What is included in daily travel expenses

When a worker is sent on a business trip, he retains his full salary, and the employer also compensates his employee for expenses incurred during the departure.

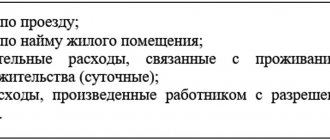

The concept of “per diem” implies reimbursement of the following production costs:

- accommodation in another city with rental of residential premises (apartments, hostel rooms);

- purchase of food or expenses for food in a cafe, canteen, restaurant;

- use of public transport, both ground and airplane;

- attending work-related events.

- other expenses necessary to fulfill the tasks set by the manager.

In practice, determining the daily allowance rate for a business trip is problematic: the employer finds it difficult to determine the needs of a subordinate and calculate the amount necessary for living.

Daily allowance limit for business trips in 2021

There are no government regulations regulating the amount of payments upon departure on behalf of management.

The head of the enterprise has the right to independently establish the procedure for receiving and calculating daily allowance for a business trip. When determining the amount of payments, the company is guided by the Tax Code, which regulates the maximum allowable amount of daily allowance for calculating personal income tax and insurance premiums.

Important! The Tax Code (paragraph 12, paragraph 3, article 217) defines the maximum allowable amount of daily allowance that is not subject to personal income tax - this is 700 rubles for business trips in Russia, and 2,500 rubles for trips abroad. When an organization allocates a larger amount, the employer is obliged to withhold personal income tax from the employee.

According to the Decree of the Government of the Russian Federation No. 729 of October 2, 2002, the minimum amount of daily allowance for both private and budget organizations should not be less than 100 rubles.

Article 217 of the Tax Code of the Russian Federation “Income not subject to taxation (exempt from taxation)”

Decree of the Government of the Russian Federation dated October 2, 2002 No. 729 “On the amount of reimbursement of expenses associated with business trips on the territory of the Russian Federation to employees who have entered into an employment contract to work in federal government bodies, employees of state extra-budgetary funds of the Russian Federation, federal government institutions”

Read also: Transfer from temporary to permanent work

What does the employer care about?

It is not worth violating the requirements of labor legislation regarding the payment of daily allowances, as this can lead to administrative and financial liability.

So, according to paragraph 1 of Article 5.27. Code of the Russian Federation on Administrative Offences, adopted by the State Duma on December 20, 2001, violation of labor legislation is fraught with a warning or a fine imposed on an official of the organization in the amount of 1-5 thousand rubles. The same measure is provided for individual entrepreneurs without forming a legal entity. As for legal entities, in their case the fine varies from 30,000 to 50,000 rubles.

If we are talking about a repeated violation, then in this case the official faces a fine of 10,000 to 20,000 rubles or disqualification for a period of 1 to 3 years. For individual entrepreneurs, the amount of the administrative fine will rise to 10,000-20,000 rubles, for legal entities - 50,000-70,000 rubles.

Sometimes an enterprise pays per diem even when an employee is sent on a business trip to a place from which it is possible to return every day. If this happens, then during the next inspection the employer may be required to charge insurance premiums and personal income tax on the amount of daily allowance.

Procedure for paying daily allowances to employees

After the employer determines what amount of daily allowance for a business trip the employee is entitled to, the relevant documentation is completed.

General procedure for reimbursement of travel expenses:

- informing the employee about the provision of a limit and the need to document costs;

- sending an employee on a trip;

- upon returning to the workplace, the employee must provide management with evidence of expenses in the form of receipts and tickets;

- the amount of daily allowance for a business trip is calculated (the number of days spent away from the main workplace is multiplied by the established limit);

- the employee receives compensation for expenses along with his salary.

Important! Depending on the organization, the procedure for receiving daily allowance varies: timing and amount of payments, documentation requirements.

The organization’s responsibilities include reimbursing employees in accordance with Article 168 of the Labor Code of the Russian Federation, not only for each day of travel, but also for weekends and holidays. Employees are compensated for their travel time, including unforeseen stops.

Article 168 of the Labor Code of the Russian Federation “Reimbursement of expenses related to business trips”

What is an employee's business trip?

A business trip is the fulfillment by an employee of the employer’s instructions outside the place of permanent work (Article 166 of the Labor Code of the Russian Federation).

If an employee is sent to a division of the same organization located separately, then this also applies to business trips. When a remote worker goes to the employer’s office located in another city, this is also a business trip.

But if travel is an integral part of the employee’s functional duties (the traveling nature of the work), then they are not considered business trips.

The Labor Code of the Russian Federation does not contain an unambiguous definition of the traveling nature of work. Rostrud recommends that work be considered traveling if the trips are of a “permanent nature” (letter dated December 12, 2013 No. 4209-TZ). Therefore, employers themselves determine which category each position belongs to. The main thing is that the nature of the work must be reflected in the employment contract (Article 57 of the Labor Code of the Russian Federation).

An individual entrepreneur cannot send “himself” on a business trip, because is not an employee (letter of the Ministry of Finance of the Russian Federation No. 03-11-11/11722 dated February 26, 2018).

Daily allowance for business trips

According to Article 167 of the Labor Code of the Russian Federation, the procedure for paying cash expenses on a business trip is regulated by a collective agreement.

Most often, the document is presented in the form of an order of the same name. Most businesses do not exceed the limit established in the Tax Code, although this is not a violation of the law. The employer retains the right to either reduce or increase the amount of cash payments.

Article 167 of the Labor Code of the Russian Federation “Guarantees when sending employees on business trips”

Daily allowance for business trips in Russia

The minimum amount is not established; the maximum often does not exceed 700 rubles. The procedure and amount of payments must be found out at the place of work in the regulations on business trips.

Daily allowance for business trips abroad

The amount of monetary compensation for trips to foreign countries is regulated by the internal regulations of the organization.

In addition to the main provisions, the payment of daily allowance on a business trip varies taking into account Resolution No. 812, which reflects the amount of payments depending on the location of the employee. In private organizations this document may not be taken into account; in budget companies it is mandatory.

Decree of the Government of the Russian Federation dated December 26, 2005 No. 812 “On the amount and procedure for payment of daily allowances in foreign currency and allowances to daily allowances in foreign currency during business trips on the territory of foreign states to employees who have entered into an employment contract to work in federal government bodies, employees of state extra-budgetary funds of the Russian Federation, federal government agencies"

To CIS countries

When an employee is sent on a business trip to one of the CIS countries, the head of the company, when calculating daily allowances, must rely on the provisions for trips abroad.

Important! When crossing the country's border, stamps are not affixed to the international passport. This feature is regulated by Customs legislation.

The employee retains travel tickets as documents confirming his stay on a business trip abroad.

Read also: Compensation for renting housing to an employee

Trip at the expense of the host party

According to the norms, daily allowances for business trips for the 2019-1010 year are paid by the employer sending the employee on the trip.

Payment by the host party is possible upon preliminary conclusion of a written agreement, which stipulates the organization paying for the employee’s stay on a business trip. In budgetary organizations, the limit is limited: the amount of daily allowance should not exceed the norms specified in the legislation.

Two trips in one day

If it is necessary to send an employee several times a day to different places, you must rely on the Business Travel Regulations. The amount of daily allowance will depend on the place of arrival.

For two trips in one day, the employer retains the right to establish other payments to the employee as compensation for expenses.

In case of early termination of the trip

When an employee returns from a business trip ahead of schedule, the company issues an advance report indicating the date of arrival.

After receiving the report, specialists in the economic department of the organization recalculate the daily allowance. Excess funds are returned to the company's budget.

Work on weekends

When an employee is on a business trip, daily allowances are paid for each calendar day, regardless of whether he was working or had a day off.

Important! The right to receive daily allowances on weekends and holidays is reflected in clause 11 of Decree of the Government of the Russian Federation No. 749 of October 13, 2009.

Decree of the Government of the Russian Federation dated October 13, 2008 No. 749 “On the specifics of sending employees on business trips” (together with the “Regulation on the specifics of sending employees on business trips”

Daily allowance for one-day business trips

There is no minimum duration of a business trip. The employer has the right to send an employee for one day. In this case, documenting a multi-day business trip is impossible, and in accordance with the law, daily allowances for one-day business trips are not required. Depending on the organization, compensation for monetary costs may be possible.

Payments for one-day business trips instead of daily allowances

At the discretion of the manager, the employee receives compensation in the amount of 50% of the generally established amount when traveling abroad. A one-day business trip within the territory of Russia is not paid if the organization has not reimbursed the expenditure of funds on a voluntary basis.

Personal income tax on daily allowances for one-day business trips

Each situation with the taxation of daily allowances for business trips for one day is considered individually.

According to the Ministry of Finance of the Russian Federation, only those expenses that have documentary evidence are not subject to personal income tax. Daily allowances that do not exceed the limit of 700 rubles in Russia and 2,500 rubles when traveling abroad are exempt from tax.

According to the Supreme Arbitration Court of the Russian Federation, the definition of “daily allowance” is not applicable to one-day business trips, therefore cash should be recognized as one of the forms of compensation for expenses related to official activities. Therefore, expenses made with the permission of management are not employee income and therefore cannot be subject to personal income tax.

Documentation of a business trip

To send an employee on a business trip, one document is enough - an order from the employer. It can be issued in the recommended form T-9 or T-9a (Resolution of the State Statistics Committee of the Russian Federation dated January 5, 2004 No. 1). Option T-9a is used if it is necessary to send several employees at once.

Upon returning from a trip, the employee must report in Form AO-1 within three days. All documents confirming expenses must be attached to the report: tickets, hotel bills, cash receipts, etc.

Forms such as travel certificate (T-10) and duty assignment (T-10a) are not mandatory since 2015. But many employers still issue them, because... this allows for better control over employees.

In particular, it is not always possible to confirm the travel time based on tickets - for example, if the employee drove his own car. In this case, the T-10 form with the receiving party’s notes on arrival and departure will help.

Sometimes it is necessary to complete some additional documents. For example, it is possible that an employee traveling will have to work on a day off. Then you need to issue an appropriate order in advance and obtain the employee’s consent.

How to calculate business trip days for which you need to pay daily allowance

Regardless of the time of departure of the employee on official business, this day is considered a full day.

When an employee returns after 12 o’clock at night, the employer does not have the right to demand that he appear in the office in the morning of the same day: the person is documented to continue to be on a business trip. Read also: Payroll fund

To calculate daily allowances, an accountant in an organization studies transport tickets and the time of arrival and departure, after which he records the exact number of days of stay on a business trip, draws up a report and determines the amount of compensation. The calculation is made by multiplying the number of days by the daily allowance limit established by management.

How to prepare an advance report?

When returning from a business trip to the accounting department within 3 days, you must fill out a cost report on a special form and confirm it with documentation.

Important! Filling out the report is the responsibility of the employee returning from a business trip.

Sample of filling out an advance report

As documentation reflecting travel expenses, the employee provides documents such as receipts, bills or rental agreements, transport tickets, receipts for taxi rides, or gasoline purchases.

Reflection of an employee’s business trip in accounting

To account for travel expenses, account 71 “Settlements with accountable persons” is used.

Before leaving, the employee is given an advance in an amount approximately equal to the expected expenses:

DT 71 – KT 50 (51)

After return, expenses are taken into account on the basis of the advance report and attached documents:

DT 20 (23, 26, 44...) – KT 71

The specific corresponding account depends on the employee’s position and the purpose of the trip.

If expenses were incurred with allocated VAT, then you need to take into account the deduction for this tax:

DT 19 – KT 71

DT 68.2 – KT 19

In this case, the amount excluding VAT is written off to expense accounts.

After calculating the full amount of costs and comparing it with the advance payment, two options are possible:

- The employee returns the unused portion of the advance:

DT 50 (51) – KT 71

- The organization reimburses the employee for overexpenses:

DT 71 – KT 50 (51)

If personal income tax and insurance contributions were assessed on any travel payments, then at the end of the month the following postings will also appear:

DT 70 - CT 68.1 - personal income tax withheld

DT 20 (23,26,44...) – CT 69 – insurance premiums have been charged.

Order

To apply for daily allowance, an organization issues an order, which displays the serial number of the document, the details of the enterprise, and the date. The order must include information about the employee, the purpose and duration of his stay on a business trip, and the source of funding.

Form No. T-9 and T-9a are used as a form for filling out the document.

Form T-9

Form T-9a