Which section of the declaration does line 170 include and what is its meaning?

Line 170 in the VAT return is included in the 2nd part of section 3, i.e., part of the deductions.

It should reflect deductions for advances received by the seller, from which he accrued tax payable at the time of receipt. The VAT return for reports for the 4th quarter of 2021 and tax periods of 2021 is applied as amended by Order of the Federal Tax Service of Russia dated August 19, 2020 No. ED-7-3/ [email protected]

ConsultantPlus experts told us what changes the form has undergone. Explore the ready-made solution by getting trial access to the K+ system for free.

Since accruals as a result of the update should be described in a larger number of transactions than in the previous edition of the document, the total number of descriptions of transactions and deductions in the section has increased. This led to line 170 changing the deduction serial number, but the description and line code itself did not change.

To learn about the form in which an advance payment can be made, read the material “VAT on advance payments: examples, postings, complex situations .

What is reflected in field 070

Tax authorities approved the current form of the declaration and the procedure for filling it out in order No. MMB-7-3/ [email protected] dated 10.29.2014 (as amended by No. CA-7-3/ [email protected] dated 12.28.2018). This is what is reflected in line 70 of the VAT return in different sections (in order of their numbers):

- Start date of the investment partnership.

- Operation code.

- The amount of advance received.

- The tax base.

- Tax deductions.

- Operation code.

- Sections 8 and 9 are the date of the seller's adjustment invoice.

- Sections 10 and 11 - adjustment invoice number.

- Section 12 is the amount of tax charged to the buyer.

IMPORTANT!

Reports for the 3rd quarter must be submitted using the form from Order No. MMB-7-3/ [email protected] The value added tax report for the 4th quarter must be submitted using the new form set forth in Order No. ED-7-3/ [email protected] dated 08/19/2020.

In section 3, fill in the cell with serial number 5, line code - 070 of the VAT declaration: in it we indicate the amount of payment or partial payment that was received from buyers as an advance. In the next cell, code 070 allocates value added tax, calculated from the prepayment. When making an advance, sellers issue an advance invoice and highlight in it the calculated value added tax to be paid.

What determines the emergence of the right to deduct advances received?

Receipt of payment (in full or partial) on account of a later shipment subject to tax obliges the seller to allocate tax from the amount of this payment (subclause 2, clause 1, article 167 of the Tax Code of the Russian Federation). This procedure is accompanied by the creation of an advance invoice (clause 3 of Article 168 of the Tax Code of the Russian Federation), which gives the buyer the opportunity to apply a deduction during the period of transfer of funds. The seller also acquires the right to use the deduction (clause 8 of Article 171 of the Tax Code of the Russian Federation), but only at a different time. This moment will occur during the period of shipment of what was sold with the condition of prepayment (clause 6 of Article 172 of the Tax Code of the Russian Federation) or during the period of cancellation of the agreement on future shipment, which will result in the return of the advance (clause 5 of Article 171 of the Tax Code of the Russian Federation).

What is the reason for the possibility of such a deduction from the seller? With the fact that there is an obligation to create an invoice at the time of shipment (clause 1 of Article 168 of the Tax Code of the Russian Federation). The use of this deduction eliminates double taxation of income received upon sale.

For details on the specifics of creating an advance invoice and entering it into the purchase/sales books, read the article “Acceptance for deduction of VAT on advances received .

Line 170 is also in section 6 of the VAT return. ConsultantPlus experts explained how to fill out this section correctly using an example. To do everything right, get trial access to the system and upgrade to the Ready Solution for free. There you will also find explanations for filling out each line of the report.

Section 3 of the VAT return

This section collects all the data for tax calculation.

Line 010 of column 3 corresponds to the amount of revenue reflected on the credit of account 90.1 for the reporting period.

Line 010 of column 5 corresponds to the amount of VAT reflected in the debit of account 90.3.

Line 070, column 5 corresponds to the amount of advance VAT reflected in the debit of account 76 “VAT on advances” (VAT accrued on prepayment received).

Line 090 of column 5 corresponds to the amount reflected in the debit of account 76 “VAT on advances” (VAT on advances issued).

Line 118 of column 5 corresponds to the amount reflected in the credit of account 68 “VAT”. In addition, this line can be checked against the total VAT amount in the sales book.

Line 120 of column 3 corresponds to the amount reflected in the credit of account 19.

Line 130 of column 3 corresponds to the amount reflected in the credit of account 76 “VAT on advances” (VAT on advances issued).

Line 170 of column 3 corresponds to the amount reflected in the credit of account 76 “VAT on advances” (VAT accrued on the received prepayment).

Line 190 of column 3 corresponds to the amount reflected in the debit of account 68 “VAT” (excluding VAT transferred to the budget for the previous tax period). In addition, this line can be checked against the total VAT amount in the purchase book.

How to fill out line 170

The rules for filling out line 170 (clause 38.19 of appendix 2 to the order of the Federal Tax Service of Russia dated October 29, 2014 No. ММВ-7-3 / [email protected] ) require correspondence between the data in section 3 falling into lines 070 and 170. This means that in deductions Only those amounts of tax can be taken that were accrued for payment from advances and were reflected, accordingly, in line 070. The amount of the deduction depends on the ratio of the amounts of prepayment and shipment:

- if the shipment amount is equal to or exceeds the amount of the advance payment, then the deduction is taken in the amount accrued from the advance payment;

- if the shipment is made for an amount less than the advance payment received, then the tax to be deducted will correspond to the amount of the shipment.

Do I need to enter data in lines 070 and 170 when receiving an advance payment and making shipments in the same quarter? The Ministry of Finance (letter dated October 12, 2011 No. 03-07-14/99) and the Federal Tax Service of Russia (letter dated July 20, 2011 No. ED-4-3/11684 and earlier) insist on the obligation to reflect these transactions if they fall within the same period.

To learn how to deal with the tax accrued on an advance payment that is among the overdue debts, read the material “VAT when writing off accounts payable: problematic situations .

Controversial cases

According to the inspectors, VAT needs to be restored in a number of cases. For example, in case of theft, destruction, confiscation of goods, etc.

However, arbitration courts take a different point of view. Their position is expressed in the decision of the Supreme Arbitration Court of Russia dated October 23, 2006 No. 10652/06.

The judges pointed out that the code obliges people to pay only legally established taxes. This means that the restoration of VAT, previously legally accepted for deduction, must be provided for by law. Cases in which it is necessary to restore the tax are listed in paragraph 3 of Article 170 of the Tax Code. This list is closed. Consequently, the obligation to restore VAT amounts, not provided for by the code, is illegal.

Later, in decision No. 3943/11 of May 19, 2011, the senior judges confirmed the earlier conclusion. They pointed out that Article 170 of the Tax Code does not provide for the restoration of VAT when writing off expired goods.

Disposal of property as a result of fire is also not mentioned in this norm. On this basis, in a letter dated May 21, 2015 No. GD-4-3/8627, the Federal Tax Service of Russia concluded that the VAT previously accepted for deduction on burnt property does not need to be restored.

The tax authorities again referred to the position of the Supreme Arbitration Court of Russia, set out in decision No. 10652/06 dated October 23, 2006. And we came to the conclusion that in situations not listed in paragraph 3 of Article 170 of the Tax Code, VAT should not be restored.

Thus, input VAT accepted for deduction when purchasing property that was subsequently burned down in a fire cannot be restored.

In Berator you will find examples of arbitration cases for VAT restoration lost by tax authorities. Type in the search bar of the berator: “VAT restoration”.

Practical encyclopedia of an accountant

All changes for 2021 have already been made to the berator by experts. In answer to any question, you have everything you need: an exact algorithm of actions, current examples from real accounting practice, postings and samples of filling out documents.

VAT restoration is a procedure for sending for payment tax that was previously accepted for deduction. Cases when such a need arises for a taxpayer are prescribed in paragraph 3 of Article 170 of the Tax Code of the Russian Federation:

- Contribution to the authorized or share capital of a company (mutual fund of a cooperative) or contribution to an investment partnership in the form of property, property rights and intangible assets, as well as replenishment of the target capital of a non-profit enterprise in the form of real estate;

- The use of acquired assets in transactions specified in paragraph 2 of Article 170 of the Tax Code of the Russian Federation, in which there is no need to charge VAT for payment (transactions exempt from VAT, as well as those sold outside the Russian Federation or not recognized as sales, the use of special regimes);

- Advance payment for planned deliveries;

- Reducing the cost of items in supplier documents or reducing the quantity;

- Receiving subsidies.

The tax must be restored only in the specified cases; the list given is closed. The exact wording of each paragraph can be found in paragraph 3 of Article 170.

As of 01/01/15, the need to restore the added tax in relation to goods used in those transactions to which a 0% rate is applicable has been abolished.

Results

Line 170, located in section 3 of the VAT return, includes those amounts of tax from advances received by the seller, which he has the right to submit for deduction at the time of shipment or return of the advance payment.

The basis for the deduction is the advance invoice issued to the buyer upon receipt of the advance payment. The advance and shipment amounts may not coincide, and then the deduction amount will correspond to the lower of these amounts. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Other recovery cases

VAT should be restored in several more cases.

1. If a company has transferred an advance to the seller, it can deduct the VAT paid as part of the advance. At the time of shipment and receipt of an invoice from the seller, the company deducts VAT on the purchased goods. And VAT, offset when paying the advance, is restored.

Please note: from October 1, 2014, a rule has been in force according to which the amounts of VAT accepted for deduction in relation to the advance payment should be restored in the amount related to the goods shipped (work performed, services rendered, transferred property rights), in payment of which the amounts are subject to offset advance That is, if the seller shipped the goods for an amount less than the advance received, the buyer is obliged to recover VAT only in the amount indicated on the shipment invoice.

3. If after the purchase the cost of purchased goods (works, services) has decreased, then VAT must be restored in the amount of the difference between the tax amounts on the cost of purchased goods before and after the reduction. In this case, VAT is restored during the period of receipt of either primary documents for changes in the cost of purchased goods or an adjustment invoice (depending on what happened earlier).

4. If a company is provided with subsidies from the federal budget to reimburse the costs of paying for purchased goods (work, services), including tax, as well as to reimburse the costs of paying tax upon import, then VAT is restored during the period of provision of subsidies.

5. If the company began to use the purchased (built) property in operations not subject to VAT, then the tax is restored within 10 years, starting from the year in which the accrual of tax depreciation began.

A similar rule applies to reconstructed (modernized) real estate properties. In this case, VAT is restored for 10 years, starting from the year in which tax depreciation began to be calculated on the changed value of the object.

From January 1, 2015, the norm on the restoration of VAT on goods (works, services) that are used in transactions at a rate of 0% was excluded from the Tax Code (clause 5, clause 3, article 170 of the Tax Code of the Russian Federation).

This norm ordered taxpayers to restore previously deductible VAT in the event of further use of goods (work, services) in sales operations subject to VAT at a zero rate in accordance with paragraph 1 of Article 164 of the Tax Code. The tax had to be restored in the period in which the goods were shipped (work performed, services provided). Let us recall that in this norm, among the operations taxed at a zero VAT rate, the sale of goods for export, services for the international transportation of goods, work (services) for the processing of goods placed under the customs procedure of processing on the customs territory, services for the provision of railway rolling stock are named and (or) containers, as well as transport and forwarding services, services for transporting passengers and luggage, etc.

Restoration of VAT upon transition to the simplified tax system

It is necessary to restore the entire amount of the added tax, which was previously accepted for deduction on goods, services, and work that had not yet been used in taxable transactions at the beginning of the transition to the simplified regime. For depreciable objects, you only need to recover a portion of the tax corresponding to their residual value (without revaluation).

This procedure should be performed in the period preceding the date of transition to the simplified regime. For example, if the transition to a simplified tax system is carried out from the beginning of 2021, then the tax should be restored in the 4th quarter of 2015.

The recovered tax is included in other expenses.

The restoration procedure is carried out in a similar way if the company changes the applied regime to UTII and PSN.

In the 4th quarter, VAT on these values should be restored by making the following entries:

- D19 K68.VAT in the amount of 100,000*18% = 18,000 – the tax on goods has been restored;

- D91 K19 in the amount of 18,000 - tax is taken into account as other expenses.

Filling out sections of the declaration

The reporting regulations for VAT must comply with the requirements of the instructions of the Ministry of Finance and the Federal Tax Service, set out in order No. ММВ-7-3/558 dated October 29, 2014.

Title page

The procedure for filling out the main sheet of the VAT return does not differ from the rules established for all types of reporting to the Federal Tax Service:

- Information about the payer’s TIN and KPP is written at the top of the sheet and does not differ from the information in the registration documents;

- The tax period is indicated by the code used for tax reporting. The decoding of the codes is indicated in Appendix No. 3 to the Instructions for filling out the Declaration.

- Tax inspectorate code - the declaration is submitted to the division of the Federal Tax Service where the payer is registered. Accurate information about all codes of territorial tax authorities is published on the Federal Tax Service website.

- The name of the business entity corresponds exactly to the name specified in the constituent documentation.

- OKVED code - the main type of activity according to the statistical code is indicated on the title page. The indicator is indicated in the Rosstat information letter and in the Unified State Register of Legal Entities extract.

- Contact phone number, number of completed and submitted declaration sheets and applications.

The signature of the payer’s representative and the date of generation of the report are affixed to the title page. On the right side of the sheet there is space for confirming records of the authorized person of the tax service.

Section 1

Section 1 is the final section in which the VAT payer reports the amounts subject to payment or reimbursement based on the results of accounting/tax accounting and information from section 3 of the declaration.

The sheet must indicate the code of the territorial entity (OKTMO) where the taxpayer operates and is registered. Line 020 records the KBK (budget classification code) for this type of tax. VAT payers are guided by the KBK for standard activities -001 1000 110. The KBK can be clarified in the latest edition of Order of the Ministry of Finance No. 65n dated 07/01/2013.

Attention: if the BCC is inaccurately indicated in the VAT return, the tax paid will not be credited to the taxpayer’s personal account and will be deposited in the accounts of the Federal Treasury until the identity of the payment is clarified. A penalty will be charged for late tax payment.

Line 030 is filled in only if the invoice is issued by a preferential taxpayer exempt from VAT.

In lines 040 and 050 you should record the amounts received for tax calculation. If the result of the calculation is positive, then the amount of VAT payable is indicated in line 040; if the result is negative, the result is recorded in line 050 and is subject to reimbursement from the state budget.

Section 2

This section is required to be completed by tax agents for each organization for which they have this status. These may be foreign partners who do not pay VAT, lessors and sellers of municipal property.

For each counterparty, a separate sheet of Section 2 is filled out, where its name, INN (if any), BCC and transaction code must be indicated.

When reselling confiscated goods or carrying out trade transactions with foreign partners, tax agents fill out line 080-100 of Section 2 - the amount of shipment and the amounts received as an advance payment. The total amount payable by the tax agent is reflected in line 060 , taking into account the values entered in the following lines - 080 and 090 . The amount of tax deduction for realized advances (line 100) reduces the final amount of VAT.

Section 3

The main section of VAT reporting, in which taxpayers calculate the tax payable/reimbursable at the rates provided by law, raises the most questions among accountants. Sequential filling of section lines looks like this:

- Lines 010-040 reflect the amount of revenue from sales (based on shipment), taxed, respectively, at the applicable tax and settlement rates. The amount recorded in these lines must be equal to the amount of income recorded in account 90.1 and shown in the calculation of income tax. If discrepancies are found in the indicators in the declarations, the fiscal authorities will request explanations.

- Page 050 is filled in in a special case - when an organization is sold as a complex of accounting assets. The tax base in this case is the book value of the property multiplied by a special adjustment indicator.

- Page 060 concerns production and construction organizations carrying out construction and installation work for their own needs. This line reproduces the cost of the work performed, which includes all actual costs incurred during construction or installation.

- Page 070 – in the column “Tax base” in this line you should enter the amount of all cash receipts received on account of upcoming deliveries. The VAT amount is calculated at the rate of 18/118 or 10/110, depending on the type of goods/services/work. If the sale occurs within 5 days after the prepayment “falls” into the current account, then this amount is not indicated in the declaration as an advance received.

In section 3 it is necessary to enter the VAT amounts, which, in accordance with the requirements of paragraph 3 of Article 170 of the Tax Code, must be restored in tax accounting. This applies to amounts previously declared as tax deductions on preferential grounds - the use of a special regime, exemption from VAT. The restored tax amounts are reflected in total on line 080, with specification on lines 090 and 100.

In lines 105-109, data on the adjustment of VAT amounts in accounting during the reporting period is entered. This may be the erroneous application of a reduced tax rate, the wrongful classification of transactions as non-taxable, or the inability to confirm a zero rate.

The total amount of accrued VAT is indicated in line 110 and consists of the sum of all indicators reflected in column 5 of lines 010-080, 105-109. The final tax figure should be equal to the amount of VAT in the sales book based on the total turnover for the reporting quarter.

Lines 120-190 (column 3) are devoted to deductions that require the amount of VAT to be paid:

- The amount of deductions on line 120 is formed on the basis of invoices received from counterparties-suppliers and is equal to the amount of VAT in the purchase book.

- Line 130 is filled in similar to page 070, but contains data on the amount of tax paid to the supplier as an advance payment.

- Line 140 duplicates line 060 and reflects the tax calculated from the amount of actual costs when carrying out construction and installation work for the needs of the taxpayer.

- Lines 150 – 160 relate to foreign trade activities and amount to VAT paid at customs or accrued on the cost of goods imported into Russia from the Customs Union countries.

- In line 170 it is necessary to indicate the amount of VAT previously accrued on advances received if sales occurred in the reporting quarter.

- Line 180 is filled in by tax agents and contains the VAT amount indicated in line 060 of Section 2.

The result from adding the amounts of deductions for all legal reasons is recorded in line 190, and lines 200 and 210 are the result of performing arithmetic operations between lines 110 gr.5 and 190 gr.3. If the result of subtracting the amount of deductions from the accrued VAT is positive, then the resulting value is reflected in line 200 as VAT payable. Otherwise, if the amount of deductions exceeds the calculated VAT amount, you should fill out page 210 gr. 3, how VAT is refundable.

The tax amounts reflected in lines 200 or 210 of section 3 should fall into lines 040-050 of section 1.

The VAT return requires filling out two appendices to section 3. These forms are filled out:

- For fixed assets that are used in non-VAT taxable activities. An important condition is that the tax on these assets was previously accepted for deduction and is now subject to restoration within 10 years. The application reflects individually the type of OS, the date of commissioning, and the amount accepted for deduction for the current year. This application must be completed only in the 4th quarter return.

- For foreign companies operating in the Russian Federation through their own representative offices/branches.

Sections 4, 5, 6

These sections must be completed only by those payers who, in their activities, use the right to apply a zero VAT rate. The difference between the sections consists of some nuances:

- Section 4 is completed by a taxpayer who is able to document the lawful use of the 0% rate. Section 4 provides for mandatory reflection of the business transaction code, the amount of revenue received and the amount of the declared tax deduction.

- Section 6 is completed in cases where, on the date of submission of the declaration, the taxpayer did not have time to collect a complete package of documents to confirm the benefit. Unjustified transactions are included in section 6, but can subsequently be accepted for reimbursement and transferred to section 4. For this, documentation is required.

- Section 5 will have to be completed by those “zeros” who previously claimed a deduction on documents, but received the right to apply a preferential rate only in this reporting period.

Important: if there are several grounds for applying Section 5, the taxpayer must fill out separately each reporting period when the deduction was claimed.

Section 7

This sheet is intended to transmit information on transactions that were carried out in the reporting quarter and, in accordance with Art. 149 clause 2 of the Tax Code of the Russian Federation, are exempt from VAT. All documented commercial actions are grouped by codes, which are named in Appendix No. 1 to the current instructions.

The category of transactions reflected in Section 7 also includes amounts of money received into the taxpayer’s bank account on account of upcoming supplies.

Only one condition must be met - the manufacture of products or the implementation of work is long-term in nature and will be completed in 6 calendar months.

Sections 8, 9

Relatively recently appeared sections provide for the inclusion in the declaration of information listed in the sales book/purchase book for the reporting period. In order for the fiscal authorities to automatically conduct a desk audit, these sheets indicate all the counterparties “included” in the tax registers for VAT.

According to the regulations, in sections 8 and 9 , information about suppliers and buyers (TIN, KPP), details of received or issued invoices, cost characteristics of goods/services, amounts of revenue and accrued VAT should be disclosed.

Important: electronic reporting modules make it possible to reconcile the data in sections 8 and 9 with counterparties before submitting the declaration. Otherwise, in the event of data discrepancies during cross-check with the Federal Tax Service, amounts to be deducted that do not correspond to the supplier’s sales book may be excluded from the calculation and the amount of VAT payable will increase.

In case of correction of data in previously declared invoices, the taxpayer is obliged to create attachments to sections 8 and 9.

Section 10, 11

These sheets are of a specific nature and must be issued only to business entities of several categories:

- commission agents and agents working for the benefit of third parties;

- persons providing forwarding services;

- developer companies.

Sections 10-11 should list information from the journal of received and submitted invoices with the amounts of VAT and taxable turnover.

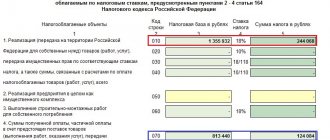

Line 070 of Section 3: requirements for filling out the Federal Tax Service order

You can see what line 070 of section 3 of the VAT return looks like and how the Federal Tax Service order No. MMB-7-3/ [email protected] instructs you to fill it out, you can see in the figure:

Before advance VAT is included in line 070 of section 3, the buyer must:

The following publications will introduce you to the nuances of filling out other lines of the VAT return:

Reconciliation with the tax office for VAT

After submitting the declaration and paying the tax, check with the inspectorate. To do this, ask the tax office for a reconciliation report or a certificate about the status of settlements with the budget. Documents are prepared within 5 working days.

In the act you will see whether your VAT calculations coincide with the information from the Federal Tax Service. If everything is correct, the act can be signed and submitted to the inspection. If not, sign the deed with Fr. After this, the tax office will ask you to provide evidence confirming the correctness of your calculations.

We recommend you the cloud service Kontur.Accounting. When filling out a VAT return, our program automatically checks all control ratios. And the report lines are filled in in accordance with the accounting accounts. We give all newbies a free trial period of 14 days.

Recovering VAT from advance payment

When making a preliminary calculation, the buyer has the opportunity to send the amount of VAT for reimbursement according to the invoice generated by the seller upon receipt of the cash advance.

At the moment when, against this payment, goods and materials are shipped or work or services are performed, the seller generates primary documentation confirming the completion of the sales operation. Based on this documentation, the buyer restores the tax that was previously sent for reimbursement.

The seller also attaches an invoice within 5 days to the shipping documentation, according to which the accrued amount of VAT is sent for deduction.

The important thing is that the tax should be restored to the amount in which it was previously deducted.

04/21 Company B hands over the invoice to Company A.

If, against the advance payment, the delivery is carried out in parts (the work is delivered in stages), then VAT must also be restored in parts. The amount of added tax to the restoration is taken from the documents provided by the seller upon shipment (delivery of work, services). This situation is relevant when the amount of the advance exceeds the cost of each batch of goods (work).

When returning an advance, the added tax must be restored in the period in which the funds were received.

Recovering tax from advances paid

After complete delivery of goods for which advance payments have already been made, the buyer must restore the previously refunded tax on them. This is carried out based on the results of the quarter in which the final movement of products to the buyer’s warehouse is carried out in accordance with subclause. 3 p. 3 art. 170 Tax Code of the Russian Federation. The basis for carrying out this operation may be:

submission by the seller of a complete package of documents for all shipped products for which an advance payment was previously received from the buyer;

return of prepayment from the counterparty;

the fact that the payment has ceased to be preliminary and has been accepted for offset on another basis not related to transfers for planned shipments;

assigning the advance amount to the financial result;

repayment of the prepayment amount by offsetting claims.

It cannot be said that the obligation to restore the VAT previously accepted for deduction on all the above grounds cannot be challenged. However, existing practice shows that the Federal Tax Service authorities insist on its occurrence upon the occurrence of 1 of the above events. At the same time, attempts by organizations to evade compliance with tax restoration requirements lead them to court.

If it is necessary to add the amount of previously credited tax to the total VAT accruals, entries are made in the accounting records inverse to those created earlier: Dt 76 “Advances issued” Kt 68 “VAT”

The results of this posting for the period form the additional amount of tax payable. It should be included in the declaration.