Every entrepreneur, organization, legal entity that has employees on a contractual basis must pay mandatory insurance premiums for them. Such amounts include payments for pension, medical, and social compulsory insurance. The last type of insurance is a special group, since it is this type of insurance that provides the employee with funds in the event of loss of ability to work, including in the case of maternity. KBK39310202050071000160 was used in 2020 to transfer contributions for social insurance in case of accidents during the production process, as well as the occurrence of occupational diseases. What changes await these payments in 2021?

Payers

Insurance premiums for injuries in 2021 are paid by all employers operating in the Russian Federation:

- Russian organizations and individual entrepreneurs;

- foreign organizations if they involve Russian citizens in their work;

- individuals if they hire persons subject to compulsory accident insurance.

At the same time, Russian organizations pay contributions both in relation to citizens of the Russian Federation and in relation to foreigners. The rules for their calculation are established by Federal Law No. 125-FZ of July 24, 1998.

After registering a new company with the Federal Tax Service, information about this is transmitted to the territorial body of the Social Insurance Fund. From this moment, the newly created organization automatically becomes a payer of contributions and is assigned a registration number. To find out it, as well as determine how much interest to pay to the Social Insurance Fund for injuries in 2021, you need to contact the Social Insurance Fund. You can find out the registration number by requesting an extract from the Unified State Register of Legal Entities from the tax office.

Payment order for contributions in 2018

Insurance premiums (except for injuries) must be transferred to the Federal Tax Service at the place of registration of the business entity. The following fields are filled in the payment order:

- TIN and KPP of the recipient (specific tax office);

- recipient (name of the Federal Treasury body and name of the tax office);

- KBK - the code consists of 20 digits. The first three of them are the code of the chief budget administrator and have the value 182 for the Federal Tax Service.

Contributions “for injuries” must be transferred to the Social Insurance Fund, for which separate BCCs are used.

Rates

The interest rate at which the payer calculates social contributions from accidents at work is set annually depending on the professional risk of the company’s main activities in accordance with Federal Law No. 179-FZ of December 22, 2005. It varies from 0.2 to 8.5%. To find out what the rate of insurance premiums for injuries will be according to OKVED, you need to refer to Order of the Ministry of Labor dated December 30, 2016 No. 851n.

Your main activity must be confirmed annually. To do this, you must provide the FSS with:

- Statement.

- Certificate confirming the main type of activity.

- A copy of the explanation to the financial statements (small businesses do not submit).

If this is not done, the FSS will set the maximum possible rate based on the OKVED codes registered in the Unified State Register of Legal Entities for the organization.

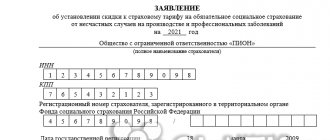

See application and certificate samples at the end of the article.

KBK: how many signs and what do they mean?

Based on Order of the Ministry of Finance No. 65n, the budget classification code consists of 20 digits. Conventionally, they can be divided into several groups consisting of 1-5 characters:

No. 1-3 – code indicating the addressee for whom the cash receipts are intended (territorial Federal Tax Service, insurance and pension funds). For example, for payment of BCC for personal income tax in 2017, the number “182” is entered, for contributions to the Pension Fund – “392”. No. 4 – show a group of cash receipts. No. 5-6 – reflects the tax code. For example, for insurance premiums the value “02” is indicated, excise taxes and insurance premiums are characterized by the number “03”, payment of state duty is “08”. No. 7-11 - elements revealing the item and subitem of income. No. 12 and 13 - reflect the level of the budget into which funds are planned to flow. The federal code is “01”, the regional code is “02”. Municipal institutions are assigned the numbers “03”, “04” or “05”. The remaining figures characterize budget and insurance funds. No. 14-17 – indicate the reason for the financial transaction:

- making the main payment – “1000”;

- accrual of penalties – “2100”;

- payment of a fine – “3000”;

- interest deduction – “2200”.

No. 18 – 20 – reflects the category of income received by the government department. For example, funds intended to pay tax are reflected with the code “110”, and gratuitous receipts – “150”.

Example . makes contributions to insurance against accidents and occupational diseases that may occur during the performance of work duties. Depending on the situation, the BCC indicated in the payment document may differ:

– 393 1 0200 160 – upon timely transfer of funds; – 393 1 0200 160 – in case of payment of penalties; – 393 1 0200 160 – payment of a mandatory fine.

Accrual procedure and reporting

Contributions for insurance against industrial accidents and occupational diseases are calculated monthly on the last date using the formula:

The calculation base includes all payments to employees accrued under employment contracts. As well as payments under civil and copyright contracts, if under the terms of the contract the customer is obliged to pay them to the Social Insurance Fund. There is no maximum accrual base for contributions for injuries, so they are accrued from all payments during the year.

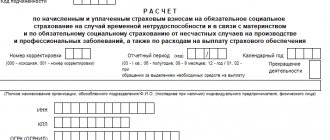

Payers submit a quarterly report 4-FSS to the Social Insurance Fund about the amounts of accruals. The deadlines for delivery are as follows:

- for a paper report - no later than the 20th day of the month following the reporting quarter;

- for electronic - no later than the 25th day of the month following the reporting quarter.

Calculation and payment of insurance premiums from accidents in 2020-2021: nuances

Accrual of “unfortunate” contributions is carried out only by employers. The tariff applied by each of them depends on the main type of activity of the employer (occupational risk class). There are 32 risk classes in total: the lowest is 0.2%, the highest is 8.5%.

For more information on the size of existing tariffs, read the article “Tariffs of contributions for compulsory social insurance against industrial accidents and occupational diseases depend on the type of economic activity .

When calculating, existing benefits, established discounts and tariff surcharges are taken into account.

Payments are calculated monthly (Clause 9, Article 22.1 of the Law “On Compulsory Social Insurance...” dated July 24, 1998 No. 125-FZ), but are carried out on an accrual basis (on the income received by the employee since the beginning of the year). The amount due for payment for the last month is calculated as the difference between the amount accrued on an accrual basis and the amount of payment received for the previous period (also determined on an accrual basis, but including the previous billing month). The final result of the calculation is expressed in rubles and kopecks.

Contributions are calculated separately by separate divisions that independently pay salaries.

The deadline for payment corresponds to the 15th day of the month following the month of accrual of the next amount of contributions, and can be postponed to a later date if it coincides with a weekend (clause 4 of Article 22 of Law No. 125-FZ).

How to issue a payment order

Social contributions are transferred to the Social Insurance Fund monthly no later than the 15th day of the month following the billing month. Bank details of the Social Insurance Fund must be requested from your territorial branch of the Fund.

As for any payment transferred to the budgetary system of the Russian Federation, contributions for injuries are assigned a BCC. The BCC for injuries in 2021 for employees is set to be uniform and does not depend on the rate:

KBC of contributions for injuries: 39310202050071000160.

In addition, when filling out a payment order, you must fill in the fields in a special way.

| Payment order field | Meaning |

| 101 - payer status | 08 |

| 104 - KBK | 39310202050071000160 |

| 106 — 109 | 0 |

| 24 — purpose of payment | In this field you should indicate the type of social contribution, the period for which it is paid, and the registration code of the company in the Social Insurance Fund |

Sample of filling out a payment order to the Social Insurance Fund

KBC for payment of contributions from accidents

The procedure for determining and lists of BCCs for 2020-2021 were approved by the Ministry of Finance.

For 2021 - order No. 99n dated 06/08/2020. Currently, “unfortunate” contributions are paid directly to the Social Insurance Fund. This circumstance predetermines the use of KBK in payments for contributions with the code of the contribution administrator represented by the corresponding state fund: 39310202050071000160, in which the first 3 digits (393) correspond to the FSS code.

To form the KBK, which is used for penalties on contributions from accidents, in the specified code the 14th and 15th digits (under the value 10) must be replaced by 21, that is, in field 104 of the order when paying penalties, KBK 39310202050072100160 is indicated. in fine payments, the value of 10 changes to 30.

“Unfortunate” contributions both for the billing periods 2020-2021 and for previous years should be sent to the details of the territorial social insurance office.

Read more about the FSS details in this material.

The payment for OSS contributions from the Taxpayer and the Pension Fund should be prepared with the Federal Tax Service data at the place of registration of the payer of the contributions and in field 104 indicate the budget classification code corresponding to the payment.

Find the KBK table on insurance premiums paid to the Federal Tax Service here.

ConsultantPlus experts explained which BCCs are used to pay insurance premiums, fines and penalties on them. To do everything correctly, get trial access to the system and go to the Ready solution. It's free.

Liability for non-payment

The following sanctions may be applied to non-payers of personal injury contributions:

- Accrual of penalties and fines.

- Forced collection of arrears.

A penalty is charged in the amount of 1/300 of the Central Bank refinancing rate for each day of delay (Article 26.11 125-FZ). When transferring them, you must indicate the KBC for penalties for injuries in 2021 - 39310202050072100160.

In case of violations in the area of calculating social contributions in the Social Insurance Fund (underestimation of the calculation base), a fine of 20% of the unpaid amount is collected. If the act was committed intentionally, then the fine increases to 40% of the arrears. When transferring a fine to the budget, you must indicate KBK 39310202050073000160.

Statement

Certificate confirming the main type of activity

The KBK was filled out incorrectly. What to do?

Errors made when filling out the BCC in payment orders are not a reason to believe that the payment was not made - this is regulated by Art. 45 of the Tax Code of the Russian Federation. But in practice, everything is more complicated: penalties and fines are often charged for incorrectly filled out budget classification codes.

The reason is as follows: regulatory authorities cannot quickly analyze a financial transaction and reflect the actions on the correct account. During this time, the funds remain unrecorded, and the taxpayer is assigned arrears.

You can correct this situation like this:

- Contact the financial institution with a request to provide written confirmation of the tax remittance within the established time frame. The document must bear a mark from the bank indicating the execution of the order.

- Write an application to clarify the payment. It is recommended to attach a certificate proving the fact of payment and a statement of reconciliation.

Having received all the necessary documentation from the payer who made an error in the KBK , tax officials will check the receipt of funds into the account and correct the situation. The incident can be resolved by submitting an updated declaration with the correct budget classification code. The Tax Code does not require additional documents to be attached, but experts recommend submitting an explanatory note stating:

- declaration filing period;

- inaccurate information that needs correction.

This way the problem will be solved much faster. It is worth remembering that during a desk audit in such cases, Federal Tax Service employees ask for explanations.

Read also

29.12.2016

Features of payment of contributions

Few people know how important it is to correctly set the period in a payment order. According to the KBK, the payment will go through with almost any wording. KBK in this case is the main attribute of payment:

The system records it in the database as successful. But if the accountant entered the reporting period incorrectly, then an overpayment for one calendar month and complete non-payment for another is possible. In this case, the FSS has the right to charge a fine for non-payment.

This practice occurs infrequently; FSS employees create a statement of reconciliation of settlements with the company and analyze the receipt of funds. But it’s better to do it right from the beginning than to prove something later when a request for clarification comes.

It is also worth noting the payment of insurance premiums for rent. It happens that an employee of a company or another individual leases premises or a car to the company. Do I need to pay insurance premiums? No no need. The need to pay contributions arises at the moment when the work or service is performed. In case of rental, the service is not provided. These are property relations. True, you will still have to pay the 13% personal income tax.