In order to get an answer to the question of what code 503 means in the 2-NDFL certificate, let’s turn to tax legislation. According to the current Art. No. 217 of the Tax Code of the Russian Federation, any income of citizens living and working in the country is taxed and must be recorded in the regulated certificate Form 2 of personal income tax.

It contains information about all possible sources of income, wages and deductions. As a rule, 2-NDFL is issued by the employer for a period of up to 1 year and is filled out on the basis of strictly established regulations. The form has a clearly defined structure and coding, containing information on income data, as well as the amounts of individual deductions and calculations. Each code is approved by the Federal Tax Service of the Russian Federation and is used to fill out data by individuals under certain conditions. They are located on the lines of the table in section No. 3 next to information about the corresponding income.

What types of income can be deducted?

Certificate 2-NDFL indicates all types of income that the taxpayer received in a specific reporting period, including:

- salary at the main and additional places of work;

- interest on deposits, income from transactions with securities;

- material assistance in cash or property (in kind);

- income from foreign currency transactions;

- winnings from bookmakers, casinos, from participation in lotteries and drawings, received in cash or property (for example, prizes);

- income from rental of vehicles and real estate;

- royalties, dividends, etc.

Tax deductions can be provided for different types of income. To avoid confusion when preparing a 2-NDFL certificate, as well as tax and accounting registers reflecting the income and expenses of individuals, an individual code is assigned to each type of income and tax deduction.

Features of deductions

Today the following tax deductions have appeared:

- Social – deductions that are issued exclusively to low-income families;

- Property deduction is a deduction that is formed in the process of selling real estate on which tax was paid, as well as the subsequent acquisition of real estate, which provides for the return of a certain amount of tax paid;

- Professional deductions are directly related to professional activities and certain professional risks;

- Investment deductions are based on the formation of the amount of risk for investment projects;

- Standard deductions for children (upbringing and maintenance), amounts spent on education and treatment, which should not be taxed.

In principle, almost anyone can apply for standard deductions. As for other deduction options, in this case you need to collect a package of documents in order to complete them.

A deduction initially helps reduce the amount of income that is subsequently taxed. But, there are situations when the deduction is provided in the form of a refund of funds from previously paid taxes.

What does tax deduction code 503 mean?

Financial assistance paid by an employer to its employees (including former employees retired due to age or disability) is one of the types of income for which a tax deduction is provided. Its amount is 4,000 rubles per year per employee, which is provided for in clause 18 of Art. 217 of the Russian Tax Code.

The deduction is indicated in the 2-NDFL certificate, as well as in the relevant tax and accounting documents, using code 503.

Let’s assume that an employee of an enterprise received financial assistance from him in the amount of 15,000 rubles. In this case, this amount will be reflected in the 2-NDFL certificate using code 2760, and the amount of the due deduction (4,000 rubles) will be reflected under code 503. The calculation of the taxable amount in this case will look like this:

15,000-4,000 = 11,000 rubles

The amount under code 503 is a fixed amount that does not depend on the amount of financial assistance. It can be used several times a year, but only within the established limit.

For example, if a person received financial assistance in April in the amount of 1,500 rubles, in August - 2,000 rubles, and in November - 6,000 rubles, then in the first and second cases the amounts will be fully discounted, and in the third, the remaining 500 rubles will be deducted from the financial assistance:

4000 - 1500 - 2000 = 500 rubles

Consequently, income tax will be withheld only from November financial assistance, and the taxable amount will be 5,500 rubles.

What is the 2-NDFL certificate used for?

As mentioned above, the provision of a 2-NDFL certificate is carried out by a tax agent. Earlier in the article we described what manipulations are carried out by the employing organization:

- issues income to the taxpayer;

- calculates and sends taxes to the budget;

- provides deductions.

Why do organizations fill out 2-NDFL certificates?

To display all the required transactions and transmit a report on them, use the form of the certificate in question established by the state.

The form itself was last updated by the government in December 2015. It was then that the use of a new sample of the required document came into force.

In addition to submitting reports to the Federal Tax Service, employees of the organization may need a 2-NDFL certificate for their own needs. To receive it, they must submit an application addressed to the head of the employing organization.

A document is submitted for verification by a tax agent if:

- he paid persons working for him funds that are subject to partial withholding in favor of the state budget through the calculation of personal income tax;

- it paid employees but was unable to withhold income taxes.

In the second case, the employing company has the obligation, no later than 60 days from the end of the current tax period, to notify employees of the Federal Tax Service about the absence of the required opportunity and, at the end of the year, to submit for verification the data in the completed 2-NDFL certificate.

Help 2-NDFL

When an employee comes to the accounting department and fills out an application for the certificate in question, he will most likely use it in the future for:

- provision at a new place of employment, in order to receive a standard or other type of deduction, since in order to issue the required funds it is necessary to take into account income paid since the beginning of the current taxation period, also taking into account funds issued by the previous employer;

- obtaining information that is then entered into the declaration form form 3-NDFL, which is submitted for verification to the tax office in certain situations;

- transfer to any other place where the certificate was required, for example, to a credit institution, to receive a cash loan.

Please pay attention to the following most important fact: a citizen who requests the issuance of a certificate should not report to accounting employees or even superiors about why he needed it. The employing organization does not have the right to refuse to issue a certificate without this information; this circumstance is determined by the Tax Code of our country.

According to the letter of the law, a certificate must be issued no later than three days from the moment the employee’s application is written and submitted for consideration. Weekends are not taken into account.

If a certificate is requested in the middle of the year, the employer fills it out based on the information already available at the moment.

If a company is not an employer, it is not required to make payroll payments and transfer income tax contributions to the state budget. This means that the organization is also not obliged to prepare, fill out and submit a tax return for verification.

In addition, exemption from this obligation is made in some other cases:

- if the company has paid income to employees, who must independently carry out the procedure for calculating income tax funds and transferring them to the state treasury;

- if such a payment of funds was made in favor of employees, which implies an independent transfer of their part to the treasury by the recipient;

- if income was issued in the form of cash, from which tax is not deducted in accordance with the letter of the law.

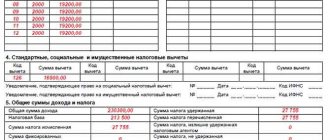

The certificate is filled out in accordance with the rules established “at the top”. The document consists of five sections, each of which implies specific information.

Table 1. Completing sections

| Order | Filling |

| 1 | First of all, data is entered on the employing organization that is filling out the required document. |

| 2 | Then indicate information about the employee receiving the funds. |

| 3 | Following is a list of income subject to income tax. |

| 4 | The fourth section lists the tax deductions provided to the employee. |

| 5 | In the fifth, they present the amount of tax that was calculated and the total income. |

Encodings in the certificate are used not only to indicate types of income and deductions. With their help, they also determine on what occasion the paper is provided for verification:

- in the column called “sign” the number 1 is entered if the paper is submitted for income tax that has been successfully transferred to the state treasury;

- The number 2 is entered in the same line if the tax was not withheld.

The transcript provided by the Federal Tax Service in the form of a list written in one of the orders issued by the service will help you understand all the encodings used for reference. You can view the full list by finding it among the attached documents on the official website of the Federal Tax Service.

The rules governing the procedure for filling out the certificate are contained within the appendix of the relevant order. Every experienced accountant has an idea about them, since he was faced with filling out the required paper not only while studying at a higher educational institution, but also probably resorted to filling it out more than once in the process of work.

If you are just starting to work in the accounting field and are filling out a document for the first time, you should find a completed sample paper on the Internet and check it first. Be sure to pay attention to the edition from which year the sample you found was created.

The certificate was last updated in 2015, however, outdated certificate forms are still floating around the Internet

What is the difference between deduction codes 503 and 508

It is worth noting that deduction code 503 has nothing to do with financial assistance paid on the occasion of the birth of a child. This is another type of income, which is reflected in the 2-NDFL certificate, as well as in the relevant tax and accounting documents, using code 2762.

In this case, the tax is calculated differently, and the corresponding tax deduction is indicated by code 508.

Thus, when filling out the 2-NDFL certificate, as well as the corresponding accounting and tax documentation, you need to remember the following:

- income code 2760 denotes financial assistance paid by an employer to its employees (including former employees retired due to age or disability), and is used only in conjunction with deduction code 503;

- income code 2762 denotes financial assistance paid by the employer on the occasion of the birth of a child, and is used only in conjunction with deduction code 508.

Let's sum it up

The use of codes when filling out documentation for verification in government systems is a frequent and necessary practice, primarily due to the fact that this method of providing information seriously reduces the time spent on carrying out this procedure; in addition, labor costs are also reduced. It is very important to have knowledge regarding encodings, or to constantly keep a list with their decoding at hand in order to avoid mistakes and not receive various types of penalties from the tax office.

Documents to confirm the right to deduct

The decision to provide an employee with financial assistance is formalized by order of the head of the enterprise. The grounds for issuing an order may be:

- employee's personal statement;

- relevant provisions of the employment or collective agreement;

- internal regulatory document regulating the procedure for providing financial assistance to employees of the enterprise.

No additional documentary evidence is required to receive a deduction under code 503. This benefit is provided for at the legislative level and is set out in paragraph 28 of Art. 217 of the Russian Tax Code.

-Accordingly, if an employee received financial assistance, then a deduction in the amount of 4,000 rubles per year is provided automatically.