitration courts | 182 1 0800 110 |

| State duty for state registration of a legal entity, individuals as individual entrepreneurs (if the service is provided by tax authorities), changes made to the constituent documents of a legal entity, for state registration of liquidation of a legal entity and other legally significant actions | 182 1 0800 110 |

| State duty for state registration of a legal entity, individuals as individual entrepreneurs (if the service is provided by a multifunctional center) | 182 1 0800 110 |

| State duty for the right to use the names “Russia”, “Russian Federation” and words and phrases formed on their basis in the names of legal entities | 182 1 0800 110 |

| Payments for the use of natural resources | |

| Payment for emissions of pollutants into the atmospheric air by stationary facilities | 048 1 1200 120 or 048 1 1200 120 (if the payment administrator is a federal government agency) |

| Payment for emissions of pollutants into the atmospheric air by mobile objects | 048 1 1200 120 or 048 1 1200 120 (if the payment administrator is a federal government agency) |

| Payment for emissions of pollutants into water bodies | 048 1 1200 120 or 048 1 1200 120 (if the payment administrator is a federal government agency) |

| Fines and sanctions | |

| Monetary penalties (fines) for violation of laws on taxes and fees | 182 1 1600 140 |

| Monetary penalties (fines) for violation of legislation on the use of cash register equipment when making cash payments and (or) payments using payment cards | 182 1 1600 140 |

| Monetary penalties (fines) for administrative offenses in the field of taxes and fees provided for by the Code of the Russian Federation on Administrative Offenses | 182 1 1600 140 |

| Monetary penalties (fines) for violation of the procedure for handling cash, conducting cash transactions and failure to fulfill obligations to monitor compliance with the rules for conducting cash transactions | 182 1 1600 140 |

Features of KBK when paying transport tax

Transport tax is paid by all vehicle owners: legal entities, organizations and individuals. Its size depends on the amount of horsepower included in the engine power of the vehicle. This is a regional tax, so it must be paid to the budget of the region where the car is registered. But the tax return must be filed at the place of registration of the taxpayer.

Which KBK should an individual write?

Having received a notification of the transport fee from the Federal Tax Service, it must be paid using the specified details, while the KBK code in field 104 of the payment order has the following combination: 182 1 0600 110.

How do legal entities pay this tax?

For each vehicle registered to an organization, you must pay a tax, which can be calculated by multiplying the tax rate by the value of the tax base.

ATTENTION! In some cases, various coefficients are added to the formula (regional, for the cost of the car, etc.)

Legal entities are required to independently calculate the amount of transport tax, as well as report on its payment before February 1. Whether an advance payment is needed or the tax must be transferred all at once is decided by the regional tax authority.

Differences in payment of transport tax for organizations

For organizations, payment must be made in advance, unless otherwise specified at the regional level. The advance is paid every quarter after reporting for the previous one. The amount of tax that must be paid after February 1 is calculated by subtracting all advance payments made from the total amount of transport tax.

The KBK code for transport tax for legal entities has not changed since last year. If you are late in paying the tax, you will also have to pay a late fee. Arrears or non-payment of tax entail an inevitable fine.

Who does the transport tax apply to?

Transport tax is assessed on each person or organization that owns any means of transportation. Calculations are made based on certain criteria. It will apply to cars, planes, helicopters and water transport. The owner of such property is obliged to make transfers on time, once a year. For organizations, this period may seem more extended. They can make small advance payments throughout the tax season. Then they are summed up and a payment notification is sent to the client’s specified place of registration. Owners of a personal account can track the amount of tax and the date of its repayment on the website of the Federal Tax Service. On the nalog.ru page the user can find a calculator that will allow him to calculate everything independently. You can also use it to repay the principal amount and pay 18210604011022100110 KBK. What tax is this? It applies to those who are late or have forgotten to pay the transport fee on time. You can gain access to your personal account only after completing an application to the Federal Tax Service. They review the application and send login information after a certain period of time. You can also recover a lost login or password only after visiting the Federal Tax Service. Those who have gained access to their personal account on the official website of the tax service will be removed from the notification mailing list, since all data will be displayed on one page, and the user will be able to choose the appropriate date or time for payment in installments or in one payment.

The law for paying taxes has quite broad concepts. It clearly states the cars that will or will not participate in the repayment of the fee. The funds collected in this way go to improve the quality of roads and the environment. Certain categories of persons are exempt from paying transport tax. This list includes owners of cars that are equipped for use by the disabled. Also cars with a power of less than 100 l/s that are stolen, vehicles used in agricultural work, and owners of cars of federal state or executive authorities.

KBK 2021

Order of the Ministry of Finance of Russia dated June 8, 2021 No. 132n “On approval of the Procedure for the formation and application of budget classification codes of the Russian Federation” approved a new procedure for the formation and application of budget classification codes of the Russian Federation, which will begin to operate from 01/01/2019.

KBK on taxes for 2021

| Payment Description | KBK |

| Income tax credited to the federal budget | 182 1 0100 110 |

| Income tax credited to the regional budget | 182 1 0100 110 |

| VAT (except import) | 182 1 0300 110 |

| Property tax | 182 1 0600 110 |

| simplified tax system with the object “income” | 182 1 0500 110 |

| simplified tax system with the object “income minus expenses” | 182 1 0500 110 |

| UTII | 182 1 0500 110 |

| Unified agricultural tax | 182 1 0500 110 |

| Personal income tax for a tax agent | 182 1 0100 110 |

| Transport tax | 182 1 0600 110 |

| Land tax from plots of Moscow, St. Petersburg, Sevastopol | 182 1 0600 110 |

KBK for 2021 for payment of penalties on taxes

| Payment Description | KBK |

| Income tax credited to the federal budget | 182 1 0100 110 |

| Income tax credited to the regional budget | 182 1 0100 110 |

| VAT | 182 1 0300 110 |

| Property tax | 182 1 0600 110 |

| simplified tax system with the object “income” | 182 1 0500 110 |

| simplified tax system with the object “income minus expenses” | 182 1 0500 110 |

| UTII | 182 1 0500 110 |

| Unified agricultural tax | 182 1 0500 110 |

| Personal income tax for a tax agent | 182 1 0100 110 |

| Transport tax | 182 1 0600 110 |

| Land tax for plots of Moscow, St. Petersburg, Sevastopol | 182 1 0600 110 |

KBK for 2021 to pay tax fines

| Payment Description | KBK |

| Income tax credited to the federal budget | 182 1 0100 110 |

| Income tax credited to the regional budget | 182 1 0100 110 |

| VAT | 182 1 0300 110 |

| Property tax | 182 1 0600 110 |

| simplified tax system with the object “income” | 182 1 0500 110 |

| simplified tax system with the object “income minus expenses” | 182 1 0500 110 |

| UTII | 182 1 0500 110 |

| Unified agricultural tax | 182 1 0500 110 |

| Personal income tax for a tax agent | 182 1 0100 110 |

| Transport tax | 182 1 0600 110 |

| Land tax for plots of Moscow, St. Petersburg, Sevastopol | 182 1 0600 110 |

KBK 2021 for insurance premiums

| Payment Description | KBK |

| Pension contributions at basic and reduced rates | 182 1 0210 160 |

| Pension contributions at an additional tariff that does not depend on the special assessment (list 1) | 182 1 0210 160 |

| Pension contributions at an additional tariff depending on the special assessment (list 1) | 182 1 0220 160 |

| Pension contributions at an additional tariff that does not depend on the special assessment (list 2) | 182 1 0210 160 |

| Pension contributions at an additional tariff depending on the special assessment (list 2) | 182 1 0220 160 |

| Contributions to compulsory medical insurance | 182 1 0213 160 |

| Contributions for temporary disability and maternity | 182 1 0210 160 |

| Contributions for injuries | 393 1 0200 160 |

KBK 2021 for payment of penalties on insurance premiums

| Payment Description | KBK |

| Pension contributions at basic and reduced rates | 182 1 0210 160 |

| Pension contributions at an additional tariff that does not depend on the special assessment (list 1) | 182 1 0210 160 |

| Pension contributions at an additional tariff depending on the special assessment (list 1) | 182 1 0210 160 |

| Pension contributions at an additional tariff that does not depend on the special assessment (list 2) | 182 1 0210 160 |

| Pension contributions at an additional tariff depending on the special assessment (list 2) | 182 1 0210 160 |

| Contributions to compulsory medical insurance | 182 1 0213 160 |

| Contributions for temporary disability and maternity | 182 1 0210 160 |

| Contributions for injuries | 393 1 0200 160 |

KBK 2021 for payment of fines on insurance premiums

| Payment Description | KBK |

| Pension contributions at basic and reduced rates | 182 1 0210 160 |

| Pension contributions at an additional tariff that does not depend on the special assessment (list 1) | 182 1 0210 160 |

| Pension contributions at an additional tariff depending on the special assessment (list 1) | 182 1 0210 160 |

| Pension contributions at an additional tariff that does not depend on the special assessment (list 2) | 182 1 0210 160 |

| Pension contributions at an additional tariff depending on the special assessment (list 2) | 182 1 0210 160 |

| Contributions to compulsory medical insurance | 182 1 0213 160 |

| Contributions for temporary disability and maternity | 182 1 0210 160 |

| Contributions for injuries | 393 1 0200 160 |

KBK 2021 for contributions for individual entrepreneurs (for oneself)

| Payment Description | KBK for payment of contributions | KBC for payment of penalties | KBC for payment of fines |

| Contributions in a fixed amount to an insurance pension (from income within 300,000 rubles) | 182 1 0210 160 | 182 1 0210 160 | 182 1 0210 160 |

| Contributions to the FFOMS in a fixed amount | 182 1 0213 160 | 182 1 0213 160 | 182 1 0213 160 |

KBC from January 1, 2021

KBK for insurance premiums for employees

| Payment type | KBK | |

| contributions for periods up to 2021 | contributions for 2017-2018 | |

Pension contributions | ||

| Contributions | 182 1 0200 160 | 182 1 0210 160 |

| Penalty | 182 1 0200 160 | 182 1 0210 160 |

| Fines | 182 1 0200 160 | 182 1 0210 160 |

Contributions for temporary disability and maternity | ||

| Contributions | 182 1 0200 160 | 182 1 0210 160 |

| Penalty | 182 1 0200 160 | 182 1 0210 160 |

| Fines | 182 1 0200 160 | 182 1 0210 160 |

| Contributions for injuries | ||

| Contributions | 393 1 0200 160 | 393 1 0200 160 |

| Penalty | 393 1 0200 160 | 393 1 0200 160 |

| Fines | 393 1 0200 160 | 393 1 0200 160 |

Contributions to compulsory medical insurance | ||

| Contributions | 182 1 0211 160 | 182 1 0213 160 |

| Penalty | 182 1 0211 160 | 182 1 0213 160 |

| Fines | 182 1 0211 160 | 182 1 0213 160 |

KBC for insurance premiums for 2021 (for individual entrepreneurs)

| Pension contributions | KBK for periods up to 2021 | KBC for 2017-2018 |

| Fixed contributions to the Pension Fund based on the minimum wage | 182 1 0200 160 | 182 1 0210 160 |

| Contributions at a rate of 1% on income over 300,000 rubles. | 182 1 0200 160 | 182 1 0210 1601 |

| Penalty | 182 1 0200 160 | 182 1 0210 160 |

| Fines | 182 1 0200 160 | 182 1 0210 160 |

Contributions to compulsory medical insurance | ||

| Contributions | 182 1 0211 160 | 182 1 0213 160 |

| Penalty | 182 1 0211 160 | 182 1 0213 160 |

| Fines | 182 1 0211 160 | 182 1 0213 160 |

KBC for insurance premiums at additional rates

| Additional pension contributions at tariff 1 | ||

| Contributions | 182 1 02 02131 06 1010 160 (tariff does not depend on the result of the special assessment) 182 1 02 02131 06 1020 160 (tariff depends on the result of the special assessment) | |

| Penalty | 182 1 02 02131 06 2100160 | 182 1 02 02131 06 2100160 |

| Fines | 182 1 02 02131 06 3000 160 | 182 1 02 02131 06 3000 160 |

| Additional pension contributions at tariff 2 | ||

| Contributions | 182 1 02 02132 06 1010 160 (tariff does not depend on the result of the special assessment) 182 1 02 02132 06 1020 160 (tariff depends on the result of the special assessment) | |

| Penalty | 182 1 02 02132 06 2100 160 | 182 1 02 02132 06 2100 160 |

| Fines | 182 1 02 02132 06 3000 160 | 182 1 02 02132 06 3000 160 |

Personal income tax 2021 on employee income (for organizations and individual entrepreneurs)

| Personal income tax on employee income | 182 1 0100 110 |

| Penalties on employee income tax | 182 1 0100 110 |

| Penalties for employee income tax | 182 1 0100 110 |

| Personal income tax for individual entrepreneurs on OSN | 182 1 0100 110 |

| Penalties for individual entrepreneurs on OSN | 182 1 0100 110 |

| Fines for individual entrepreneurs on OSN | 182 1 0100 110 |

KBK 2021 for VAT payment

| Payment Description | Mandatory payment | Penalty | Fines |

| VAT on goods (work, services) sold in Russia | 182 1 0300 110 | 182 1 0300 110 | 182 1 0300 110 |

| VAT on goods imported into Russia (from the Republics of Belarus and Kazakhstan) | 182 1 0400 110 | 182 1 0400 110 | 182 1 0400 110 |

| VAT on goods imported into Russia (payment administrator - Federal Customs Service of Russia) | 153 1 0400 110 | 153 1 0400 110 | 153 1 0400 110 |

BCC 2021 on property tax for legal entities

| Purpose of payment | Mandatory payment | Penalty | Fine |

| for property not included in the Unified Gas Supply System | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| for property included in the Unified Gas Supply System | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

KBK for payment of transport tax in 2021

| Purpose of payment | Mandatory payment | Penalty | Fine |

| for legal entities | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

| for individuals | 182 1 0600 110 | 182 1 0600 110 | 182 1 0600 110 |

KBK for simplified tax system – 2021 (income)

| Purpose of payment | KBK |

| Advances and tax for the object “income” | 182 1 0500 110 |

| Penalties for the object “income” | 182 1 0500 110 |

| Fines for the object “income” | 182 1 0500 110 |

KBK for simplified tax system – 2021 (income minus expenses)

| Purpose of payment | KBK |

| Advances, tax and minimum tax for the object “income minus expenses” | 182 1 0500 110 |

| Penalties for the object “income minus expenses” | 182 1 0500 110 |

| Fines for the object “income minus expenses” | 182 1 0500 110 |

KBK for UTII

BCC for the patent taxation system (for individual entrepreneurs)

KBK for payment of land tax

KBK for payment of trade tax

KBK 2021 for payment of state duty

KBK 2021 for payment of fines, sanctions, damages

The article was written and posted on January 30, 2012. Added - 12/20/2012, 01/10/2013, 01/08/2014, 01/11/2015, 01/15/2016, 12/16/2016, 08/24/2018, 10/12/2018, 01/09/2020 ATTENTION! Copying the article without providing a direct link is prohibited. Changes to the article are possible only with the permission of the author. |

Error in the KBK transport tax in 2021 for legal entities

To fill out a payment order for the transfer of transport tax in 2021, legal entities should use only valid BCCs. If the KBK incorrectly indicates the transport tax, the tax will still be considered paid: tax authorities will not be able to charge additional penalties and fines for the error in the KBK. However, if you indicate the wrong budget classification code on the payment slip, problems may arise with the payment. You will need to clarify the payment.

The payment date is considered to be the initial payment of the tax. If the deadline for the initial payment is met, there should be no penalties. Already accrued penalties must be canceled from the moment the tax office receives an application from the taxpayer organization. To avoid such problems, check the KBK when filling out the payment form.

What happens if you fail to pay transport tax?

Payment of transport tax is mandatory not only for individuals, but also for organizations that own a car or other type of vehicle. And if for some reason the timely receipt of tax funds to the budget was not carried out, then the organization, like an individual, will expect the same punishment, namely the accrual of penalties, which will then have to be paid according to the KBK code 18210604011022100110.

Of course, only a few know about this code, namely those who had to personally face the payment of penalties accrued for late payment of transport tax. Only in this situation does the KBK code 18210604011022100110 become known, what tax applies to it and when it should be paid. You can easily avoid troubles with penalties, as well as using this code; to do this, you only need to pay the tax accrued for the vehicle on time.

Each region provides a sufficient period for payment of taxes. At the moment, the last day for an organization when it can legally pay tax without any negative consequences is October 1 of the year following the previous annual period. This means that, for example, for 2015, tax payment will be made in 2021. But if the tax payment was not made within the specified period, then this amount will be collected from the organization.

What tax do you need to pay under KBK 18210604011022100110

Every person who is registered in the Russian Federation and owns a vehicle needs to be well acquainted with the rules written down in the Tax Code for paying the transport tax. No matter how conscientious a payer he is, any person may encounter unforeseen circumstances, which causes a delay in payment. In this case, penalties, fines and interest will be charged. They must be transferred to specific numbers.

- Who does the transport tax apply to?

- What are the criteria taken into account for its accrual?

- 18210604011022100110 KBK what tax?

Collection procedure

After the end of the period when the organization was supposed to pay the tax, it receives a notification about the presence of debt and accrued penalties. In this situation, to quickly end this trouble, the best choice would be to make a late payment of tax and accrued penalties. To do this, in the special payment documents used, in addition to the recipient’s personal account, the BCC must also be correctly indicated. To pay the tax it will be 18210604011021000110, and for penalties it will be 18210604011022100110.

Only in this case will the funds be received at the right address, and in the near future the tax authorities will not make themselves known. But if all notifications and demands coming from the tax service regarding the payment of tax and the penalty accrued due to its absence are ignored by the organization. Then, after the expiration of the deadline allocated by the tax authorities for their payment, they submit an application for collection of the required amount to the court. Although it is worth noting that such a turn of events awaits only those organizations whose total debt will be at least 3,000 rubles.

The application is submitted only six months after the date on which the deadline specified by the tax authorities for paying the tax expired. In this situation, the tax amount is collected from the organization’s property. The entire collection process is carried out sequentially. First of all, collection is carried out from funds in the organization’s bank account. This also applies to currency in electronic form.

If the collected funds do not repay the existing debt, then the remaining amount of the arrears is subsequently collected against the property. Property transferred under an agreement to a person who does not have rights to own it, and a previously concluded agreement was terminated to pay the debt, is subject to seizure. Other types of property that are not household items or things intended for individual use are also subject to arrest. The only exceptions are jewelry and antiques.

Yes, transport for many is an important element in everyday life. But paying taxes is his constant companion. Therefore, when deciding to use a car or any other transport, you should immediately be prepared to pay the tax, otherwise KBK 18210604011022100110, or even a trial cannot be avoided.

Decoding KBK 18210604011021000110

Transport tax is a regional tax that is introduced by regional authorities. The fee is required to be paid by both individuals and legal entities. Each category of payer contributes tax funds according to the appropriate code. The BCC for transport tax in 2021 for legal entities is also valid in the current year 2019. Organizations pay this fee only for those vehicles that are registered and accounted for as main vehicles.

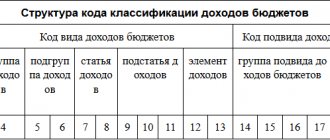

KBK 18210604011021000110 is the code for payment of transport tax for legal entities. The cipher consists of 20 digits, divided into seven combinations, each of which determines:

- 182 - agency administering the payment: tax office.

- 1 — category of receipts: payments.

- 06 - type of fees: property taxes.

- 04011 - tax subcategory, budget to which the funds are sent: transport tax for legal entities to the regional budget.

- 02 - specific budget: budget of a constituent entity of the Russian Federation.

- 1000 - definition of receipts: standard payment.

- 110 - clarification of income: tax receipts. This category also includes customs payments.