You should start filling out the tax return from sections 2.1.1 and 2.1.2 (for subjects of the simplified tax system that have chosen “income” as the object of taxation) or 2.2 (for subjects of the simplified tax system that have chosen “income minus expenses” as the object of taxation). Next, based on sections 2.1.1, 2.1.2 or 2.2, section 1.1 or 1.2 is filled in, respectively. Lastly, the title page is drawn up. Section 3 can be completed in any order, because The information presented in this section does not participate in the calculation of indicators in other sections of the declaration.

When filling out the declaration, you should pay attention to the fact that the lines “TIN” and “KPP” in each section are filled in automatically from the client’s registration card. The page serial number is also indicated automatically.

Attention! The declaration can be completed in the usual way, i.e. by sections (see here) and simplified with the help of a wizard.

- Filling using the wizard

- Title page

- Section 1.1. The amount of tax (advance tax payment) paid in connection with the application of the simplified taxation system (object of taxation - income), subject to payment (reduction), according to the taxpayer

- Section 1.2. The amount of tax (advance tax payment) paid in connection with the application of the simplified taxation system (the object of taxation is income reduced by the amount of expenses), and the minimum tax subject to payment (reduction), according to the taxpayer

- Section 2.1.1. Calculation of tax paid in connection with the application of the simplified taxation system (object of taxation - income)

- Section 2.1.2. Calculation of the amount of trade tax that reduces the amount of tax (advance tax payment) paid in connection with the application of the simplified taxation system (object of taxation - income), calculated based on the results of the tax (reporting) period for the object of taxation from the type of business activity in respect of which In accordance with Chapter 33 of the Tax Code of the Russian Federation, a trade tax has been established

- Section 2.2. Calculation of the tax paid in connection with the application of the simplified taxation system and the minimum tax (the object of taxation is income reduced by the amount of expenses)

- Section 3. Report on the intended use of property (including funds), work, services received as part of charitable activities, targeted income, targeted financing

Deadlines for submitting reports to the simplified tax system “income-expenses” for 2019

| Who rents | When is it available for rent (inclusive) |

| Organization | until March 31, 2021 |

| IP | until April 30, 2021 |

If the deadline for submitting the declaration falls on a weekend or holiday, it is postponed to the next working day (Clause 7, Article 6.1 of the Tax Code of the Russian Federation). In 2021, the deadline for submitting simplified reports does not fall on weekends and therefore will not be postponed.

If you lose your right to the simplified tax system, the declaration must be submitted by the 25th day of the month following the quarter in which you violated the rules for applying the simplified tax system (clause 3 of article 346.23 of the Tax Code of the Russian Federation). If you voluntarily refuse the simplified tax system, the reports must be sent to the Federal Tax Service by the 25th day of the month following the day you removed the simplified tax system (submitted an application on form 26.2-8).

Basic rules for entering data

There are two options for filling out the reporting document: by hand and on the computer . In the first case, use a pen with black ink and write in capital letters. When printing a computer version, double-sided printing is not allowed: the back side of each page of the form must be left blank.

If no information is indicated in the column, then a dash is placed in it. Financial calculations are rounded to the nearest ruble. The sheets are numbered consecutively.

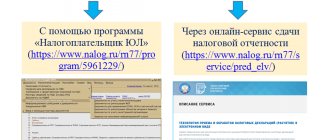

The reporting document can be filled out online on specialized resources that will help you make the correct calculation and check for errors before sending or printing the document.

Declaration form for the simplified tax system “income minus expenses”

In 2021, the reporting form for the simplified tax system has not changed; the declaration for 2021 must be submitted as before, on a form, approved. By Order of the Federal Tax Service of the Russian Federation dated February 26, 2016 No. ММВ-7-3/ [email protected]

For the simplified tax system “income-expenses” the following sections of the declaration are required to be completed:

- Title page.

Contains basic information about the simplifier submitting the report, the tax period and the Federal Tax Service with which the organization or individual entrepreneur is registered.

- Section 1.2.

Includes data on the amounts of advance payments and tax payable (reduced) based on the results of the reporting or tax period.

- Section 2.2.

Reflects information on income and expenses, the amount of loss received, the tax rate and the amount of calculated tax at the end of each reporting (tax) period.

Section 3 (Report on the intended use of property) is completed only if you received assets as part of charity or targeted financing (according to the provisions of Article 251 of the Tax Code of the Russian Federation).

Declaration form for the simplified tax system “income minus expenses” 2019

Fill out section 2.1.1

Filling out the calculation part of the declaration begins with section 2.1.1. Here it is necessary to reflect data for the reporting period on income received and contributions paid.

The line “Taxpayer Attribute” indicates whether the subject makes payments to individuals or not. Organizations and individual entrepreneurs indicate “1”, and entrepreneurs without employees - “2”.

Next come lines 110-130, in which you must indicate the amount of income received. Income is reflected not for each individual quarter, but on an accrual basis:

- line 110 will reflect income for the first quarter,

- in line 111 - for half a year,

- in line 112 - for 9 months,

- in line 113 - for the entire year 2021.

The next four lines are for specifying the tax rate. The default is 6%. However, different regions may have their own rates.

Note! Many regions on their territory have established reduced tax rates under the simplified tax system. For example, in the Saratov region for certain types of activities the rate is 2%, in the Smolensk region - 4.5%, in the Tula region - 1%.

Does an entrepreneur need to submit a declaration if his activities in the region are taxed at a rate of 0%? Undoubtedly. He will not have any tax to pay, but a return must be filed. In this case, income is indicated as usual, and “0” is entered in the field for indicating the tax rate.

The next four lines with codes 130-133 are intended to indicate the accrued tax amount (advance payment) for the quarter, six months, 9 months and year. The amount is calculated by multiplying the income received for the corresponding period by the tax rate. When using special programs or services, this value is filled in automatically.

The following indicates the amounts that the subject paid in the relevant periods as insurance premiums, benefits and other payments deducted from tax .

Contributions and payments that reduce tax are reflected in the period in which they were actually made, and not in the period to which they relate.

How to reduce tax on contributions

The procedure for reducing tax on contributions and payments depends on whether the taxpayer is an employer.

- An individual entrepreneur without employees (line 102 indicates sign “2”) can deduct insurance premiums paid for himself without a 50% limitation. That is, he can reduce his tax down to zero if his amount is less than the contributions paid. In this case, lines 140-143 indicate the same amounts as lines 130-133. That is, deductions are equal to the tax amounts, and nothing should be paid to the budget. However, the data on lines 140-143 cannot be greater than the corresponding tax amounts. After all, these lines indicate the amount of the deduction, and it cannot exceed the amount of the accrued tax.

- Organizations and individual entrepreneurs with employees (code “1” in line 102) can reduce their tax by no more than 50%. In lines 140-143, such a taxpayer reflects amounts of no more than half of those indicated in lines 130-133.

This is the general case. However, if the subject pays a trade fee, then the calculation is made differently. In any case, the trading fee data does not appear in lines 140-143.

Section 2.1.1

The procedure for filling out the simplified taxation system “income-expenses” declaration for 2019

The procedure for filling out reports under the simplified tax system is prescribed in Appendix 3 to the Order of the Federal Tax Service of the Russian Federation No. ММВ-7-3/ [email protected]

General rules for filling out the declaration

When filling out a declaration under the simplified tax system, you must not only enter all the data correctly, but also correctly prepare the reporting itself. A seemingly insignificant error, for example, in the page number, binding of document sheets or ink color, can cause refusal to accept the declaration.

Let us recall the basic rules for filling out a report on the simplified tax system:

- Amounts are indicated in full rubles: values up to 50 kopecks are discarded, values above are rounded to the nearest full ruble.

- The numbering of pages in the declaration is continuous: the sheets are numbered in the order in which they appear one after another.

- If some sheets and sections are not filled out, you do not need to submit them.

- When filling out the declaration by hand, you must use black, purple or blue ink. You cannot correct errors with the corrector. It is advisable not to correct them at all, since the report is checked by a machine. It is better to redo a sheet containing an error.

- When filling out a report on a computer, use Courier New font with a height of 16-18 points. Double-sided printing is prohibited, as is stapling sheets. When using a paper clip, it is advisable not to touch the barcodes in the upper corner of the title page - damage to it may make it difficult for a machine to read the information from the report.

- Indicators are entered from left to right, starting from the leftmost cell. If the report is filled out using a special program, then the numerical indicators must be aligned to the right margin.

- The text in the declaration is indicated in capital block letters.

- If some indicator is missing, put a dash in the corresponding line. If a line is not filled in completely, then we also put a dash in its unfilled cells.

- On each page of the declaration, the Taxpayer Identification Number (TIN) (for all taxpayers) and KPP (for organizations only) are indicated.

Categories of reported income

Reporting under the simplified tax system involves reflecting all income from the activities of the HOA that is subject to taxation. The Partnership as a non-profit organization receives the following types of income :

- contributions;

- rent and utility bills;

- income from economic activities;

- subsidies from the budget;

- other income.

The legislation allows not all types of income to be reflected when calculating the tax base. Thus, contributions from partnership participants for repairs and maintenance of property are considered as received as a result of the statutory activities of the HOA and are not subject to taxation. Whereas contributions from other persons are subject to accounting in the income side of the organization’s activities with subsequent payment of taxes.

ATTENTION! If the charter of the HOA does not stipulate its obligation to supply heat, electricity, etc., then funds received from residents for utilities are included in the tax base.

If agency agreements have been concluded with residents, then only the amounts of agency fees are reflected in the income portion.

Read more about the organization’s income and how it is reflected in accounting in this material.

Sample of filling out the simplified taxation system 15% declaration

An example of calculating the tax-USN and a sample of filling out this report will help you understand the procedure for filling out the simplified tax system “income minus expenses” declaration.

Example

LLC "Kadrovik" provides accounting and legal services. The firm's income and expenses are shown in the table below:

Table 1.

| Reporting period | Amount of income, rub. (lines 210-213 of Section 2.2) | Amount of expenses, rub. (lines 220-223 of Section 2.2) |

| 1st quarter | 350 000 | 143 180 |

| half year | 720 000 | 287 360 |

| 9 months | 935 000 | 421 540 |

| year | 1 110 000 | 568 720 |

The tax rate for the simplified tax system “income-expenses” is 15%.

The accountant of Kadrovik LLC fills out the simplified taxation system declaration for 2021 based on the following data:

Table 2.

| Reporting period | Tax base, rub. (lines 240-243 of Section 2.2) | Amount of calculated tax, rub. (lines 270-273 of Section 2.2) | Amounts of advances and annual tax, rub. (lines 020, 040, 070, 100 of Section 1.2) |

| 1st quarter | 206 820 | 31 023 | 31 023 |

| half year | 432 640 | 64 896 | 33 873 |

| 9 months | 513 460 | 77 019 | 12 123 |

| year | 541 280 | 81 192 | 4 173 |

Tax payable is calculated as 15% of the difference between income and expenses.

As can be seen from Table 2, the tax on the difference between income and expenses for 2021 is 81,192 rubles. We compare this amount with the minimum tax - 1% of income for 2021.

The income of Kadrovik LLC for 2021 is RUB 1,110,000. The minimum tax on this amount is 11,100 rubles. Therefore, at the end of the year, you need to pay tax calculated in the general manner, minus the amounts of previously paid advances - 4,173 rubles.

Sample of filling out a declaration under the simplified tax system “income minus expenses” 2019

Tax base calculation

At its core, determining the tax base under the simplified tax system “income minus expenses” is very similar to a similar process when calculating income tax.

Income is divided into those received from sales and non-sales . Sales income includes revenue from the sale of goods, works and services produced by an organization or individual entrepreneur, the sale of goods that were purchased, and property rights. Included in revenue are the amounts of advances transferred by buyers against future deliveries.

Non-operating income includes other income in accordance with Article 250 of the Tax Code . For example, such income is recognized as:

- rental income;

- gratuitously received valuables and property rights;

- interest on loans issued and more.

As for expenses, a closed list of them is translated into Article 346.16 of the Tax Code of the Russian Federation . If any expenses are not on this list, then they are not included in the calculation of the tax base.

Condition for recognizing expenses included in the list:

- Economic feasibility . If the tax inspectorate doubts the need for any company expenses, they may not be recognized and excluded from expenses taken into account for tax purposes. However, a businessman can make any expenses, but at the expense of net profit.

- Documentary confirmation . It is provided by two types of documents, which, with rare exceptions, must be completed for each operation:

- a primary document (act, invoice) that confirms the fact of economic activity;

- a document evidencing payment of expenses (payment order, account statement, cash receipt).

The procedure for submitting the simplified taxation system “income-expenses” declaration

The declaration can be submitted in several ways:

- personally;

- through a representative by proxy - please note that inspections require a notarized power of attorney from the representative of the individual entrepreneur;

- by mail - we recommend sending by registered mail with an inventory and receipt of receipt;

- electronically, signing it with an electronic signature (EDS).

Entrepreneurs submit a report to the inspectorate at their place of registration. Organizations - to the Federal Tax Service at their location, that is, legal address.

In what form is the declaration submitted under the simplified tax system?

The declaration under the simplified tax system is submitted on paper or electronically.

The easiest and most reliable way to submit a declaration is to send it electronically. But in this case, your company must be connected to the document flow with regulatory authorities.

If there is no agreement with a special operator, you can send the document by mail.

And another method that individual entrepreneurs most often use is a personal visit to the inspector. The tax return under the simplified tax system is submitted to the reporting office. As a sign of confirmation of acceptance of the declaration according to the simplified tax system, the inspector puts a mark on its acceptance and the date.

Responsibility for late submission of the declaration

Penalties for late submission of the report include:

- if the tax is paid - 1 thousand rubles;

- if the tax has not been paid - 5% of the amount of tax payable on the basis of this declaration, for each full or partial month from the day established for its submission, but not more than 30% of the specified amount and not less than 1 thousand rubles. (Article 119 of the Tax Code of the Russian Federation).

The fine can be reduced if there are mitigating circumstances (Article 112 of the Tax Code of the Russian Federation, information from the Federal Tax Service). But, unfortunately, it will not be possible to completely cancel the fine.

For late submission of a report, an official of the organization - the person responsible for the untimely submission of reports - may be held accountable. Most often this is the chief accountant or individual entrepreneur (or director of the company). The official may be given a warning or a fine in the amount of 300 to 500 rubles. (Article 15.5, Part 3 of Article 23.1 of the Code of Administrative Offenses of the Russian Federation).

If the period of delay exceeds 10 working days, tax authorities have the right to block the company’s current account (Clause 2 of Article 76 of the Tax Code of the Russian Federation).

You can learn more about reporting based on the results of 2021 in the “Employer reporting” section.

Completing section 3 is a report on targeted revenues with codes for subsidies and contributions

This section displays target revenues and their expenditure in the past calendar year (contributions from members of the partnership, subsidies for major repairs):

- in column 1 indicate codes 112 for subsidies and 120 for contributions for property maintenance;

- column 2/5 is not filled out in accordance with the letter of the Federal Tax Service of Russia dated January 20, 2015 No. GD-4-3/2700;

- in column 3/6 indicate the annual amount of target receipts and their balance in the current account of the partnership;

- Column 4/7 reflects the annual amount of expenses of these funds and the unused balance, which must be included in non-operating income when calculating the tax base.

For example, this section might look like this:

| 1 | 2/5 | 3/6 | 4/7 |

| 112 | —————————— | 500000 | 500000 |

| —————————— | —————————— | —————————— |

Let's sum it up

- The declaration under the simplified tax system “income-expenses” for 2021 is submitted: by 03/31/2020 - by organizations and by 04/30/2020 - by individual entrepreneurs.

- The simplifier for the “income minus expenses” object fills out only the title page, sections 1.2 and 2.2.

- Section 3 is completed if assets were received as part of charity or targeted financing during the tax period.

- For late submission of a declaration, an individual entrepreneur or organization may be held liable in the form of a fine.

If you find an error, please select a piece of text and press Ctrl+Enter.

Title page

The title page of the declaration is filled out by taxpayers, except for the section “To be filled out by a tax authority employee .

When filling out the “Adjustment number” field, “0” is automatically entered in the primary declaration for the tax period; in the updated declaration for the corresponding tax period, the adjustment number must be indicated (for example, “1”, “2”, etc.).

“Tax period (code)” field is filled in in accordance with the codes given in the directory. If the declaration is submitted for the tax period, then code “34” is indicated - calendar year; if the declaration is submitted for the last tax period during the reorganization (liquidation) of the organization (upon termination of activities as an individual entrepreneur), the code “50” is selected in the specified field, etc.

When filling out the “Reporting year” , the year for the tax period for which the declaration is submitted is automatically indicated.

When filling out the line “Submitted to the tax authority (code)”, indicate the code of the tax authority to which the declaration is submitted, according to the certificate of registration with the tax authority. By default, the program enters the tax authority code specified in the payer’s registration card. You can find out the code of your tax authority using the electronic service of the Federal Tax Service “Address and payment details of your inspection” (https://nalog.ru, section “All services”).

In the “By location (accounting) (code)” , select a code, the list of which is given in the drop-down list. If the declaration is submitted by an individual entrepreneur at the place of residence, then code “120” is selected; if the declaration is submitted at the location of the Russian organization, then code “210” is selected. If the declaration is submitted by a legal successor who is not the largest taxpayer, then code “215” is indicated.

When filling out the “Taxpayer” , the full (without abbreviations) name of the organization is reflected, corresponding to that indicated in the constituent documents or the last name, first name, patronymic of an individual entrepreneur. By default, this detail is filled in in the program in accordance with the name (full name) specified in the taxpayer’s registration card.

The field “Code of the type of economic activity according to the OKVED classifier” is filled in automatically (if the client is already registered in the system), or is selected from the classifier. These codes are determined by organizations and individual entrepreneurs independently and are contained in extracts from the Unified State Register of Legal Entities and the Unified State Register of Individual Entrepreneurs. You can also find out your OKVED code using the electronic service of the Federal Tax Service “Obtaining an extract from the Unified State Register of Legal Entities / Unified State Register of Individual Entrepreneurs via the Internet” (https://nalog.ru, section “All services”).

Attention! The fields “Form of reorganization (liquidation) (code)” and “TIN/KPP of the reorganized organization” are filled in only by those organizations that are reorganized or liquidated during the tax period.

“Contact telephone number” field automatically reflects the taxpayer’s telephone number specified during registration.

When filling out the field “On ____ pages”, indicate the number of pages on which the declaration is drawn up. The field value is filled in automatically and recalculated when the composition of the declaration changes (adding/deleting sections).

The field “with supporting documents or their copies on ___ sheets” reflects the number of sheets of supporting documents and (or) their copies (if any). Such documents may be: the original (or a certified copy) of a power of attorney confirming the authority of the taxpayer’s representative (if the declaration is submitted by the taxpayer’s representative), etc.

In the section of the title page “I confirm the accuracy and completeness of the information:” the following is indicated:

1 - if the document is submitted by the taxpayer,

2 - if the document is presented by a legal or authorized representative of the taxpayer. In this case, the name of the representative and the document confirming his authority are indicated.

Also on the title page, in the “I confirm the accuracy and completeness of the information” field, the date is automatically indicated.

Declaration form and submission deadlines

The figure below shows the minimum set of necessary information about the current declaration form under the simplified tax system and the deadlines for reporting dates for individual entrepreneurs and companies:

The above deadlines for submitting a declaration under the simplified tax system must be observed by those taxpayers who continue to apply the simplified taxation system as usual. For those companies and individual entrepreneurs that have lost the right to use this special regime, the deadline for filing a declaration is different (clauses 2 and 3 of Article 346.23 of the Tax Code of the Russian Federation).

Since 2021, increased limits of the simplified tax system have been introduced, at which increased tax rates are applied, allowing taxpayers to continue to apply the simplified tax system when exceeding standard limits.

ConsultantPlus experts spoke in more detail about the innovations. Get free demo access to K+ and go to the Ready Solution to find out all the details of the changes.