Intangible assets (intangible assets) of an enterprise are considered to be property objects operated by the copyright holder for a long time (more than a year), contributing to the generation of profit (economic benefit), which do not have a physical embodiment (material expression).

Intangible assets of an organization belong to the category of non-current assets and, as is known, require proper accounting.

Such objects are often products of intellectual activity or, alternatively, means of unambiguous individualization of their copyright holder.

Such assets appear in a company as a result of purposeful actions of an interested party to create, transfer/receive or acquire them.

The main feature of all these activities is that the enterprise has an exclusive right to the beneficial use of the corresponding intangible asset.

In order to reliably determine (clarify) the presence of intangible assets, their condition and the degree of obsolescence, it is necessary to regularly conduct an inventory (audit, verification) of the relevant assets in the company.

It is important for specialized specialists to know what such an inventory is, how often it should be carried out, in what order it is carried out, what documents are used to document its results, and how its accounting is carried out.

The specifics of appropriate accounting actions based on the results of an inventory carried out for certain intangible assets are determined by the result that was obtained - full compliance with accounting information or identification of a shortage/surplus.

It should be noted, however, that some aspects of the conduct and execution of such an audit are specifically regulated by regulatory requirements that are generally binding.

The essence of the object

So, intangible assets are the commercial values of the company. Accordingly, they are aimed purely at obtaining benefits. Otherwise, they are not recognized as such; they also do not have a material form, they are immaterial. But they belong to the company legally. This can be either full copyright, which in fact should be equated to ownership, or use by proxy for a temporary period with restrictions. This category refers to that part of the property that is not involved in turnover. After all, their sale occurs not just once, but constantly during the period that they are owned. Receiving benefits multiple times is the main goal. Therefore, accounting is carried out as an inventory of the non-current assets of the enterprise.

But even though they do not have a material form, they are still subject to accounting, the results of which are stored in special documents. Of course, it is impossible to verify the actual availability by regular reconciliation. After all, they don’t exist in the physical world. But it is permissible to identify the documentary basis for their use, the correctness of execution, the correctness of reception or transmission, the possibility of implementation within a certain period of time and in a specific geographical area.

Moreover, often the number of such objects can even exceed the rest; accordingly, verification becomes a lengthy procedure. And it is extremely difficult to carry out it without the appropriate knowledge, as well as suitable software.

Business Solutions

- shops clothing, shoes, groceries, toys, cosmetics, appliances Read more

- warehouses

material, in-production, sales and transport organizations Read more

- marking

tobacco, shoes, consumer goods, medicines Read more

- production

meat, procurement, machining, assembly and installation Read more

- rfid

radio frequency identification of inventory items More details

- egais

automation of accounting operations with alcoholic beverages Read more

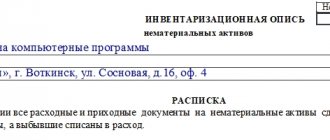

Inventory list of intangible assets

In order to begin the process, it is first necessary to understand what falls into our field of vision.

And this:

- Copyright. It is generally accepted that these include only various achievements in the field of culture and art. Works of art, paintings, illustrations, musical fragments or video sequences. But the list turns out to be much wider. This should include programs, various models, plans, strategies, algorithms and much more. And the specificity from cultural easily develops into scientific.

- Patents. These rights relate to inventions. That is, some kind of device, mechanism, form, graphical shell and much more. The key difference is that in this case it is not the specific result itself, for example, a scientific article. But only a principle that is further used only by those whose action is permitted by law.

- Slogans, names, trademarks, brands and similar. The main value is in the commercial component. And also in associations that people assign to a certain name.

- The reputation of the project, infringement of which is punishable under the current legislation of the Russian Federation.

And these are just simple objects. These include those whose use is permitted on the basis of a separate document. But if one paper makes it possible to implement a mass of patents at once, these are already complex. Which also fall under the inventory.

In addition to those listed, the verified documents also include certificates of state registration and licenses. It all depends on what needs to be legalized.

Purpose and rules

In fact, the inventory of fixed assets and intangible assets is an audit, but it has its own personal characteristics and rules. Which it is better to adhere to in order to carry out the procedure as correctly as possible.

As you know, this method is the best way to control the safety of property. Constantly examine whether all title documents are in order. Enter them into the database, note their presence, and record that their service life has not yet expired. But all actions are performed according to the following rules.

- A certain frequency is established. The number of inventories is the competence of the founders and management; arbitrary is acceptable. But this is if we talk about optional events. But the audit should definitely be carried out at least once a year, before closing the annual reporting. And also in cases where the employees responsible for security left their positions and other persons took their place. The same principle works when changing the organizational structure of a company: reorganization, merger or even liquidation. Especially if the cessation of activity occurs against the backdrop of accumulated debts, not to mention bankruptcy. When detecting theft, it is also necessary to carry out an event for reliability.

- The implementation falls on the shoulders of a special commission. It must include certain links, representatives of accounting, management, experts and other employees. The appointment of the composition is carried out by the director or his authorized deputy. This is the only way to take inventory of non-financial intangible assets; for example, an assistant manager, an accountant, an appraiser, a loader and, inevitably, a storekeeper. Or another person who bears personal responsibility for the safety of the values being studied.

- Even before the start of the action, the commission receives all the papers that record the acceptance, distribution or transfer of objects. To be aware of the state of affairs, to know what to compare with.

- The final result is strictly recorded in duplicate. And this does not happen at the end of the entire event, but at the end of the working day. Even if everything resumes in the morning. The reporting is certified by all those present. The storekeeper also signs, as a supervisory authority that verified the legality and absence of criminal intent during the event. After all, he has financial obligations in case of loss.

- If there are discrepancies in any plan, a special statement is drawn up. It, like the title order, the results of the inventory of intangible assets for each working day, constitutes a complete reporting package.

Regulatory regulation

From the point of view of the law, the main regulator is the order of the Russian Ministry of Finance. It was established back in 1995 at number 49. It reflects the very fact of the need for reconciliation and puts forward basic definitions of key concepts. But the specific procedure and conditions are not regulated. They were changed already in 2007. Again, by the Ministry of Finance, but in PBU (accounting regulations).

Any deviations from the norms specified in the law indicate a violation. And the results obtained are not considered true, and it is unacceptable to refer to them. If a violation of an essential condition has been identified, the procedure must be repeated.

How is it carried out?

The procedure for conducting the inventory is important; intangible assets identified as a result will have to be checked again if there is a violation of the regulations. Therefore, we will pay close attention to it.

Initiation occurs by implementing an order in a special form. This is INV-22. But it does not work in all cases. It, in fact, forms a new commission that will solve the task. But if all the required members already exist as usual and are constantly engaged in this matter, then another order is activated. This is INV-23.

The procedure also applies to storekeepers or other responsible persons. In addition to direct supervision, they also create their own small reports. Or rather, they fill out receipts. The fact that a specific object was registered was revealed during the inspection. Or written off at the end of its operational life. And besides this, they enter all the details of the papers that were handed over to the members of the commission for review. And they strictly note their return to storage.

By the way, if previously the responsible persons were given funds for the purchase of certain goods, both tangible and intangible, and reporting on sales was not carried out, this is also noted.

It is noteworthy that the commission also has an additional goal: deciding whether the things being checked are these intangible assets. Do they meet all the requirements, categories, and conditions specified in the order of the Ministry of Finance? And if something does not fit the description, a corresponding entry is made about it. And he himself is excluded from view during the procedure.

Reflection of inventory results in accounting.

As noted above, as a result of the inventory, surpluses, shortages of property, facts of non-compliance of property with the criteria for recognizing it as an asset, losses from impairment of assets or their reduction may be identified.

The basis for recording records based on inventory results in accounting are properly executed statements of discrepancies based on inventory results (form 0504092), acts on inventory results (form 0504835) and other documents substantiating the relevant facts of economic life.

If documents based on the results of an inventory carried out for the purpose of drawing up annual financial statements are signed after the reporting date, the inventory results are included in the annual reporting indicators based on the provisions of the institution’s accounting policy on the procedure for reflecting events after the reporting date.

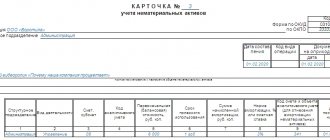

Inventory of intangible assets, documentation of intangible assets

The main final document is the statement. It is formed strictly according to the INV-1A model. And although it is often led by only one person, all members of the commission must confirm the fact of their participation and agreement with the indicated results. And the responsible persons, of course, including.

But, as we have already clarified, there is also a second statement, a comparison statement. It is not always initiated, but only in cases where there are discrepancies. Unaccounted for values or, on the contrary, the absence of such when they are noted on papers. Its form sounds like INV-18.

All results obtained are sent to the accounting department. What is noteworthy is that now, or rather, since 2013, the requirement for strict compliance with the form has been abolished. Of course, in many companies the surplus of intangible assets (INA) identified during the inventory and their reflection is also shown in the matching statement INV-18. But with amendments, companies have the right to develop their own personal form. And act on it, marking documents in your own way. Of course, if the variation does not in any way contradict the legal norms established by the Ministry of Finance. Otherwise, such a form will be excluded and not taken into account.

It’s easier to adapt your own form to automated verification. Which is ten times superior to manual in both speed and quality. , offers various software solutions. They will make the procedure an easy task. With the help of mobile applications adapted to all amendments of the Ministry of Finance, reconciliation is much easier, and recording a report does not require a lot of fiddling with papers and studying reports.

Pre-Inventory Activities

Inventory is carried out by permanent or one-time commissions. The composition is organized from members and a chairman with a total number of at least 3 people. An order is issued on the start of the inventory in form No. INV-22. For permanent commissions when conducting mandatory inventories, issuing an order is not a mandatory condition for starting an inspection. The order is registered in the accounting book INV-23.

Persons responsible for accounting and storage of assets must take part in the audit of intangible assets . Persons provide receipts included in inspection documents. The document confirms the fact:

- Transfers for the audit of documents used during the acceptance, movement and disposal of intangible assets.

- Capitalization of all assets at the disposal of persons.

- Write-offs of intangible assets by disposal dates.

If there are accountable amounts issued to responsible persons for the acquisition of intangible assets, the report for which has not been submitted to the accounting department, you will also need to draw up a receipt regarding their availability.

Business Solutions

- the shops

clothes, shoes, products, toys, cosmetics, appliances Read more

- warehouses

material, in-production, sales and transport organizations Read more

- marking

tobacco, shoes, consumer goods, medicines Read more

- production

meat, procurement, machining, assembly and installation Read more

- rfid

radio frequency identification of inventory items More details

- egais

automation of accounting operations with alcoholic beverages Read more

Surpluses and disadvantages

For clarity, we will show what the final table looks like. After all, checking the accounting of the results of the inventory of intangible assets is an important part, which is mandatory before the commission members add their signatures.

| Action | D-t | Kit |

| Accounting for surplus | 05 | 92 |

| Written off depreciation due to surplus valuables | 06 | 05 |

| Write-off with value terms | 93 | 05 |

| Transferred to the repayment account at the expense of the financial responsible person | 70 | 93 |

| Difference from the market price and the potential balance when written off at the expense of the financial responsible person | 72 | 73 |

| The amount of potential income after the compensation is realized | 70 | 72 |

| Total losses based on findings | 98 | 95 |

What is a concept

The accounting information for intangible assets, verified and confirmed by the corresponding inventory, is used by the accountants of the copyright holder enterprise.

Based on the information, annual financial statements and all interim balance sheets are compiled.

Periodic checking of the presence and condition of such assets helps to monitor their safety and increase the efficiency (profitability) of their practical use.

The inventory of certain intangible assets may result in one of the following results:

- The results of the audit performed completely coincide with the accounting data.

- Identification of assets not recorded in accounting at the start date of the audit. The detected intangible material is included in the inventory list and registered.

- Damage, loss, and other force majeure circumstances determined the absence of intangible assets, which, however, were registered by the copyright holder enterprise. The fact that there is no documentary justification for the intangible asset is recorded in the inventory act indicating the guilty party.

As a rule, an inventory of existing intangible assets is assigned for individual situations (cases), prompting the company's management to check the actual status of these assets on a certain date.

What is checked during the process, inventory object of intangible assets

As we have already clarified above, the main task is the reconciliation of documents. But at the same time, it is not just the availability of the necessary paper that is calculated. There are a lot of factors that the commission pays attention to.

First of all, the place of application is studied. Everything is permissible for use only in a certain area. Of course, sometimes the entire Russian Federation is a territory. But often this location is much narrower.

Attention is also drawn to the correctness of the design. If an error was made in the preliminary records, for example, about capitalization, then now the assessment is not made as such. After all, there was no receipt. First you need to correct the mistake.

Next, each object is checked for compliance with the definition of intangible assets, focusing on legal norms in the form of orders of the Ministry of Finance. And only if the value, in principle, fits the given definition, the title documentation is checked.

The depreciation period is determined, as well as the permissible maximum period of use.

How often to initiate the procedure

As we have already clarified, it is necessary to carry out this once a year, when changing the organizational structure or when replacing the person responsible for storage. The rest depends specifically on the organization and the amount of valuables in the property. For small volumes and constant use, it is, in principle, permissible not to carry out additional measures. But if the quantitative factor goes off scale, then it is better to issue a corresponding order at least once every 3 months. And if there is an opportunity and free employees, then even more often.

Postings

This is done with the following wiring:

- Dt04/Kt91 – acceptance of the surplus discovered during the audit into accounting as non-operating income.

- Dt94/Kt04 – write-off of the shortage in intangible assets at the expense of the culprit at the residual value.

- Dt91/Kt94 – write-off if the culprit is not found (as non-operating expenses).

- Dt99/Kt91 – write-off to the loss account.

- Dt05/Kt04 – writing off depreciation from undetected intangible assets.

This video will tell you about such an inventory:

conclusions

To summarize, this process is extremely important for almost any commercial project. After all, there is not a single person who does not use such intangible assets to at least some extent.

The main thing is to understand that not only knowing how to conduct an inventory of intangible assets will allow you to obtain effective results. But also the appropriate software, which will also simplify the task. And for exclusive offers developed specifically for the needs of a specific company, you should contact us. Cleverence software will always help you solve a problem faster, easier and more productively.

Here you can download the necessary documentation layouts.

Number of impressions: 3133

Posting of discovered intangible assets

Warehouse – Inventory – Receipt of goods – Create.

Directory element Other income and expenses .

Checking the reflection of income from the capitalization of intangible assets in accounting and accounting records.

Did the article help?

Get another secret bonus and full access to the BukhExpert8 help system for 14 days free of charge