Author: Ivan Ivanov

Keeping a book of material assets is not difficult. But since this procedure is provided for the purpose of monitoring the receipt of materials at the enterprise and their issuance, it plays a particularly important role. The person responsible for the arrival and disposal of inventory items must be extremely attentive to his responsibility for documenting the transactions performed.

Since 2015, a new form of register of material assets has been introduced at the enterprise, and therefore some rules for filling out and maintaining primary documentation have changed. Due to the high importance and maximum responsibility for the imputed organizational property, storekeepers and other materially responsible persons must be aware of the changes that have occurred and the rules for documenting material flows.

How to organize inventory accounting

If the institution does not have a lot of material assets, then it is enough to reflect their receipt in accounting and further write-off when worn out.

use, transfer. That is, it is not necessary to fill out a warehouse journal; Keeping records of material assets is justified if the enterprise has a large stock of material assets, and their use implies movement between structural divisions. This approach makes it possible to ensure appropriate control over the safety and intended use of the enterprise’s property. The head of the organization must appoint a responsible employee who will record entries in the journal.

Typically, these responsibilities are assigned to the storekeeper or another materially responsible person, for example, a warehouse manager or a housekeeping manager.

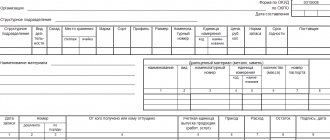

IN THE DIVISION

______________________________________________________

(division (workshop))

______________________________________________________

(military unit (formation, warehouse, base))

Started "__" _____________ 19__

Finished “__” ___________ 19__

Name of materials Pages of the book Name of materials Pages of the book

initial subsequent initial subsequent

Form 26

(Left and right sides)

__________________________________________________________________

(type of material resources)

Recording date Document name N and document date Supplier (recipient) Name of material assets and their category

Item code

Unit

when there was a hundred and t when there was a hundred and t when there was a s o s t o i t a r i v e r . when there was a hundred and so on

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31

EXPLANATIONS FOR FORM 26

1. The book is intended to record the presence and movement of weapons, equipment, ammunition, fuel, food, various property, equipment, tools and other material assets.

A separate book is kept to record toxic and potent substances.

2. The book is kept in the unit, workshop and other military (ship) facilities.

3. A personal account is assigned to each name and category of material assets in the book. The grouping of personal accounts on the sheet is carried out taking into account the movement of individual items of material assets and their list according to the product classifier.

4. Transactions related to the receipt and expenditure of material resources are reflected in the book on a daily basis.

5. Accounting for equipment and tools in the repair department (workshop) is kept in the workshop book. At the same time, for each workshop, depending on the number of items of material assets taken into account, the required number of pages is allocated.

6. Data entries in the columns of the “Consists” requisite are made only for those material assets through which there was movement.

7. Notes on reconciliation of credentials are recorded in the next line. In this case, the following is written down: in column 1 - the date of reconciliation, in column 2 - “Reconciled”, in the columns of the “Consists” details - the balance of material assets on the day of reconciliation. The persons who carried out the reconciliation sign in column 4.

Similar works:

“Test work No. 1 option 1 No. 1 Translate 500 bytes = bit 5 KB = MB 87 GB = byte 7 MB = bit 46 bytes = MB 700000 bits = KB No. 2 How much information does a message contain, occupying three pages of 25 lines , each line contains 80 characters of a 32-character alphabet? No. 3 Message,..."

“List of TSO MBOU Neklinovskaya evening school as of 02/01/2017 Section I “Computers” Name Year of commissioning Brief description with year of commissioning (if replaced) Inventory number Condition Quantity, pcs. Computer assembly 2010 1360196-1360221, 1360223, 13602...”

“Philosophical anthropology, its place in the system of knowledge about man. Philosophical anthropology, its place in the system of knowledge about man.• Philosophical anthropology is one of the influential areas of social thought of the 20th century. Worldozz..."

“The child is constantly developing, and every development process (in addition to slow, gradual changes) is characterized by abrupt transitions - crises. They are necessary; they are the driving force of development. During a crisis, a change occurs not only in the mental, but ... "

“Plan of an open lesson on industrial training for professional training of drivers of vehicles of category “B”, master of industrial training, Kalyuzhny Evgeniy Sergeevich Topic of the program: Training in practical driving in real traffic conditions. Topic of the lesson: Driving along the route...”

“Talnivka backlighting school of І-ІІ stages No. 3 Lesson on the topic: Differentiation of sounds - the letters D-T in writing Prepared by teacher-speech therapist Podlisetska L.V. 2014 river Differentiation of sounds - the letters D-T in the letter Meta: learn to differentiate sounds - how ... "

“Appendix to the decision of the Assembly of Deputies of the Kopeisk City District of the Chelyabinsk Region dated May 25, 2016 No. 148 List of movable property transferred free of charge from state property of the Chelyabinsk Region to municipal property...”

"GBPOU Oktyabrsky Petroleum College named after. S.I. Kuvykina Methodological development of the event “New Year’s Carnival” Developed by: teacher of hostel No. 2 L.R. Guzey, Oktyabrsky 2014

Document form: which one to use

To record the movement of inventory items, use a special journal for the issue of material assets; you can develop a sample yourself. This right is enshrined in Law No. 402-FZ. Or use the unified forms approved by Resolution of the State Statistics Committee of the Russian Federation dated 08/09/1999 No. 66.

For example, to reflect receipts of inventory items, you can use form MX-5 (OKUD 0335005).

To reflect the consumption of material assets, a different form is used - MX-6 (OKUD 0335006).

In military units where strict records of ammunition, weapons and equipment are kept, a special form is used: material inventory log form 26.

Based on these unified forms, the institution has the right to independently develop a form that will meet all the specific features of its activities. Such a form should be approved in the accounting policy or in a separate local order.

Results

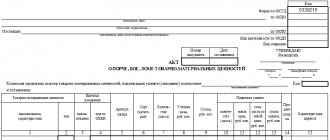

Form INV-26 is a document that can be used both to reflect the results of a single inventory and to record the results of all audits carried out by the company during the year.

One of the main goals of inventory is to identify surpluses or shortages of certain values.

Form INV-26 is one of the most convenient tools for solving this problem, since its structure provides fields for indicating all the key parameters for accounting for surpluses, shortages or damaged property of the company. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

How to Journal

Maintaining an accounting register has its own characteristics:

- Only the responsible employee can make entries in the document.

- All property of an enterprise is subject to registration, regardless of quantitative, qualitative and cost characteristics.

- The responsible employee issues valuables to employees and/or financially responsible persons against signature.

- Upon receipt or disposal of inventory items, information is reflected in the accounting register on the same day.

- The final journal data for a specific date must match the actual availability of inventory items.

Book of accounting of availability and movement of material assets form 26

cop. 1 2 3 4 5 6 7 8 1 03/24/2011

Oleshko P.V.

Set of winter tires PIRELLI Winter 190 Snowsport 205/60R15 91T, N XP 3/9

PC. 5 3300-00 16 500-00 2 03/25/2011

Koretskaya P.S.

166 Steel Radial 82S Tubeless 168Я502311, N ХР 3/10

PC. 5 2000-00 10 000-00 3 04/11/2011

Semenov S.S.

Set of winter tires KUMHO KW22 225/50R17 98T, N XP 3/1

PC. 4 5000-00 20 000-00 4 04/19/2011

Zelentsova O.K.

Set of winter tires N OKIAN HAKKAPELIITTA CQ 205/65R15 102/100Q, N XP 3/5

PC. 4 3800-00 15 200-00 5 04/20/2011

Rzhavko O.Kh.

Set of winter tires MICHELIN X-ICE X12 225/60R18 100T, N XP 2/5

PC. 5 8000-00 40 000-00 6 04/20/2011

Smith A.

Set of winter tires GOODYEAR ULTRA GRIP 500 245/65R17 107T, N XP 3/6

PC. 4 7700-00 30 800-00 — — — — — — — — — — — — — — — — —

Total

27 X 132 500-00

Using this sample, print even pages of the magazine according to form N MX-2

Place of storage, name, address, telephone number Document on acceptance of inventory items Inventory items accepted for storage returned received by the depositor. There are no claims regarding the quantity and quality of inventory items date financially responsible person return document financially responsible person number date signature last name, first name, patronymic number date signature last name, first name, patronymic date signature last name, first name, patronymic 9 10 11 12 13 14 15 16 17 18 19 20 21

Rack No. 3, cell 9

1 24.03.2011 24.03.2011

Savin K.H.

67 24.10.2011

Gorbukhin O.I.

24.10.2011

Oleshko P.V.

Rack No. 3, cell 10

2 25.03.2011 25.03.2011

Savin K.H.

68 25.10.2011

Gorbukhin O.I.

25.10.2011

Koretskaya P.S.

Rack No. 3, cell 1

3 11.04.2011 11.04.2011

Gorbukhin O.I.

71 11.11.2011

Savin K.H.

11.11.2011

Semenov S.S.

Rack No. 3, cell 5

4 19.04.2011 19.04.2011

Savin K.H.

72 19.11.2011

Gorbukhin O.I.

19.11.2011

Zelentsova O.K.

Rack No. 2, cell 5

5 20.04.2011 20.04.2011

Gorbukhin O.I.

69 28.10.2011

Savin K.H.

28.11.2011

Rzhavko O.Kh.

Rack No. 3, cell 6

6 20.04.2011 20.04.2011

Gorbukhin O.I.

70 10.11.2011

Savin K.H.

10.11.2011

Smith A.

etc.

Using this sample, print odd-numbered pages of the journal according to form N MX-2

How to fill

The material assets accounting journal (filling sample) is no different in structure from ordinary accounting registers. It consists of a title page and pages arranged in the form of a table.

The title page is filled out once - when creating a document. The following information is provided here:

- name of the institution and name of the structural unit;

- the period for which entries are made (month, quarter, year, depending on the number of transactions);

- information about the position and full name is indicated. employee responsible for maintaining the register.

It is acceptable to provide additional information. For example, type of activity according to OKVED, TIN, OKPO, KPP and other registration data.

The tabular part of the document is filled with data on the movement of inventory items:

- The number is entered in order.

- Then enter the date of the transaction.

- The data of the primary document on the basis of which the entry is made is indicated. For example, when receiving goods and materials, indicate the number and date of the invoice. Upon disposal - the number and date of the act for write-off, transfer.

- Specify the recipient. If this is an employee of the institution, then write down the position and full name, if it is a third-party company, then indicate the name of the company.

- Register the name of the inventory, unit of measurement and cost for the product, then indicate the quantity and amount based on the quantity issued (received).

You can download the completed wealth register for free.

Regulatory acts

The requirement established by Article 9 of the Federal Law “On Accounting” is that all business transactions carried out at the enterprise must be documented with supporting documentation, i.e.

primary documents used for accounting purposes has been cancelled. However, organizations continue to follow it due to the requirements of other regulations. If a business transaction is not documented in a primary accounting document, it is not accepted for accounting and is not reflected in the accounting registers. Primary documentation is compiled on strict forms included in albums of unified primary accounting forms.

Decree of the Government of the Russian Federation No. 835 “On primary accounting documents” requires the use of developed and approved forms of primary documents by all companies, regardless of their legal form.