Normative base

Order of the Ministry of Finance of Russia dated October 6, 2008 N 106n “On approval of accounting regulations” (together with the “Accounting Regulations “Accounting Policy of the Organization” (PBU 1/2008)”, “Accounting Regulations “Changes in Estimated Values” (PBU 21/2008)")

Order of the Ministry of Finance of Russia dated July 29, 1998 N 34n “On approval of the Regulations on accounting and financial reporting in the Russian Federation”

Resolution of the State Statistics Committee of the Russian Federation dated August 18, 1998 N 88 “On approval of unified forms of primary accounting documentation for recording cash transactions and recording inventory results”

Resolution of the State Statistics Committee of the Russian Federation dated March 27, 2000 N 26 “On approval of the unified form of primary accounting documentation N INV-26 “Record of results identified by inventory”

Any organization conducts an inventory of material assets at least once a year. To do this, it is necessary to appoint a special commission from among authorized employees and issue an order to conduct an inventory. The procedure and schedule for conducting an inventory in an organization must be enshrined in the accounting policy for accounting purposes (clause 4 of PBU 1/2008). However, an inventory commission is created for each specific case. Its composition, powers, as well as the timing of the inventory must be enshrined in a separate internal act of the organization.

In budgetary organizations, through an inventory, it becomes possible to check the availability and condition of property. Compare property data since the last inspection with the results as of the current date, identify the nature and reasons for possible discrepancies. And based on the data obtained, evaluate the correctness and compliance of the accounting carried out at the enterprise. In general, the reasons and procedure for inventory in a budgetary and commercial organization are approximately the same.

Inventory in legislative regulations

The procedure for carrying out the activities that make up the inventory procedure is regulated by several regulations:

- Law of the Russian Federation dated December 6, 2011 No. 402-FZ “On Accounting”;

- Order of the Ministry of Finance of the Russian Federation No. 34n dated July 29, 1998 (as amended on April 11, 2018), which approved the Regulations on accounting;

- “Guidelines for inventory of property and liabilities”, approved by Order of the Ministry of Finance of the Russian Federation No. dated June 13, 1995;

In addition to the above-mentioned regulatory documents, the legislation prescribes that a business entity must include regulations for carrying out inventory activities in the accounting policy of the enterprise.

When is inventory needed?

A sample order for inventory is usually required in some cases listed in clause 27 of Order of the Ministry of Finance of the Russian Federation dated July 29, 1998 No. 34n, in particular:

- before drawing up the annual report;

- when appointing new financially responsible persons, including in connection with the transfer of property to third parties;

- after thefts or natural or man-made emergencies (fires, floods, explosions, etc.).

Typically, the order to begin an inspection is issued by the head of the organization, either scheduled or unscheduled. The person responsible for such an event is usually the chief accountant or another accounting employee. A special commission is engaged in counting material assets, the members of which must be familiarized with the relevant local act upon signature.

What is needed for this?

The head of the organization issues an appropriate order, on the basis of which the composition of the inventory commission is formed. Its members must have the authority to verify the compliance of the funds actually available with the data reflected in the accounting records. This could be a merchandiser, an accountant, a quality control specialist, etc., the main thing is that the number of members in the commission is at least 3 people.

The accounting department is obliged to transfer to the members of the commission all accounting data on the product, fixed assets or inventory items that are subject to the inventory. Depending on what is being inventoried, these can be accounting registers, book balances, reports on the movement of inventory items.

If necessary, the inspection location may be sealed. The commission begins its work and verifies whether the actual availability of valuables corresponds to the quantity indicated in the accounting documents.

Inventory order form

The main document of the inventory process is the order. Therefore, we will consider it in more detail and learn how to compose this document correctly. A unified sample order for inventory for 2021 can be found in Resolution No. 88 of the State Statistics Committee of Russia dated August 18, 1998. Form No. INV-22 is a universal form that can be used by organizations of all forms of ownership. The form can be used both when conducting scheduled and unscheduled inspections of material assets.

Sample of filling out an order to conduct an inventory of 2021 in budgetary institutions

Form of order to conduct inventory according to form No. INV-22

If for some reason this form is not suitable, you can develop your own. The main thing is that it is enshrined in the company's accounting policy. An arbitrary sample order for inventory of material assets 2021 may look something like this:

In any case, the document must contain the following mandatory details and information:

- company name;

- date of preparation and document number;

- the purpose of the inspection and what it will concern: goods, fixed assets, tangible assets, accounts receivable, all property of the company;

- divisions and departments of the company in which the inspection will be carried out: warehouse, store, accounting or the entire company as a whole;

- period and duration of the event - from what date to what date, when to provide the results of verification actions;

- composition of the commission and full name its chairman (the commission, in addition to the company’s employees, can include third-party auditors);

- details of the manager who signed the document.

After publication, the local act must be registered in a special journal to record control over the implementation of such decisions. Its recommended form can be taken from Goskomstat Resolution No. 88 (Form No. INV-23) or developed independently. All employees listed in it must be familiarized with the order. They can sign the acquaintance directly on the form or on a separate sheet of acquaintance with the document, which is filed with the order.

Summarizing

After the commission has completed the inventory, a meeting is held. During it, the main results and identified discrepancies are determined. At the same time, the cause of the discrepancies and ways to correct the situation are determined. Based on the results, minutes of the meeting are drawn up. Typically this document has the following structure:

- name of the company indicating the organizational and legal form;

- the name of the unit where the inventory was carried out;

- name of the document - protocol of the inventory commission;

- list of commission members indicating surnames, initials and positions;

- description of the test results;

- list of speakers at the meeting;

- decision;

- conclusion of the commission;

- identified violations (if any);

- those responsible for the violation, indicating their surnames, initials and positions;

- information about measures to eliminate violations;

- signatures of the chairman and all members of the commission;

- applications.

As an illustration, we will give a variant of the protocol.

To easily draw up such a document, prepare the minutes of the meeting attached to the article.

The following documents are attached as appendices to the minutes of the meeting:

- acts and inventories of the inventory carried out according to INV forms for each materially responsible employee, facility, warehouse or division;

- list of products unsuitable for further use;

- a list of missing or excess products with an indication of price;

- explanatory notes from financially responsible employees or other officials.

We would like to add that at the meeting the commission must make the following proposals:

- on the timing and methods of eliminating shortages, on conducting internal investigations (if a shortage is detected);

- on the continued use of outdated and unsuitable products for subsequent use;

- other proposals regarding work with inventory items.

If no violations were found during the inspection, then there is no need to draw up an inventory protocol.

Based on such a protocol, the manager issues an order based on the results of the inventory.

Step-by-step instructions for drawing up an order

Step 1. Specify the name of the document.

Step 2. In the appropriate fields, enter the name of the organization (IP), indicate OKPO, and write the date of compilation.

Step 3. Fill out the main part of the order. Here you should clarify the type of inspection and its purpose, as well as list the members of the inventory commission participating in the event and its chairman. Their first and middle names can be abbreviated.

Step 4. We indicate which material assets and in which departments and separate divisions of the company should be checked.

Step 5. We indicate the exact timing of the inspection with its start and end dates.

Step 6. We inform you about the reasons for the need to inventory valuables.

Step 7. We indicate the deadline for submitting the audit results to the accounting department.

Step 8. We certify the document from the manager.

Step 9. Assign a number and register it in a special journal.

Step 10. We introduce it to all interested parties, including employees of departments and divisions where the inspection will take place.

document

dated December 18, 2008

To carry out an inventory in the organization, an inventory commission is appointed consisting of:

1. Chairman - Deputy General Director of Mak LLC Antonov Alexander Petrovich.

2. Members of the commission: senior accountant Vera Alekseevna Mechnikova, program manager Valery Sergeevich Okunev.

The following are subject to inventory: fixed assets, cash in the organization's cash register, financial liabilities.

The inventory will begin on December 23, 2008 and end on December 25, 2008.

Reason for inventory: preparation for the preparation of annual reports (control check, change of financially responsible persons, etc.).

Inventory materials must be submitted to the accounting department on December 29, 2008.

- Order: samples (Full list of documents)

- Search for the phrase “Order” throughout the site

- “Order on the appointment of an inventory commission to carry out an inventory (example).”doc

- Documents downloaded

Entered into the database

Corrections have been made to

- Treaties

- All documents

- Holidays and weekends calendar for 2021

- Small business registration is useful

- How to draw up a contract yourself

- OKVED code table

On our website, everyone can find a contract or a sample document of interest for free; the database of contracts is updated regularly. Our database contains more than 5,000 contracts and documents of various types. If you notice an inaccuracy in any agreement, or the impossibility of the “download” function of any agreement, please contact us using the contact information. Have a good time!

Today and forever

— download the document in a convenient format! A unique opportunity to download any document in DOC and PDF absolutely free of charge. Only we have many documents in such formats. After downloading the file, click “Thank you”, this helps us form a rating of all documents in the database.

Results of inspection of goods and materials and another order

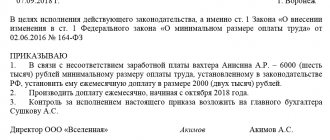

At the end of the procedure for calculating and comparing the results, members of the commission must properly document the results of the inspection. All identified discrepancies must be recorded in the results record sheet (form No. INV-26) from Goskomstat Resolution No. 26 dated March 27, 2000. And after discussing the results and the inventory commission making a verdict, which is recorded in a special protocol, the manager must issue another order to this time about the results of verification activities and the results that were achieved. The reaction of the head of the company to the proposals of the commission members and instructions on the necessary actions should be given. This could be: additional verification, sanctions for perpetrators, introduction of additional security measures. The same local act appoints employees responsible for its implementation, who should also be familiarized with the document for signature. Control over the execution of orders is usually left to the director of the company.

Inventory and registration of its results

The verification consists of comparing and contrasting the actual volumes of values with those recorded in the primary documents. Therefore, first, the commission members get acquainted with the inventories of existing valuables, goods, and supplies. They then compare the property on hand to what is on paper.

At the end of the counting and comparison procedure, the commission members draw up documents containing the results of the inspection. Most often this is not one document, but several. Thus, the identified discrepancies are recorded in the results sheet. As a template for such a document, use form No. INV-26 from Goskomstat Resolution No. 26 dated March 27, 2000.

Documents for recording the results of the inventory are drawn up after it is completed. For example, if your organization carried out an inventory before drawing up annual reports in December 2019, then you are allowed to draw up documents based on its results as early as January 2021. If a discrepancy is identified between the actual data and accounting data, then they must be recorded in the reconciliation statement. A separate comparison sheet is drawn up for objects in custody or leased objects.

The accountant draws up a matching statement in two copies. One of them will remain in the accounting department, the second will be transferred to the financially responsible person.

Later, the results are discussed at a special meeting of the permanent inventory commission, which is the basis for drawing up a protocol. There is no approved form for the protocol, so the main requirements are to correctly indicate the data from the order on the initiation of control measures, about the members of the commission, and the discrepancies identified. If there are no discrepancies, this must be documented. At the same time, the commission puts forward proposals to capitalize, write off the identified surpluses (deficiencies), and reflect them on the balance sheet. In addition, it is permissible to record other initiatives in the protocol, for example, to strengthen security in order to avoid theft in the future. So, the list of final documents contains the following documents:

- a statement of records of the results identified by the inventory;

- comparison sheet of inventory results;

- a comparative statement of the results of the inventory of valuables owned by the organization;

- a comparative statement of the results of the inventory of rented objects;

- inventory list;

- explanatory letter.

How it goes

The procedure for conducting a property inventory takes place in four stages:

- Preparation. During the preparatory stage, the organization develops a sample order for inventory before the annual report, for example, and also creates an inventory commission, sets the deadlines for the process and determines the OS objects that will be checked.

- Direct verification activities. Members of the commission study the quantitative and qualitative properties of OS objects, check their actual condition and availability, and draw up an inventory.

- The analytical stage, during which accounting data is compared with the results of the assessment process. If discrepancies are discovered by members of the commission, statements are drawn up and results are summed up.

- Registration of the results of checking the availability and current condition of property. Accounting brings accounting data into conformity with the commission's reports, those responsible for the errors are identified, and a measure of responsibility is established.

Please note that during the procedure it is necessary to issue not only an order for inventory according to the new standards, but also other orders. We will also talk about them in the article.

ORDER

| "04" March 2014 | № 34 |

Kostroma

On the creation of an attestation commission

In order to implement the provisions of the Rules for Certification of Workplaces on Working Conditions, approved in the Order of the Ministry of Health and Social Development of the Russian Federation dated July 15, 2010 No. 345b order:

- Create a certification commission of the following composition:

| Chairman of the commission: | chief engineer of the safety department N.B. Firefighter |

| Members of the commission: | HSE engineer V.S. Stikharev |

| Deputy Chairman of the Trade Union Y.R. Fair | |

| engineer of the certifying organization JSC "BTR" Trubnova D.O. |

- Control over the proper execution of this order is entrusted to B.D. Kotikov. - and about. chief engineer for occupational safety

| CEO | A.A. Sokolov |

When drawing up a new order, do not forget to cancel the old ones, so that a situation does not arise where there are actually two commissions.

In the case where the name of only one or two commission members is subject to change in the order, use the example below as a sample.

CLOSED JOINT STOCK COMPANY "MOTYLEK"

(JSC "Motylek")

Inventory commission: how it is created

To carry out an inventory in an organization, an inventory commission is created without fail, without which further inspection is impossible. Such a group is not created for one check, but is a permanent operating group, which is entrusted with the responsibility for the constant provision of inventory. Such an inspection group consists of certain persons, among whom must be:

- Representatives of the management staff, for example, manager, deputy director, financial director, etc.;

- Accounting representatives. Both the chief accountant and ordinary specialists can participate;

- Other specialists.

The appointment of an inventory commission is approved only by the manager himself, who signs the order to create a permanent inventory commission. And at the discretion of the manager, it is possible to include a variety of attracted specialists in the group. By the way, the law does not prohibit the involvement of third parties who can also take part in such an audit.

Important: the formation of an inventory commission; its composition does not provide for the inclusion of materially responsible persons in the group. It is unacceptable.

Many people are concerned about another question: how many people should be in such a group? There is no regulated quantity, so the inventory commission can consist of an unlimited number of subjects. But, as a rule, it is not recommended to create a group of less than three or four people.

ORDER

| "14" November 2013 | № 45 |

Almetyevsk

On the creation of an expert commission

In order to conduct an examination to establish the value of documents and select documents with an expired storage period for destruction, the order:

- Form an assessment expert commission consisting of the following:

| Chairman: | and about. Deputy Director N.T. Ordansky |

| Members of the commission: | Head of HR Department G.S. Yablokova |

| Head of the Office E.L. Marnova | |

| chief accountant T.F. Buravina | |

| Archive specialist N.I. Myshkina |

- Head of the archive N.E. Khvostikova develop regulations on the evaluation expert commission by November 16, 2013.

When you need to draw up an order to radically change the composition of the commission, you can use the following example as a sample:

PEASANT FARM "FLAME"

(Plamya Peasant Farm)

Accounting for surpluses, shortages and re-grading

The commission is engaged in making an inventory of the company's property, analyzing it, and also drawing up the results, indicating specific surpluses and shortages.

It is important to note that the reason that led to a failure in the data and its inconsistency with the facts of the documents should be noted.

What mistakes can be made, watch the video:

In conclusion, we note that inventory is a mandatory procedure for all operating organizations. It allows you to identify deviations from the norm in production assets, and an annual accounting report is also compiled on its basis.

Top

Write your question in the form below

Approval of the commission protocol

The protocol indicates the results of the procedure, but it is required for registration only if deviations from the norm are identified. It is worth noting that most often managers resort to drawing up a protocol, since it is convenient to indicate the results of the event and specific decisions made during the inventory. In addition, the complete absence of deviations is a rare occurrence, and therefore one should not take into account the optionality of the protocol in the literal sense.

The slightest deviation from the norm is already a reason to draw up a protocol.