If an organization, individual entrepreneur or individual transfers money by mistake using a payment order, if the amount has not yet been posted to the accounts, you can make a refund through a chargeback . To do this, you need to urgently call the bank that serviced this transaction and ask to cancel it.

If there are no more funds in the account, then you can only hope for the law-abiding nature and conscience of the recipient. An application for the return of funds that were transferred erroneously is written in his name

Sometimes it is possible to reach an agreement with a person or the management of an organization, if you act quickly, and they will make a reverse transfer of funds . But more often than not, such a mistake, which is made instantly, requires a lot of time to correct.

In order to return misdirected funds, you will need to spend a lot of time drawing up paperwork and communicating with people who are caught up in this situation. You may have to go to court. If the amount is large, then you should immediately contact an experienced lawyer, and then you can get out of this situation with the least losses.

Return of over-transferred funds

From time to time, situations arise when the recipient learns that there is excess funds in his account.

A company or individual can find out about this from a credit institution by receiving a corresponding notification or using a statement. And also the payer himself, who suddenly discovered an erroneous payment, can inform him about the excess. If the amount was credited to the account of another recipient, then you need to take the following steps:

- Report this to the credit institution.

- Return the funds to your account.

Refund based on payment order

These payment transfers may be carried out with errors:

- Money transferred to the budget.

- Other payments with incorrectly entered details (for example, transfer of funds to the wrong recipient, transfer of a loan).

How can I clarify the payment if there is an error in the payment order for insurance premiums?

There are different stages of refund. In particular, this is the period before and after the irrevocability stage. Let's consider the features of passing this stage:

| Circumstances | Solution |

| The money has not yet arrived in the bank account | The irrevocability stage has not yet passed. This is the most favorable option. If the money has not yet arrived on the account, the payer simply needs to submit an application for a refund. The specifics of the return are specified by Order No. 383-P dated 07/19/12. |

| The irrevocability stage has already passed | The money has already gone through the wrong details. In this case, the person who received the funds will have to be involved to return the money. |

Until the irrevocability stage, the return of payments to the budget and other payments does not differ. The procedure is performed in the same order.

Incorrectly sent money that passes through the treasury budget is returned on the basis of Order No. 125-n dated 12/18/13. How is a refund made? Money with incorrectly specified payments receives the status of funds whose purpose has not been identified. They are returned by the Treasury if these conditions are met:

- It is not clear from the line “Purpose” that the money was sent to the budget.

- The purpose of the payment cannot be determined due to a bank error.

Clause 17 of Order No. 125 specifies other cases of money return. The following mechanism is used:

- The payer sends an application to the treasury.

- The government agency creates a request for a refund.

- Based on the application, the money is returned to the payer within 3 days.

If the irrevocability stage has passed, it is more difficult to return the payment. The funds in this situation have already been transferred. They have already arrived to the recipient. That is, to return you will have to interact with the recipient. It will not be possible to cancel a payment through the banking system; in this case, the return of the payment will partly depend on the will of the recipient.

At the same time, the recipient must remember that he is obliged to return the money by law. The corresponding instruction is contained in Article 1102 of the Civil Code of the Russian Federation. This article states that a person who has received property without any reason must return it. Money transferred by mistake can be classified as unlawfully received property. If the payer refuses, then he can be sued.

The forms of applications for refunds and refund payments are specified in the Appendix to the Letter of the Treasury No. 42-7.4-05/5.3-61 dated February 9, 2009.

Features of filling out a payment form for the return of overpaid amounts

As stated earlier, erroneously paid charges can vary. These may be payments to the budget or other payments. An error is considered to be not only incorrectly specified details, but also incorrectly recorded payment amounts. For example, an organization transferred taxes to the budget. However, the company made an excessive payment. For example, tax was assessed in the amount of 2,000 rubles, and the organization mistakenly paid 3,000 rubles.

The procedure for returning money in this case is specified in Letter of the Ministry of Finance No. 02-14-10A/2275. The return order must contain these details:

- Payment number (field 3).

- Date completed (4).

- Type of payment (5).

- Legal status of the payer (field 101).

- Payout amount in words (6).

- Payment amount in numbers (7).

- TIN and checkpoint of the person who made the decision to return.

- Treasury name.

- The name of the banking institution where the account is opened to record income.

- Bank BIC (11).

- Number of the correspondent account of the subject where the account is opened to record income (12).

- TIN and checkpoint of the recipient of the money (161 and 103).

- Name of the recipient of funds (16).

- Recipient's banking institution, account number, BIC (13, 17 and 14).

- Corresponding account number of the recipient's banking institution (15).

- Type of operation (18).

- Budget code (104).

- Reason for payment (106).

- Purpose of payment (24).

In field 21 you must also indicate the order of payment. Such payments are made in third place.

Options requiring the return of the amount and the consequences of non-refund

The main mistakes associated with the transfer of funds are:

- Selecting the wrong counterparty for whom the payment was intended.

- Incorrect amount specified when generating the document.

- The purpose of the contribution itself contains the details of a document that does not exist in the relationship.

These kinds of mistakes can be noticed by two participants in the relationship. But the payer himself must notify in writing of his consent to carry out operations to return the funds.

The error can be corrected by adjusting the contribution assignment. This can be done if there is a supplier-buyer relationship between the counterparties.

The erroneous amount may be credited towards future payments. Such actions are prohibited unless there are contractual obligations between the companies. All money in this case is subject to mandatory return to the buyer.

This is important to know: Cassation appeal in a civil case: deadlines for filing

Accounting for such contributions is carried out by the seller and the payer according to a typical scenario - a mirror image. It does not matter here why the erroneous payment was made.

Expert opinion

Mikhailov Evgeniy Alexandrovich

Teacher of civil law. Lawyer with 20 years of experience

Since unjustified contributions do not in any way relate to mutual settlements between organizations, value added tax on them is not charged either for payment or refund. But it is worth noting that if payments are made in foreign currency, then exchange rate differences may arise. The party that returns the amount must indicate in the purpose of payment that this is the return of an erroneous contribution. And also indicate the details of the document according to which the buyer asked for a refund.

If a mistake is counted as future payments, then it will be taken into account as a seller-buyer relationship. Then value added tax will also be taken into account here.

What is an assignment

Article 31 of Federal Law No. 395-1 of December 2, 1990 “On Banks” states that credit institutions must carry out money transfer orders. In this case, the rules approved by the Central Bank must be observed. The form is established by Central Bank Rules No. 383-P dated June 19, 2012. The order must contain mandatory information. A list of them is in Appendix 1 to Central Bank Regulation No. 383-P dated June 19, 2012.

The correct indication of all details in the payment order is essential for the correct identification of the payment. Without the details, it is impossible to complete the order. Without them, it is simply not clear to whom to transfer money. If the document contains incorrect details, the funds will be transferred to the wrong place. What to do if such an error occurs? It is necessary to issue a refund for the payment.

What do you need to know about the payment order ?

Posting options for displaying erroneous contributions

The recipient of an unreasonable payment will reflect such receipt of funds using a posting that will be generated at the time the payment document is linked to the accounting accounts.

Such funds belong to account number 76, and it will look like this: Dt76 Kt51 (52).

If you return the money, then the wiring will look like this: Dt51 (52) Kt76. In this case, the difference in exchange rates will be displayed in the following posting: Dt91 Kt76 or Dt76 Kt91.

If you plan to leave the amount as payment for a future product or service, then, based on the payer’s written notification, the posting will look like this: Dt62 Kt76. Be sure to reflect the value added tax wording.

Accounting and tax accounting

Entries are entered into accounting that are completely opposite to those that were used when accepting money for accounting. In particular, these wirings are needed:

- DT51 KT62. Arrival of money.

- DT62 KT51. Refund.

- DT76 KT51. Write-off for refund of erroneous payment.

Let's consider tax accounting for refunds on payment orders:

- USN. The transfer of money is recorded in taxable income. The payment must be reflected on the date of receipt of money on the account. When funds are returned by payment, it is necessary to reverse the income, which is taxed. The reversal is issued on the date of refund.

- BASIC. The crediting and return of money transferred by mistake is an operation that is not recorded in the OSNO.

Important! When accounting and tax accounting, it is important to pay attention to the dates of return/crediting of money. Each operation must be confirmed by the appropriate document.

Errors

Among the possible errors encountered when drawing up a notice of overpaid amounts of money, it is worth highlighting:

- incorrect filling of bank details for return;

- absence of the official seal of the organization (if the letter is not written on company letterhead and signed not by the head, but by another official);

- unreasonable demand (lack of data on payment and amount of overpayment).

If there are such errors, the refusal to refund will be lawful.

Procedure on the part of the recipient of the money

What should a company do if it has received an erroneous payment? She needs to send a notification of the error to the bank within 10 days. The form of notification is not specified by law. It is established by internal acts. If the bank does not have a prescribed form, the notice is drawn up in free form.

Further actions on the part of the banking institution:

- If direct debit is possible, the funds are debited without additional instructions.

- If this option is not available, a debit order will be required from the recipient of the erroneous payment.

Partially, the procedure for returning funds depends on local instructions established for a particular bank.

vozvrat.jpg

Related publications

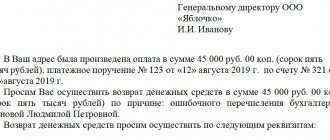

Transactions with non-cash money transfers are carried out through payment orders. The form of the document and the procedure for filling it out are regulated by the regulatory documents of the Bank of Russia (Regulation of the Central Bank of the Russian Federation No. 383-P dated June 19, 2012). When generating a payment order, the correct details of the parties to the transaction, the amount of the transfer, VAT must be highlighted, and the essence of the transaction must be indicated. How the purpose of payment is formed when returning funds to the buyer, we will consider further.

Compilation deadlines

The Civil Code of the Russian Federation does not contain any mention of the maximum time limit for sending an appeal with a demand for the return of unjustifiably received amounts of money. Based on the general statute of limitations, an application to a person who has unjustifiably enriched himself can be filed within three years from the moment the organization learned or should have learned about the excessive payments made.

However, it is considered in good faith to notify the counterparty within a reasonable time after identifying an accounting error. In civil law, this period usually does not exceed 7-10 days.

To whom is it sent and how is it transmitted?

A letter about excessively transferred funds must be sent to the manager, even if it is signed by an accountant or other specialist of the affected organization. No one other than the manager can give orders for the payment of funds to third parties. And it is better for the chief accountant not to take on such responsibility.

The person who has received unjust enrichment may not satisfy the request stated in the document. In this case, the organization sending the letter must take care of evidence that the addressee received the request. Therefore, it is better to send a refund notification:

- through the office or reception of the head, provided that the second copy of the letter is affixed with a company stamp, date and signature of the employee who received the document;

- according to the acceptance certificate, which will indicate the signature of the official who received the letter;

- by a valuable letter with a description of the addition, if the counterparty refuses to independently accept the notice.

If the funds are not returned voluntarily by the counterparty, the refund of overpaid amounts must be made in court.

Cancellation of an outstanding payment

If an erroneous payment was made, but the person realized it in time and, as soon as possible, wrote an application to the bank to cancel the transfer of funds, the bank has the opportunity to cancel the transaction and return the funds to the previous account or send them to the newly specified details.

To do this you need to fill out an application

:

- The appeal itself is submitted to the general director (or other authorized person) of the bank. And the payer’s information is indicated in the header of the application:

- FULL NAME; — residential address; — passport data; - contact phone number.

- Next, the statement itself is written about the request for a refund or cancellation of the erroneously made payment. And, if necessary, new card or account details where the funds should be transferred.

- If desired, you can indicate and provide a payment receipt or any other documents confirming the fact of an erroneous transfer of funds in the attachments.

- At the end there is a date and signature of the applicant.

Document structure

A letter (notice or notification) about excessively transferred funds is drawn up in any form. The legislation of the Russian Federation does not determine the structure of this document. However, in order for the unjustly enriched person to be provided with the most complete information, the text of the letter should indicate:

- business name of the company sending the letter;

- outgoing document number and date of its preparation;

- full name of the addressee (name of the enterprise, address, full name of the manager);

- address to the manager (for example, “Dear Pyotr Petrovich!”);

- actual data (date, time of transfer of funds, payment order number, amount, how much it exceeds the required payments);

- reasons for the overpayment (calculator error, late submission of information to a specialist, etc.);

- a request to return amounts paid in excess of the norm;

- the exact amount of funds to be refunded;

- bank details to make a refund;

- initials and position of the person signing the document.

The letter can indicate legislative acts that establish obligations to return unjustifiably received amounts, as well as notify the counterparty of the negative consequences that will result from ignoring the request for a return.

The return notice may be signed:

- the head of the organization or his deputy (subject to confirmation of his authority);

- chief accountant;

- by any employee of the enterprise, provided that the signature is affixed with the official seal of the company.

To return funds, some organizations (banks, government settlement authorities) ask you to fill out an application using a special form. In this case, the sample or form is issued by the organization itself.

Documents confirming unjust enrichment can be attached to the letter requesting the return of funds, namely:

- money orders;

- bank account statements;

- acts of reconciliation of mutual settlements.

Topic: How to properly return an erroneous payment? and what should I write in the payment instructions?

Quick transition Individual entrepreneurs. Special modes (UTII, simplified tax system, PSN, unified agricultural tax) Up

- Navigation

- Cabinet

- Private messages

- Subscriptions

- Who's on the site

- Search the forum

- Forum home page

- Forum

- Accounting

- General Accounting Accounting and Taxation

- Payroll and personnel records

- Documentation and reporting

- Accounting for securities and foreign exchange transactions

- Foreign economic activity

- Foreign economic activity. Customs Union

- Alcohol: licensing and declaration

- Online cash register, BSO, acquiring and cash transactions

- Industries and special regimes

- Individual entrepreneurs. Special modes (UTII, simplified tax system, PSN, unified agricultural tax)

- Accounting in non-profit organizations and housing sector

- Accounting in construction

- Accounting in tourism

- Budgetary, autonomous and government institutions

- Budget accounting

- Programs for budget accounting

- Banks

- IFRS, GAAP, management accounting

- Legal department

- Legal assistance

- Registration

- Inspection experience

- Enterprise management

- Administration and management at the enterprise

- Outsourcing

- Enterprise automation

- Programs for accounting and tax accounting Info-Accountant

- Other programs

- 1C

- Electronic document management and electronic reporting

- Other tools for automating the work of accountants

- Clerks Guild

- Relationships at work

- Accounting business

- Education

- Labor exchange Looking for a job

- I offer a job

- Club Clerk.Ru

- Friday

- Private investment

- Policy

- Sport. Tourism

- Meetings and congratulations

- Author forums Interviews

- Simple as a moo

- Author's forum Goblin_Gaga Accountant can...

- Gaga's opusnik

- Internet conferences

- To whom do I owe - goodbye to everyone: all about bankruptcy of individuals

- Archive of Internet conferences Internet conferences Exchange of electronic documents and surprises from the Federal Tax Service

- Violation of citizens' rights during employment and dismissal

- New procedure for submitting VAT reports in electronic format

- Preparation of annual financial/accounting statements for 2014

- Everything you wanted to ask the electronic document exchange operator

- How to turn a financial crisis into a window of opportunity?

- VAT: changes in regulatory regulation and their implementation in the 1C: Accounting 8 program

- Ensuring the reliability of the results of inventory activities

- Protection of personal information. Application of ZPK "1C:Enterprise 8.2z"

- Formation of a company's accounting policy: opportunities for convergence with IFRS

- Electronic document management in the service of an accountant

- Time tracking for various remuneration systems in the program “1C: Salary and Personnel Management 8”

- Semi-annual income tax report: we will reveal all the secrets

- Interpersonal relationships in the workplace

- Cloud accounting 1C. Is it worth going to the cloud?

- Bank deposits: how not to lose and win

- Sick leave and other benefits at the expense of the Social Insurance Fund. Procedure for calculation and accrual

- Clerk.Ru: ask any question to the site management

- Rules for calculating VAT when carrying out export-import transactions

- How to submit reports to the Pension Fund for the 3rd quarter of 2012

- Reporting to the Social Insurance Fund for 9 months of 2012

- Preparation of reports to the Pension Fund for the 2nd quarter. Difficult questions

- Launch of electronic invoices in Russia

- How to reduce costs for IT equipment, software and IT personnel using cloud power

- Reporting to the Pension Fund for the 1st quarter of 2012. Main changes

- Income tax: nuances of filling out the declaration for 2011

- Annual reporting to the Pension Fund. Current issues

- New in financial statements for 2011

- Reporting to the Social Insurance Fund in questions and answers

- Semi-annual reporting to the Pension Fund in questions and answers

- Calculation of temporary disability benefits in 2011

- Electronic invoices and electronic primary documents

- Preparation of financial statements for 2010

- Calculation of sick leave in 2011. Maternity and transition benefits

- New in the legislation on taxes and insurance premiums in 2011

- Changes in financial statements in 2011

- DDoS attacks in Russia as a method of unfair competition.

- Banking products for individuals: lending, deposits, special offers

- A document in electronic form is an effective solution to current problems

- How to find a job using Clerk.Ru

- Providing information per person. accounting for the first half of 2010

- Tax liability: who is responsible for what?

- Inspections, collection, refund/offset of taxes and other issues of Part 1 of the Tax Code of the Russian Federation

- Calculation of sick sheets and insurance premiums in the light of quarterly reporting

- Replacement of unified social tax with insurance premiums and other innovations of 2010

- Liquidation of commercial and non-profit organizations

- Accounting and tax accounting of inventory items

- Mandatory re-registration of companies in accordance with Law No. 312-FZ

- PR and marketing in the field of professional services in-house

- Clerk.Ru: design change

- Building a personal financial plan: dreams and reality

- Preparation of accounting reporting. Changes in Russia accounting standards in 2009

- Kickbacks in sales: pros and cons

- Losing a job during a crisis. What to do?

- Everything you wanted to know about Clerk.Ru, but were embarrassed to ask

- Credit in a crisis: conditions and opportunities

- Preserving capital during a crisis: strategies for private investors

- VAT: deductions on advances. Questions with and without answers

- Press conference of Santa Claus

- Changes to the Tax Code coming into force in 2009

- Income tax taking into account the latest changes and clarifications from the Ministry of Finance

- Russian crisis: threats and opportunities

- Network business: quality goods or a scam?

- CASCO: insurance without secrets

- Payments to individuals

- Raiding. How to protect your own business?

- Current issues of VAT calculation and reimbursement

- Special modes: UTII and simplified tax system. Features and difficult questions

- Income tax. Calculation, features of calculus, controversial issues

- Accounting policies for accounting purposes

- Tax audits. Practice of application of new rules

- VAT: calculation procedure

- Outsourcing Q&A

- How can an accountant comply with the requirements of the Law “On Personal Data”

- The ideal archive of accounting documents

- Service forums

- Archive FAQ (Frequently Asked Questions) FAQ: Frequently Asked Questions on Accounting and Taxes

- Games and trainings

- Self-confidence training

- Foreign trade activities in harsh reality

- Book of complaints and suggestions

- Diaries

Deduction of VAT from the seller when returning advances and goods

CORRECT OPTION OF CALCULATIONS At the time of provision of services: DEBIT 62 CREDIT 90-1 – 107,600 rubles. — revenue from the provision of services is reflected; DEBIT 90-3 CREDIT 68 – 16,414 rub. — VAT is charged on the sale of services; DEBIT 68 CREDIT 62 “Advance received” – 16,414 rubles. — previously accrued VAT was accepted for deduction in the part of the realized CREDIT 62 – 107,600 rubles. - offset of advance payment. At the time of transfer of the unused advance: DEBIT 62 “Advance received” CREDIT 51 – 10,400 rubles. — return of the advance payment to the buyer; DEBIT 68 CREDIT 62 “Advance received” – 1586 rubles. — accepted for deduction of VAT on the returned part of the advance. Please note that in practice a situation may arise when the seller returns the unused advance payment to the buyer for the upcoming delivery of goods, performance of work or provision of services. In this case, the return of the advance payment is not related to the termination of the contract.

As a rule, the amount of tax previously accrued upon receipt of this amount has already been taken for deduction. With a literal interpretation of the provisions of the Tax Code, in the case of a refund of an advance payment not related to a change or termination of a contract, a deduction of previously accrued tax is not provided. Therefore, there is a high probability of tax disputes related to the legality of deducting VAT previously accrued on payment amounts for upcoming deliveries of goods (performance of work, provision of services). In this case, we recommend that you reverse this tax amount in your accounting and submit an updated VAT return to the tax authorities.

In one of their latest letters, tax authorities explained the procedure for applying VAT deductions in the event that the receipt and return of advance payments are carried out in the same tax period upon termination of the contract. The organization must reflect in the VAT return the amount of tax on the prepayment received and in the same tax period, if there are documents confirming the return of the amounts of this prepayment, and subject to a change or termination of the contract, it has the right to deduct the corresponding amount of tax 5. Upon receipt of the prepayment, the seller ( the contractor) is obliged to charge VAT, including if the advance payment was received in non-monetary means (for example, by a third party’s bill of exchange). In paragraph 5 of Article 172 of the Tax Code, the condition for deducting VAT in the event of a change in conditions or termination of a previously concluded agreement with the buyer (customer) is the return of the corresponding amounts of advance payments. However, it is not indicated that such a return must necessarily be made in cash. In this regard, we can conclude that when an advance payment previously received by the seller is returned by a third party bill of exchange, the corresponding amount of VAT is subject to deduction, regardless of whether this third party bill of exchange was received as an advance from the buyer (customer) or otherwise. This conclusion is also confirmed by a number of court decisions (post. FAS MO dated June 20, 2005 in case No. KA-A40/5402-05, FAS PO dated March 28, 2005 in case No. A12-20637/04-C36, dated April 26, 2007 in case N A55-11874/06, dated January 15, 2009 in case N A65-9611/2008).

How to properly notify the bank about what happened

The mechanism is like this. The organization that accepted the payment by mistake sends a request to resolve this issue to the bank. This must be done in writing. It is important to contact bank employees within 10 days from the date of receipt of the bank account statement about the receipt of excess funds. Otherwise, it will be more difficult to return the payment order.

There is no generally accepted form for submitting such a request document. But each bank usually has its own developed forms. If the credit institution does not have a specific form for submitting an application, then a free form application is acceptable.

The bank can refund the excess amount received in several ways:

- Debiting funds from an account without an order from its owner. This is only possible if there is an agreement between the bank and the organization.

- Write-off of funds after receiving a payment order for the return of funds (if there is no corresponding agreement between the bank and the organization).