Entrepreneurs report profits and losses using a declaration. It also reflects income and expenses, benefits received (clause 1 of Article 80 of the Tax Code of the Russian Federation). Starting with annual reporting for 2021, organizations use the form introduced by Order of the Federal Tax Service of Russia dated October 19, 2016 No. ММВ-7-3 / [email protected] The electronic format of the report and the filling algorithm are also described here. In this article we will look at when monthly income tax reporting is required, who submits quarterly returns, and what fines are provided for failure to comply with these requirements.

The principle of determining deadlines

Organizations using the general taxation system submit income tax returns during the year based on the results of the reporting periods. The deadline for submitting such declarations depends on the method of payment of advance payments:

- organizations paying only quarterly advances, as well as organizations paying monthly advances with an additional payment based on the results of the quarter, submit income tax returns quarterly no later than the 28th day of the month following the reporting period (1st quarter, half-year, 9 months);

- organizations that pay monthly advances based on the actual profit received submit declarations monthly - no later than the 28th day of the month following the reporting month (clause 3 of Article 289 of the Tax Code of the Russian Federation).

The deadline for submitting a declaration based on the results of 2021 is the same for all payers - no later than March 28 of the year following the reporting year (clause 4 of Article 289 of the Tax Code of the Russian Federation). However, due to non-working days, quarantine and coronavirus, it was postponed to June 29, 2020.

Also see “ Deadlines for submitting all tax reports in 2021: table .”

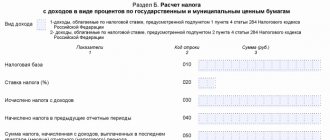

Tax agent reporting on profits

Russian organizations are recognized as tax agents for income tax if they pay:

- interest on state and municipal securities to Russian organizations and foreign organizations with permanent representative offices in the Russian Federation (clause 5 of Article 286 of the Tax Code of the Russian Federation);

- income to foreign organizations that have permanent representative offices in the Russian Federation, not related to the activities of such representative offices (clause 4 of Article 286, subclause 1 of clause 4 of Article 282, clause 6 of Article 282.1 of the Tax Code of the Russian Federation);

- individual income to foreign organizations that do not have permanent representative offices in the Russian Federation (clause 1 of Article 309, clause 1 of Article 310 of the Tax Code of the Russian Federation);

- dividends to other Russian organizations (clause 3 of Article 275 of the Tax Code of the Russian Federation) or foreign organizations with permanent representative offices in the Russian Federation (clause 3 of Article 275, clause 6 of Article 282.1 of the Tax Code of the Russian Federation).

For information on how dividends are reflected in the declaration, read the article “How to correctly calculate the tax on dividends?” .

Agents submit income tax calculations at the end of each reporting (tax) period in which they paid income (clauses 1, 3, 4 of Article 289, Article 285 of the Tax Code of the Russian Federation).

ConsultantPlus experts explained how to fill out and when to submit a profit-making declaration to a foreign organization. If you do not have access to the system, get trial online access and upgrade to the Ready Solution for free.

Income tax: deadline for filing returns 2019

The Federal Tax Service has approved a new form of income tax return, the procedure for filling it out and the format for submitting it in electronic form. They must be applied starting with reporting for 2021. Compared to the current form, the changes are minor. First of all, these are new barcodes. In addition, there is no longer a field on the title page where the OKVED code was indicated.

Note:

- New income tax return form for 2020

- Review of changes in income tax in 2021

Late submission of the declaration: the company’s responsibility

Organizations that fail to submit reports to the Federal Tax Service on time are subject to tax and administrative liability.

Specific tax measures are defined in Art. 119 of the Tax Code of the Russian Federation. Thus, if the annual declaration is not submitted to the tax authorities on time, the company may be subject to a fine of 5-30% of the unpaid tax amount indicated in the report for each month of delay (full and incomplete). The specific amount of the fine is determined individually for each taxpayer, but the minimum value of the fine is 1,000 rubles (even if the profit declaration is zero).

If an organization is late with delivery by more than 10 days, its current account may be blocked (Article of the Tax Code of the Russian Federation).

In addition to tax liability, in accordance with Art. 15.5 of the Code of Administrative Offenses of the Russian Federation, an administrative fine is applied to company officials, the amount of which will be 300-500 rubles.

Income tax: deadline for filing the declaration 2020 (table)

Based on the results of the reporting periods in 2021, organizations must submit declarations within the following deadlines:

| The period for which the income tax return is submitted | Deadline for submitting income tax returns |

| For organizations paying only quarterly advances, as well as for organizations paying monthly advances with an additional payment at the end of the quarter | |

| For the first quarter of 2021 | No later than 07/28/2020 (postponement due to coronavirus) |

| For the first half of 2021 | No later than July 28, 2020 |

| For 9 months of 2021 | No later than October 28, 2020 |

| For organizations paying monthly advances based on actual profits | |

| For January 2021 | No later than 02/28/2020 |

| For February 2021 | No later than 30.03.2020 |

| For March 2021 | No later than 07/28/2020 (postponement) |

| For April 2021 | No later than 08/28/2020 (postponement) |

| For May 2021 | No later than 09.28.2020 (postponement) |

| For June 2021 | No later than July 28, 2020 |

| For July 2021 | No later than 08/28/2020 |

| For August 2021 | No later than September 28, 2020 |

| For September 2021 | No later than October 28, 2020 |

| For October 2021 | No later than November 30, 2020 |

| For November 2021 | No later than 12/28/2020 |

Read also

08.10.2019

Sheet 2 and Appendices 4 and 5 to sheet 2 of the income tax return for 2021

For a number of organizations, codes have been set for the line “Taxpayer Attribute”.

- Code 15 – organizations that hold licenses to use subsoil plots and apply a reduced rate of income tax paid to the budget of a constituent entity of the Russian Federation.

- Code 16 – organizations that carry out activities in the production of liquefied natural gas and/or processing of hydrocarbons into goods.

- Code 17 – organizations that work in the field of information technology.

- Code 18 – organizations – residents of the Arctic zone of the Russian Federation.

- Code 19 – organizations carrying out activities in the design and development of electronic components and electronic (radio-electronic) products.

Reporting if there are two bases (average annual and cadastral value)

The amount of property tax can be calculated from two fundamentally different tax bases (Article 375 of the Tax Code of the Russian Federation):

- the average annual value of property that forms all fixed assets of a legal entity, with the exception of land, non-taxable objects and objects with a tax base in the form of cadastral value;

How to determine the residual value of an operating system, see here.

- cadastral value applied to real estate objects of a certain type (clause 1 of Article 378.2 of the Tax Code of the Russian Federation), which have undergone a cadastral assessment and are assigned as an object subject to taxation according to “cadastral” rules in the region (clauses 2 and 7 of Article 378.2 of the Tax Code of the Russian Federation) .

For which real estate properties property tax is calculated based on the cadastral value, find out here.

The tax periods for both bases are the same and equal to a year. The tax for the year for each of the bases should be calculated in full (clause 1 of Article 382 of the Tax Code of the Russian Federation), but the total amount payable will be determined taking into account advances accrued during the year (clause 2 of Article 382 of the Tax Code of the Russian Federation).

A ready-made solution from ConsultantPlus will help you calculate property tax and advances on it. Get trial access to the system for free and proceed to the material.

The declaration, despite the possibility of simultaneous presence of two different bases, is compiled into a single one, but the corresponding calculations are given in different sections:

- according to the average annual value of property for the year - in section 2;

- for cadastral value - in section 3, and the number of sheets in it is equal to the number of objects that have such a base.

Form – electronic only

All organizations that are required to submit annual accounting (financial) statements to GIBO submit a copy only in the form of an electronic document signed with an electronic signature (Part 5, Article 18 of the Federal Law of December 6, 2011 No. 402-FZ “On Accounting” ).

As of the 2021 report, this requirement also applies to small businesses. They could still submit reports for 2021 on paper, and only if they wished – in electronic form. Now representatives of SMEs are deprived of the right to choose in what form to present accounting (financial) statements. Electronic document only.

The declaration is submitted to the Federal Tax Service at the location of the taxable property.

A foreign organization that does not have a representative office in our country, but has real estate, can also have taxable property on the territory of the Russian Federation. In this case, the obligation to pay tax also arises. According to paragraph 4 of Art. 386 of the Tax Code of the Russian Federation, if a foreign legal entity has not submitted a declaration, the inspectorate independently assesses tax according to available data without additional control measures, and then compares the result obtained with the amount that the enterprise will pay. If the calculated tax exceeds the paid tax, arrears are detected.

A single tax on imputed income

UTII is a convenient special mode in which the amount of taxes does not depend on actual income. From January 1, 2021, UTII will be abolished, so you will no longer have to submit a declaration. But the report for the fourth quarter of 2021 has not been canceled, and it must be submitted in 2021.

Who is renting? Organizations and entrepreneurs who work for UTII.

Deadlines for delivery . You must report quarterly. The last UTII declaration for the fourth quarter of 2021 will need to be submitted by January 20, 2021. No other reports are expected in 2021.

Form and delivery format. The report can be submitted in paper or electronic form. The declaration form was approved by order of the Federal Tax Service dated June 26, 2018 No. ММВ-7-3/ [email protected]

Section 3

The section is completed in relation to property, the tax base for which is determined in accordance with its cadastral value.

Line 001 is filled out in accordance with Appendix No. 5 of the Filling Out Procedure. In our case, code “11”, which corresponds to real estate objects, the tax base for which is determined as the cadastral value

Line 002 is filled in similarly to line 002 from Section 2.

In line 014, you must indicate the property property attribute:

- “1” for property other than premises

- "2" for premises (for example, garage)

Line 015 is for the cadastral number of the property.

Section 3 (part 1)

Line 020 indicates the cadastral value of the property as of January 1 of the reporting period, including the non-taxable value on line 025 .

Line 030 is filled in if there is equity participation.

Line 035 is filled in if the cadastral value has not been established for the taxable object, but it is available for the building in which the object is located. In this case, the share of cost is determined.

Line 040 is filled in based on the codes from Appendix No. 6 to the Filling Procedure.

Line 050 displays the share of the cost of the object if it is located on the territory of several constituent entities of the Russian Federation.

In line 060 the value of the tax base is entered, which is defined as the difference between lines 020 and 025. If there are values other than zero on lines 030 and 050, then the resulting difference must be multiplied by these values.

If there are grounds for applying a reduced tax rate, then the relevant information must be reflected on line 070 .

Line 080 indicates the final tax rate taking into account available benefits.

Line 090 corresponds to a coefficient that is calculated provided that the property has been owned for less than a year (the ratio of the number of full months of ownership to the number of months in the tax period).

The coefficient on line 095 is indicated in the event of a change in the cadastral value due to a change in qualitative or quantitative characteristics and is calculated as the ratio of the number of full months in the tax period during which the cadastral value indicated in line 020 was in effect to the number of months in the tax period.

Line 100 indicates the tax amount, when calculating which you need to take into account the non-zero values of lines 090 and 095.

in line 130 , taking into account the tax benefits reflected in line 120 .

Section 3 (part 2)

Results

The deadline for submitting a property declaration for the year is indicated in the Tax Code of the Russian Federation as March 30 of the year following the reporting year. Failure to submit these reports on time will result in a fine. Payment deadlines vary by region, since the right to establish them is granted to regional authorities.

Sources:

- Tax Code of the Russian Federation

- Code of Administrative Violations of the Russian Federation

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

What does annual financial reporting include?

This type of reporting, on the one hand, is mandatory for submission, and on the other hand, financial statements are a source of reliable information about the economic activities of the company.

It is based on the data from this report that forecasts are made and various analytical studies are carried out. To understand what reports should be provided and within what time frame, we will pay some attention to the composition of the annual financial statements. Accounting statements consist of the following forms of documents:

Each of the presented forms has features and nuances when filling out, which must be taken into account when generating reports.