Personal income tax with financial assistance in 2018

Natural disaster, terrorist act Such financial assistance will not be subject to personal income tax, regardless of the amount.

Accrued funds also do not need to be reflected in the 2-NDFL certificate (see Letter from the Ministry of Finance). Treatment Let's say an employee was paid 50,000 rubles. In this case, only 4,000 rubles are not subject to taxation. Accordingly, such a payment will be subject to personal income tax from 46,000 rubles. The tax amount (13% of the amount 46,000) will be 5,980 rubles. The funds that the employee will receive will amount to 44,020 rubles. The 2-NDFL certificate will be reflected with codes: income - 2770 and deductions - 504. The income and deduction codes for filling out the 2-NDFL certificate are given in Order of the Federal Tax Service of Russia dated September 10, 2015 No. MMV-7-11/ (as amended on November 22. 2016).

- Code 2710 - used to reflect any type of financial assistance, including that whose amount does not exceed 4,000 rubles, with the exception of:

- Code 2760 - used to reflect financial assistance to retired workers.

- Code 2761 - used to reflect financial assistance to disabled people, provided that it is provided by public organizations and not by the employer.

- Code 2762 - reflects financial assistance, which is paid at the birth of children or upon their adoption.

- financial assistance to retired employees (due to old age or disability);

- financial assistance for the birth or adoption of children;

- financial assistance provided to disabled people by public organizations.

So, we have looked at all types of income codes and deductions that are indicated in the 2-NDFL certificate when paying financial aid.

In fact, such an exemption is nothing more than a type of property tax deduction. Both income and deductions have special codes. The material assistance code in the 2-NDFL certificate and deduction codes are reflected by personnel employees or other responsible persons.

Next, we’ll figure out what the income codes are. assistance, and by what regulatory act they are established. Income code - material assistance up to 4,000 rubles Income codes for material assistance are reflected in the Order of the Federal Tax Service of Russia dated September 10, 2015 No. ММВ-7-11/ The income code for material assistance of 4,000 rubles or less is entered in the 2-NDFL certificate. The codes are indicated in Appendix No. 1 to the above Order of the Federal Tax Service. Guided by the requirements of this order, specific income codes - financial assistance, as well as deduction codes for financial assistance of 4,000 rubles or less, entered in the 2-NDFL certificate, depend on the amount of payment and the purpose of such support (i.e., the type of financial assistance). When the total support paid to an employee does not exceed 4,000 rubles (for any type of financial assistance), the deduction code is as follows: 503. When financial assistance is paid in connection with the birth (adoption) of a child, deduction code 508 is entered. No other deduction codes are currently established. Material assistance: income code in the 2-NDFL certificate. Entering the income code on the material assistance received in the 2-NDFL certificate is carried out in accordance with the requirements of the already mentioned order No. MMV-7-11/387.

Mat Assistance at Birth of a Child 2021 Income Code

The Tax Code establishes different procedures for taxation of funds provided as financial assistance, depending on the type of this assistance, as well as the reasons for the provision: Type of financial assistance Nuances of paying personal income tax Funds the reason for the allocation of which is the birth of a child or adoption There is no provision for payment of tax on amounts up to 50 thousand rubles for both parents per year per child Funds allocated in connection with the death of a close relative Payment is not provided Funds for victims of a natural disaster or other emergency Payment is not required Funds allocated in connection with other circumstances Tax is not paid on amounts up to 4 thousand rubles per year Sample of filling out form 2-NDFL Documentation Payment of financial assistance is made on the basis of the decision of the head of the enterprise, and its amounts are not regulated at the legislative level in any way.

- Code 2761. This code is used for financial assistance provided to disabled people by charitable organizations, and not by employers.

- Code 2762. This code indicates financial assistance issued by the employer on the occasion of the birth of a child.

Rules for reflecting financial aid in 2-NDFL

The Tax Code establishes different procedures for taxing financial aid with personal income tax depending on the reason for which it is paid or what “type” this financial aid is. Conventionally, all financial assistance can be divided into 2 groups: limited by the amount not subject to personal income tax and unlimited.

So, any financial assistance that is not subject to personal income tax in a certain amount must be reflected in the 2-personal income tax certificate. It is necessary to show the entire amount of income in the form of financial assistance and the deduction applied to it (in the amount not subject to personal income tax).

For example, in 2-NDFL, financial assistance up to 4,000 rubles paid to an employee (clause 28 of Article 217 of the Tax Code of the Russian Federation) must be shown with income code 2760 and at the same time with deduction code 503. Similarly, the certificate indicates a lump sum payment accrued to the employee in connection with the birth of his child. As you know, it is not subject to personal income tax up to 50 thousand rubles. for each child, but for both parents, and provided that it is paid within a year from the date of birth. For this financial assistance, income code 2762 and at the same time deduction code 504 are used (Appendices No. 1, No. 2 to the Order of the Federal Tax Service of September 10, 2015 No. MMV-7-11 / [email protected] ).

But financial assistance, which is not subject to personal income tax regardless of its size, is not indicated at all in 2-personal income tax. For example, there is no need to reflect in the certificate the payment of one-time assistance to an employee whose apartment burned down for reasons beyond his control. After all, it was paid due to an emergency circumstance, which means it is completely not subject to personal income tax (clause 8.3 of Article 217 of the Tax Code of the Russian Federation).

Maternity assistance for the birth of a child 2021 postings

The following entries will be made in accounting: One-time financial assistance in connection with the birth of a child has been accrued 91 73 60,000 Insurance contributions have been accrued for the taxable amount of financial assistance* ((60,000 - 50,000) rub. x 30.2%**) 91 69 3,020 Personal income tax withheld from the taxable amount of material assistance ((60,000 - 50,000) rub. x 13%) 73 68 1,300 Material assistance was paid from the cash register (60,000 - 1,300) rub. 73 50 58 700 Reflected PIT from expenses not taken into account when taxing profits (RUB 60,000 x 20%) 99 68 12,000 * Insurance premiums are included in expenses in the generally established manner on the basis of paragraphs. 1, 45 p. 1 art. 264 of the Tax Code of the Russian Federation (letters of the Ministry of Finance of the Russian Federation dated March 20, 2021 No. 03-04-06/8592, dated September 3, 2021 No. 03-03-06/1/457, dated August 17, 2021 No. 03-03-06/1/419) .

Taxation From the point of view of taxation, material assistance is considered as an economic benefit, and therefore is subject to tax (Articles 208, 209, 210 of the Tax Code). However, the social nature of the targeted income made it possible to exempt from taxation certain types of financial assistance, or certain amounts within the established limit. We wrote about this in the article “Maternity assistance in 6-NDFL”. When financial assistance is calculated for the birth of a child, taxation allows you to exclude an amount of up to 50,000 rubles from the personal income tax base. for each of the children (clause 8 of article 217

Payment classification

All required benefits are conditionally divided into mandatory and optional. Mandatory payments contain all types of assistance that are paid by the state. Optional - paid by the organization where the expectant mother works, in other words, this is financial assistance paid by the company to its employee on a voluntary basis.

There is also a difference: one-time payments and benefits that are paid monthly.

In addition, cash benefits are:

- federal (received by all citizens of the Russian Federation from the country’s budget);

- regional (the region has the right to issue additional benefits from its budget).

From the state

A lump sum payment upon the birth of a child is due once. It is possible for both the father and mother of a newborn to receive it. Every woman receives the payment, regardless of her employment before maternity leave. An unemployed woman can also receive this money.

The following documents are needed:

- statement;

- child's birth certificate;

- parents' passports;

- certificate from the other parent’s place of work;

- child's birth certificate and copy.

Documents for download (free)

- Sample application from an employee for financial assistance

The law allows 10 days for the calculation and issuance of money from the moment the package of documents is transferred to the accounting department at the address of work or study of a family member.

For child care

This subsidy is available to those who plan to take parental leave for up to 1.5 years. This could be any of the spouses. If an unemployed parent plans to provide care, you can do everything necessary to receive funds at the nearest branch of the Federal Social Insurance Fund of the Russian Federation.

For a working citizen, the benefit is calculated in the amount of 40% of the average monthly salary, 2 years before the birth of the child are taken into account, the amount is paid every month.

According to the law, the amount should not be less than 4,465.20 rubles if this is the first child, and 6,284.65 rubles for subsequent children.

A woman who has never worked before the birth of a child has the right to a minimum level payment, for which she needs to visit the Social Insurance Fund office at her place of residence. If a woman, while on leave to care for her first child, goes on leave to care for her next child, she becomes entitled to a subsidy, which will consist of the amount of benefits for caring for the first child and the second.

The maximum amount should not be more than 100% of the average salary for the last 2 years and be less than the minimum amount.

It is important that in this case the woman has the right to count on either payment of benefits or maternity benefits.

The following documents are required:

- parents' passports;

- child's birth certificate;

- parents' work records;

- a certificate from the employment service stating that no payment was made (for the mother);

- certificate from place of work (study);

- personal account number in the Security Council of the Russian Federation;

- certificate of family composition.

Maternal capital

Maternity capital is paid once in the event of the birth of a second and/or next child in the family. If there is more than one child in a family, and they did not use the capital, then when the next one appears, the family can issue a payment.

In addition to the child’s mother, the father can also receive state payments if he remains the sole adoptive parent of the second or subsequent children.

It is important to understand that current legislation allows the use of this capital exclusively for the following purposes:

- Elimination of housing problems (buying an apartment or a larger house).

- Children's education. Capital is allowed to pay for the education of any of the children in the family. You can pay with the amount of maternity capital to study at the desired accredited educational institution in the Russian Federation.

- Compensation for expenses for disabled children.

- To pay for the pension of the child’s mother, its funded part.

The use of capital for other needs is punishable by Russian law and is criminally punishable.

Maternity capital is registered at the Pension Fund branch. You are allowed to submit a package of documents at any convenient time. To receive capital, a personal certificate is required.

Basic documents for receiving funds:

- statement;

- parents' passports;

- children's birth certificate.

From the employer

An employer can pay financial assistance to employees upon the arrival of a child in the family; to do this, you need to write an application, to which you must attach the documents required by company regulations. But this payment is not mandatory and is paid solely at the request of the company. Therefore, the application will not necessarily receive a positive response.

The Labor Code does not provide for regulation of this payment. The conditions must be specified in the employment and collective agreement, and it must also indicate what documents must be attached to the application. As a rule, these should be:

- child's birth certificate;

- certificate of income of the second parent.

Registration with the employer

Let's consider the procedure for preparing documents to provide employees with such financial assistance.

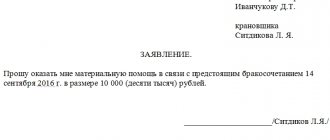

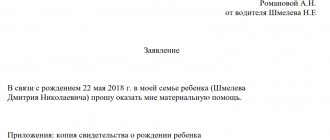

Step 1. The employee draws up an application for financial assistance at the birth of a child addressed to the head of the organization.

Step 2. Attaches documents:

- certificate and birth certificate issued by civil registry authorities (for each);

- an extract from the decision to establish guardianship (a copy of the court decision on adoption that has entered into legal force, a copy of the agreement on the transfer of one or more children to a foster family).

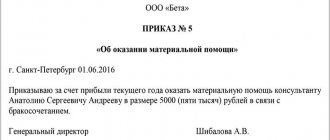

Step 3. Based on the application, the head of the organization issues an administrative document (order) on the appointment of financial assistance in the exact amount specified.

Step 5. After the calculations, the accounting department generates a payment document. If the organization has adopted a non-cash form of payment for wages, financial assistance is transferred to the employee’s card. If cash payments are used, an expense cash order is issued.

Financial assistance for the birth of a child from the employer is provided to one of the parents. The intricacies of providing this payment in 2021 will be discussed in this article.

Taxation and contributions, deduction code

Tax deductions can also be considered one of the types of financial assistance. For example, the amount of financial assistance up to 50,000 rubles is not subject to personal income tax.

The employee has the right to independently decide whether to use this type of assistance or not. The employee must also provide documents independently. The limit on the standard deduction in 2018 was 391,454.79 rubles. If the total income from the beginning of the year is more than this amount, then the right to deduction disappears.

Also, for the first and second child, you can receive a deduction in the amount of 1,400 rubles, for the third and subsequent children, a deduction of 3,000 rubles.

In addition, insurance premiums are not charged for financial assistance for the birth of a child; the non-taxable amount is 50,000 rubles.

The employer submits a 2-NDFL certificate to the inspectorate - the deduction for the child is indicated in it as a separate line for each employee. To fill out the certificate, tax deduction codes for children are used (they are detailed in the Order of the Federal Tax Service of the Russian Federation).

For example, the deduction code for the first child is 126, for the second - 127, for the third and next - 129, for a disabled child under 18 years old (provided that he is studying full-time, then from 18 to 24 years old, from I or II disability group) - code 129.

What does it mean

It is through this code that the material assistance allocated by the manager to former or current employees is displayed. The legislator notes the point that there are types of income receipts that are not subject to taxes, but all of them, one way or another, must be reflected within the tax documentation.

- If there is a deduction to state funds under the receipt, then it must be subject to mandatory indication in the reporting papers.

- If we are talking about income that is not subject to tax calculation, then it is not indicated in the declaration.

The legislation also provides for the fact that different types of revenue require the calculation of taxes at different rates. It is also very important to ensure that this document is filled out correctly and the required codes are indicated. Registration of a certificate also includes a certain set of rules and nuances:

- Registration is carried out strictly on a specialized template - a form, which is established by the powers of government bodies.

- The document should display data relating to the employee and the employer.

- All income receipts are generated strictly in code format. If it was not possible to find the necessary information in the directory, the amounts may be indicated under the value 4800.

It should be taken into account that modern computer technologies and systems, created for the correct implementation of all settlement actions, initially include a specialized algorithm that determines the % rate for certain types of profit.

Thus, it is easy to guess that it is necessary to ensure that the correct code is specified for the correct implementation of the calculation process. Upon completion of the preparation of reporting documentation, it is mandatory to indicate information on the tax that was calculated and collected by the state. If for some reason this does not happen, the chapter remains blank.

Sample payment order

Basic requirements when filling out a payment order:

- Payer status – the person making the payment (01 – legal entity; 02 – tax agent, etc.).

- When indicating tax payments in the fields provided, you should carefully fill in the account numbers and bank names.

- Priority of payment (for tax contributions - 5).

- BCC (104) must be indicated as valid at the time of payment.

- OKTMO code – indicated at the location of the legal entity.

- The period for which the insurance or tax contribution is paid.

The form of the payment order does not change; the only thing that differs when transferring insurance premiums in case of disability due to maternity is the KBC.

Insurance premiums in case of disability due to maternity are paid according to KBC 182 1 02 02090 07 1010 160 from January 2021.

Can both parents receive financial assistance?

According to current legislation, both parents can receive financial assistance from the employer, but it is important not to forget that the non-taxable amount of 50,000 rubles consists of total birth benefits.

What to do if management refuses to pay financial assistance?

The fact is that a financial payment from an employer is voluntary assistance from an organization. This payment is not regulated by the Labor Code, so the employer has every right not to pay it.

Is it possible to receive payment before the birth of the child?

No, the payment is made only after the birth of the child, and the basis is a document confirming the birth.

One-time benefit for the birth of a child, personal income tax code

Line 050 indicates the date and number of the entry in the register of accredited organizations operating in the field of information technology, based on the received extract from the register sent by the authorized federal executive body.

Unemployed citizens, in order to receive a one-time benefit at birth in 2021, must visit the department of the social security authority at their place of residence, providing, in addition to the above documents confirming the birth (adoption) of a child, the following:

Accounting entries

When paying out financial assistance, the postings may differ; it depends only on the source of the payment.

In the case when these payments are made from retained earnings from previous years:

Dt 87 Kt 73 (76) It must be remembered that retained earnings can be transferred to provide financial assistance to employees only with the consent of the founders or shareholders of the company.

If the current year’s profit is used for financial assistance:

Dt 91.2 Kt 73 (76)

The founders' permission is not required. Such a decision can be made by the management of the organization.

Financial assistance issued:

Dt 73 (76) Kt 50 (51)

At the birth of a child, a woman has the right to financial assistance both from the organization in which she works and from the state. Even if a woman has never worked before having a child, she can count on financial support from the state.

Of course, these cash receipts will not solve the financial issue once and for all, but, nevertheless, they will serve as a good help. After all, right after birth it is necessary to purchase a lot of things necessary for the child. Therefore, it is important to know your rights and timely collect and submit the necessary documents for each payment location.

Fresh materials

- Clarification on 4 FSS When it is necessary to adjust 4-FSS The calculation presented in the FSS in form 4-FSS does not need adjustments if...

- Social tax 2021 Tax accrualIn accounting, the amounts of advance tax payments are reflected in the credit of account 69 (68)…

- Tax planning Tax planning in an organization Tax planning can significantly affect the formation of the financial results of an organization,…

- Why do they buy gold? Selling gold competently is a process that will require you to spend some free time. It will be necessary to find out...

Financial assistance for the birth of a child in 2021: application and postings

Dt 84 – Kt 73(76) Note that it is possible to use retained earnings to provide financial assistance from the employer at the birth of a child only with the permission of the founders or participants/shareholders of the company, adopted at the general meeting. Accordingly, when an organization has a single founder, a general meeting is not held.

If the pregnancy progresses well and the birth is normal, she will be given a certificate of temporary incapacity for work for 2 months before giving birth and for three months after. And if complications arise during labor and delivery, sick leave is issued for a larger number of days.

We recommend reading: Housing and Utilities Benefits for Combat Veterans in 2021

Application from an employee

The basis for the accrual and payment of financial assistance at the birth of a child is an application from the employee and an order from the organization. The application form is arbitrary addressed to the head of the organization with a request for assistance. The application does not indicate the amount of payment, since it is set by the employer.

The application must be certified by the personal signature of the employee indicating the date of preparation:

After agreement with the manager, based on the application, an order is drawn up for the organization, which indicates the amount of payment. It serves as a guide to action for accounting.

Help from the employer

At the birth of a child, the father or mother can receive feasible financial assistance from the employer. Such a measure of employee support should be provided for by the internal local acts of the enterprise or organization.

The Labor Code of the Russian Federation does not oblige employers to create a fund for additional financial assistance, but does not prohibit doing so.

If the employer has foreseen in advance the possibility of providing financial assistance at the birth of a child to an employee, in 2021 the following may apply for it:

- employees who are on maternity leave after the birth of a baby;

- workers who became fathers.

To receive financial support from the employer, you will need to write an application and document the birth of the baby.

Support size

Payments from the employer cannot be the same for all enterprises in the country. Each employer independently determines the general annual limit on providing financial assistance to employees, as well as on specific payments.

In 2021, an employee can receive financial assistance at the birth of a child if he writes a corresponding application addressed to the manager. The payment amount is governed by the following factors:

- the amount established by the collective or labor agreement upon the occurrence of this event;

- the amount specified in the employee’s application for financial assistance.

Taxation of financial assistance

Any receipt of funds, including financial assistance to employees at the birth of a child, is income and therefore must be subject to personal income tax. However, Russian legislation provides for the use of benefits for young parents if the following conditions are met:

- the payment was received within a year from the date of birth of the baby;

- the entire amount is transferred to the recipient at a time.

If there are no violations, the amount is not subject to taxation.

Financial assistance from the employer

Not a single legislative act provides for the obligation to pay financial aid to an enterprise or individual entrepreneur to its employees. Obligations can be secured by a local internal document.

If there is no such provision in the collective agreement, then financial assistance for the birth of a child from the employer is exclusively an “act of goodwill.”

Amount and source of payment

Financial assistance is paid at the expense of the net profit remaining at the disposal of the enterprise, and is not limited to the maximum amount.

To receive the employee, the following documents must be submitted:

- an application for financial assistance in any form addressed to the manager, indicating the reason (for the birth of a child); a copy of the birth certificate or a certificate from the registry office; a certificate of non-receipt of financial assistance by the second parent (in case of non-receipt) or form 2-NDFL indicating the amount (in case of receipt).

- What are the salary supplements?

Reflection in accounting

| Postings | % of charges | Sum, | Normative | Business transaction | |

| Dt | CT | and deductions | rubles | document | |

| 84 | 70 | — | 60000 | Director's order | Financial assistance awarded |

| 70 | 68 | 13 | 1300 | Article 224 of the Tax Code of the Russian Federation | Personal income tax withheld from 10,000 rubles |

| 84 | 69.1 | 2,9 | 290 | Article 426 of the Tax Code of the Russian Federation | Contribution to the social insurance fund has been accrued |

| 84 | 69.2 | 22 | 2200 | Article 426 of the Tax Code of the Russian Federation. | Contribution to the pension fund has been accrued |

| 84 | 69.3 | 5,1 | 510 | Article 426 of the Tax Code of the Russian Federation | Contribution to the health insurance fund has been accrued |

| 70 | 50 | 50000 + (100000 — 100000*0,13) | 58700 | — | Financial assistance was paid from the company's cash desk to the employee |

| 68 | 51 | — | 1300 | Article 224 of the Tax Code of the Russian Federation | Personal income tax transferred to the budget |

| 69 | 51 | 290+2200+510 | 3000 | Article 426 of the Tax Code of the Russian Federation | Contributions to social funds are transferred |

Financial assistance is paid regardless of the financial results of the enterprise and the personal contribution of the recipient as a specialist. It does not belong to the wage fund either as a salary or as a bonus, since it does not require the fulfillment of production targets.

Therefore, they are not taken into account in income tax expenses (clause 23 of Article 270 of the Tax Code of the Russian Federation) and are not reflected in tax accounting. Financing is provided from our own sources.