Who can give money for business needs?

Employers are obliged to organize and maintain internal control of the facts of economic life. You can find such a requirement in Part 1 of Article 19 of the Federal Law of December 6, 2011 No. 402-FZ “On Accounting”. The procedure for control over the issuance of money to accountable persons must be determined by the general director of the company. He may issue an order with a list of persons who are entitled to receive funds. Here is a sample of such an order, according to which funds can be issued on account:

In order to comply with cash discipline, an employee is considered to be a person with whom an employment or civil law contract has been concluded (clauses 5 and 6.3 of Bank of Russia Directive No. 3210-U dated March 11, 2014). Consequently, money can be issued, including to the contractor, on account. He may need them, for example, to purchase materials to perform work under a civil contract. This amount can be given to him for the report, for example, from the cash register.

Accountable amounts can be transferred to the bank card of the accountable person, incl. for salary (Letter of the Ministry of Finance dated August 25, 2014 No. 03-11-11/42288).

Results

Each enterprise (IE) must necessarily approve an order on accountable persons in order to be able to allocate funds to its employees on account for making purchases for the needs of the enterprise. In this order, in addition to the list of responsible persons, information about the deadline for the funds issued on account and their maximum amount must be displayed.

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

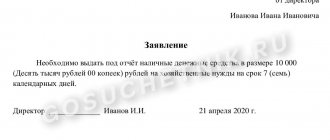

Application for the issuance of money: is it necessary?

Until recently, in order to receive cash on account, an employee had to submit an application for the issuance of funds to the accounting department or human resources department. A sample of such an application shows that it was necessary to indicate the required amount, as well as explain for what purposes it will be spent. Here is a sample of such an application for the issuance of funds:

However, as of August 19, 2021, the situation has changed. The amendments are provided for by Directive of the Central Bank of Russia dated June 19, 2017 No. 4416-U. From the specified date, you can give the employee money on account without his application. To issue money, an order for the issuance of funds from a report or other administrative document of the company is sufficient. The same rules for issuing money on account continue to apply in 2021.

Is it possible to do without an order?

It is necessary if the company uses the practice of transferring funds to employees on account.

There are no statutory penalties for incorrect execution of the issuance of money on account. But in practice, in the absence of an order, the inspection authorities (tax service or labor inspectorate) have the right to impose a fine for violation of cash rules (see Part 1 of Article 15.1 of the Code of Administrative Offenses of the Russian Federation):

- for officials in the amount of 4,000 to 5,000 rubles;

- for legal entities - from 40,000 to 50,000 rubles.

How to issue an order to issue money: example

So, the issuance of funds for reporting in 2021 is possible on the basis of an order or other administrative document (clause 6.3 of the Bank of Russia instructions dated March 11, 2014 No. 3210-U). At the same time, there are no restrictions on the amount of accountable amounts and the period for issuing money. Here is an order for the issuance of funds on account (sample):

Moreover, there are no special requirements for how to draw up an order for the issuance of accountable amounts. In our opinion, it makes sense to record in the order: the employee’s full name, amount, goals and terms of issue.

We also note that it is possible to issue a general order for several amounts. So, for example, if the issuance of cash for reporting is necessary for several employees, then the order may look like this:

From August 19, 2021, the basis for issuing funds is an order or other administrative document. At the same time, no one prohibits employers from continuing to accept applications from employees for the necessary amounts of money. However, keep in mind that the procedure for issuing appropriations should be fixed in the regulations on the issuance of funds in the report. You can provide an example of a provision on the issuance of accountable funds.

The concept of accountable money

This is the common name for funds given in advance to an employee from the organization’s cash desk to pay for the needs of the enterprise.

The amount of amounts issued for reporting is indicated in the document. The settlement limit (no more than 100,000 rubles per agreement) is taken into account only when making payments between organizations.

At the same time, all expenses incurred by employees using the money issued are economically justified by production necessity. The employer has the right to establish rules and deadlines for submitting reports on expenses incurred, and, if necessary, issue an order to tighten the acceptance of reporting documents from accountable persons, if this measure is economically or organizationally justified.

Deadlines for issuing funds

What are the deadlines for issuing funds? When do employees need to submit a report on money spent to their employer? The answer to this question must be sought in the order of the general director. After all, it is in it that such a period is indicated.

As a general rule, an employee must report on the amounts received for reporting no later than three working days after the expiration of the period for which these amounts were issued (clause 6.3 of the Directive of the Central Bank of the Russian Federation dated March 11, 2014 No. 3210-U). But what to do if the return period has not been set? According to tax authorities, in such a situation the employee must submit the report on the same day on which they received them (letter of the Federal Tax Service of Russia dated January 24, 2005 No. 04-1-02/704).

Travel allowance report

Special conditions are defined for travel expenses. The employee must report on them within three working days from the date of return from a business trip (clause 26 of the Regulations, approved by Decree of the Government of the Russian Federation of October 13, 2008 No. 749).

Issuance of accountable amounts

If a certain amount needs to be given to one of the employees of the enterprise, a corresponding order is drawn up to allocate accountable funds to the employee’s account, into which the following data is entered:

- name of company;

- name of the published paper;

- document number, date, place of its preparation;

- rationale and basis for publication;

- who is responsible for issuing accountable amounts;

- maximum amount of amounts;

- the period for which they are issued;

- an employee who has the right to receive the necessary funds from the cash register;

- official responsible for execution.

The paper is signed by the head of the enterprise, the employee who has the right to receive money, and the person responsible for executing the order. Also, the details of the decree should be recorded in a special accounting journal.

Process of issuing money

To issue money, the employer needs to do the following:

- issue a cash expense order (RKO). It must be signed by the chief accountant or other authorized person (clauses 4.2, 4.3, clause 4 of Directive No. 3210-U).

- after the accountant puts his signature on the cash register, the cashier gives him money from the cash register and signs the cash register (clause 6.2, clause 6 of Directive No. 3210-U).

- register the issuance of money under the reporting posting (cash flow item):

| Wiring | Operation |

| D 71 - K 50 | The employee was given money on account |

Here is a sample cash settlement report for the issuance of funds:

Money issued on account is not subject to personal income tax and insurance premiums.

You can issue cash on account if the employee has not repaid the debt on previously issued funds. This can be done from August 19, 2021. However, this does not mean that employees no longer need to prepare advance reports on the amount spent. Even after August 19, 2021 (for example, in 2020), the employee must submit reporting documents to the accounting department about the money spent.

It is worth noting that the issuance of funds to the founder or director is not prohibited. However, it is worth understanding that no “indulgences” are provided for managers in this part. For example, the founder, like any other employee, is obliged to return the accountable funds received.

Read also

11.07.2016

Who are called accountable persons?

The category of accountable persons may include any employees of the enterprise:

- secretaries who receive money from the cash register to purchase stationery, materials for office equipment and other office equipment,

- caretakers, to whom money is given to purchase household or household supplies. Accountable persons also include specialists who often go on business trips; they are given funds in advance against the report to pay for tickets, hotels, entertainment expenses, etc.,

- drivers who receive “cash” to pay for gasoline and other fuel liquids and spare parts also have accountable status,

- accountants and cashiers of enterprises.

Separately, we can single out employees of branches and structural divisions who do not have an independent balance sheet and receive money for business and other expenses from the main cash register of the enterprise.

Read more about who the accountable persons are in this material.

What to rely on when creating an order

Orders issued at an enterprise must always be based on something. This means the basis and justification, which must be present in every administrative order.

As a basis, an article of the law (and its specific paragraphs) is used, which is directly related to the order being issued, or a reference to an internal document of the enterprise (an act, an official or memorandum, some provision in the accounting policy, etc.). Justification is the actual reason for creating the order.

Reporting on money spent

After the accountable funds have been spent, the person who made the expenses must report to the accounting department.

This must be done no later than three days after the day indicated as the last day for using the money.

To do this, the following documents must be attached to the expense report:

- receipts;

- sales and cash receipts;

- travel tickets;

- other forms confirming payment.

All documents are then properly verified by an accountant.

What is the responsibility for missing a statement?

There is no special liability for legal entities for violating the procedure for drawing up an application or administrative document for the issuance of funds on account. However, tax officials, when checking compliance with cash discipline at an enterprise, and discovering the absence of documents for reporting, can charge a violation with:

- The procedure for storing cash amounts exceeding the established limit. The basis for imposing liability in accordance with Art. 15.1 of the Code of Administrative Offenses of Russia, the tax inspector most often concludes that funds from the cash register were issued unlawfully, and therefore should remain in the cash register. If the limit is exceeded, excess cash must be deposited at the bank on the same day. There is judicial practice unfavorable for taxpayers based on such conclusions (resolution of the 9th Arbitration Court of Appeal dated May 6, 2013 No. 09AP-11841/2013-AK).

- The procedure for maintaining cash discipline in general.

But there is also a practice that is positive for taxpayers, thanks to which it is clear that not all judges see the need to impose liability for such violations of cash discipline as the lack of documents for reporting (resolution of the 9th Arbitration Court of Appeal dated May 13, 2013 No. 09AP-10884/2013) .

At the same time, if there are significant (in the opinion of tax authorities) violations of cash discipline, such as the lack of instructions on the timing of the release of funds for reporting, judges usually take the side of the tax service employees (resolution of the 9th Arbitration Court of Appeal dated March 6, 2013 No. 09AP- 2451/2013).

In order to avoid imposing a fine (if the inspection has already begun), you can exercise your right and provide the requested documents the next day (clause 31 of the regulations approved by order of the Ministry of Finance dated October 17, 2011 No. 133n). During this day, the director can draw up the missing papers for issuing a report, and the cashier can pin them to the appropriate cash registers.

Errors of this kind should be corrected only in the last 2 months, because in accordance with paragraph 1 of Art. 4.5 of the Administrative Code, the statute of limitations for imposing administrative liability is 2 months from the date of the violation.

More information about liability for violation of cash discipline can be found in our article “Cash discipline and liability for its violation .

IMPORTANT! If accountable funds are transferred to a payment card (salary, corporate), an application from the accountable person or an administrative document, in the opinion of the financial department of the Russian Federation, is also necessary. This is stated in the letter of the Ministry of Finance dated August 25, 2014 No. 03-11-11/42288.

We transfer money against the report to the employee’s bank card

Transferring money to an employee's card against a report is much more convenient compared to cash payments: there is no need to prepare cash documents or go to the bank to withdraw cash.

However, as practice shows, these conveniences are canceled out by writing off the money received to pay off the employee’s debts (for example, loans), or blocking the employee’s card.

The company can transfer the accountable money to the employee’s salary or personal bank card.

The list of accountable expenses includes entertainment, travel expenses, expenses for administrative and business needs (purchase of office supplies, household equipment, maintenance of office equipment and similar expenses). The basis for payment of the accountable amount is an order (instruction, decision) signed by the head of the company. There is no need for the employee to fill out an application for the release of funds against the report.

At the same time, the issuance (transfer to a bank card) of accountable amounts can be carried out even if the accountable person has a debt.

The legislation does not establish a specific period during which the employee must report on the accountable amounts spent. According to clause 6.3 of the Directive of the Central Bank of the Russian Federation dated March 11, 2014 No. 3210-U, the employee is obliged to provide the accounting department with a report on the amounts received no later than three working days after the expiration of the period for which these amounts were issued. If the company does not have such an order, we can assume that the deadline for issuing accountable amounts has not been established, which means that settlements on accountable amounts must be made within one business day (Letter of the Federal Tax Service of the Russian Federation dated January 24, 2005 No. 04-1-02/ 704).

Important! Funds issued on account to employees can be transferred to employees’ bank cards to carry out transactions related to:

- with payment of expenses of organizations for the supply of goods, performance of work, provision of services;

- with travel expenses;

- with compensation to employees for documented expenses (Letter of the Ministry of Finance of the Russian Federation dated July 21, 2017 No. 09-01-07/46781).

As a rule, accountable money is transferred to the bank card to which the company transfers the employee’s salary.

To transfer accountable money to an employee’s bank card, the company issues an order, a sample of which is given below:

ORDER No. 2/1

on the transfer of accountable amounts to the employee’s bank card

January 9, 2021 Moscow

For the purpose of purchasing household goods

1. Transfer to the bank card of employee T.E. Tsvetochkin. 50,000 (fifty thousand) rubles for the purchase of household goods using the following details:

card number 845044442000008882, account number 40817425550000567044 in Bank PJSC OTP, bank BIC 044573474.

2. Appoint the head of the financial department P.G. as responsible for the execution of the order. Romashkin.

General Director D.I. Lyutikov

As financiers note, “...taking into account the provisions of Article 8 of the Federal Law of December 6, 2011 No. 402-FZ “On Accounting”, when transferring funds to the personal bank cards of employees to pay for business needs (goods, materials) in the regulatory act ", defining the accounting policy of the organization, it is necessary to provide provisions defining the procedure for settlements with accountable persons (Letter of the Ministry of Finance of the Russian Federation dated August 25, 2014 No. 03-11-11/42288)."

In the Accounting Policy, you can make a reference to the Regulations on Settlements with Accountable Persons approved by the company.

Fragment of the Regulations:

_____________ D.I. Lyutikov

"01" January 2021

On the procedure for issuing funds for reporting, submitting, checking and approving advance reports of JSC “Lutik”

Appendix No. 1 to Order No. 48 dated 01.01.2019

REGULATIONS on settlements with accountable persons

This Regulation has been developed in accordance with:

- with the Decree of the Central Bank of the Russian Federation “On the procedure for conducting cash transactions” dated March 11, 2014 No. 3210-U;

- Federal Law “On Accounting” dated December 6, 2011 No. 402-FZ;

- Order of the Ministry of Finance of Russia “On approval of the Chart of Accounts” dated October 31, 2000 No. 94n;

- Labor Code of the Russian Federation.

The purpose of the Regulations is to ensure the correctness of accounting and control in settlements with accountable persons of Buttercup JSC.

The procedure for issuing funds for reporting

Funds under the report are transferred either for business and operating expenses or for expenses associated with business trips.

The list of employees who have the right to receive funds on account is established by the Company Order.

Funds are transferred on account regardless of whether the accountable person is indebted for previous accountable amounts.

Individuals who have signed a civil contract with JSC Buttercup to perform work or provide services during the validity period of this agreement also have the right to receive funds on account from the cash desk of JSC Buttercup.

Basis for issuing funds on account

Funds for the report are transferred on the basis of an order from Buttercup JSC, signed by the manager. The administrative and economic department is responsible for preparing the order.

The order must contain the following information:

- date of;

- surname, first name, patronymic (full name) of the accountable person;

- advance amount;

- the period for which the advance is transferred;

- signature of the manager or authorized person by power of attorney.

Methods for issuing accountable amounts

The report is issued to the employee by non-cash transfer from the current account of Buttercup JSC to the employee’s salary card (Letter of the Ministry of Finance of the Russian Federation dated July 21, 2017 No. 09-01-07/46781).

Problems with blocking a bank card

Recently, there have been legal proceedings related to the blocking of a bank card to which accountable money is transferred.

Blocking a card is a procedure of technical restriction on transactions using it, providing for the bank’s refusal to provide authorization (obtaining from the bank the permission necessary to use the card transaction, and obliging the bank to execute the order of its holder), that is, limiting the remote ability to manage the account.

This is due to the fact that the bank is obliged to document information obtained as a result of implementing internal control rules in order to combat the legalization (laundering) of proceeds from crime and the financing of terrorism in cases where unusual transactions are detected.

For this reason, the bank has the right to request, and clients are obliged to provide the bank with the necessary information (clause 14 of article 7 of the Law of 07.08.2011 No. 115-FZ “On combating the legalization (laundering) of proceeds from crime and the financing of terrorism" , clause 4.1 of the Regulations on the requirements for the internal control rules of a credit organization in order to combat the legalization (laundering) of proceeds from crime and the financing of terrorism, approved by the Bank of the Russian Federation dated March 2, 2012 No. 375-P).

Important! At the same time, the current legislation in the field of combating the legalization (laundering) of proceeds from crime and the financing of terrorism does not limit credit institutions in terms of the volume of documents requested from clients.

In turn, clients are obliged to provide organizations carrying out transactions with funds or other property with the information necessary for these organizations to fulfill the requirements of this federal law, including information about their beneficiaries and beneficial owners (clause 14 of article 7 of Law No. 115-FZ ).

For example, in one of the court cases reviewed, in the period from November 2021 to January 2021, large sums of money were regularly credited to an individual’s bank card account. Transfers were made in equal amounts, with the purpose of payment “On account for business needs.” The total amount of funds transferred to the account was: 2 payments of 250 thousand rubles, 17 payments of 100 thousand rubles.

The bank requested clarification on the transactions for depositing funds, as well as documents confirming the economic meaning of the transactions performed.

In response to the Bank’s request, the client provided the following documents: an employment order for the position of chief accountant, an employment contract, receipts for cash receipts with the purpose of “return from an accountable person.” No other documents confirming the posting of funds to the organization's cash desk were presented. No explanations were provided about the reasons for the multiple returns to the company's cash desk of funds received on account.

From an analysis of the documents provided by the Bank, it was concluded that the client’s transactions did not have clear economic meaning. The information and documents provided did not allow us to exclude suspicions about the dubious nature of the transactions carried out by the client. Taking into account all the information available to the Bank, a decision was made to recognize the client’s transactions as suspicious.

Subsequently, at the court hearing, the employee confirmed that she used these funds in cash to pay contractors under business contracts. If the counterparty could not accept payment, she handed over the money to the cashier, but did this only for the bank, holding it for some time.

The court recognized the actions of Sberbank PJSC as legal (Decision of the Budennovsky City Court (Stavropol Territory) dated 06/07/2018 No. 2-563/2018).

But if you submit all documents to the bank in a timely manner and explain the essence of the transactions, then there will be no grounds for blocking the card. As noted in the Determination of the Moscow City Court dated 09/07/2016 No. 4g-10455/2016 “... an individual is not engaged in entrepreneurial activity and the transfer of funds to his personal card cannot be considered entrepreneurial activity, as well as arguments about the absence of a ban on the transfer organization of accountable amounts to the personal cards of employees, since they are based on an incorrect interpretation of substantive law and are not supported by evidence.”

What should be written in a payment order for the transfer of accountable money?

In order to eliminate possible problems with the bank, when transferring accountable amounts to the employee’s card in the payment order, you must indicate in field 24 “Purpose of payment” “Transfer of funds against the report for payment of business expenses.”

This formulation will eliminate tax risks, because during tax audits, funds transferred as accountable to employees’ bank cards may be classified by the tax authorities as wages. Accordingly, personal income tax and insurance premiums may be charged on these amounts, in the opinion of the tax authorities.

| On the forum since: 10/31/2007 Posts: 498 | On the forum since: December 14, 2006 Posts: 6,407 |

Dispute Resolution

There are often situations when the accountable person did not report on time and did not return the money received on time. In this situation, the company has one month after the expiration of the return date to withhold the unreturned accountable advance. To do this, it is necessary to issue an order from the manager to withhold the funds issued from wages, familiarize the accountant with it and obtain his written consent to the withholding.

If the employee does not agree with the withholding, the company will have to recover the money through the court. The limitation period for accountable amounts is three years from the date of non-repayment (Article 196 of the Civil Code of the Russian Federation). During this time, the company has the opportunity to recover accountable amounts not returned on time in court.

Please note that an undocumented expense in the interests of the organization, an unreturned and uncollected account in a timely manner, in the opinion of the Federal Tax Service, is the employee’s income, and personal income tax must be withheld from him. This position is set out in Letter No. SA-4-7/23263 dated December 24, 2013, and the judges support it: For more details, see the Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated March 5, 2013 No. 14376/12.

How to decide on the period

Attention! The rule on the period for issuing accountable amounts, which is three days, should be observed by absolutely all employees of the organization, including the head of the enterprise.

When determining a specific reporting period for an organization, it is undeniable that it must be respected. Otherwise, the tax office may fine the company due to failure to post the amount to the cash register. The amount of the fine is regulated by the Code of Administrative Offenses of the Russian Federation (clause 1, article 15). This doesn't always happen, but there is a risk. That is why it is so important to formulate the issuance period on the basis of internal corporate acts.

Attention! Organizational issues regarding the issuance of accountable amounts should be fixed only in administrative documentation. If this is done in the accounting policy, changing the procedure if necessary will be extremely problematic.

Thus, the deadlines are not set; they are determined by the subject himself. The data is recorded in local acts.