Documentation

Of course, an organization can provide for the payment of one-time bonuses, including for special occasions, in internal documents:

- employment contract (paragraph 5, part 2, article 57 of the Labor Code of the Russian Federation);

- collective agreement (part 2 of article 135 of the Labor Code of the Russian Federation);

- a special local regulatory act, for example, the Regulations on Bonuses (Part 2 of Article 135, Article 8 of the Labor Code of the Russian Federation).

Such bonuses are part of the organization's labor system. However, much more often, anniversary bonuses are awarded by order of the head of the company. The basis for calculating a bonus is an order to reward an employee or group of employees (forms No. T-11 and No. T-11a, respectively).

The anniversary bonus is paid by bank transfer or according to a payroll slip or cash order (clauses 4.1, 6 of Bank of Russia Directive No. 3210-U dated March 11, 2014).

The calculation of average earnings includes only those bonuses that are provided for by the remuneration system (clause 2 of the Regulations, approved by Government Decree No. 922 of December 24, 2007). Therefore, the anniversary bonus is included in the calculation of average earnings only if this condition is met.

As for the reflection of bonuses in accounting, non-production one-time bonuses are classified as other expenses (clause 11 of PBU 10/99). They are charged as follows:

- Dt 91-2 Kt 70 – bonus accrued at the expense of other expenses.

If the bonus is paid from retained earnings, the posting will be the same:

- Dt 91-2 Kt 70 – bonus accrued at the expense of net profit.

Accrual procedure

The procedure for calculating such a bonus is simple, but requires coordinated actions of employees of several departments (we talked about the principle and how bonuses are calculated to employees in a separate article).

Registration and maintenance of personal files of employees is one of the main functions of the HR department. As a rule, it is the personnel officer who monitors employee anniversaries and launches the mechanism for calculating anniversary bonuses.

Preparation of papers

Payment of incentives to an employee requires documentation for further taxation. Article 252 of the Tax Code of the Russian Federation requires documentary support for the company's expenses; confirmation is required in the form of a link to the clause of the collective agreement or labor agreement regulating incentives.

Issuing funds to an employee

The incentive payment system must comply with Article 191 of the Labor Code. Bonus payments that are not related to the labor process can be paid directly on the anniversary day, and not with the rest of the salary.

Registration of the procedure

Registration of the incentive involves the following steps:

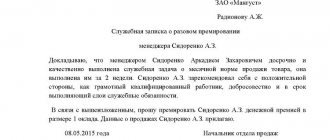

- drawing up a memo with a proposal to reward the employee, the essence and amount of the awarded bonus;

- agreeing on the payment amount with the accounting department to ensure it is available by a specific date;

- submitting the paper for consideration to the head of the company;

- execution of an order for bonuses based on a signed memo, as required by Resolution of the State Statistics Committee of the Russian Federation No. 1 (January 2004);

- solemn congratulations to the employee;

- confirmation of the fact of familiarization with the paper (signing);

- making a record of bonuses in the company personnel records.

Petition

The purpose of the petition for an anniversary payment is to encourage management to pay the bonus. Given the absence of a template, it is written in free form with the following structure:

- title “Application for bonus No.”;

- day, month, year of paper submission;

- information about the employee nominated for the award (example: V.V. Andreev, freight forwarder, has been continuously working at Parma LLC for 10 years, all this time he has been a reliable professional employee, an example for colleagues, and has taken part in training young people);

- bonus motive (example: for impeccable work and for the 55th anniversary);

- type and amount of incentive (example: I propose to reward V.V. Andreev with a cash bonus in the amount of 15,000);

- signature of the applicant (example: head of department R.N. Sorokin).

The petition is characterized by an expanded approach to the bonus motive. The document emphasizes the employee’s personal and professional qualities and special merits.

You can learn more about how to correctly write a request for a bonus for an employee, as well as see a sample document here.

Service memo

ATTENTION! A variant of the document addressed to the director with a request for a bonus for the hero of the day is a memo. It can be submitted by the head of the unit or the chairman of the organization's trade union.

The memo is written in the following format:

- “header”, reflecting the details of the head of the enterprise to whom it is addressed, and information about the originator;

- the name of the document in the middle of the sheet “Memo on bonuses”;

- the text of the note, including a proposal for encouragement in the form of a bonus (example: for 15 years, senior inspector Semenkevich E.A. has proven herself to be a competent and efficient specialist, which is confirmed by bonuses and certificates from management. I ask for impeccable work and in connection with the 50th anniversary award Semenkevich E.A. the company’s gold insignia and a bonus in accordance with the collective agreement);

- date of filing the note;

- signature of the compiler (example: head of personnel service Tsoi A.V.).

Position

The provision on bonuses (Article 135 of the Labor Code) does not apply to the company’s mandatory documents, but is often developed due to its usefulness:

- it is more convenient to adopt a single document regulating the incentive system without overloading employee contracts;

- the fact of having a bonus paper stimulates employees to improve their work results;

- The provision serves as documentary justification and confirmation of expenses for employee incentives, allowing to reduce the amount subject to income tax.

The regulation determines the procedure for calculating incentive payments:

- bonus conditions;

- amounts of payments;

- list of employees covered by the document;

- frequency, timing and sources of payments;

- procedure for issuing incentives;

- persons responsible for making decisions on incentives;

- bonus rules.

You can find out how to draw up an order approving the bonus regulations here.

Order of encouragement

REFERENCE! An order to award an employee a bonus is issued on the basis of the submitted proposal and contains a note about the decision made and a deadline for execution. The hero of the day must be familiarized with the order against signature.

We talked more about how to fill out an employee incentive application using the sample for paying a bonus in this article.

To draw up an order, the T-11 form has been developed, but it is also permissible to issue it in free form, indicating:

- Date and place of compilation.

- Details of the hero of the day.

- Reasons for bonuses (example: for long-term and conscientious work and to commemorate an anniversary). You can view the list of reasons for paying bonuses here.

- Type of incentive (example: I order you to declare gratitude with an entry in the work book and award a bonus in the amount of 20,000 rubles).

- Grounds for the order (example: based on the petition for incentives dated June 22, 2012 No. 12).

- Signature of the manager with transcript.

We talked in detail about how to draw up an order for bonuses for an employee here.

Taxes

Personal income tax must be withheld from the premium amount. This rule must be strictly followed by all employers (clause 1 of article 208 of the Tax Code of the Russian Federation). Is the anniversary bonus subject to insurance premiums? Of course, the amount of the one-time bonus must be credited:

contributions for compulsory pension, social, medical insurance (Article 420 of the Tax Code of the Russian Federation); contributions for insurance against accidents and occupational diseases (clause 1, article 20.1 of the Federal Law of July 24, 1998 No. 125-FZ). This should be done regardless of whether the anniversary bonus is provided for in the employment contract with the employee or not.

When calculating income tax, the anniversary bonus cannot be taken into account. In order for such costs to be included in the tax base, the bonus must relate to incentive payments and depend on labor performance (clause 2 of Article 255 of the Tax Code of the Russian Federation, letter of the Ministry of Finance dated March 15, 2013 No. 03-03-10/7999, Federal Tax Service dated August 13 .2014 No. GD-4-3/157

Read also

29.07.2016

How is the size calculated?

ATTENTION! The incentive can be assigned as a percentage of the employee’s salary or in a specific monetary amount. The percentage of salary format is convenient because there is no need to index the amount specified in the document.

Specifying a range between the lower and upper limits of the amount allows you to differentiate bonuses depending on the age and salary of the employee.

You can find out more about the calculation of the bonus, its size, and what its maximum value is here.

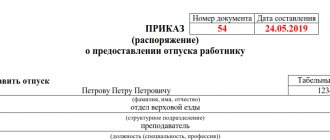

Orders in form T-11 and T-11a

The form can be drawn up according to the standard form T-11, approved by the State Statistics Committee (but not currently mandatory for use), or in free form. The organization has the right to develop its own sample.

Form T-11 is used if one employee needs to receive a bonus.

If several employees are worthy of a bonus, a collective agreement is issued in form T-11a.

Document structure:

- a header containing the details of the organization and the document (name of the enterprise, number, date of issue of the order, its subject);

- the main part with written documentation of the employer’s order and its basis;

- final (signatures, their transcripts, there must be a note about the employee’s familiarization).

The main part must indicate:

- who exactly is being rewarded (full last name, first name and patronymic, personnel number, department and position held);

- what the bonus is for (indication of specific achievements, merits or other reasons). For example, the following formulations are often used: “in connection with the anniversary”, “for production successes”, “for professionalism and processing”, etc.;

- the amount of remuneration or the procedure for determining it;

- the period for which the allowance is made.

How to fill out an order if a company’s employees have been given a bonus (sample)

To issue an order for bonuses, there are unified forms approved by Resolution of the State Statistics Committee of the Russian Federation dated January 5, 2004 No. 1:

- T-11, issued when awarding bonuses to one employee;

- T-11a, compiled with the encouragement of a group of workers.

However, these forms are not mandatory for use and nothing prevents the employer from issuing such orders using a form developed independently.

The basis for issuing an order will be:

- the results of the distribution of regular (systematic) bonuses approved by the head of the organization;

- a memorandum with a positive resolution from the head of the organization regarding the nomination of an employee for an irregular (one-time) bonus.

A sample of filling out an order for bonuses, drawn up on form T-11, can be seen on our website.

Insurance payments

Article 20.1 of Law No. 125-FZ indicates the mandatory nature of insurance contributions from labor accruals.

Since all issues of company employees are regulated by an employment contract, holiday incentives fall under this definition.

An alternative point of view is also possible.

The counter-argument in the dispute about whether the bonus paid is related to the work will be that the size of the anniversary bonus does not depend either on the position or on the volume and quality of the work performed. Judicial practice on this matter is ambiguous; it is not possible to determine the outcome of the hearing in absentia in this case.

Are there any differences in the concepts of “monetary remuneration” and “wages”

The term "cash reward" can be applied to any payment made in money, regardless of its purpose. That is, it can be either remuneration for work or any other payment. Additional incentive payments made for the employee’s labor achievements are part of the salary and, when issued in cash, are regarded as monetary rewards issued as payment for labor.

But in addition to payments related to labor achievements, the employer can use other additional payments that are not determined by the employee’s labor functions. Usually they are one-time in nature and do not have a regular accrual period. An example of such additional payments are bonuses paid for anniversaries or holidays. They fully correspond to the term “monetary remuneration not related to wages.”

Employee birthday bonus income tax

The date of personal income tax withholding is considered to be the day the bonus amount is paid in cash at the campaign cash desk or the day it is transferred to a bank account. From the funds received, income tax and insurance payments are calculated and the money is transferred to the treasury. Note: Those bonuses that are specified in Decree of the Government of the Russian Federation No. 89 of February 6, 2001 are exempt from taxation.

These are prizes in the fields of science, education, culture and technology. In addition to personal income tax, the premium is subject to the costs of insurance premiums. Art. 7 FZ-212 establishes that any deductions under an employment agreement are subject to payments to the extra-budgetary funds of the Pension Fund, Compulsory Medical Insurance Fund, Social Insurance Fund. The accountant makes the deduction on the day of actual issuance of the legal bonus.

Results

One of the components of the remuneration system can be incentive payments.

The main role among these payments is given to bonuses. Bonuses can be regular or one-time, expensed and paid out of net profit. But they are taxed according to the same rules with the calculation of personal income tax and insurance contributions. Payment of the premium must be formalized by order. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Incentive payments (bonuses) as a form of payment for work

The current labor legislation (Article 129 of the Labor Code of the Russian Federation) allows the employer to establish a wage system consisting of several parts:

- payments for work performed in accordance with job duties;

- compensatory payments taking into account the conditions in which work is carried out;

- additional incentive payments designed to increase employee interest in work.

By adopting such a remuneration system, the employer has the opportunity to:

- influence the employee’s interest in the results of his activities;

- regulate the amount of labor costs taken into account when calculating the income tax base.

The types of bonuses and remunerations used as additional incentive payments are reflected in the internal regulations developed by the employer (Article 135 of the Labor Code of the Russian Federation). This act establishes:

- list of types of incentives used;

- conditions and frequency of their accrual;

- the circle of persons to whom each type of incentive applies;

- a list of indicators that allow an employee to qualify for appropriate remuneration and deprive him of such an opportunity;

- a system for assessing indicators giving the right to remuneration, the result of processing of which will be the monetary value of the remuneration;

- procedure for reviewing assessment results and challenging its results.

However, incentive additional payments, when included in the remuneration system, become mandatory for the employer if all conditions for applying the incentive are met.

For information on how an internal regulatory act on bonuses , read the article “Regulations on the remuneration of employees - sample 2019-2020”.