IT and SHE: what is it and how to calculate

Deferred tax assets (DTA) and deferred tax liabilities (DTL) are special concepts introduced into the accounting system to reflect the differences between accounting and tax profits.

The article “Calculating the difference between accounting and tax profit” will tell you why such differences arise.

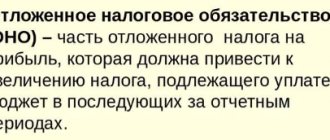

How accounting legislation deciphers the terms ONA and ONO, see the figure:

SHE and IT are determined based on the size of temporary differences, due to which differences arise between accounting and tax profits. The difference arises due to the fact that certain expenses and income are recognized in accounting in the reporting tax period, and in tax accounting in the next period and vice versa. To calculate the amount of SHE and IT, you need to multiply the temporary difference by the income tax rate.

What changes in income tax await us:

- “The list of income on which it is not necessary to pay income tax has been added”;

- “Disputes around the income tax rate: one less reason.”

Correct calculation of discrepancies in the amount of accounting and tax profits allows you to generate reliable indicators in reporting, as well as determine the amount of tax payments for the current and subsequent periods.

Reasons for the occurrence of taxable temporary differences

When taxable temporary differences result in taxable profit (loss), this gives rise to deferred income tax, which, in turn, will increase the amount of income tax payable to the budget in the year following the reporting period or in the subsequent year. Let's look at the reasons why taxable temporary differences may arise:

- The use by an enterprise accountant of different procedures for reflecting the interest that the company pays to creditors for the use of borrowed funds for tax and accounting purposes.

- Recognition in the reporting period of income from the sale of manufactured products, goods, services and works in the form of income from ordinary activities.

- Application of various methods of calculating depreciation for calculating income tax and accounting purposes.

- Recognition of interest income of a company for accounting purposes based on the assumption of temporary certainty of facts of economic activity, and for tax purposes - on a cash basis.

- Other similar differences between accounting and tax accounting.

Which entry should be used to record the amount of tax liabilities and assets?

SHE and IT are reflected in accounting in two ways:

- As differences arise in accounting and tax accounting;

- At the time of calculation of income tax at the end of the year or reporting period.

The first method is typical for automated accounting programs. The second method is used in conditions of manual calculations for income tax.

How the amount of a deferred tax asset can be reflected - the posting links the following accounting accounts:

How the amount of deferred tax liability can be reflected - the posting is as follows:

Thus, different accounting accounts are provided for ONO and ONA. At the same time, all information about the value of these indicators is collected in one subaccount “Calculations for income tax” to account 68. As a result, SHE and IT participate in determining the final amount of the current income tax.

The latest clarifications on legislative innovations can be found on our website:

- “Land tax: changes 2019”;

- “Starting from 2021, the sale of part of the property of individual entrepreneurs will be preferential”;

- “The deduction for Plato is cancelled.”

Examples of ONA postings on account 09

To consider the features of accounting for transactions on account 09, we will analyze examples.

Posting for accrual of deferred tax asset

At the end of the 3rd quarter of 2015, 3 batches of materials (spare parts for electrical equipment) were delivered to the warehouse of Marker JSC for a total amount of 484,300 rubles, VAT 73,876 rubles. Payment for spare parts was made partially - in the amount of 232,500 rubles, VAT 35,466 rubles.

To reflect the amounts of IT in accounting, the accountant of Marker JSC made the following calculations:

Based on the above calculations, the following entries were made in the accounting of Marker JSC:

| Dt | CT | Description | Sum | Document |

| 10 | 60 | Spare parts have arrived at the Marker JSC warehouse (RUB 484,300 - RUB 73,876) | RUR 410,424 | Packing list |

| 19 | 60 | The amount of VAT on purchased spare parts is taken into account | RUR 73,876 | Invoice |

| 60 | 51 | Funds were transferred to the supplier to partially repay the debt for supplied spare parts | 232,500 rub. | Payment order |

| 60 | 60 Deductible temporary differences | The amount of the deductible temporary difference is reflected | RUR 213,390 | Accounting certificate-calculation |

| 09 | 68 Income tax | The increase in the amount of IT is taken into account (RUB 213,390 * 20%) | RUR 42,678 | Accounting certificate-calculation |

Write-off ONA

In April 2021, Bogatyr JSC sold a unit of production equipment. As of the date of sale, the amount of depreciation accrued on the equipment amounted to RUB 42,300. (accounting) and 39,800 rub. (tax accounting). The amount of IT for this object is 895 rubles.

When writing off equipment, the accountant of Bogatyr JSC will make the following entry:

| Dt | CT | Description | Sum | Document |

| 99 | 09 | The amount of ONA for sold equipment is written off | 895 rub. | OS write-off act |

Adjustment of the amount of ONA

From 01/01/2016 for Metropol JSC the income tax rate was reduced from 24% to 20%. The balance sheet of JSC Metropol as of December 31, 2015 on Dt 09 includes the amount of 64,900 rubles. The accountant recalculated the amount of ONA (64,900 rubles / 24% * 20% = 54,083 rubles) and made the following entry in accounting account 09:

| Dt | CT | Description | Sum | Document |

| 84 | 09 | The ONA has been adjusted (RUB 64,900 - RUB 54,083) | RUB 10,817 | Accounting certificate-calculation |

Reflection of ONA in case of loss received

The Profit and Loss Statement and Tax Return of JSC Sever contains the following information:

| Index | Data based on the results of 2015 | Data based on the results of the 1st quarter of 2021 | Data based on the results of the 2nd quarter of 2016 |

| Profit and loss statement (accounting) | Loss 181,300 rub. | Profit 211,400 rub. | Profit 53,200 rub. |

| Tax return (tax accounting) | Loss 181,300 rub. | Profit 211,400 rub. | Profit 53,200 rub. |

Based on the above information, the following entries were made in the accounting of JSC Sever to repay the deferred tax asset:

| Dt | CT | Description | Sum | Document |

| 68 Income tax | 99 Income from income tax (conditional) | The amount of conditional income at the end of 2015 is taken into account (RUB 181,300 * 20%) | RUR 36,260 | Accounting certificate-calculation |

| 09 | 68 Income tax | The amount of ONA from the resulting loss was taken into account at the end of 2015 | RUR 36,260 | Accounting certificate-calculation |

| 99 Income from income tax (conditional) | 68 Income tax | The amount of conditional income tax accrued for the 1st quarter of 2021 is reflected (RUB 211,400 * 20%) | RUB 42,280 | Accounting certificate-calculation |

| 68 Income tax | 09 | The amount of OTA from the loss was repaid | RUR 36,260 | Accounting certificate-calculation |

| 99 Income from income tax (conditional) | 68 Income tax | Reversal of conditional income tax accrued for the 1st quarter of 2016 | RUB 42,280 | Accounting certificate-calculation |

| 68 Income tax | 09 | The amount of ONA from the loss for 2015 was restored | RUR 36,260 | Accounting certificate-calculation |

| 99 Income from income tax (conditional) | 68 Income tax | The amount of conditional income tax accrued for the 1st half of 2021 is reflected (RUB 53,200 * 20%) | RUB 10,640 | Accounting certificate-calculation |

| 68 Income tax | 09 | The amount of OTA from the loss reducing taxable profit has been repaid | 10.640 | Accounting certificate-calculation |

Who does not need to understand the entries for accounting for deferred tax assets and liabilities

Organizations that are legally allowed to submit simplified reporting and keep records according to simplified rules, as well as a number of other entities, may not apply PBU 18/02 and, therefore, not reflect IT and ONA in accounting:

If NPOs, Skolkovo residents and small businesses decide to voluntarily apply PBU 18/02, they have the right to do so. The legislation does not contain any prohibitions in this regard. They need to consolidate their intention in their accounting policies.

Whether NPOs submit reports using the SZV-M form, we tell you here.

Will the accounting treatment of deferred tax assets and liabilities change in 2019-2020?

Taxpayers applying PBU 18/02 or planning to do so in the future should pay attention to the order of the Ministry of Finance of Russia “On Amendments...” dated November 20, 2018 No. 236n. He made adjustments to PBU 18/02, which are applied from reporting for 2021. Early application of the updated version of this PBU is also allowed if the taxpayer wants to introduce changes to accounting practices starting next year (clause 2 of Order No. 236n).

What are the adjustments:

- changes affected the terms used in the text;

- the list of temporary differences has been expanded;

- the composition of the information reflected in the reporting has been changed, etc.

We informed you about these changes in one of our publications.

Do the amendments affect the procedure for reflecting ONA and ONO in accounting? Do the current postings change due to adjustments to the accounting regulations? Law No. 236n does not contain any instructions for changing the entries used in accounting. Consequently, the wiring diagram for ONA and ONO remains the same.

Results

The posting for the reflection of a deferred tax asset is made to the debit of account 09 “Deferred tax assets” and the credit of the sub-account “Calculations for income tax” to account 68. The same sub-account corresponds by debit with the credit of account 77 “Deferred tax liabilities”, if it is formed in the accounting deferred tax liability.

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Example of formation of line 1420 “Deferred tax liabilities”

Let's analyze the situation with filling out line 1420 of the Balance Sheet using the example of a hypothetical commercial organization Smart Finance LLC. It is known that management made a decision to reflect the amount of deferred tax assets/liabilities in expanded form. The indicators for accounts 77 and 09 in the company’s accounting are as follows:

Fragment of the Balance Sheet for 2013:

If it were decided to show deferred tax liabilities/assets on a net basis:

The solution of the problem.

- If a company chooses to report the net amount of deferred tax assets/liabilities on its balance sheet:

The balance of deferred tax assets/liabilities as of December 31, 2014 will be equal to:

66 tr. – 396 tr. = -330 tr.

Since the amount of deferred tax assets turned out to be less than the amount of deferred tax liabilities, column 4 on page 1420 will indicate the amount of the excess, namely 330 tr.

Fragment of the Balance Sheet for this case:

- If the company reflects the amount of deferred tax assets (it will not roll up the balance on accounts 77 and 09):

The amount of deferred tax liabilities as of December 31, 2014 will be equal to 396 tr.

Fragment of the Balance Sheet: