The assets and liabilities of an enterprise are important economic concepts that allow us to evaluate the efficiency and effectiveness of the company’s activities, its success and reliability. Next, we will look at what they are from the point of view of economics and accounting, how they differ, their meaning and relationship with each other.

Assets are the totality of a company's resources that are used in economic activities and can generate profit. These include both property and cash, as well as values that do not have material expression. An example of an intangible resource is intellectual property and, in particular, patents. Moreover, such assets can be even more valuable than property in the classical sense: everyone knows the confrontation between Apple and Samsung corporations and their struggle to own patents that can bring billions of dollars in profits in the future. The corresponding section of the balance sheet consists of current and non-current assets, and also reflects the total amount for such.

An enterprise's liabilities are the sources from which assets are formed. Every resource an organization has must come from something. The liabilities section of the balance sheet shows the capital and liabilities of the company, which are the sources of obtaining existing assets. The enlarged balance sheet structure can be depicted in the form of a table.

| Assets | Passive |

|

|

Important!

In the balance sheet, assets are grouped by liquidity, i.e. if possible, convert into money. For liabilities, grouping by urgency of payment is used. Let's take a closer look at each of the concepts.

Why is account 02 needed?

Fixed assets (PE) are assets that a company uses to produce products or provide services for more than a year.

Depreciation is regularly charged on fixed assets - their cost, as they wear out, is transferred in parts to the cost of goods, work, and services. Most fixed assets are very expensive, so a one-time write-off of the cost as an expense will result in the cost of production being greatly inflated. Account 02 according to the chart of accounts is called “Depreciation of fixed assets”. On it, accountants keep records of accrued depreciation, its increase and decrease, write-off, and through it they register the disposal of fixed assets.

Depreciation and wear should not be confused. Depreciation is accounted for in off-balance sheet account 010, and is accrued at the end of the year for housing stock, housing and communal services, or fixed assets of non-profit organizations.

Explanations for account 02 are given in the chart of accounts approved by Order of the Ministry of Finance dated October 31, 2000 No. 94n.

Costs: fixed, variable, indirect, direct

What wear will be depends very little on production volumes and their changes. This allows you to classify depreciation charges as permanent expenses. The company decides in favor of a specific method for calculating funds and takes into account the same amount every month. This means that when producing hundreds of units of a product, deductions for depreciation are the same as when producing a thousand units.

According to the laws currently in force in our country, entrepreneurs are not limited in where and how to allocate costs. If you wish, you can qualify a specific article as indirect, and call another direct; you can do the opposite. Chapter 25 of the Tax Code is devoted to this, but there are no specific explanations or working rules in it yet. The taxpayer can independently make a decision and set up accounting in a way that is beneficial to him. In practice, depreciation charges are almost always classified as indirect costs.

How does depreciation work?

You need to start accruing depreciation from the first day of the month following the day when the fixed asset was accepted for accounting. We accepted the OS in August - we calculate depreciation from September.

Until the useful life expires, accruals cannot be stopped. Suspension of work or cessation of use of equipment is not a reason to stop accrual. Suspension is permitted only for conservation for a period of more than 3 months or for a restoration period of more than 12 months.

Accrual must be stopped from the first day of the month following the one in which the object was written off or its cost was fully paid off. That is, depreciation does not need to be charged on any fully depreciated fixed assets with zero residual value, even if your company continues to use them.

Depreciation for recording is calculated monthly in accordance with the method approved in the accounting policy for individual groups or fixed assets:

- linear;

- reducing balance;

- by the sum of the numbers of years of useful life;

- proportional to production volume.

For any method, the useful life is important - this is the period during which the depreciable object generates income. The organization determines the period when it accepts the asset for accounting. When repairing or improving equipment, the useful life is increased.

What are assets and liabilities in accounting - the concept in simple words

Assets are the property of an organization used in business activities; its main task is to generate profit.

Assets include:

- funds - cash at the cash desk, non-cash funds in a current account, in foreign currency, in special accounts, monetary documents;

- property - goods, products, materials, real estate, transport, equipment;

- debt of other persons to the organization - buyers, suppliers, other organizations;

- loans issued to employees and other organizations.

Liabilities are debts, liabilities and capital, which show where the assets come from and are their sources.

In general, this is a debt to someone that sooner or later needs to be repaid - contributions to the authorized capital are returned to the founders at closing, loans are returned to banks, salaries are issued to employees, debts are paid to counterparties, taxes are transferred to the budget.

Liabilities include:

- own capital - authorized, additional, reserve, sold shares, shares;

- borrowed capital - loans and borrowings provided to an enterprise by banks and other persons;

- debts of the organization to other persons - accounts payable;

- wage arrears to staff;

- taxes are a debt to the budget.

Example table

| Assets | Liabilities |

| Cash and non-cash money and monetary documents | Debts to staff (salaries and others) |

| Revenue from ordinary activities | Authorized capital |

| Fixed assets | Reserve capital |

| Objects of intangible assets | Extra capital |

| Goods and material assets | Shares |

| Products at all stages of production | Repurchased shares |

| Raw materials and semi-finished products | Results of revaluation of fixed assets, intangible assets |

| Debts of counterparties | Debts to counterparties |

| Credits and loans provided | Borrowings taken out |

| Financial investments | Debts to the budget (taxes and contributions) |

| VAT on purchased assets | Retained earnings and uncovered losses |

Why are they always equal in accounting?

Assets and liabilities are always equal - this is the main rule of accounting, showing the error-free conduct of accounting activities.

Why is equality true?

Liabilities are sources of assets; they form them.

Example 1:

Operation: Receipt of goods to the warehouse from the supplier.

A liability (accounts payable to a supplier) created an asset (goods in stock).

Example 2:

Operation: Obtaining a loan from a bank.

P. (credit) created A. (money in the current account).

Example 3:

Operation: The founder makes a contribution to the authorized capital in the form of a car.

P. (contribution to the authorized capital) created A. (car).

Since liabilities form assets, their total amounts must be equal. When liabilities change by the same amount, assets change.

Example 4:

Operation: Transfer of payment for goods to the supplier in the amount of 200,000 rubles.

During the operation, a decrease in P. (repayment of accounts payable) by 200,000 led to a decrease in A. (the amount of money in the current account) by the same amount of 200,000.

That is, any change in liabilities always entails a corresponding change in assets (↑ P. → ↑ A., ↓ P. → ↓ A.). As a result, after any transaction completed, the total amount of assets equals the total amount of liabilities at any given time.

Failure to comply with this equality indicates incorrect accounting and errors.

Balance sheet

It is important to be able to distinguish assets from liabilities; this will allow you to correctly draw up a balance sheet and check the accuracy of your accounting.

All accounting ultimately comes down to drawing up a final annual report - a balance sheet, which shows the financial condition of the enterprise. Throughout the year, records are kept of all business transactions; at the end of the year, all recorded amounts are grouped into balance sheet items.

The balance sheet is a two-sided table: the left half collects the organization’s assets, the right half collects capital, reserves and liabilities, grouped according to homogeneous criteria. Next, the total amount is calculated for each side of the balance sheet and the final equality of assets and liabilities is checked.

The balance sheet form has been approved, but it may be supplemented depending on the specifics of the company’s activities.

Small enterprises have the right to use a simplified version of the balance sheet, which provides data in a generalized form.

Assets on the balance sheet are divided into:

- non-current - intended to generate profit in the long term (intangible, fixed assets, long-term investments);

- circulating - mobile and quickly consumed, require constant replenishment, capable of generating profit in a short time (goods, products, materials, money, raw materials, accounts receivable).

Liabilities in the balance sheet are divided into:

- capital and reserves - reserve, additional, authorized, results of revaluation, purchased own shares;

- long-term liabilities - debts whose repayment period exceeds 1 year;

- short-term liabilities are debts that must be repaid within 1 year.

An example of a company's annual balance sheet:

Account 02 - active or passive

Account 02 is classified as passive. This means that the accrual and accumulation of depreciation is reflected on the loan. The reduction or write-off of accrued amounts is carried out by debiting account 02. The account is closed by posting Debit 02 - Credit 01.

Although the account is passive, it is not reflected in sections III-V of the balance sheet, but it participates in the formation of an asset - a line of fixed assets. Let us recall that fixed assets in the balance sheet are reflected at their residual value, that is, they are reduced by the credit balance of account 02.

Keep records of exports and imports in the Kontur.Accounting web service. Simple accounting, payroll and reporting in one service

Analytical accounting for account 02

Depreciation is tightly tied to fixed assets, so all analytics for account 02 are built around individual fixed assets inventory objects. They include both the asset itself and all the necessary fixtures and accessories for its functioning.

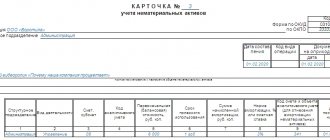

They keep analytical records in one of three standard documents, which are also used for OS analytics:

- OS object inventory card;

- inventory card for group accounting of OS objects;

- inventory book for accounting of OS objects.

They reflect information about the receipt, movement, disposal, modifications, improvements of fixed assets, and also make entries about depreciation accrued from the beginning of operation.

A separate story

A situation is possible when there is a certain fixed asset, divided into several components, and the analysis for each of them shows the same time intervals for reflecting depreciation in the balance sheet, and the theory also recommends using the same calculation methods. If there is such a coincidence, grouping of similar objects is allowed. The period of operation of the facility depends on:

- from the time interval planned by the company for using the facility;

- from the number of production units, similar, planned to be received during the operation of the facility.

Correspondence of account 02 with other accounting accounts

| Account 02 by debit | Account 02 on loan |

| 01 Fixed assets 02 Depreciation 03 Profitable investments in material assets 79 On-farm calculations 83 Additional capital | 02 Depreciation 08 Investments in non-current assets 20 Main production 23 Auxiliary production 25 General production expenses 26 General business expenses 29 Servicing production and facilities 44 Selling expenses 79 On-farm settlements 83 Additional capital 91 Other income and expenses 97 Deferred expenses |

Standard operations on account 02

Any company has fixed assets - its own or leased. Therefore, almost everyone uses 02 account. There are typical accounting entries that occur most often.

| Wiring | The essence of the operation |

| Dt 02-1 Kt 02-2 | The amounts of depreciation of leased fixed assets that became property are reflected |

| Dt 02 Kt 01 | Depreciation accrued during use is written off |

| Dt 02 Kt 83 | Reduced depreciation as a result of markdown |

| Dt 02 Kt 79 | Reduced depreciation on fixed assets transferred to OP on a separate balance sheet |

| Dt 20 (25, 23, 26, 44, 91) Kt 02 | Accrued depreciation on fixed assets |

| Dt 79 Kt 02 | Depreciation was accrued for fixed assets of a separate division |

| Dt 83 Kt 02 | Increased depreciation as a result of revaluation of fixed assets |

| Dt 91 Kt 02 | Depreciation accrued by the lessor organization on leased fixed assets |

Use the cloud service Kontur.Accounting to automate the calculation and calculation of depreciation. Keep records, submit reports, pay salaries and calculate sick leave - 14 days free for all new users.