There are often cases when the accounting department accidentally overestimated the amount of a certain tax in the entries and contributed more funds to the budget than expected. If you decide to start returning these funds, then find out well whether you have even the slightest debts on other fees.

According to Article No. 78 and Clause No. 6, the overpaid amount will not be returned to you until all arrears are repaid in its amount. And only after paying all tax debts will you be able to receive the remaining difference.

A repayment against another unpaid tax occurs if the overpaid and outstanding fees relate to the same type of payment. For example, if you overpaid VAT, then with this overpayment you can only pay off the federal tax, because that’s what value added tax is. Hence, unpaid fees can be reimbursed if they belong to the same group of payments together with the excess payment; there are 3 types in total:

Why is reconciliation with the counterparty necessary?

The legislation on accounting or tax accounting does not contain requirements for cases when reconciliation should be mandatory. It can be carried out:

- as part of the inventory of calculations and obligations when preparing the annual report;

- upon expiration of the contract to close settlements under it;

- to confirm accounts payable or receivable by the counterparty in order not to miss the statute of limitations for collection;

- to formalize the offset of mutual claims with a counterparty with whom you have several agreements, under which there are both receivables and payables;

- in other cases.

In addition, timely reconciliation of accounting data with the counterparty will help to avoid accounting errors. After all, if the debt according to your data and the data of the counterparty coincides, it means that all business transactions for this counterparty are correctly reflected in the accounting: there are no unrecorded acts or “double” payments. If the reconciliation reveals discrepancies, obviously one of the parties must adjust the debt.

Reflection of tax write-offs and refunds in transactions

All data on tax payments made must be on analytical account No. 68. In order to divide each fee separately, account No. 68 is scattered into several sub-accounts, where each individual account corresponds to a specific tax.

- Offset of overpayment of tax fees in favor of repayment of another,

- Penalty debts,

- Debts on fines should be reflected in subaccount No. 68.

To correctly create a debit posting, indicate the subaccount on which the debt arose, and for a credit – the subaccount with the identified overpayment.

Another point of view is also allowed when, with a tax offset, a third order of sub-accounts is opened, for example: 68.02.1.

Postings for overpayment of taxes and their refund:

Good afternoon Tell me, how can I adjust the balance of taxes according to Kt in accounting, which has been going on for a long time, but does not correspond to the balances according to the reconciliation with the budget?

Get another secret bonus and full access to the BukhExpert8 help system for 14 days free of charge

Reconciliation period

The parties themselves agree on the period for which they will check.

To confirm accounts receivable and accounts payable in the annual balance sheet, you need to reconcile the calendar year.

It is possible that reconciliations with the counterparty have already been carried out, in which case the period for the new one begins when the previous one ended. In this case, the debt from the previous one will be reflected as a debt at the beginning of a new reconciliation.

If the parties have been cooperating for several years under several contracts, and the need for reconciliation has arisen only in the current period, it can be carried out in several stages to facilitate the process.

Additional taxes

Taxes assessed by inspectors during an audit are, in fact, errors discovered. They need to be corrected in accounting depending on the period to which they relate.

If these are taxes for the current year, then they must be accrued on the date of the audit decision.

If taxes relate to last year, and the annual balance has not yet been approved, then the additional accrual must be shown in December of last year.

If additional accruals relate to previous periods, the reporting for which has already been approved, then the accountant will have to figure out whether the amount is significant.

For minor errors, a rule is established: they are shown on the date of detection (in this case, on the date of the inspection decision). Minor errors should be reflected as losses from previous years identified in the reporting period in the debit of account 91 (in the case of income tax - in the debit of account 99).

As for significant errors, they should be shown in the debit of account 84 and the comparative indicators of previous years should be recalculated in the reporting for the current period. This is the requirement of PBU 22/2010 “Correcting errors in accounting and reporting.” In addition, different taxes have their own accounting subtleties. Let's consider each of them separately.

We suggest you read: How to calculate income tax on wages if you have 3 children

Preparation of adjustment entries

During the transformation, there is a need to draw up adjustment entries that eliminate the identified differences between IFRS and the current accounting system in Russia. There are two types of adjustment entries:

- Adjusting entries relating to the reporting period are necessary to reflect inconsistencies in the company's business transactions for the reporting period in relation to IFRS. Adjusting entries are entered into the trial balance at the end of the reporting period and are charged to the account of retained earnings (uncovered loss) of the reporting period.

- Adjusting entries relating to prior periods are required to reflect inconsistencies in the recording of historical transactions under IFRS. These adjusting entries are entered into the trial balances at the beginning and end of the reporting period and are charged to the account of retained earnings (uncovered losses) of previous years.

For the purpose of monitoring adjusting entries made during the transformation process, it is recommended to allocate two additional accounts in the current Russian Chart of Accounts:

- account 84.11 “Adjustments to retained earnings/uncovered losses of the reporting period” - for grouping adjusting entries by events related to the reporting period;

- account 84.12 “Adjustments to retained earnings/uncovered losses of previous years” - for grouping adjustment entries by events of previous years.

If at the beginning of the reporting period an adjusting entry was made affecting account 84.12, then this entry must be repeated at the end of the reporting period so that the balance of retained earnings of previous years in the balance sheet at the beginning and end of the reporting period is the same.

Adjustments associated with the transition to the IFRS accrual method

In accordance with IFRS, financial statements must be prepared and presented on an accrual basis. In accrual accounting, income and expenses are recorded when they are made, not when the cash is paid or received.

To prepare adjustment entries you must:

a) Based on the analysis of the enterprise’s accounting information, it is necessary to identify income and expenses for the reporting period that were not reflected in the reporting period.

Unaccrued income and expenses that relate to the current period must be adjusted to account 84.11 “Adjustments to retained earnings/uncovered loss of the reporting period.”

Income and expenses received or paid during the current year, but relating to the previous year, must be separated from the profit of the current year, adjusted to account 84.12 “Adjustments to retained earnings/uncovered losses of previous years.”

These income and expenses may include:

- Wages of workers and salaries of employees;

- Payroll taxes;

- Utility and telephone expenses;

- Unpaid overhead;

- Interest on loans;

- Interest income;

- Income in the form of dividends, etc.

Show entire table

| Account name | Debit | Credit |

| Adjustments to retained earnings/uncovered losses of the reporting period (previous years) | 84.11/84.12 | |

| Interest on short-term and long-term loans and borrowings | 66.2/67.2 | |

| Calculations for social insurance and security | 69 | |

| Staff payroll calculations | 70 | |

| Settlements with various debtors and creditors | 76 | |

| Settlements with various debtors and creditors | 76 | |

| Adjustments to retained earnings/uncovered losses of the reporting period (previous years) | 84.11/84.12 | |

| Additional accrual of income and expenses of the reporting period (previous years) is made. |

b) Carefully study the information on account 45 “Goods shipped” and determine whether there is a balance on the account. Determine according to the score:

- whether the goods are for sale, and whether the seller bears the risks and rewards for these goods. This means that in the event of loss of goods or any event leading to a decrease in the value of the goods, the seller in possession of the goods is liable.

To convert accounts to accrual accounting, make the following entry:

Show entire table

| Account name | Debit | Credit |

| Finished products (at actual cost) or Goods (at acquisition cost) Goods shipped | 43 41 | 45 |

| Balances on account 45 are transferred to the inventory accounts |

- whether the goods are for sale, and whether the buyer bears the risks and rewards for these goods (i.e. the buyer has an obligation). This means that in the event of loss of goods or any event leading to a decrease in the value of the goods, the buyer in possession of the goods is responsible for them.

In this case, make the following entries:

Step I – write-off of goods in transit at cost

Show entire table

| Account name | Debit | Credit |

| Adjustments to undistributed loss of the reporting period | 84.11 | |

| Adjustments to unallocated losses from prior years | 84.12 | |

| Goods shipped profit/uncovered profit/uncovered | 45 | |

| Cost of goods in transit |

Step II – recognition of sales revenue

Show entire table

| Account name | Debit | Credit |

| Settlements with buyers and customers | 62 | |

| Adjustments to retained earnings/uncovered losses of the reporting period | 84.11 | |

| Adjustments to retained earnings/uncovered losses from prior years | 84.12 | |

| Revenues from sales |

Step III – recognition of VAT obligations

Show entire table

| Account name | Debit | Credit |

| Adjustments to retained earnings/uncovered losses of the reporting period | 84.11 | |

| Adjustments to retained earnings/uncovered losses from prior years | 84.12 | |

| Calculations for taxes and duties (VAT) | 68.(VAT) | |

| VAT due from the buyer has been taken into account |

As a result of the transactions described above, a procedure is carried out to recognize sales revenue and the cost of goods sold that were sold, but were considered as shipped goods (in transit).

c) If the company is engaged in construction and installation work, then it is necessary to reconsider the recognition of revenue from work in progress. Study the information on account 20 “Main production” and determine whether there is a balance on the account. Based on contract performance analysis, determine:

- The outcome of the contract can be reliably assessed.

Revenues and expenses should be recognized by reference to the stage of completion of the contract at the reporting date. In this case, the percentage of work completion method determines the amount of income and expenses that must be recognized in the reporting period;- The outcome of the contract cannot be reliably assessed, but costs will be recovered.

Revenue should be recognized only to the extent that the costs incurred under the contract are likely to be recovered. Contract costs should be recognized as an expense in the period in which they are incurred.

To convert accounts to accrual accounting, make the following entries:

Step I – recognition of revenue from unfinished contracts:

Show entire table

| Account name | Debit | Credit |

| Settlements with buyers and customers | 62 | |

| Adjustments to retained earnings/uncovered losses of the reporting period | 84.11 | |

| Adjustments to retained earnings/uncovered losses from prior years | 84.12 | |

| Revenue is recognized using the percentage of completion method (or the amount of reimbursable costs) |

Step II - reflection of the cost of unfinished contracts:

Show entire table

| Account name | Debit | Credit |

| Adjustments to retained earnings/uncovered losses of the reporting period | 84.11 | |

| Adjustments to retained earnings/uncovered losses from prior years | 84.12 | |

| Primary production | 20 | |

| The cost is reflected using the method of percentage of work completed (or in the amount of costs incurred) |

Step III – recognition of VAT obligations

Show entire table

| Account name | Debit | Credit |

| Adjustments to retained earnings/uncovered losses of the reporting period | 84.11 | |

| Adjustments to retained earnings/uncovered losses from prior years | 84.12 | |

| Calculations for taxes and duties (VAT) | 68.(VAT) | |

| VAT due from the buyer has been taken into account |

- If it is not probable that the costs will be recovered, then the expected losses should be recognized immediately. To do this, recognize losses under contract agreements:

Show entire table

| Account name | Debit | Credit |

| Adjustments to retained earnings/uncovered losses of the reporting period | 84.11 | |

| Adjustments to retained earnings/uncovered losses from prior years | 84.12 | |

| Primary production | 20 | |

| Losses are recognized for unfinished work contracts |

Account 01 “Fixed Assets”, 02 “Depreciation of Fixed Assets”, 03 “Profitable Investments in Material Assets”, 07 “Equipment for Installation”, 08 “Investments in Non-Current Assets”

a) Based on the analysis of accounting information, it is necessary to identify assets that do not meet the definition and conditions for recognition of assets under IFRS. These assets (for example, library collections) should be written off as expenses for the reporting period/previous years.

According to IFRS, capitalization of subsequent costs occurs if it is probable that future economic benefits will flow in excess of the initial productivity of fixed assets. As a result of the analysis of accounting information for account 08, it is necessary to determine the possibility of capitalizing costs or make a decision to attribute them to expenses of the reporting period / previous years.

Show entire table

| Account name | Debit | Credit |

| Adjustments to retained earnings/uncovered losses of the reporting period (previous years) | 84.11/84.12 | |

| Accounts for non-current assets | 01;07;08.X | |

| Non-current assets that do not meet the definition of assets are written off |

b) When analyzing information, special attention must be paid to housing facilities. According to the current accounting rules for fixed assets (PBU 6/01), accounting for depreciation of the housing stock should be carried out on off-balance sheet account 010 “Depreciation of fixed assets.” According to IFRS requirements, the amount of depreciation for the housing stock must be accrued by reducing retained earnings/uncovered losses of the reporting period (previous years).

Show entire table

| Account name | Debit | Credit |

| Depreciation of fixed assets | 02 | |

| Adjustments to retained earnings/uncovered losses of the reporting period (previous years) | 84.11/84.12 | |

| Depreciation is calculated on housing assets |

Account 04 “Intangible assets”

As part of intangible assets, Russian organizations take into account intellectual property, organizational expenses, business reputation, etc. In accordance with IFRS, not all of the above assets are classified as intangible assets. Intangible assets that do not meet the definition and conditions for recognizing assets under IFRS should be expensed in the reporting period (previous years).

Show entire table

| Account name | Debit | Credit |

| Adjustments to retained earnings/uncovered losses of the reporting period (previous years) | 84.11/84.12 | |

| Amortization of intangible assets | 05 | |

| Intangible assets | 04 | |

| Intangible assets that do not meet the definition of assets are written off |

Account 10 “Materials”

When switching to the new Chart of Accounts, most enterprises wrote off the MPB to subaccount 10.9 “Inventory and household supplies.” And if, in this subaccount as part of other materials, property that does not meet the definition of assets is taken into account, then it must be written off as an expense for the period.

Show entire table

| Account name | Debit | Credit |

| Adjustments to retained earnings/uncovered losses of the reporting period (previous years) | 84.11/84.12 | |

| Materials | 10.X | |

| Materials that do not meet the definition of assets are written off |

Account 14 “Reserves for reduction in the value of material assets”

According to IFRS, provisions for reduction in the value of material assets are not formed. Raw materials and supplies in inventories are not written down below cost if the finished goods in which they are included are expected to be sold at or above cost. In this case, the profit of the reporting period (previous years) should be restored to the amount of the balance in the “Reserves for reduction in the value of material assets” account.

Show entire table

| Account name | Debit | Credit |

| Reserves for reduction in the value of material assets | 14 | |

| Adjustments to retained earnings/uncovered losses of the reporting period (previous years) | 84.11/84.12 | |

| The amount of the reserve for reducing the value of material assets is written off |

If the cost of finished products is expected to exceed the possible net sales price, then the cost of the corresponding inventory items should be reduced by the amount of the balance on this account:

Show entire table

| Account name | Debit | Credit |

| Reserves for reduction in the value of material assets Materials | 14 | 10.X |

| Inventories are written off to net realizable value |

Account 15 “Procurement and acquisition of material assets”

The balance of account 15 “Procurement and acquisition of material assets” shows the presence of inventories in transit belonging to the enterprise. According to IFRS requirements, balances on account 15 must be transferred to account 10 “Materials”.

Show entire table

| Account name | Debit | Credit |

| Materials | 10.X | |

| Procurement and acquisition of material assets | 15 | |

| Expenses associated with the procurement and purchase of materials are written off |

Removing general administrative expenses from inventory balances

In accordance with IFRS 2 “Inventories”, the cost of inventory must include all acquisition costs, processing costs and other costs incurred directly in moving and bringing the products into proper condition.

In Russian accounting practice, enterprises sometimes include general business expenses in the value of inventory balances. It is necessary to analyze all balances of work in progress (WP) and finished goods (GP) and draw up an adjustment entry to remove general and administrative expenses from the balances of GP and FP and include them in the expenses of the period. In this regard, it is necessary:

a) Calculate the % of general and administrative expenses included in the cost of production. The percentage of general and administrative expenses in the cost price can be calculated as the ratio of general and administrative expenses (account 26 turnover) accrued for the period to the sum of all expenses allocated to production (account 20 debit) for the same period:

general and administrative expenses (turnover of account 26) / Cost of production (debit of account 20) x 100% = 2. The percentage of general and administrative expenses in the cost of production

b) Calculate the share of general and administrative expenses in the balances of finished products:

The amount of balances of finished products xZ%-Xgp

Amount of general and administrative expenses to be removed from SOE balances

c) Calculate the share of general and administrative expenses in the balance of work in progress:

The sum of the balances of unfinished production xZ%-Xnzp

The amount of general and administrative expenses to be removed from the balances of NP

d) Adjust the balances of work in progress and finished goods:

Work in progress – Xnzp = Y – balance of NEP at the end of the period

Finished products – Xgp = Y – inventory balance at the end of the period.

d.) We draw up an adjustment entry to remove general and administrative expenses from the cost of inventories:

Show entire table

| Account name | Debit | Credit |

| Adjustments to retained earnings/uncovered losses of the reporting period (previous years) | 84.11/84.12 | |

| Primary production | 20 | |

| Finished products | 43 | |

| General business expenses are derived from the value of inventory balances |

The method of deducing general and administrative expenses from the balances on accounts 21 - “Semi-finished products of own production”, 23 - “Auxiliary production” is similar.

Account 42 “Trade margin”

According to IFRS, goods must be reflected in accounting records at the lower of two values: cost of acquisition and possible net selling price. Therefore, it is necessary to reduce the cost of the corresponding goods recorded in account 41 “Goods” by the amount of the trade margin.

Show entire table

| Account name | Debit | Credit |

| Trade margin | 42 | |

| Goods | 41 | |

| The cost of inventory items is reduced by the amount of the trade margin |

Account 44 “Sales expenses”

Transportation costs accounted for on account 44 “Sales expenses” should be considered as expenses of the period, except for the case where these expenses can be directly attributed to certain inventory items.

Balances in account 44 “Sales expenses” are written off to account 41 “Goods”, if their occurrence is related to purchased goods, or as expenses of the reporting period (previous years), if they can be attributed to expenses associated with the sale of goods.

Show entire table

| Account name | Debit | Credit |

| Selling expenses | 44 | |

| Goods | 41 | |

| Adjustments to retained earnings/uncovered losses of the reporting period (previous years) | 84.11/84.12 | |

| Account balance 44 is written off |

Account 46 “Completed stages of unfinished work”

This account summarizes information about stages of work completed in accordance with concluded contracts that have independent significance. In accordance with the requirements of IFRS, for the cost of completed stages of work paid by the customer, it is necessary to reduce the debt on account 62 “Settlements with buyers and customers” for the relevant counterparties:

Show entire table

| Account name | Debit | Credit |

| Settlements with buyers and customers | 62 | |

| Completed stages of unfinished work | 46 | |

| Account balance 46 is written off |

Account 50 "Cashier"

In the Chart of Accounts, subaccount 50.3 is intended for accounting for monetary documents. It is necessary to analyze subaccount 50.3 “Cash documents” by type of document. IFRS does not contain the concept of monetary documents, so the balance must be written off to account 97 “Deferred expenses”. However, if the account contains documents that do not meet the definition of an asset and the company does not expect to receive economic benefits from them in the future, then they must be written off as expenses for the corresponding period.

Show entire table

| Account name | Debit | Credit |

| Adjustments to retained earnings/uncovered losses of the reporting period (previous years) | 84.11/84.12 | |

| Future expenses | 97 | |

| Money documents | 50.3 | |

| Cash documents written off |

Account 51 “Currency accounts” and account 52 “Currency accounts”

It is necessary to analyze the balances on accounts 51, 52. If the amount of balances on account 51, 52 includes cash balances in “bankrupt banks”, then these amounts must be written off as expenses as not satisfying the definition and conditions for recognition of assets under IFRS.

Show entire table

| Account name | Debit | Credit |

| Adjustments to retained earnings/uncovered losses of the reporting period (previous years) | 84.11/84.12 | |

| Current accounts | 51 | |

| Currency accounts | 52 | |

| Money written off in “bankrupt banks” |

Account 57 “Transfers on the way”

If there are balances on account 57, then, based on the analysis of available documents, the balance amount should be added to the balances on accounts 51 and 52.

Show entire table

| Account name | Debit | Credit |

| Transfers on the way | 57 | |

| Current accounts | 52 | |

| Currency accounts | 51 | |

| The amount of the account balance is written off for transfers in transit |

Account 58 “Financial investments, account 59 “Reserves for impairment of investments in securities”

Based on the analysis of accounting information, the balances of accounts 58 and 59 should be divided into 2 categories in order to comply with IFRS requirements:

- Investments in joint ventures, associates and subsidiaries;

- Financial assets: Financial assets held for trading (assets purchased for the purpose of profiting from short-term price fluctuations or dealer margins);

- Held-to-maturity investments (financial assets with fixed or determinable payments and fixed maturities that an entity has the positive intention and ability to hold to maturity);

- Financial assets available for sale (other financial assets).

After initial recognition, an entity should measure financial assets (held for trading; available for sale) at their fair value plus transaction costs.

If the enterprise has created a reserve for the impairment of these financial assets, then it is necessary to reduce the carrying value of these securities by the amount of the previously created reserve.

Show entire table

| Account name | Debit | Credit |

| Provisions for impairment of investments in securities | 59.X | |

| Financial investments | 58.X | |

| The carrying amount of financial assets has been reduced to fair value |

Financial assets that are not measured at fair value (held-to-maturity investments; any other financial assets without a quoted market price) must be measured at cost or amortized cost using the effective interest method.

If the enterprise has created a reserve for the impairment of these financial assets, then the following adjustment entry must be made:

Show entire table

| Account name | Debit | Credit |

| Provisions for impairment of investments in securities | 59.X | |

| Adjustments to retained earnings/uncovered losses of the reporting period (previous years) | 84.11/84.12 | |

| The amount of the reserve is written off to income |

Account 60 “Settlements with suppliers and contractors”

It is necessary to conduct an inventory of the organization's accounts payable according to the timing of its occurrence and identify those that are unrealistic for collection (for example, the statute of limitations has passed or the organization has gone bankrupt).

Show entire table

| Account name | Debit | Credit |

| Settlements with suppliers and contractors | 60.X | |

| Adjustments to retained earnings/uncovered losses of the reporting period (previous years) | 84.11/84.12 | |

| Uncollectible accounts payable written off |

Account 62 “Settlements with buyers and customers”

It is necessary to conduct an inventory of the organization's receivables according to the timing of their occurrence. A reserve must be created for doubtful accounts receivable. According to the principle of prudence, in conditions of uncertainty, assets or income should not be overstated, and liabilities or expenses should not be understated. The amount of the created reserve is included in the expenses of the organization.

Show entire table

| Account name | Debit | Credit |

| Adjustments to retained earnings/uncovered losses of the reporting period (previous years) | 84.11/84.12 | |

| Provisions for doubtful debts | 63 | |

| A reserve for doubtful debts has been created |

Account 76 “Settlements with various debtors and creditors”

On this account, most Russian enterprises take into account VAT on advances received for future supplies of goods, performance of work, and provision of services. According to IFRS requirements, advances received from buyers and customers must be accounted for in full, including VAT. Therefore, it is necessary to include the balance on the “VAT” subaccount in the amount of the corresponding advance payments on account 62.

Show entire table

| Account name | Debit | Credit |

| Settlements with various debtors and creditors (VAT sub-account) | 76.X | |

| Settlements with buyers and customers (advances received) | 62.X | |

| VAT amount written off |

Account 86 “Targeted financing”

The unused balance of target funds that are not subject to return and for which there are no obligations to fulfill must be written off as income of the reporting period (previous years)

Show entire table

| Account name | Debit | Credit |

| Special-purpose financing | 86 | |

| Adjustments to retained earnings/uncovered losses of the reporting period (previous years) | 84.11/84.12 | |

| Unused balances of target funds that are not subject to return are written off |

Account 94 “Shortages and losses from damage to valuables”

Based on the analysis of accounting information, it is necessary to identify compensable shortages and losses from damage to valuables, which should be transferred to account 73 for the relevant guilty parties. Shortages and losses from damage to valuables that are not subject to compensation must be written off as expenses of the reporting period (previous years)

Show entire table

| Account name | Debit | Credit |

| Settlements with personnel for other operations | 73 | |

| Shortages and losses from damage to valuables | 94 | |

| Adjustments to retained earnings/uncovered losses of the reporting period (previous years) | 84.11/84.12 | |

| Shortages and losses from damage to valuables are written off |

Account 98 “Deferred income”

Based on the analysis of accounting information, it is necessary to identify all gratuitous receipts and, in accordance with IFRS, recognize them as income for the period in which they were actually received; it is also necessary to identify future receipts of debt for shortfalls reflected in this account and recognize them as income of previous years. To do this, you need to make the following adjustment entry:

Show entire table

| Account name | Debit | Credit |

| revenue of the future periods | 98.X | |

| Adjustments to retained earnings/uncovered losses of the reporting period (previous years) | 84.11/84.12 | |

| Gratuitous receipts are recognized as income for the period in which they are actually received |

Previous part | Contents | Next part

Documenting

There are no legal requirements for registration of reconciliations. In already established practice, this procedure occurs by signing a reconciliation act for mutual settlements. In this document, the parties include all transactions that were carried out by them during the reconciled period, indicating the dates of their completion, the amounts of transactions, links to supporting documents, the amount of debt of each party is displayed and, if any, discrepancies between the data are recorded.

The form is developed by each organization and approved as an appendix to the accounting policy. In addition, in automated accounting programs this form is already programmed and the report is generated automatically when you select the desired counterparty, specific contracts (if necessary) and specify the reconciliation period.

Income tax

There are only two reasons why inspectors charge additional income tax: either income is underestimated or expenses are overstated. Accordingly, based on the results of the audit, the accountant needs to correct the situation: cancel “extra” expenses or show missing income.

When adjusting expenses, keep the following in mind. Since costs were underestimated in the previous tax period, no corrections need to be made in the current year’s tax accounting. There is also no need to submit an updated declaration, because the inspectors have already assessed an additional amount of tax and reflected it in the budget settlement card.

Sometimes expenses that are not accepted in tax accounting need to be canceled in accounting (for example, if depreciation of fixed assets is incorrectly calculated). Then in the accounting of the current period it is necessary to show the profit of previous years. Because of this, a permanent negative difference is formed, which generates a permanent tax asset (PTA).

More often than not, costs canceled in tax accounting can be retained in accounting. In particular, this applies to amounts transferred to the accounts of dubious counterparties, which the auditors considered “fly-by-night”. In this case, there will be no adjustments in the accounting of the current period.

Income from previous periods should be adjusted according to the same rules as expenses. Thus, there is no need to make any corrections in the tax accounting of the current period (as well as submit an “update”).

If income is also underestimated in accounting, then in the current period it is necessary to reflect the profit of previous years and show a permanent tax asset. If income is formed correctly in accounting, then there will be no adjustments in the current period (see table).

Income tax adjustments and entries

| Reason for additional income tax assessment | Adjustments to current period accounting | |||

| Expenses of the previous tax period were not accepted into the NU, but were saved in the accounting system | ||||

| Expenses of the previous tax period were not accepted either in NU or BU | The accounting system shows the profit of previous years and the conditional income tax expense | |||

| Income of the previous tax period is underestimated in the tax accounting system, but is taken into account in the accounting system | ||||

| Income from the previous tax period is underestimated in both NU and BU | The accounting system shows the profit of previous years and the conditional income tax expense | |||

Adjustment of sales from previous years

Now let's look at how adjustments to sales from previous years are reflected in accounting and tax accounting. Let's change the conditions of the previous example:

Example 2

| Information about the discovery of a defect in the product by the buyer was received by Romashka LLC in May 2021 after submitting a tax return under the simplified tax system and after signing the financial statements for 2016. The organization makes the necessary changes to the accounting and tax records and submits an updated tax return under the simplified tax system for 2021 to the tax authority. |

In this case, on the Calculations tab of the Sales Adjustment document, you need to set the flag Last year’s accounting is closed for adjustment (the reporting is signed) and indicate the item of other income and expenses, for example, Profit (loss) of previous years.

After posting the Sales Adjustment document with the specified settings, the following accounting entries will be generated:

Debit 41.01 Credit 91.01 - for the amount of other income identified as a result of adjusting the sale of goods (RUB 2,500.00); Debit 91.02 Credit 62.01 - for the amount of other expenses (RUB 5,000.00); Debit 62.01 Credit 62.02 - for the allocation of an advance received from the buyer (RUB 5,000.00).

The posting date corresponds to the date of the Sales Adjustment document (May 2021).

In tax accounting, compared to Example 1, nothing will change: in the register Book of Income and Expenses (Section I), expenses for the purchase of goods recognized in the previous period are reversed, and in Section I of the report Book of Income and Expenses of the simplified tax system for 2016, an entry the decrease in consumption is reflected in the last line. But, unlike Example 1, the declaration under the simplified tax system was submitted before the adjustments were made.

Since the expenses of the previous tax period were overestimated, and, therefore, the amount of tax was underestimated, the organization is obliged to submit an updated declaration under the simplified tax system for 2021.

When automatically filling out an updated tax return, the adjustment made will be reflected in the indicators in Section 2.2.

To additionally charge the tax paid in connection with the application of the simplified tax system, in connection with the increase in the tax base that occurred as a result of corrections made to tax accounting, during the period when the error was discovered (in May 2021), you need to enter an accounting entry into the program using the Operation document:

Debit 99.01.1 Credit 68.12 - for the amount of additional tax (2,500.00 x 15% = 375 rubles).

Such an entry needs to be made only if the amount of tax calculated for the tax period in the general manner (taking into account the adjustments made) exceeds the amount of the minimum tax.

If the due amounts of taxes are paid on time later than those established by the legislation on taxes and fees, then the organization must independently calculate and pay penalties (Clause 1 of Article 75 of the Tax Code of the Russian Federation).

If discrepancies are identified, why is there a need for adjustment?

Firstly, incorrect reflection of transactions in accounting, as well as their non-reflection, distorts information about the assets and liabilities of the organization, including in the financial statements. In this case, due to an accountant’s mistake, the business owner may receive incorrect information not only about his financial situation, but also about the organization’s property. Building a further business plan on such information is fraught with the ruin of the company.

Secondly, any error in accounting leads to a distortion of the tax base for any tax. This, in turn, becomes the reason for claims from the tax authorities in the form of additional taxes, penalties and fines. Inaccuracies that led not to an understatement, but to an overpayment of taxes, are also undesirable, because in this case the accountant unreasonably withdrew a certain amount of working capital from the company’s budget.

The accountant, based on the results of a reconciliation carried out with the counterparty after the approval of the annual statements, discovered that, according to the act with the counterparty for August last year, they capitalized the work performed instead of the 8,500 rubles indicated in the act. for 10,000 rubles. wiring:

- Dt 20 Kt 60 (reflected in work costs). This error did not affect any balance sheet or financial statement indicator;

- Dt 91 Kt 20 (work costs are recognized as expenses). The error affected the indicators “Retained earnings” (uncovered loss) of the balance sheet and “Net profit” (loss) of the financial results report.

We invite you to read: How to terminate a full liability agreement

Correcting:

- Dt 20 Kt 60 in the amount of 10,000 rubles. - reversal;

- Dt 20 Kt 60 in the amount of 8500 rubles. — reflected the correct amount in the reconciliation report;

- Dt 20 Kt 91 in the amount of 10,000 rubles. — the erroneous amount for work was restored from expenses;

- Dt 91 Kt 20 in the amount of 8500 rubles. — reflected the correct amount of costs according to the reconciliation report with the counterparty.

How to correct a significant error identified after approval of the reporting by the manager depends on whether it was identified before the approval of the reporting by the organization’s participants or after (clause 3 of PBU 22/2010).

Adjustment of expenses for the reporting year

Let's look at how in the 1C: Accounting 8 version 3.0 program you can correct a technical error made when registering a current year receipt document if the taxpayer uses a simplified taxation system with the object “Income minus expenses”.

Example 3

| In October 2021, Romashka LLC entered into a lease agreement for office space with the landlord. In the same month, Romashka LLC paid 200,000.00 rubles to the landlord. (including VAT 18%), of which RUB 100,000.00 is the rent for the fourth quarter, and 100,000.00 rubles. — security payment in the amount of RUB 100,000.00. In December 2021, the accounting records of Romashka LLC erroneously included the costs of renting office space in the amount of RUB 200,000.00. In February 2021, the error was discovered and corrected. Adjustments in the accounting of Romashka LLC were made before the submission of a tax return under the simplified tax system for 2021 and before the signing of the financial statements for 2021. |

The costs of renting office space are reflected in the program using the document Receipt (act, invoice) with the transaction type Services (act). As a result of the document, accounting entries were generated:

Debit 60.01 Credit 60.02 - for the amount of the offset prepayment for the rental of premises (RUB 200,000); Debit 26 Credit 60.01 - for the cost of renting the premises (200,000 rubles).

The amount of 200,000.00 is reflected in the register Book of Income and Expenses (Section I) as an expense of the simplified tax system.

To reflect accounting errors made by the user when registering primary documents received from the supplier, we will use the Receipt Adjustment document, which we will create based on the Receipt document (act, invoice).

The form of the document Adjustment of receipts on the Main tab is modified depending on the selected type of operation, as well as on the period of making changes to the basis document.

According to paragraph 6 of PBU 22/2010, an error in the reporting year identified after the end of this year, but before the date of signing the financial statements for this year, should be corrected by entries in the corresponding accounting accounts for December of the reporting year. Therefore, in our case, the Receipt Adjustment document should be dated December 2021 (from field).

On the Main tab, in the Operation type field, the following operations are available:

- Correction in primary documents;

- Adjustment by agreement of the parties;

- Correcting your own mistake. This operation is intended to correct data entry errors made by the user when registering primary documents and (or) a received invoice, and allows you to correct erroneously entered invoice details, including totals. The correction refers to the same period as the incorrectly entered document itself.

Since, according to the conditions of Example 3, a technical error was made in the organization’s accounting, it is necessary to select the type of operation Correction of own error (Fig. 3).

Rice. 3. Adjustment of receipts

The tabular part on the Services tab is filled in automatically based on the document specified in the Basis field. In the line after the change you need to indicate the corrected totals.

After posting the Receipt Adjustment document, the following accounting entries will be generated:

Debit 60.02 Credit 60.01 - for the resulting advance amount to the supplier (RUB 100,000.00), paid as a security payment; REVERSE Debit 26 Credit 60.01 - for erroneously inflating the cost of renting the premises (-RUB 100,000.00).

For the purposes of the tax paid in connection with the application of the simplified tax system, corrective entries are entered into the accumulation registers, the Book of Income and Expenses (Section I) and the Explanation of KUDiR.

In the register Book of Income and Expenses (Section I), the expense of the simplified tax system is reversed in the amount of 100,000.00 rubles, and in Section I of the Book of Income and Expenses of the simplified tax system for 2021, the entry about the decrease in expense is automatically reflected in chronological order by the date of the document Adjustment of receipts , that is, December 31, 2016.

Value added tax

The Tax Code does not provide a clear answer to the question of whether the amount of VAT accrued based on the results of an audit can be included in expenses when taxing profits.

According to officials, the amount of VAT can be included in expenses only in one case - if the company mistakenly accepted for deduction an amount that should have been included in the initial cost of goods (work, services) on the basis of Article 170 of the Tax Code of the Russian Federation. After the auditors cancel such a deduction, the accountant can write it off as an expense, provided that the cost of goods, work or services is taken into account when calculating income tax (a similar conclusion can be drawn from the letter of the Ministry of Finance of Russia dated 06/07/08 No. 03-07-11 /222).

In any other situations, inspectors do not allow additional VAT to be charged as expenses. As an argument, they refer to subparagraph 19 of Article 270 of the Tax Code of the Russian Federation. It states that it is not permissible to accept tax charged to the buyer as expenses. However, there is another opinion. According to it, VAT, like any other tax, refers to other expenses associated with production and sales.

If the organization nevertheless takes a cautious position and does not include additional VAT in “tax” costs, it will have to reflect a permanent tax liability in accounting.

How to fix

An entire PBU 22/2010 “Correcting Errors in Accounting and Reporting” is devoted to correcting errors in accounting. It gives the concept of an “error” and ways to correct it, which depend on the type (material, non-essential) and the moment of its detection: before or after signing the statements. The level of materiality is established by each enterprise in its accounting policies. Typically, errors that distort the value of any reporting line by 5% or more are considered significant.

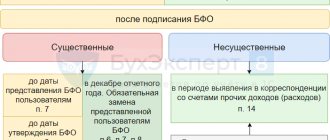

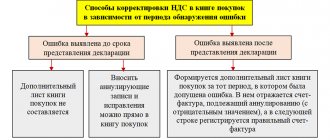

If an inaccuracy (material or insignificant) was made in the reporting year and was discovered before the statements were approved by the head of the organization, it must be corrected taking into account the following:

- if it is discovered before December 31 of the reporting year, adjusting entries are made on the date the error was discovered (clause 5 of PBU 22/2010);

- if identified on December 31 of the reporting year or later, adjusting entries are made on December 31 of the reporting year (clause 6 of PBU 22/2010).

To fix it you need:

- draw up an accounting certificate with the required content: when and what error was made, the date of its discovery, corrective entries;

- reverse incorrect entries;

- reflect the correct entries in accounting.

If, after signing the reporting, an insignificant error is identified, corrective entries are made on the date of its discovery (clause 14 of PBU 22/2010) by drawing up an accounting certificate, the contents of which are similar to those described above.

Depending on the impact of the error on the financial result, it should be corrected as follows:

- inaccuracies in accounting simultaneously affected the indicators “Retained earnings” (uncovered loss) of the balance sheet and “Net profit” (loss) of the financial results report. In this case, we make the posting opposite to the incorrect one, but in correspondence with the account. 91. The correct entry is also made in correspondence with account 91 (if necessary). For example, it was discovered that depreciation was erroneously calculated not for 9,000 rubles, but for 10,000 rubles. wiring Dt 20 Kt 02. We fix:

- Dt 02 Kt 91 in the amount of 10,000 rubles;

Dt 91 Kt 02 in the amount of 9000 rubles;

We suggest you read: Car tax upon inheritance

If the error did not affect any balance sheet or financial statement indicators, then there is no need to make corrections. For example, depreciation on capital production equipment is not accounted for. 20, and on the count. 26.

Be sure to do this in the tax register even if the distortion did not result in an understatement of tax.

If an error was identified from a previous period and it affected the tax amount or the tax base, we will correct it in the income tax return.

If an inaccuracy is identified for the current year, it can be corrected in the tax return of the next reporting period or for the year.

As a rule, errors from previous years are corrected by filing amended tax returns, but there are exceptions.

General principles for adjusting tax accounting

The general principles for adjusting tax accounting and reporting are set out in Articles 54 and 81 of the Tax Code of the Russian Federation and do not depend on the taxation system used - general or simplified.

In accordance with paragraph 1 of Article 81 of the Tax Code of the Russian Federation, a taxpayer who has discovered in the declaration submitted to the tax authority that information is not reflected or is incompletely reflected, as well as errors:

- is obliged to make the necessary changes to the tax return and submit an updated tax return to the tax authority if errors (distortions) led to an understatement of the amount of tax payable;

- has the right to make the necessary changes to the tax return and submit an updated tax return to the tax authority if errors (distortions) do not lead to an understatement of the amount of tax payable.

Errors (distortions) that did not lead to an understatement of the amount of tax payable when applying the simplified tax system include failure to reflect or understate expenses, as well as overstatement of income. And, of course, the taxpayer is interested in returning the overpayment of taxes resulting from these situations or offsetting them against future payments. This can be done by filing an amended return or, in some cases, by making changes to tax accounting data in the current period.

In the general case, errors (distortions) relating to previous tax (reporting) periods and discovered in the current tax (reporting) period are corrected by recalculating the tax base and the amount of tax for the period in which these errors (distortions) were committed (clause 1 Article 54 of the Tax Code of the Russian Federation).

At the same time, the taxpayer has the right to recalculate the tax base and tax amount in the tax (reporting) period in which errors (distortions) were identified if:

- it is impossible to determine the period of commission of these errors (distortions);

- such errors (distortions) led to excessive payment of tax.

When commenting on the taxpayer’s right to correct errors (distortions) in the current period, regulatory authorities draw attention to the fact of the existence of a tax base in the current period. If in the current reporting (tax) period the organization incurred a loss, then in this period recalculation of the tax base is impossible, since the tax base is recognized as equal to zero (clause 8 of Article 274 of the Tax Code of the Russian Federation, letter of the Ministry of Finance of Russia dated March 24, 2017 No. 03-03-06 /1/17177).

As for the condition of excessive payment of tax in the previous period, then, according to the Russian Ministry of Finance, it is not met if in the specified period the organization incurred a loss or the tax base was equal to zero. Therefore, in such situations, corrections must be made during the period of the error (letter dated 05/07/2010 No. 03-02-07/1-225).

The explanations given relate to the adjustment of the tax base for income tax. Despite this, we believe that under the simplified tax system it is also impossible to “edit” tax accounting in the current period if an error in calculating the tax base was made in a “zero” or “unprofitable” declaration, or if a loss was incurred in the current period.

According to Article 346.24 of the Tax Code of the Russian Federation, tax accounting under the simplified tax system is the accounting of income and expenses in the book of income and expenses of organizations and individual entrepreneurs using the simplified taxation system (hereinafter referred to as KUDiR).

In “1C: Accounting 8”, the report Book of Income and Expenses of the simplified tax system (section Reports) is filled out automatically based on special accumulation registers. Entries in accounting registers for the purposes of the simplified tax system are entered, as a rule, automatically when posting documents that register business transactions. For manual registration of register entries, use the document Entry of the book of income and expenses (STS) (section Operations - STS).

The date of receipt of income is the day of receipt of funds, as well as the day of payment to the taxpayer in another way - the cash method (clause 1 of Article 346.17 of the Tax Code of the Russian Federation).

The procedure for recognizing expenses depends on the conditions set out in paragraph 2 of Article 346.17 of the Tax Code of the Russian Federation, mandatory of which is their actual payment.

Thus, when correcting errors (distortions) made when reflecting (non-reflecting) business transactions in the accounting of an organization using the simplified tax system, tax accounting is adjusted in accordance with the provisions of Article 346.17 of the Tax Code of the Russian Federation, that is, taking into account the payment factor.

Property tax, transport and land taxes

Amounts of arrears for property tax, transport or land tax identified during the audit reduce the taxable base for profit (subclause 1, clause 1, article 264 of the Tax Code of the Russian Federation). It happens that auditors themselves reflect this in their decision. But more often accountants have to create costs and recalculate the taxable base.

The easiest way is to include additional accrued amounts in the expenses of the current tax period. In accounting, they should also be shown in the costs of the current year as of the date of the inspection decision. There will be no difference between tax and accounting accounting.