Maintaining records of authorized capital

The process of forming a company's own fund begins even before it is incorporated. In this case, we are talking about the contribution of monetary resources or property when registering a company, which represents a key source of obtaining own funds.

Authorized capital should be understood as the cost expression of fixed and working resources that are contributed by the founders when registering an enterprise to carry out activities that are indicated in its constituent documents. Based on the volume of the designated fund, one can judge the amount of invested resources. And it is with the formation of this resource that the company begins its activities.

According to current regulatory documents, the debt of members of the company as a contribution to the registered capital is reflected by the entry:

1) Dt 75

Kt 80.

You can contribute funds as a founder in the following ways:

- by depositing financial resources into a current account opened with one of the credit institutions;

- by transferring funds from a personal deposit to the deposit of a newly created organization.

The legislation introduced such a concept as the minimum amount of registered equity capital, the level of which depends on the form of ownership. If, for example, earlier for limited liability companies the minimum permissible amount of these resources was fixed, and in the case of joint-stock companies and public joint-stock companies it depended on the size of the minimum wage, then today the legislation states:

- the established minimum size for closed joint stock companies and LLCs is 10,000.0 rubles;

- for JSC this figure reaches 100,000.0 rubles.

Accounting for reserve capital (account 82)

Reserve capital is one of the components of an enterprise’s own capital, along with authorized and additional capital. Reserve capital is formed on account 82, with a loan the reserve capital is formed and increased, with a debit it is reduced (used).

Reserve capital is not formed by all organizations; many enterprises do without reserves, but in some cases it is required to be formed. In particular, joint-stock companies must reserve funds, but other organizations create reserves at their own discretion, in accordance with their constituent documents and accounting policies adopted by the organization.

Reserve funds can be spent on possible unforeseen expenses that may arise during the operation of the enterprise. JSCs can use these funds to buy back their own shares.

Reserve capital consists primarily of a reserve fund. In addition, it may include other funds, for example, a special fund for the corporatization of employees, a special fund for the payment of dividends on preferred shares. The composition of the reserve capital is prescribed in the company's charter.

The procedure for forming reserve capital

A reserve is formed at the beginning of the year, when the net profit received for the year is distributed. At the end of the year, a meeting of the founders is held, at which the reporting date is approved, various decisions are made, net profit for the year is distributed, including a decision on the creation or replenishment of reserve capital.

The amount of reserve capital for joint stock companies has a minimum limit, which cannot be lower - 5% of the authorized capital. The actual amount of the reserve is established by each organization independently (taking into account the minimum limit). The amount of reserve capital is specified in the constituent documents. All other organizations can create reserve capital of any size; there are no restrictions in this case.

Thus, at the beginning of the year, funds from net profit can be spent to replenish reserve capital. Replenishment occurs up to the amount specified in the company's charter.

A reserve is formed on account 82 “Reserve capital”. At the same time, you can not use a separate account 82, but create a reserve directly in account 84 Retained earnings (uncovered loss) separately in a separate subaccount.

Postings to account 82:

D84 K82 – replenishment of reserve capital with funds from net profit received during the reporting year.

D82 K84 – reserve funds cover losses incurred during the year.

The role and significance of position 75

75 account is active-passive in nature, i.e. its balance at the end of the reporting period can be either debit or credit. It is necessary for maintaining analytical records of transactions related to settlements with holders of company shares. In this situation, we are talking about the following types of operations:

- completion of registered equity capital when creating a company;

- increasing the volume of the designated initial resource in the enterprise’s activities;

- reduction in the level of capital of the company's owners;

- repurchase of shares or shares of shareholders;

- distribution of dividends;

- payment of loans to shareholders of the created company.

At the same time, accounting reflects settlements with the owners of the company in the company’s financial statements. If on the date of drawing up the balance the account balance is debit, then it is transferred to line 1230 of the “Assets” section of Form No. 1; if there is a credit balance, it is transferred to line 1520 of the balance sheet liability.

Active or passive?

Account 75 is active-passive; it can simultaneously account for both the assets and liabilities of the organization.

In this case, the balance can be either a debit or a credit.

Account 75 can behave as active, then it will be characterized by the properties of active accounts, and it can also behave as passive.

Characteristics - that debit and credit, subaccounts are shown

The debit of account 75 shows the cost of contributions that the founders must make as their share in the authorized capital. The debit also reflects the payment of dividends.

The credit of account 75 shows the value of the deposits made by the company's participants in the management company. In addition, the loan also takes into account the accrual of dividends in favor of the founders.

In accordance with the instructions for accounting account 75, the following sub-accounts can be opened on it:

- 01 – settlements on deposits in the Criminal Code: on it, accordingly, records are kept of the debt on the deposit and the amounts deposited in the Criminal Code;

- 02 – calculations for payment of income: mutual settlements between the organization and the founders for dividends are shown - accrual and payment;

- 03 – other mutual settlements that are not reflected in subaccounts 01 and 02.

The organization has the right to maintain analytical accounting in accordance with Article 75.

It is convenient to conduct analytics in the context of each founder, this will allow you to track the payment of shares by each of the participants, the accrual and payment of dividends to them depending on the size of their shares in the authorized capital.

Accounting

75 accounting account is intended for accounting for contributions to the authorized capital and for accounting for the distribution of income. Deposits are reflected in 01 sub-account, dividends in 02 sub-account.

Accounting for contributions of shares to the capital includes making entries to reflect the founders' debt on deposits and their payment - the debit of subaccount 75.01 shows the debt on contributions (the amount of contributions that the founders must make to the authorized capital), the credit of subaccount 75.01 shows the payment of contributions (contribution of the value of shares in cash or property):

- Dt 75.01 Kt 80 – debt on deposits in the Criminal Code is reflected;

- Dt 50, 51, 52, 55 (10, 08, 15, 20, 41) Kt 75.01 – payment of contributions is reflected.

In addition, the debit of subaccount 75.01 reflects additional contributions of participants to the capital account when it increases: entry Dt 75.01 Kt 80 - increase in the capital account due to additional contributions.

Accounting for dividends is carried out using subaccount 75.02: the debit shows the payment of dividends, and the credit shows their accrual:

- Dt 75.02 Kt 84 – accrual of dividends to the founders in accordance with the retained earnings received;

- Dt 75.2 Kt 83 – distribution of additional capital of the company between participants;

- Dt 50, 51, 52 Kt 75.02 – payment of dividends.

Posting examples

The table below shows the main transactions that are made on the debit and credit of account 75 in the course of the organization’s activities:

| Operation | Debit | Credit |

| By debit of account 75: | ||

| The authorized capital of the company has been formed (the debt of the founders to the organization for contributions to the management company) | 75.01 | 80 |

| Increasing the authorized capital due to additional contributions from participants | 75.01 | 80 |

| Payment of income in money (cash, non-cash, currency) | 75.02 | 50, 51,52 |

| Withholding taxes on dividends | 75.02 | 68 |

| Write-off of debt on accrued income due to the expiration of the statute of limitations | 75.02 | 91 |

| For loan 75 account: | ||

| Contribution to the authorized capital through the cash desk in cash | 50 | 75.01 |

| Depositing a share to a current account | 51 | 75.01 |

| Deposit in foreign currency | 52 | 75.01 |

| Property contribution in the form of materials | 10 | 75.01 |

| Fixed assets (equipment, movable, immovable property) are included in the Criminal Code | 08 | 75.01 |

| Acceptance of payment for a share in the form of fixed assets for accounting | 01 | 08 |

| Contribution of a share in the form of goods | 41 | 75.01 |

| Reducing the authorized capital by returning the share to the participant | 80 | 75.01 |

| Accrual of income from retained earnings | 84 | 75.02 |

| Distribution of additional capital | 83 | 75.02 |

Typical transaction transactions

In practice, relationships with founders are reflected in the following accounting entries:

1) Dt 07.08, 10, 11, 15 or 41

Kt 75 – contribution of valuable property as a contribution to the authorized capital;

2) Dt 50, 51 or 52

Kt 75 – contribution to your own registered fund of monetary resources;

3) Dt 58

Kt 75 – financial investments in founder’s capital;

4) Dt 80

Kt 75 – change in the size of the founding fund;

5) Dt 84

Kt 75 – accrual of income to company participants based on the results of the reporting period;

6) Dt 75

Kt 50, 51 or 52 – payment of accrued income to company participants;

7) Dt 75

Kt 80 – debt of the founders for contributions to the capital of the owners of the company;

Dt 75

Kt 91 – writing off the debt of the founders after the expiration of the limitation period;

9) Dt 75

Kt 83 – taking into account the difference between the nominal and market value of shares, etc.

Features of working with score 75

The main purpose of account 75 in the accounting of an organization is to record settlements with the founders of the company. The number of transactions for which accounting is kept within the designated account includes:

- contributions to the authorized capital of the company at the stage of its creation;

- increase or decrease in the amount of the authorized capital;

- repurchase of shares from a shareholder or their sale;

- payment of dividend amounts on shares;

- providing loans and paid copies of documents to founders.

Count 75 – active-passive. It can carry both positive and negative remainders. In the first case, transactions are recorded as a debit of the account, and in the second - as a credit. In addition, the account reflects general information about settlements with each of the founders. To maintain full-fledged detailed accounting, additional sub-accounts are opened for account 75:

- 75.01 – contributions to the authorized capital;

- 75.02 – payment of income.

Analytical accounting is maintained separately for each founder in a separate open sub-account. Subsequently, the indicators are combined into a total score of 75.

One of the cases in practice

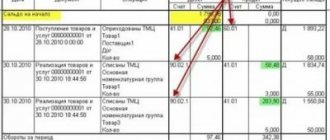

Let's assume that a certain LLC was registered, the authorized capital of which was 130,000.0 rubles. Part of these funds, or 25%, was contributed in cash, and the remaining amount was formed by contributing a passenger car. At the same time, the accountant of the newly created LLC made the following entries:

1) Dt 75

Kt 80 – 130,000.0 rubles, debt of the founders for contributions to the management company;

2) Dt 50

Kt 75 – RUB 32,500.0, depositing cash as a contribution to the management company;

3) Dt 01

Kt 75 – 97,500.0 rubles, accounting for the cost of the car as a contribution to the management company.

Typical accounting entries for account 75

Since the list of transactions carried out on account 75 is very wide, we will highlight only the most significant and frequently used by the accountant. We are talking about the following wiring:

| Debit correspondence | Loan correspondence | the name of the operation |

| 75 | Calculations of contributions to the company's management company | |

| , , | 75 | Contributions from founders, including contributions to temporary savings accounts |

| 75 | Fixing the cost of fixed assets or intangible assets on the balance sheet of the enterprise | |

| , | 08 | Arrival of OS and intangible assets |

| 10, 41 | 75 | Goods contributed as a contribution to the management company are capitalized |

| 75 | Reflection of financial investments, including shares | |

| 66 | 75 | The loan debt is offset against the share of the company's management company |

| 75 | 50, 51 | The founders were paid the difference by which the authorized capital was reduced |

| 81 | 75 | Debt to the founder who left the organization, and distribution of the remaining amount among the remaining founders |

There are many other transactions associated with the provision of loans to founders, as well as the sale or purchase of shares. Their use is independently regulated by the company’s management and is prescribed in the accounting policies.