In any commercial organization, inventories are periodically carried out in order to check the availability of its assets and assess their actual condition.

Intangible assets (intangible assets) of an enterprise are also regularly subject to such an audit. As a rule, the inventory of intangible assets is accompanied by the proper filling out of a special document - an inventory list, often compiled according to the INV-1a form.

Intangible assets

Intangible assets include various inventions, trademarks, computer programs, any production secrets, etc.

The document that established the rules for accounting for intangible assets is PBU 14/2007. It was approved by Order of the Ministry of Finance of Russia dated December 27, 2007 No. 153n. It is this PBU that needs to be used when working with an organization’s intangible assets.

When conducting an inventory, intangible assets are checked in accordance with Order of the Ministry of Finance dated June 13, 1995 No. 49:

- whether intangible assets were reflected correctly and on time on the company’s balance sheet;

- does the company have documents that can confirm that it has the rights to use intangible assets.

INV-1a: sample filling

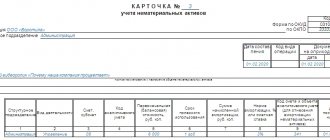

The procedure for entering information into the inventory form based on the results of checking the organization’s intangible assets begins with indicating the details of the enterprise and listing the objects that are registered. The list must include all those objects whose presence needs to be checked, linking them to their locations. The document must contain information about the actual location of its storage next to each asset.

INV-1a on the second page contains a tabular part. It is filled out by the participants of the inventory commission. The names of assets are entered into the columns of the table block. For each object the date of commissioning is given. The completed form must reflect the purpose of the intangible asset and the documentation serving as the basis for acquiring the rights to use a specific object (registration certificate or other official document).

At the next stage of registration of INV-1a (an example of filling can be seen below), you must:

- indicate the date on which the company was registered;

- based on the available primary documents, enter information in lines 7 and 8 (they contain data on the valuation of the assets being inspected, which must match the primary documents and accounting registers);

- accounting data and actual availability, the total amount are recorded.

INV-1, sample filling

Is it necessary to work with the INV-1a form?

The INV-1a form was developed and approved by the State Statistics Committee of Russia, by resolution No. 88 of August 18, 1998. Until the beginning of 2013, the form was mandatory for use, after which it became only recommended. That is, to conduct an inventory of intangible assets, a company today can use a document developed independently for its own convenience based on INV-1a. However, in this case, management must remember that the unified form cannot be completely changed: the mandatory details must always be on the document, otherwise the inspection authorities will doubt its authenticity.

Not all companies enjoy the right to develop their own forms. For some, it is more convenient to use INV-1a, since this is a familiar form for many experienced workers, and in this case, the inspection authorities will not have questions about these documents.

For your information! The choice of certain forms must be recorded by the company's management in its accounting policies.

When is it drawn up in relation to intangible assets?

Form INV-1a is intended for accounting for intangible assets during the next audit of the company.

Accordingly, its completion is carried out by authorized specialists of the organization if an inventory of assets of this category is carried out.

Such an inspection can be regulated (to prepare a balance sheet for the year) or unscheduled (for example, when preparing an enterprise or its property for sale).

If previously commercial structures were required to use this form without fail, now (since 2013) enterprises are allowed to develop and use their own forms for inventory accounting of non-current assets.

Commission

A special commission is always appointed to conduct any inventory. It may include an accountant, lawyer, administration employees, department heads, and specialists. The composition must be approved by the head of the company (Order of the Ministry of Finance of the Russian Federation dated June 13, 1995 No. 49).

Financially responsible persons are not included in the commission, since the inventory checks their work. The commission is created on an ongoing basis. The number of people is not limited, but usually it is 3-4 employees.

INV-1 form and content

The official INV-1 form is not required for use just like other unified inventory forms. A company or entrepreneur can develop their own forms and use them to conduct property inventories. However, companies often prefer to use the official form. Therefore, let's take a closer look at it.

Below we have placed the INV-1 form, which you can download for free.

1732 downloads

We have also prepared for you a sample of filling out INV-1. Please note that the inventory must be made in at least 2 copies (the first for the accounting department, the second for the employee bearing financial responsibility). For leased property, a third copy of the inventory is drawn up for each lessor.

How to correctly fill out the INV-1a form

The form consists of three pages. Let's talk in detail about each of them.

First page

Here you need to enter information such as:

- Name of the company, enterprise and structural unit. The name must be the same as in all other documents.

- OKPO code.

- Activity code.

- Details of the document (number and date of preparation) on the basis of which the inventory is carried out. This is an order, decree or direction. As a rule, there is an order.

- Start and end dates of the inventory procedure.

- Type of operation (not always filled in).

- Number and date of compilation of the completed inventory.

- List of intangible assets that are subject to inventory.

- Their location. Here it is noted in which structural unit the intangible assets are located.

This is followed by a receipt stating that all intangible assets have been sent to the accounting department, and the intangible assets themselves have been accounted for or written off. The employees responsible for storing papers on the company’s right to intangible assets put their signatures.

Second page

There is a table on this page. The following data is entered into it:

- Number in order.

- Intangible asset name, function and brief description.

- A document confirming its registration, with details such as name, date of preparation and number.

- Date of registration with the company.

- Actual cost according to primary data.

- Cost according to accounting data.

At the end of the table, the total value of all assets is summarized. Then they summarize the page: indicate the number of serial numbers in the table and the actual amount. These entries must be made in words.

Attention! If the organization has a lot of intangible assets, then you can add the required number of pages to the form. Then each of them will need to be summarized at the end.

Third page

First of all, sum up the overall inventory. Then the chairman and members of the commission put their signatures, after which the persons responsible for the safety of documents on the right to intangible assets sign that all intangible assets were checked in their presence and there are no claims against the commission.

At the end, the accountant signs that he has checked all the calculations in this inventory.

If, based on the results of the inventory, discrepancies were identified between accounting and actual data, then fill out a matching statement in the INV-18 form.

Inventory list of intangible assets: structure and filling procedure

The INV-1a inventory is compiled in two copies. The first copy is taken by the accounting department, and the second by the person responsible for the safety of documents that confirm the company’s rights to use intangible assets. You can fill out the form on the computer or by hand. Each form is signed by the responsible persons of the inventory commission and the person responsible for documents on intangible assets. Keep the inventories for 5 years.

The inventory includes three pages. Let's analyze the filling of each.

Keep records of exports and imports in the Kontur.Accounting web service. Simple accounting, payroll and reporting in one service

First page: company information and receipt

On the first page, indicate the name of the company and the structural division for which the inventory is being carried out. The name of the organization must match what is indicated in the constituent documents.

In the tabular part on the right, indicate the OKPO and OKVED codes. Next, fill in the information about the document that became the basis for starting the inventory. This could be an order, instruction or resolution - cross out unnecessary options. Also enter the start and end dates of the inventory procedure.

In the next block, indicate the inventory list number and the date it was completed. List the intangible assets that are subject to inventory and their location.

Even before the start of the inventory, the persons responsible for storing documents on intangible assets fill out a receipt with their data on the first page. So they confirm that all expenditure and receipt documents for intangible assets have been transferred to the accounting department, and all necessary assets have been capitalized or written off.

Second page: inventory data

The second page provides data on the inventory results. The tabular part is filled out by members of the inventory commission.

In the second column of the table, enter the name of the intangible asset and its brief description. Next, for each object, indicate information about registration documents - name, number and date. The date of registration of the asset is indicated in a separate column 6.

Columns 7 and 8 provide data on the value of the asset. It must coincide with the data in primary documents and accounting registers.

If the commission finds an intangible asset that is not registered, it is also included in the inventory. At the same time, dashes are entered in columns 6 and 8, and the total amounts according to the accounting data and the primary documents do not coincide.

Following the table are the page totals: how many assets have been inventoried and for what amount. If the organization has more than 15 intangible assets, then the second page is printed in several copies and a summary is made for each.

What is important to remember

- The inventory can be filled out either by hand or on the computer. In the first case there should be no blots.

- The document is drawn up in 2 copies. The first is transferred to the accounting department, and the second remains with the employee who is responsible for the safety of documents for the right to intangible assets.

- If a factual error is found in the document, it is corrected by notifying all persons involved in the inventory. Incorrect information is crossed out and the correct option is written on top. All participants in the procedure put their signatures.

- Inventory records must be stored in the organization for 5 years.

conclusions

Form INV-1a is one of the options for compiling an inventory list intended to document the results of the audit of intangible assets.

Business entities have the right to choose - either to develop their own accounting form or to use this form.

This document is filled out and signed in the prescribed manner by members of the audit (inventory) commission. In addition, the paper is signed by financially responsible entities.

The information specified in this inventory is used for comparison (reconciliation) and accounting procedures performed by the accounting department of the copyright holder organization.

Inventory list of intangible assets INV-1a

The company's intangible assets, like any other property, are subject to periodic inventory. It is mandatory to check once a year at the end of December before reporting; an inventory of intangible assets can also be carried out in other cases during the year.

The reason for this may be, for example, a change in the person responsible for intangible assets.

To carry out an inventory of intangible assets, an order is drawn up; the unified form INV-1a can be used. The order is transmitted to the members of the inventory commission, the composition of which is precisely appointed by the order.

The commission is preparing for the inspection, the responsible persons are convinced of the correct accounting of all intangible assets, and the transfer of documents to the accounting department. An inventory list is being prepared in the INV-1a form, in which members of the commission will record information about actual data.

This data is taken from the primary documentation accompanying the receipt of the intangible asset.

When organizing accounting at an enterprise using specialized computer programs, INV-1a inventories are prepared on their basis, with lines filled in based on the accounting data, after which the inventories are transferred to members of the commission for entering documentary information.

https://www.youtube.com/watch?v=bFX4yFF5SqU

After carrying out the preparatory activities, members of the inventory commission proceed directly to the inventory - reviewing the documentation for intangible assets and reflecting information from the documents in the inventory list INV-1a.

The inventory list of intangible assets INV-1a and a sample of filling can be found at the bottom of the article in Excel format.

Sample of filling out INV-1a

In the intangible asset inventory form, you need to fill out the title page, table, summarize the results for each sheet with the table and the inventory as a whole, and then certify the reflected information with your signatures on the last sheet of the INV-1a form.

Materially responsible persons (MRPs) must be present during the inventory; their inclusion in the inventory commission is not allowed.

MOLs must also reflect their signatures in the INV-1a inventory. On the title page, the MOL signs in the “receipt” section, which confirms the readiness of the assets for inventory. On the last sheet of the inventory, the MOL puts a signature as a sign of agreement with the actions of the members of the inventory commission and the results obtained.

Next, a signed copy of the inventory list INV-1a is transferred to the accounting department, which is carried out on top of accounting and documentary information, identified inconsistencies are transferred to the matching sheet INV-18, the form and sample of which can be downloaded here.

The inventory table provides a list of all intangible assets available in the organization according to the primary documentation; for each asset the following is written:

- name, characteristics in brief;

- information about the document from which data on intangible assets is taken;

- the day the intangible asset is accepted for accounting;

- its ruble value according to documentary data;

- The cost according to the accounting data is filled in by the accountant.

Inventory list INV-1a

When conducting an inventory, it is necessary to reflect the data on the inspection carried out in a special form of the unified form INV-1a - an inventory list designed to reflect indicators specifically for intangible assets.

For the inventory of fixed assets, you need to fill out an inventory of another form - INV-1; the form and sample for filling out this inventory list can be found here.

Members of a special commission created are appointed responsible for the formation of inventories. The surname composition of the inventory commission, as well as the timing and procedure for conducting an inventory of intangible assets (INA) are fixed in the order of the head (download order INV-22).

The need for an inventory of intangible assets usually arises at the end of the year before the preparation of annual reports, and a mandatory reason for this procedure is a change in the financially responsible person. In other cases, inventory is carried out at the request of the company itself.

The results of the inventory must be documented. Initially, inventory lists with actual indicators are filled out; at this stage, members of the commission sign the inventory and transfer it to the accounting department.

The accountant carries out further processing of the document, recording information from accounting registers next to the actual data. Next, the actual and accounting indicators are reconciled, the identified discrepancies are transferred to the comparison sheet, and the INV-18 statement form is filled out for fixed assets and intangible assets.

At the end of the year, the accountant summarizes the results of all inventories carried out during the year for all the company’s facilities, the summary data is entered into the INV-26 statement.

In this article we also offer a sample of filling out the inventory list of intangible assets, form INV-1a. Free download links are at the bottom of the article.

Sample of filling out INV-1a

The following information is entered into the INV-1 inventory form:

- name of the company and division;

- code of the main activity;

- details of the document approving the terms and composition of the commission members for conducting an inventory of intangible assets;

- the start and end date of the inventory - according to the order;

- number and day of compilation of the inventory;

- clarification of those intangible assets for which the inventory will be carried out;

- finding these assets;

- in the table in columns 1 to 7, data on the actual availability of intangible assets is entered (name of the asset, document on registration of the exclusive right to it (details), day of receipt of the intangible assets, actual cost (taken from the accompanying primary documentation);

- all intangible assets are entered into the table, if there is a large number of assets, additional sheets with the table are filled in, for each sheet the results are summarized about the specified number of items (the number of completed rows of the table of the INV-1a form) and the total actual amount, the final data are summed up for the entire table as a whole;

- signatures of the commission members.

On the first page of the INV-1a form there is a subsection called “receipt”, in which financially responsible persons put their signatures, thereby confirming that all intangible assets are available at the storage location, all documents on them have been transferred to the accounting department for recording information in accounting registers.

The MOL is also signed at the bottom of the form after the members of the inventory commission sign the INV-1a inventory upon completion, thereby agreeing with the data shown in the inventory inventory.

Next, the INV-1a inventory is transferred to the accounting department, where it undergoes further processing indicating accounting indicators, the accounting value for each item reflected in the inventory inventory is entered in the last eighth column of the INV-1a table.

The accountant signs at the bottom of the form, confirming the correctness of the inventory.

and form

Source: https://9blank.ru/inventarizacionnaya-opis-inv-1-2/