Form INV-5 is an inventory list of goods accepted for safekeeping in warehouse premises. It is an important primary reporting document, confirmation of the delivery and receipt of material resources. The form is convenient in that it can be used to immediately compare data on the actual availability of inventory items in the warehouse and information regarding this availability in accounting.

- Form and sample

- Free download

- Online viewing

- Expert tested

FILES

Inventory: administrative documents

Before conducting a general inventory of an enterprise’s property or an inventory of property transferred for safekeeping to a specific person, an order is issued for the enterprise, which prescribes and assigns:

- conducting an inventory indicating the date on which the inspection of property and financial assets is carried out;

- the composition includes at least 3 people, the chairman and members of the commission;

- indicating the start date of the inspection and the exact date of its completion;

After signing the order, financially responsible persons, members of the commission and the official appointed to monitor its implementation must be familiarized with it. Based on this document, the financially responsible person is obliged to provide members of the commission with access to goods and materials stored in entrusted storage and accounting documentation for them.

Characteristics

A characteristic feature of filling out these types of forms is that for their correctness and further legal force, it is necessary to form a special commission. It must consist of at least three people, in addition to the main person financially responsible for warehousing of inventory items.

A chairman must be elected in the commission, the remaining representatives are appointed by members of the commission. The entire document is based on a listing of the facts established by the commission.

Who exactly will fill out the form is not particularly important. Moreover, all members of the commission must sign their signature, even if they do not agree with the results of its conduct. In addition to signatures, in this case they simply make a note stating that it is in the final indicators that they are not satisfied or do not correspond to the facts they have established.

It is important to know that not all fields need to be completed by the end of the inventory process. Some of them are deliberately left blank, since the INV-5 form, after filling out, goes to the accounting department and the rest of the necessary data is entered into it there.

INV-5: document structure

The INV-5 form approved by Goskomstat is presented in four main elements:

- title part company installation data

- information on the order to carry out an inventory

- confirms the removal of balances and their actual availability in accordance with accounting at the time of the start of the inventory;

- table for entering data on inventory items and their movement;

- conclusions and additional information of the commission;

Components of the form

The inventory has several pages. The first is introductory, it contains a part with a receipt, the second and subsequent elements are presented in the form of a table. At the conclusion, the signatures of the responsible persons are affixed.

First part of the form

Fundamentally important points are indicated at the beginning. In the form of a small table on the far right side of the sheet, the form numbers according to OKUD, OKPO, the code of the type of activity of the organization, the document number and the date of its preparation, two dates: the beginning and end of the inventory are listed (even if it was carried out on one day, indicating both identical ones is mandatory), type of transaction performed and accounting account number. The last two columns are filled in by the accountant after the signatures of the commission members and consideration by the manager.

Also, separate lines are left for the full name of the organization (abbreviations to LLC, OJSC, individual entrepreneur, etc.) and the name of the division are acceptable. The latter, in the vast majority of cases, is a warehouse under some serial number, since the INV-5 form is the most common in warehouse policy.

Important point! At the top, the basis for the inventory must be indicated. This may be an order, notification or order from the head of the company as a whole or its division.

In any case, the inventory process must be carried out under the guidance and knowledge of the persons concerned. This fact must have documentary evidence.

Part with receipt

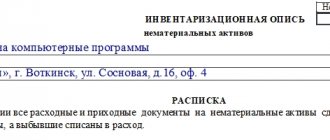

On the first sheet of the document there is a receipt from the financially responsible person stating that by the time the inventory began, all the primary reporting documents necessary for this had been submitted to the accounting department, and goods and materials (inventory assets) had been capitalized and accepted for safekeeping.

Also, at the beginning of the verification process, all material resources written off from accounts must be indicated in the disposal papers. It is undesirable for them to actually be in the warehouse itself to avoid misunderstandings.

The receipt must also indicate the date of its signature and the deadline for removing the remaining material assets.

The second part of the form is tabular

The information is very compactly placed in the table. Using the latter is extremely convenient. The form was formed in the 90s, but still remains relevant. The rows of the table are filled in as the actual availability of inventory items in the warehouse is compared with the data in existing documents. The columns should contain the following information:

- The sequence number of the line.

- Name and OKPO code of the supplier or recipient.

- Nomenclature number of the product, its grade, type or group, full name.

- Storage location (usually the cell or location number is indicated).

- The date when the goods were accepted for responsible warehousing.

- Name, number and date of the document that indicates the receipt of goods and materials at the warehouse (for example, invoice 25 dated August 23, 2019).

- The unit of measurement of the purchased goods and the code of this unit according to OKEI (g, kg, l, pcs., etc.).

- How much inventory material actually exists, total quantity and cost.

- How much goods are available according to currently maintained accounting records.

If the last two columns of the same column are not identical, then this is a defect of the accountant or storekeeper (or other person financially responsible for the product being described). The INV-5 form is convenient precisely because it is possible to illustrate this kind of discrepancy.

Final part

When the inventory is nearing completion, the chairman of the commission and all its members must review the compiled table and put their signatures at the end of the inventory list of inventory items accepted for safekeeping. The signatures will indicate that the availability of goods, their actual quantity and cost have been verified.

Important! Separately at the end, the total amount of all inventory items is indicated in numbers and words.

The financially responsible person puts his signature after all members of the commission as a sign that he has no complaints about their work and agrees with the data provided. The form leaves space for the signatures of two such MOLs, but there may be more. Below the signature of the responsible person is usually the signature of the accountant who verifies the calculations made in the document.

Working with Inventory Lists

Before conducting an audit, members of the commission must thoroughly study the structure of INV-5, a sample for filling out the statement, the principle of acceptance and transfer and accounting for inventory items in safekeeping.

Before the commission begins its work, financially responsible persons must provide the chairman of the commission with a receipt on the availability and safety of goods and materials, which is contained in the header part of the document.

As the audit is carried out, members of the commission fill out a unified inventory form INV-5, the form of which is approved by the State Statistics Committee.

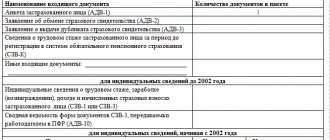

The inventory for each storage item must reflect the following data:

- about the supplier;

- Inventory (name, code);

- date of acceptance and storage location;

- data on documents confirming the turnover and balance of inventory items after their acceptance for storage;

- unit of measurement and actual availability of inventory items in storage;

- information on the quantity and cost of inventory items stored by the responsible person, according to accounting balances.

Filling out the inventory list is carried out by members of the commission, in the presence of the materially responsible person, displaying the actual availability of goods and materials and their monetary value at the time of the inspection, as well as the availability and data of documents on their movement.

Download inventory of inventory items. Form and sample INV-5

Download sample forms for inventory at the enterprise: INV-1 Inventory list INV-1a Inventory list of intangible assets INV-3 Entering data into the inventory list INV-4 Inventory of shipped goods and materials INV-6 Inventory of goods and materials in transit INV-15 Inventory of cash availability INV-17 Inventory of settlements with buyers and suppliersINV-18 Comparison sheet of inventory resultsINV-19 Comparison sheet of inventory items INV-22 Order for inventory INV-26 Accounting for inventory resultsHow is an inventory of materials carried out?

How is inventory carried out?

First, let's look at the question of how companies inventory fixed assets and inventory items. First of all, the corresponding order is issued. A unified form No. INV-22, form according to OKUD 0317018, has been developed for it. It contains the following information:

- name of company;

- structural subdivision;

- composition of the inventory commission;

- list of verified liabilities, property and fixed assets;

- time and place of inventory;

- basis for conducting an inventory.

Both fixed assets and assets owned by the organization, as well as fixed assets that had to be rented, are subject to inventory.

The list is compiled in two copies. The first is for the accounting service to draw up a reconciliation statement (if there are discrepancies with the accounting records). The second is for the financially responsible person (MRP).

IMPORTANT!

When changing the financially responsible person, the inventory is drawn up in triplicate.

Before the start of the procedure, a receipt is taken from the financially responsible person that all documents have been submitted to the accounting department, therefore, accepted for accounting or written off as an expense. It is drawn up on a unified inventory form, at the bottom of the title page. No separate document is needed.

Inventory form for goods and materials

The form “inventory list of inventory items” is a unified document No. INV-3 (form according to OKUD 0317004), approved by Resolution of the State Statistics Committee No. 88. It is necessary during the inventory of materials, goods and finished products. You can take an inventory of inventory items, and then we will tell you step by step how to fill it out correctly. We remind you that the inventory based on the results of the inventory of fixed assets is compiled separately.

Filling out an inventory list of fixed assets

A sample of filling out an inventory list of fixed assets is a unified form No. INV-1. The document for fixed assets is filled out similarly to the example for form No. INV-3. Feel free to use the instructions provided.

Also on our website you can make an inventory of fixed assets.