Account 03 - what is it for?

Account 03 is called “Profitable investments in material assets.”

On it, accountants keep records of inflows and outflows of such assets. An important condition is the material form. Intangible assets cannot be taken into account in account 03. Do not confuse count 03 with count 01. They are similar, but are intended for different purposes. Account 01 records fixed assets that the company purchased to use for the production of goods, performance of work, provision of services or management of these processes. An additional purpose for the purchase may be rental or leasing.

On account 03, you can only take into account those objects on which the business will earn money by renting or leasing to other companies. If the object is used in the production process, it is sent to account 01. The accountant, together with management, decides on which account to record the fixed asset.

Example . A large supplier of medical equipment, MedSi LLC, purchased a building in the city center and medical equipment for a dental office. He will rent out his property to a group of dentists for a monthly fee, and they will work in his building and on his equipment. Such an investment by MedSi LLC will be reflected in account 03.

Examples of transactions and postings for account 03

Example No. 1. Purchase and lease of vehicles

For example, on behalf of a motor transport company, a leasing company purchased 5 buses. There is a consignment note from JSC Avtotekhnika No. 8 dated 04/17/2014. in the amount of RUB 9,500,000, incl. VAT RUB 1,449,152.54 A purchase and sale agreement was concluded between the leasing company and Avtotekhnika JSC.

Subsequently, a vehicle leasing agreement was concluded between the leasing company and the motor transport enterprise for 4 years with the right to purchase.

The vehicles were transferred to the lessee in accordance with the transfer acceptance certificate.

Leasing company on the general taxation system.

According to the accounting policy, for accounting purposes, the amount of depreciation charges for property that is the object of leasing with the right to purchase is determined by the linear method based on the useful life corresponding to the term of the leasing agreement.

The duration of the leasing agreement is 48 months. Consequently, the period during which the use of leased property brings economic benefits is also 48 months.

In the accounting records of the leasing company, entries have been created where:

- Account 03.1 - property of the leasing company;

- Account 03.2 - property transferred to the lessee:

| Dt | CT | Amount, rub. | Wiring Description | Document |

| 08 | 60 | 8 050 847,46 | The costs of purchasing vehicles are reflected | Bill of lading, purchase and sale agreement |

| 19 | 60 | 1 449 152,54 | VAT allocated | Invoice |

| 68 | 19 | 1 449 152,54 | VAT is deductible | Invoice |

| 03.1 | 08 | 8 050 847,46 | Vehicles registered | Act of Handover |

| 03.2 | 03.1 | 8 050 847,46 | Vehicles are leased | Act of Handover |

| 20 | 02 | 167 725,99 | Monthly depreciation since May 2014. | Accounting certificate-calculation 8050847.46/48 months |

Characteristics of account 03

03 account is active. The debit reflects the increase in the value of the asset, and the credit reflects the decrease. The balance (balance) of account 03 can only be debit, since credit would mean a negative value of the asset, which is impossible.

To calculate the balance at the end of the period, you need to add the debit balance to the beginning balance and subtract the credit balance. To simplify, we calculate using the formula:

Balance = how much was + how much came - how much went out.

Where is account 03 located in the chart of accounts and where to find it in the accounting records

Account 03 “Profitable investments in material assets” is located in section 1 of the chart of accounts, approved. by order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n. This section is called “Non-current assets”.

Income-bearing investments in material assets are reflected in the accounting records, or more precisely in the balance sheet, at their residual value as part of non-current assets on line 1160 of the same name in Section 1. Information about income-generating investments is also subject to disclosure in the explanations to the balance sheet and the financial results report (clause 32 of PBU 6/01 ; table 2 from Appendix 3 to the order of the Ministry of Finance of Russia dated July 2, 2010 No. 66n).

NOTE! The residual value of income-generating investments in the balance sheet is determined by subtracting the credit balance on account 02, which relates specifically to income-generating investments, from the debit balance on account 03.

How the value of profitable investments in material assets is formed

Fixed assets are accepted into account 03 at their original cost. It is formed from the following expenses:

- costs of purchasing the asset (excluding VAT and other refundable taxes);

- consultants and intermediaries;

- delivery;

- installation and installation;

- payments at customs.

Let us remind you that before transferring to account 03, the fixed asset will always go to account 08 “Investments in non-current assets”. This simplifies the calculation of the initial cost, since it is formed over time.

Example . An individual entrepreneur bought an office space with rough finishing for rent. First, you need to make repairs, arrange sockets, hang a lamp, buy furniture - all these expenses are sent to account 08 and remain there until the office is completely ready for rent. After this, the entire initial cost is transferred to the debit of account 03.

Depreciation of income investments in MC is similar to depreciation of fixed assets and is reflected in account 02. It makes sense to open a sub-account for the depreciation account, since the parties to the leasing agreement can apply accelerated depreciation.

Keep records of exports and imports in the Kontur.Accounting web service. Simple accounting, payroll and reporting in one service

Renting or leasing – what types of profitable investments are there?

The cost of a leased fixed asset can only be taken into account when it is actually a lease. There are two types of rent - property and financial (leasing). A classic lease means the following transaction:

- the object passes to another person temporarily and not forever;

- the lessor does not lose rights to the property;

- Tenants can use the property, but cannot dispose of it.

If we are talking about financial lease (leasing), the tenant buys the object from the owner only upon completion of the period specified in the agreement. In this case, the parties may decide that during the validity of the agreement the property will be on the balance sheet of the recipient, but ownership will remain with the lessor.

Analytical accounting and subaccounts

You can consider analytics for account 03 by type of material assets, by their individual objects, or by tenants/lessees. The following subaccounts can be distinguished:

- MC for rent/leasing;

- MCs rented out/leasing;

- disposal of MC facilities.

If there are subaccounts, the initial cost of the fixed asset will be transferred from Kt 08 to Dt 03 “MC for renting/leasing”. Having transferred the fixed assets for rent, you should transfer it to another subaccount by posting Dt 03 “MC, rented out/leasing” Kt 03 “MC for renting/leasing”.

The disposal of investments is reflected in accounting by the following entries:

- Dt 03 “Disposal of MC” Kt 03 - write-off of the original cost;

- Dt 02 Kt 03 “Disposal of MC” - accumulated depreciation;

- Dt 91 Kt 03 “Disposal of MC” - write-off of residual value.

Basic accounting rules

The account is active, so the debit shows the receipt of fixed assets, and the credit shows their disposal. Property recorded on the account is depreciated. 03, to account 02, like any fixed asset.

Analytical accounts for accounts. 03 are opened for each property and each tenant. The object is accepted for accounting in account 03 at its original cost, the rules for determining which are established in PBU 6/01. Final account balance 03 is the cost of the property that has been transferred or will be transferred for use. In the balance sheet it is shown as part of fixed assets at residual value, that is, minus depreciation.

Correspondence of account 03 with other accounting accounts

We have already found out that account 03 corresponds with accounts 02, 08 and 91. But these are not all possible combinations. Let's consider all the options:

| By debit | By loan |

| 08 “Investments in non-current assets” 76 “Settlements with various debtors and creditors” 80 “Authorized capital” | 01 “Fixed assets” 02 “Depreciation of fixed assets” 76 “Settlements with various debtors and creditors” 80 “Authorized capital” 91 “Other income and expenses” 94 “Shortages and losses” 99 “Profits and losses” |

Table of main accounting entries for account 03

| Dt | CT | Wiring Description | A document base |

| 03 | 08 | Property accepted for registration | Transfer and Acceptance Certificate |

| 03 | 80 | Income investments accepted as a contribution to the authorized capital | Decision of the general meeting of participants |

| 94 | 03 | Shortage (damage) of property listed on account 03 | Write-off act |

| 99 | 03 | The cost of profitable investments is included in extraordinary expenses | Write-off act |

| 91.2 | 03 | The residual value of the disposed income investment is reflected | Transfer and Acceptance Certificate |

Income investments: concept and types

Income investments are understood as funds capitalized in the form of acquired material assets in order to obtain additional benefits from their use. The main types of profitable investments are buildings, premises, production and other equipment, vehicles and other fixed assets.

To receive income from investments, organizations, as a rule, transfer valuables for temporary use and ownership to other enterprises and organizations for a fee. The basis for the transfer of property is an agreement (rent, leasing, etc.), as well as an acceptance certificate confirming the fact of receipt of valuables by the tenant.

Modern practice shows that property that acts as income-generating investments is most often cars (car rental services) and premises (residential and industrial).

| ★ Best-selling book “Accounting from scratch” for dummies (understand how to do accounting in 72 hours) > 8000 books purchased |

Account 03. Accounting of transactions using examples

For a detailed examination of the features of accounting for transactions on account 03, we use examples of typical situations.

Account 03. Renting out your own equipment

Example No. 1.

Let’s say that JSC “Kolosok” purchased from LLC “Selkhoztekhnik” a machine and tractor unit for pre-sowing tillage at a price of 484,620 rubles, VAT 73,925 rubles. On March 25, 2016, Kolosok entered into a leasing agreement with Fermer LLC, according to which the tractor was leased. The useful life of the machine-tractor unit is set at 7 years.

The Koloska accountant reflected the transactions of purchasing a tractor and leasing it as follows:

| Debit | Credit | Operation description | Sum | A document base |

| 08 | 60 | The amount of expenses for a tractor purchased from Selkhoztekhnik LLC for subsequent leasing is taken into account (RUB 484,620 – RUB 73,925) | RUR 410,695 | Sales contract, delivery note |

| 19 | 60 | The amount of VAT on the cost of the purchased machine and tractor unit is taken into account | RUR 73,925 | Invoice |

| 60 | 51 | Payment was made to “Agricultural Equipment” for the purchased tractor | RUR 484,620 | Payment order |

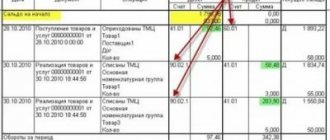

| 03 Property owned | 08 | A tractor purchased from Selkhoztekhnik LLC was registered for subsequent leasing | RUR 410,695 | Transfer and Acceptance Certificate |

| 68 VAT | 19 | The amount of VAT on the purchased tractor is accepted for deduction | RUR 73,925 | Invoice |

| 03 Property under lease | 03 Property owned | The tractor was transferred to “Farmer” under a lease agreement | RUR 410,695 | Transfer and Acceptance Certificate |

| 20 | 02 | The amount of depreciation accrued on the machine and tractor unit for April 2021 is reflected (RUB 410,695 / 7 years / 12 months) | RUB 4,889 | Depreciation statement |

Example No. 2.

Let's consider a situation where, when purchasing property for leasing, an organization incurred additional expenses paid through an accountable person.

The activities of JSC “Kladovshchik” are related to the rental of warehouses and other utility premises.

In February 2021 “Storekeeper”:

- purchased premises for a food warehouse from JSC Monolit at a price of 1,240,600 rubles, VAT 189,244 rubles;

- paid the expenses for registration of the premises in the amount of 2,760 rubles, the amount of which was paid through an employee of JSC “Storekeeper” Isaev V.R.;

- leased the warehouse to Products Plus LLC.

It has been established that the useful life of the warehouse premises is 11 years.

Here is how the above operations were reflected in the “Storekeeper” accounting:

| Debit | Credit | Operation description | Sum | A document base |

| 08 | 60 | The amount of expenses for a food warehouse purchased from Monolit for subsequent leasing is taken into account (1,240,600 rubles - 189,244 rubles) | RUB 1,051,356 | Purchase and sale agreement, transfer and acceptance certificate, certificate of ownership |

| 19 | 60 | The amount of VAT on the cost of purchased warehouse premises is taken into account | RUR 189,244 | Invoice |

| 60 | 51 | A settlement has been made with Monolit JSC | 1,240,600 rub. | Payment order |

| 71 | 50 | Isaev was given an advance for household needs (calculations for the design of a warehouse) | RUB 2,760 | Account cash warrant |

| 08 | 71 | Savelyev received permits for the premises | RUB 2,760 | Advance report |

| 03 Property owned | 08 | The cost of the premises is reflected as part of income-generating investments (RUB 1,051,356 + RUB 2,760) | RUB 1,054,116 | Purchase and sale agreement, transfer and acceptance certificate, certificate of ownership, permitting documents |

| 68 VAT | 19 | VAT deduction on purchased premises has been taken into account | RUR 189,244 | Invoice |

| 03 Property under lease | 03 Property owned | The transfer of the warehouse to the use of LLC “Products Plus” is reflected | RUB 1,054,116 | Transfer and Acceptance Certificate |

| 20 | 02 | The amount of accrued depreciation for the leased premises was carried out (RUB 1,054,116 / 11 years / 12 months) | RUR 7,986 | Depreciation statement |