The balance sheet is a basic element of the annual reporting of legal entities. For individual entrepreneurs, the obligation to draw it up is not provided. Individual entrepreneurs are exempt from the need to register under Article 6 of Law 400-FZ of December 6, 2011. However, many businessmen use forms for internal control purposes. Summarized financial information allows you to evaluate the profitability of projects and the effectiveness of decisions. Balance Sheet Structure

The legislative basis for economic accounting in small businesses is represented mainly by federal acts. The list of key documents includes:

- Law No. 402-FZ of December 6, 2011;

- recommendations of the Ministry of Finance of Russia No. 64-dated December 21, 1998;

- Order of the Ministry of Finance of the Russian Federation No. 86n dated August 13, 2002;

- letter of the Ministry of Finance of the Russian Federation No. P3-3/2015 dated 06/03/2015.

The regulations answer the question of what a balance sheet is and also provide detailed instructions for its preparation. Recommendations are addressed to legal entities. However, learning the general principles will ensure successful financial management of a business.

The balance sheet for individual entrepreneurs is a comprehensive analysis of resources and liabilities. There is no need to hand it over anywhere. The structure of the document will be standard. The report includes two sections of equal value.

| Assets | Liabilities |

| An entrepreneur should include in this category the cost of fixed assets, taking into account depreciation (depreciation), inventories, materials, money in the cash register and in the current account, balances of payments under copyright agreements, patents, and accounts receivable. The official definition of assets is given in paragraph 7.2 of the Accounting Concept. The document was approved by the Presidential Council and the Council of the Ministry of Finance of Russia on December 29, 1997. The key characteristics are the presence of control, and the real possibility of making a profit in the future | The composition of this part of the balance sheet will be determined by the specifics of individual entrepreneurship. Individual entrepreneurs do not have an authorized capital. The category of liabilities includes accounts payable, obligations under loan agreements, and other debts. The group should include all sources of business financing |

Annual form for individual entrepreneurs and LLCs on the simplified tax system: what balance to submit for 2019

Taxpayers submit:

- a regular 3-page report with numerous appendices;

- or simplified on 2 pages with explanations if necessary (for example, to clarify the degree of materiality of indicators and other clarifications).

Depending on the type of activity of the organization and the accounting accounts used: if rare accounts are used that are not in the short form of the report, then it is recommended to use the full version. For companies engaged in such common activities as trade, transportation or construction, the lightweight version of the form reflects the results of financial activities quite fully.

Objectives of its delivery

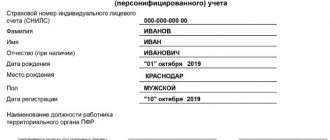

Registration number in the Pension Fund of the Russian Federation for individual entrepreneurs - how to find out and why it is needed

It is necessary to understand that the balance sheet is one of the basic elements of annual reporting used by legal entities. There are no mandatory conditions for use for individual entrepreneurs. Moreover, according to federal legislation, they are completely exempt from the need to register.

Despite this, most individual entrepreneurs use the form in question for the purpose of maintaining internal control. Thanks to this financial information, the individual entrepreneur has the opportunity to:

- evaluate the profitability of previously developed and already used projects - perhaps some of them will need to be closed or modified in order to increase income levels, issue bonuses to employees for successful development, etc.;

- analyze the effectiveness of management decisions made - as a rule, this is manifested in total annual income. Based on the results of the data obtained, you can assess your strengths, for example, when making a decision to purchase a home with a mortgage.

The Tax Code of the Russian Federation determines the goals and objectives of the balance sheet

When figuring out whether individual entrepreneurs submit their balance sheet or not, it is worth saying that submitting the document is advisable when using the general taxation regime. In fact, for individual entrepreneurs, reporting is considered a comprehensive analysis of available resources and assigned obligations. Surrender is not required under federal law.

How to make a simplified balance sheet for the simplified tax system for 2019: form and recommendations

First you need to close the accounting reporting period. To balance the balance, accounts 90, 91 and 99 are closed on December 31 of the reporting year - this is called reformation. If you use a simplified balance sheet on the simplified tax system, this procedure is the same as for a regular one. The necessary transactions are presented in the table; an example of filling out a statement of financial results based on these transactions is shown in Fig. 2. For such entities, subaccounts for value added tax and excise taxes (90-3, 90-4, 91-3) are irrelevant.

Table. Postings during the reformation.

| Debit | Credit | Amount, thousand rubles | Note |

| 90-1 | 90-9 | 125 | Account 90 reformed (closed) |

| 90-9 | 90-2 | 90 | |

| 91-1 | 91-9 | 5 | Account 91 is closed |

| 91-9 | 91-2 | 0 | |

| 99 | 84 | 40 | Account 99 is closed with a profit (in the example the organization is profitable) |

| 84 | 99 | -10 | This is how account 99 is closed with a loss |

Simplified Accounting: Example of a 2021 Income Statement.

Before drawing up a balance sheet under the simplified tax system in 2020, take a ready-made form. Data can be entered into forms manually, on a computer, or automatically through an accounting program.

The balance under the simplified tax system for 2021 had to be submitted on March 31st. In 2020, the date does not fall on a weekend; it must be submitted by 03/31/2020. Simplified companies do not report quarterly, and the full balance sheet form is submitted only for the year.

Financial statements must be submitted to the Federal Tax Service. For some organizations, accounting data is public, in particular for non-profit organizations, and they are required to be published in a printed publication. But most ordinary organizations are not subject to this requirement.

Results

Drawing up a full-fledged balance sheet for individual entrepreneurs is impossible. A businessman’s property is inextricably linked with personal obligations. Moreover, for married entrepreneurs, part of the assets will belong to the spouse. This circumstance will significantly complicate the procedure.

Private businessmen do not pay for authorized capital, do not purchase shares, and do not distribute profits. They do not have to pay dividends. The traditional form of annual reporting for individual entrepreneurs is irrelevant. Even when applying the general regime, you do not need to submit your balance to regulatory authorities.

The only option is to keep simplified records. Such forms allow you to analyze financial results, as well as monitor compliance with the restrictions provided for by tax legislation.

Form_Accounting_Balance Sheet

An example of filling out a balance under the simplified tax system for 2021

The information on the first two pages of the new simplified financial statements for 2021 should contain all information about the organization and summary accounting data.

"Descriptive" pages of financial statements

Drawing up a balance sheet under the simplified tax system for 2021 implies only 5 types of assets and 6 types of liabilities. Passive accounts have been detailed compared to the previous form. Two added items - “targeted funds” and “fund of real estate and especially valuable movable property” - are necessary to detail the organization’s assets. In them, indicate data on targeted funds aimed at major repairs, modernization of fixed assets or innovation. In addition, many organizations will be required to record the value of real estate or vehicles on their balance sheet.

Please note: the line code corresponds to the account that has the greatest share of it. For example, an enterprise has intangible assets worth 100,000 rubles. (code 1110) and financial investments of 50,000 rubles. (code 1170). In the report, in the line “Intangible, financial and other non-current assets”, code 1110 is indicated, but the total amount is entered - 150,000 rubles. - on both counts.

A company's income is shown on its income statement. It is filled out together with a simplified balance sheet. It is known as Form 2, Profit and Loss Statement.

About accounting under different tax regimes

It is advisable for entrepreneurs using the general taxation system to keep full records and draw up a balance sheet. Under the simplified tax system, such a need arises in the event of a stable increase in the value of fixed assets. The right to apply a special regime remains with the owners of assets with a valuation of up to 150 million rubles (Article 346.12 of the Tax Code of the Russian Federation). The Russian Ministry of Finance announced the extension of the norm to individual entrepreneurs in letter No. 03-11-11/55403 dated August 29, 2017. This means that “simplifiers” are obliged to control the value of property.

Businessmen can keep records on UTII in order to prevent theft and analyze profitability. The specifics of the mode will not have a special impact on the order of data processing. As a basis, you can take samples of balance sheets of business companies that have switched to UTII.

Payments to the Social Insurance Fund

The entrepreneur is required to submit a report in Form 4-FSS. The formula for calculation will look like this: amount to be accrued at the beginning of the year and until the end of the current month * 2.9 percent.

There are two ways to report to the Social Insurance Fund - paper and electronic. At the same time, if you employ more than 25 people, then the report is accepted only in electronic format.

The rules for reporting deadlines are:

- For the 1st quarter - until April 20 in paper form and until April 25 in electronic form.

- For the 1st and 2nd - until July 20 and 25, respectively.

- For 9 months of work - until October 20 and 25.

- For the whole year - until January 20 and 25.

Payments for reporting are transferred until the 15th of the next month.

Employee tax for individual entrepreneurs

The requirements for an individual entrepreneur who has become an employer are such that he is forced to pay a portion of the entire amount of funds paid to his employees (under an employment or civil law contract) to the treasury.

The calculation of this tax is calculated according to the following principle: (employee’s income for the month minus tax deductions) * tax rate.

2-NDFL is issued separately for all individual entrepreneurs. The 2-NDFL declaration must be submitted before April 1 of the reporting period.

The payer will have to transfer the withheld personal income tax before the day following the payday. In the case of personal income tax on sick leave, benefits and vacation pay, payment of these components is due until the last day of the month. 3 percent is paid for persons with Russian citizenship and 30 percent for foreign persons.

Reports on OSNO

Personal income tax

Personal income tax refers to the income that was received after the sale of property.

Personal income tax is calculated based on income for the tax period. From this amount, deductions must first be made. In the case of OSNO, the costs of commercial activities are subtracted from there. The tax rate is 13 percent. In cases where deductions are actually greater than profits, the tax is equal to zero.

The declaration document for this type of tax must be submitted to the main system before April 30th. The reporting form is filled out according to form 3-NDFL.

4-NDFL is used to calculate advance payments. Those who have just started work must be handed over within five days after the month in which the first profit was received. For those who have been working for a long time - together with 3-NDFL. Refers to those investors whose profits for the current year and the previous year differ by more than twice.

When to pay personal income tax:

- 1st payment – until July 15

- 2nd – until October 15

- 3rd – until January 15

The final one, which takes into account those paid earlier - until July 15

VAT

A lot of things apply to VAT. This includes the sale of goods and the provision of various types of services. This is simply a transfer of rights to property or goods (in the case where expenses on them are not included in profit). This is performing work for your own needs, and even importing. VAT is paid in cases where an individual entrepreneur generates an invoice in which this tax is allocated after a completed transaction is not recorded as taxable.

The tax rate is 18 percent. For some individual entrepreneurs - 10% (in certain categories of goods; details are specified in Decree of the Government of the Russian Federation No. 597 of June 18, 2012).

For those who export goods, the rate = zero.

The first step is to calculate “VAT for crediting”. To calculate this figure, the following calculation formulas are used:

In the case of a rate of 18 percent, the amount of income including VAT is divided by 118 and multiplied by 18.

In the case of a bet of 10 - on 110 and 10, respectively.

Then you need to get “VAT creditable” - from the received amount of expenses we find 18 or 10 percent.

Then we get “VAT payable to the budget.” This is the relationship between “VAT accrued” minus “VAT credited”. If the total amount is negative, then you are entitled to a refund from budget funds.

VAT reporting is submitted once every three months, but no later than the 25th day of the month following the reporting quarter. These are April 25, July, October and January.

Payment of VAT is calculated as follows: take the accrual figure for 3 months, divide by exactly three. Then, in the next three months of the next quarterly reporting period, we pay one amount each (also until the twenty-fifth).

Property tax for individuals

Will be superimposed on the price of inventory property owned by an individual. No reporting is required for this fee. And for those who own real estate, the FSN itself sends notification letters. Must be paid by December 1st.

Types of reports for individual entrepreneurs

Fiscal reports

Once a year or once every three months, such a report is submitted by those entrepreneurs who operate within the framework of the simplified tax system, unified agricultural tax and UTII regimes. OSNO - naturally too, since they generally file all declarations. But it’s easier for patent holders; they don’t have to report to the tax authorities in the form of fiscal declarations.

Additional reports

This type of declaration includes a kind of data such as the average headcount. You can read more about this type of reporting on our website in a separate article.

Reports to extra-budgetary funds

The funds include the Pension Fund, the Social Insurance Fund and the Compulsory Medical Insurance Fund. Most individual entrepreneurs, especially those who are employers and enter into employment contracts with employees, need to submit documents there.

Reports to Rosstat

They are needed so that the government body can conduct research and understand the business environment in Russia. It is usually taken from those whose business is larger and is of greater interest in terms of data volume. The statistics department itself decides who needs to submit the report.

We’ll talk more about each type of reporting and related papers later. In the meantime, it would be useful to remind you that the most important thing in submitting reports is not to miss deadlines. Violations are strictly suppressed with fines and freezing of current accounts.

Unified agricultural tax

Entrepreneurs registered with the Unified Agricultural Tax submit a declaration once a year by March 31. Tax payment is made twice a year: by transferring an advance payment for the 1st half of the year and the final tax calculation by March 31.

Important : maintaining KUDiR is mandatory.

| Report | Periodicity | Due dates | Notes | Submit IP | ||

| With staff | no employees | |||||

| Declaration on Unified Agricultural Tax | annual | until March 31st | Form according to KND 1151059 | V | V | |

| Wed. payroll | annual | until January 20 | V | |||

| 2 – personal income tax | annual | until April 1 | V | |||

| RSV-2 in the Pension Fund of Russia | annual | until March 31 | Provided to the Pension Fund and the Compulsory Medical Insurance Fund by heads of peasant farms that do not have staff. | V | ||

If there are taxable objects, other local taxes are paid. If there are obligations to Rosprirodnadzor due to the type of activity, then you will need to calculate and transfer fees for harmful effects on the environment. The deadlines for paying local taxes are set by the regions, but all of them must be calculated quarterly and transferred to the Federal Tax Service.

When submitting a declaration under the Unified Agricultural Tax to the Federal Tax Service, no supporting documents need to be attached to it.

Legislation on record keeping

On December 6, 2011, a special law “On Accounting” No. 402-FZ came into force. Subparagraph 4 of paragraph 1 of Article 2 of this law determines that its effect also applies to entrepreneurs. That is, individual entrepreneurs are required to keep accounting records. However, Article 6 of this law clarifies: the obligation does not arise if income and/or expenses or necessary physical indicators are taken into account in accordance with the law.

What does it mean? We explain: if an entrepreneur does not fill out books of income and expenses (KUDIR), which are required to be maintained by the chosen taxation system, he must organize full-fledged accounting for all documents.

Video: Important changes in simplification since 2015

It should be noted that all reporting (tax and funds), which, in addition to the declaration, must be submitted to an individual entrepreneur who has a staff of employees, regarding the number of staff, its income, benefits paid and contributions transferred, is relevant for any type of taxation.

Addition: we draw your attention to the fact that for individual entrepreneurs who are on the simplified tax system and who have chosen “income” as the taxable base, they submit similar reports as under the simplified tax system, income minus expenses.