What counts as implementation?

Goods are considered sold if the ownership of them has passed from the seller to the buyer (Clause 1, Article 39 of the Tax Code of the Russian Federation).

For the purposes of calculating excise taxes, the following operations are considered to be sales:

- gratuitous transfer of ownership of excisable goods or the use of excisable goods with payment in kind (subclause 1, clause 1, article 182 of the Tax Code of the Russian Federation);

- shortage of excisable goods in excess of the norms of natural loss (clause 4 of article 195 of the Tax Code of the Russian Federation).

The procedure for confirming the right to apply a 0 percent tax rate

From 2021, the value added tax will increase. The standard tariff has been increased from 18 to 20%. Other duty levels remained the same.

:

- for objects exported through the free economic zone (clause 2, clause 1, article 164 of the Tax Code);

- for some types of rail and air transportation (clause 2. clause 1 of article 164 of the Tax Code);

- for goods transported through the free customs zone (clause 1, clause 1, article 164 of the Tax Code).

10%:

- for some food and medical products, as well as printed press and goods for children (clause 2 of article 164 of the Tax Code).

From January 1, 2021, the list of documents provided to confirm the right to receive a 0% preferential rate has been expanded. For goods sold in a free customs zone, the following must be submitted:

- confirmation of registration of residence in the territory of rapid socio-economic development (in the form of a certificate issued by the management company);

- confirmation of residence in the territory of the free port of Vladivostok (certificate issued by an authorized federal executive body);

- confirmation of participation in a free economic zone (certificate issued by a federal executive body authorized by the Government of the Russian Federation).

When to charge excise tax

When selling (transferring) excisable goods, accrue excise tax on the day of shipment (transfer) to the buyer (recipient) of the goods (clause 2 of Article 195 of the Tax Code of the Russian Federation, letter of the Ministry of Finance of Russia dated January 14, 2010 No. 03-07-06/03).

If an organization sells goods at retail, then the date of sale for the purposes of calculating excise taxes is the date of transfer of goods to the division that carries out retail sales (clause 2 of Article 195 of the Tax Code of the Russian Federation).

An exception is the case of the sale of goods pledged if they have been in the possession of the pledgee since the conclusion of the pledge agreement. In this case, excise tax can be charged only after a public auction. This is explained by the fact that when concluding a pledge agreement, goods are transferred to the pledgee not for the purpose of sale (Article 337 of the Civil Code of the Russian Federation).

If the obligation to pay excise duty is related to the discovery of a shortage of goods, the date of sale is the date the shortage was discovered. At the same time, excise tax is imposed on the quantity of missing goods that exceeds the norms of natural loss (clause 4 of Article 195 of the Tax Code of the Russian Federation).

For transactions of transfer of goods produced from customer-supplied raw materials, excise duty is charged on the date of signing the acceptance certificate for such goods (Clause 2 of Article 195 of the Tax Code of the Russian Federation).

Accrue excise tax on all transactions, the date of implementation (transfer) of which relates to the current month (clause 5 of Article 194, Article 192 of the Tax Code of the Russian Federation).

Situation: at what point should excise tax be charged when selling goods through an intermediary?

When selling goods under intermediary agreements, accrue excise tax at the time of transfer of goods to the intermediary.

It is explained this way.

When selling manufactured excisable goods, an object of excise taxation arises (subclause 1, clause 1, article 182 of the Tax Code of the Russian Federation).

The sale of goods is recognized as the transfer of ownership of goods (on a compensated or gratuitous basis) from one person to another (clause 1 of Article 39 of the Tax Code of the Russian Federation). That is, in general, the date of sale is considered to be the date of transfer of ownership.

At the same time, for the purposes of calculating excise taxes, the date of sale of excisable goods is defined as the day of their shipment (transfer) (clause 2 of Article 195 of the Tax Code of the Russian Federation).

Thus, if the terms of the agreement provide for the transfer of ownership, excise duty must be charged on the date of shipment of goods as part of the execution of such an agreement, regardless of the date of transfer of ownership or the date of payment. This conclusion is confirmed by the letter of the Ministry of Finance of Russia dated January 14, 2010 No. 03-07-06/03.

When selling goods through intermediaries, ownership of the goods remains with the manufacturer until they are sold by the intermediary (Clause 1, Article 996, Article 1011 of the Civil Code of the Russian Federation). However, they are transferred to an intermediary for the purpose of their sale, as a result of which ownership from the manufacturer will pass directly to the buyer. Therefore, based on the rules set out above, excise duty must be charged on the date of shipment of goods to the intermediary. Similar explanations are contained in the letter of the Ministry of Finance of Russia dated October 7, 2008 No. 03-07-06/87.

Excise and non-excise goods

The legislator recognizes the following as goods subject to excise tax:

- alcohols and products containing them;

- drinks containing alcohol;

- tobacco, products made from it, including those used by heating, liquid nicotine, electronic cigarettes;

- passenger cars and motorcycles;

- gasoline, diesel fuel, motor oils, aviation kerosene, middle distillates (for example, heating and marine fuels), crude oil;

- natural gas (in the context of international treaties of the Russian Federation);

- paraxylene, benzene, orthoxylene.

There are exceptions to the general rule. Thus, the following are not subject to excise taxes containing alcohol: medicines, veterinary preparations (if they are bottled in small containers, no more than 100 ml), perfumes and cosmetics (up to 90% inclusive of alcohol content, bottled in containers of 100 ml, there is a mechanism for spraying, if the percentage of alcohol up to 80, a spray bottle is not needed; or if the percentage of alcohol is up to 90, and the filling volume is up to 3 ml); alcohol production waste, wort, wine materials.

How are excise taxes paid on fuels and lubricants (diesel fuel, gasoline) ?

Alcoholic drinks containing more than 0.5% alcohol are taxed in the same way, with some exceptions. There is a government List of food products, which also includes goods with an alcohol content of more than 0.5%, and they are not subject to excise tax (document approved by Government Decree No. 1344 of 9/11/17). These, for example, include fermented drinks, kvass, spicy drinks up to 1.2% strength inclusive, fermented milk products (Article 181 of the Tax Code of the Russian Federation, List, approved post. No. 1344).

Excise tax rates

After determining the moment of accrual of excise duty, determine the excise tax rate on the sold (transferred) product. This is due to the fact that the procedure for determining the tax base depends on the type of tax rates established for various excisable goods.

Tax legislation provides for three types of excise tax rates:

- hard or specific - in rubles per unit of measurement of the volume of excisable goods sold (transferred);

- ad valorem - as a percentage of the price (cost) of sold (transferred) excisable goods;

- combined - simultaneously including both fixed and ad valorem tax rates.

Currently, only two types of tax rates apply:

- combined – established for cigarettes and cigarettes;

- solid or specific - established for other excisable goods.

This conclusion follows from the provisions of paragraph 2 of Article 187 and Article 193 of the Tax Code of the Russian Federation.

The excise tax rate is determined based on the provisions of Article 193 of the Tax Code of the Russian Federation.

Situation: at what rate should the excise tax be charged on the sale of carbonated wine products with a volume fraction of ethyl alcohol over 8.5 percent?

When selling carbonated wine products, charge excise tax at the rate established for sparkling (champagne) wines.

This is explained as follows.

According to the All-Russian Classification of Products (OKP), wine products with a volume fraction of ethyl alcohol over 8.5 percent are carbonated wine (OKP code 15.93.11.210). That is, wine with a volume fraction of ethyl alcohol from 8.5 to 12.5 percent, obtained by artificially saturating table wine material with carbon dioxide. In turn, carbonated wines (code 15.93.11.210) are included in group 15.93.11 “Sparkling and carbonated wines.” Even if carbonated wine products are made on the basis of fruit wines, they cannot be classified as fermented drinks (code 15.94.10).

For alcoholic products, the excise tax rates established in Article 193 of the Tax Code of the Russian Federation are applied. There is no separate excise tax rate for carbonated wines. However, based on the grouping of alcoholic beverages presented in the All-Russian Classification of Products, for the purpose of calculating excise taxes, carbonated wines should be classified as sparkling wines (champagne).

Thus, when selling carbonated wine products with a volume fraction of ethyl alcohol over 8.5 percent, apply an excise tax rate of 26 rubles. for 1 l.

General procedure for calculating the tax base

Once the excise tax rate has been determined, calculate the tax base for each type of excisable goods. Currently, for all excisable goods (except for cigarettes and cigarettes), the tax base is determined as the volume of sold (transferred) excisable goods in kind. In this case, the volume of excisable goods sold should be calculated in those units of measurement that are indicated in the excise tax rate.

This procedure follows from the provisions of Article 187 of the Tax Code of the Russian Federation.

If an organization sells goods of the same type, but with different excise tax rates, determine the tax base separately for each subtype of products sold (transferred), in relation to each rate (clause 1 of Article 190 of the Tax Code of the Russian Federation). To do this, it is necessary to maintain separate records (clause 2 of Article 190 of the Tax Code of the Russian Federation). If maintaining such records is impossible, tax all sold (transferred) products at a single tax rate. It must be determined based on the maximum excise tax rate provided for a given type of goods. This is stated in Article 190 of the Tax Code of the Russian Federation

An example of determining the tax base for excise duty when selling one type of product for which different tax rates are established

Alpha LLC produces beer of various strengths. Thus, Alpha’s assortment includes the following varieties:

- non-alcoholic beer (with a volume fraction of ethyl alcohol up to 0.5 percent);

- beer (with a volume fraction of ethyl alcohol from 0.5 to 8.6 percent);

- strong beer (with a volume fraction of ethyl alcohol over 8.6 percent).

Each of these three groups of beer has different excise tax rates.

If Alpha keeps separate records of beer transactions across these three groups, then to calculate the excise tax it must determine three tax bases and apply the appropriate rates to them.

If Alpha does not maintain separate accounting, it will have to determine a single tax base for beer. Then calculate the excise tax based on the maximum excise tax rate provided for beer (37 rubles per 1 liter).

An example of determining the tax base for the sale of excisable goods for which a fixed excise tax rate has been established

Alpha LLC produces beer. In July, the organization sold 500 bottles of beer (with an alcohol content of 0.5 to 8.6 percent by volume). Of the total number of beer bottles sold, 400 bottles were 0.5 liters and 100 bottles were 0.33 liters. The contractual cost of goods sold is 23,600 rubles. (including VAT - 3600 rubles, excise tax - 3495 rubles). The excise tax rate for beer with an alcohol content by volume from 0.5 to 8.6 percent is set at 20 rubles. for 1 l.

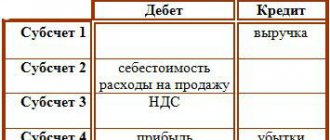

Alpha's accountant made the following entries in the accounting.

In July:

Debit 62 Credit 90-1 – 23,600 rubles. – revenue from beer sales is reflected;

Debit 90-3 Credit 68 subaccount “Calculations for VAT” – 3600 rubles. – VAT is charged on sales proceeds;

Debit 90-4 subaccount “Excise taxes” Credit 68 subaccount “Calculations for excise duties” - 4660 rubles. ((400 bottles × 0.5 l + 100 bottles × 0.33 l) × 20 rub./l) – excise tax is charged on the sale of beer.

Determination of the tax base when selling or receiving excisable goods

Excise taxes

Excise tax ( from the French accise) is one of the types of tax that represents an indirect tax on the sale of a certain type of consumer goods, not related to the receipt of income by the seller. Excise tax is included in the price of goods and withdrawn to the state and local budgets. Most often, excise tax (fee) is imposed on wine and vodka products, beer, tobacco products, delicacies, luxury goods, and cars. Excise tax payers are actually consumers purchasing goods that are subject to excise duty.

Excise tax , like value added tax, has been introduced in Russia since 1992. Currently, the procedure for taxation of excise taxes is regulated by the Tax Code of the Russian Federation (Part II Chapter 22).

The extent of excise taxes varies from country to country. For example, in Germany, about 20 types of goods are subject to excise tax, and in Japan - over 600. In general, excise taxes annually replenish the budgets of industrialized countries by 4-8%.

Excise tax payers

admit

1) organizations;

2) individual entrepreneurs;

3) persons recognized as taxpayers in connection with the movement of goods across the customs border of the Customs Union, determined in accordance with the customs legislation of the Customs Union and the legislation of the Russian Federation on customs affairs.

According to Art. 181 of the Tax Code of the Russian Federation the following are recognized as excisable goods:

1) ethyl alcohol from all types of raw materials;

1.1) cognac alcohol;

2) alcohol-containing products (solutions, emulsions, suspensions and other types of products in liquid form) with a volume fraction of ethyl alcohol of more than 9 percent, with the exception of alcoholic products specified in subparagraph 3 of this paragraph.

3) alcoholic products (drinking alcohol, vodka, liqueurs, cognacs, wine, beer, drinks made from beer, other drinks with a volume fraction of ethyl alcohol of more than 1.5 percent;

5) tobacco products;

6) passenger cars;

6.1) motorcycles with an engine power exceeding 112.5 kW (150 hp);

7) motor gasoline;

diesel fuel;

diesel fuel;

9) motor oils for diesel and (or) carburetor (injection) engines;

10) straight-run gasoline. For the purposes of this chapter, straight-run gasoline refers to gasoline fractions obtained from the refining of oil, gas condensate, associated petroleum gas, natural gas, oil shale, coal and other raw materials, as well as products of their processing, with the exception of motor gasoline and petrochemical products.

The following transactions are recognized as the object of taxation (Article 182 of the Tax Code of the Russian Federation):

1) sale on the territory of the Russian Federation by persons of excisable goods produced by them, including the sale of pledged items and the transfer of excisable goods under an agreement on the provision of compensation or novation.

6) sale by persons of confiscated and (or) ownerless excisable goods, excisable goods, which were refused in favor of the state and which are subject to circulation to the state and (or ) municipal property;

7) transfer on the territory of the Russian Federation by persons of excisable goods produced by them from customer-supplied raw materials (materials) to the owner of the specified raw materials (materials) or other persons, including receipt of the specified excisable goods into ownership in payment for services for the production of excisable goods from customer-supplied raw materials (materials) );

transfer within the structure of the organization of produced excisable goods for the further production of non-excise goods, with the exception of the transfer of produced straight-run gasoline for further production of petrochemical products within the structure of an organization that has a certificate of registration of a person carrying out transactions with straight-run gasoline, and (or) transfer of produced denatured ethyl alcohol for production of non-alcohol-containing products within the structure of an organization that has a certificate of registration of an organization performing operations with denatured ethyl alcohol;

9) transfer on the territory of the Russian Federation by persons of excisable goods produced by them for their own needs;

10) transfer on the territory of the Russian Federation by persons of excisable goods produced by them to the authorized (share) capital of organizations, mutual funds of cooperatives, as well as as a contribution under a simple partnership agreement (agreement on joint activities);

11) transfer on the territory of the Russian Federation by an organization (business company or partnership) of excisable goods produced by it to its participant (his legal successor or heir) upon his exit (departure) from the organization (business company or partnership), as well as the transfer of excisable goods produced within the framework of a simple partnership agreement (agreement on joint activities), to a participant (his legal successor or heir) of the specified agreement when allocating his share from the property that is in common ownership of the parties to the agreement, or the division of such property;

12) transfer of produced excisable goods for processing on a toll basis;

13) import of excisable goods into the territory of the Russian Federation and other territories under its jurisdiction;

20) receipt (receipt) of denatured ethyl alcohol by an organization that has a certificate for the production of non-alcohol-containing products.

For the purposes of this chapter, the receipt of denatured ethyl alcohol is the acquisition of denatured ethyl alcohol into ownership;

21) receipt of straight-run gasoline by an organization that has a certificate for processing straight-run gasoline.

22) transfer by one structural unit of an organization that is not an independent taxpayer to another similar structural unit of this organization of produced ethyl alcohol and (or) cognac alcohol for further production of alcoholic and (or) excisable alcohol-containing products, including transfer of produced raw ethyl alcohol for the production of rectified ethyl alcohol, which is subsequently used by the same organization for the production of alcoholic and (or) excisable alcohol-containing products (with the exception of alcohol-containing perfume and cosmetic products in metal aerosol packaging and (or) alcohol-containing household chemical products in metal aerosol packaging).

When an enterprise is reorganized, the rights and obligations to pay excise tax are transferred to its legal successor.

The tax base is determined separately for each type of product depending on the type of taxation rates.

For goods that are subject to specific rates, the tax base is the volume of excisable goods sold in physical terms.

For excisable goods subject to ad valorem rates (as a percentage of the product price), the tax base is established as the cost of sold excisable goods, calculated on the basis of market prices excluding VAT, excise tax and sales tax.

When selling excisable goods to the public, the tax amount is included in the price of the goods. At the same time, the corresponding amount of tax is not indicated on price tags issued by the seller, as well as on checks and other documents issued to the buyer.

The tax base is determined separately for each type of excisable product.

The tax base for the sale of excisable goods produced by a taxpayer, depending on the tax rates established for these goods, is determined:

· as the volume of excisable goods sold in physical terms - for excisable goods for which fixed (specific) tax rates are established (in absolute amount per unit of measurement);

· as the cost of sold excisable goods, calculated on the basis of prices determined taking into account the provisions of Article 40 of the Tax Code of the Russian Federation, excluding excise duty, value added tax and sales tax - for excisable goods for which ad valorem (in percentage) tax rates are established;

· as the value of transferred excisable goods, calculated on the basis of average sales prices in force in the previous tax period, and in their absence, based on market prices excluding excise tax, value added tax and sales tax - for excisable goods in respect of which ad valorem taxes are established (in percent) tax rates. In a similar manner, the tax base is determined for excisable goods, in respect of which ad valorem (in percentage) tax rates are established, when they are sold on a gratuitous basis, when carrying out commodity exchange (barter) transactions, as well as when transferring excisable goods under an agreement on the provision of compensation or novation and transfer of excisable goods with payment in kind.

When determining the tax base, the taxpayer's revenue received in foreign currency is recalculated into the currency of the Russian Federation at the rate of the Central Bank of the Russian Federation in effect on the date of sale of excisable goods.

Funds received by the taxpayer that are not related to the sale of excisable goods are not included in the tax base.

In relation to excisable goods for which different tax rates are established, the tax base is determined in relation to each tax rate.

If the taxpayer does not keep separate records, a single tax base is determined for all transactions of sale and receipt of excisable goods.

Tax rates

The following rates are established throughout Russia:

— ad valorem — as a percentage of the cost of goods at selling prices excluding excise tax.

- specific - in rubles and kopecks per unit of measurement of goods.

Specific rates prevail. Ad valorem rates are established for such types of goods as cigarettes (cigarettes).

The uniform rates valid throughout the Russian Federation are specified in Article 193 of the Tax Code of the Russian Federation.

In 2009, amendments to the Code were adopted, providing for annual indexation of excise tax rates in 2010-2012, taking into account the projected level of inflation. At the same time, excise tax rates on beer, tobacco products, and low-alcohol products were significantly increased. For the first time since 2005, excise tax rates on petroleum products were indexed.

Also in 2009, changes were made to the relevant chapter of the Code to prevent the use of various schemes for evading excise taxes on alcoholic products by limiting the right to tax deductions in the case of using alcohol-containing products instead of alcohol as raw materials in the production of strong alcohol.

Taxable period

The tax period is a calendar month.

Procedure for calculating excise tax

The amount of excise duty on excisable goods (including those imported into the territory of the Russian Federation), in respect of which fixed (specific) tax rates are established, is calculated as the product of the corresponding tax rate and the tax base.

The amount of excise duty on excisable goods (including those imported into the territory of the Russian Federation), in respect of which ad valorem (in percentage) tax rates are established, is calculated as the percentage share of the tax base corresponding to the tax rate.

The amount of excise duty on excisable goods (including those imported into the territory of the Russian Federation), in respect of which combined tax rates have been established (consisting of fixed (specific) and ad valorem (percentage) tax rates), is calculated as the amount obtained by adding the excise tax amounts , calculated as the product of a fixed (specific) tax rate and the volume of sold (transferred, imported) excisable goods in kind and as a percentage of the cost (customs value) of such goods corresponding to the ad valorem (in percentage) tax rate.

The amount of excise duty on excisable goods is calculated based on the results of each tax period in relation to all transactions for the sale of excisable goods, the date of sale (transfer) of which relates to the corresponding tax period, as well as taking into account all changes that increase or decrease the tax base in the corresponding tax period.

If the taxpayer does not keep separate records, the amount of excise duty on excisable goods is determined based on the maximum tax rate applied by the taxpayer from the single tax base determined for all excise-taxable transactions.

The date of sale of excisable goods is defined as the day of shipment (transfer) of the corresponding excisable goods.

When calculating the amount of excise tax payable to the budget, the taxpayer has the right to reduce the total amount of excise tax on excisable goods, determined in accordance with Article 194 of the Tax Code of the Russian Federation, by the tax deductions established by Article 200 of the Tax Code of the Russian Federation.

Amounts of excise tax calculated by the taxpayer upon the sale of excisable goods (except for sales on a gratuitous basis) and presented to the buyer are attributed to the taxpayer as expenses accepted for deduction when calculating corporate income tax.

Amounts of excise tax calculated by the taxpayer for transactions of transfer of excisable goods recognized as an object of taxation in accordance with the Tax Code of the Russian Federation, as well as when they are sold free of charge, are attributed to the taxpayer at the expense of the appropriate sources, from which expenses on these excisable goods are attributed.

The excise tax amounts charged by the taxpayer to the buyer when selling excisable goods are taken into account by the buyer in the cost of the purchased excisable goods.

The amounts of excise tax presented by the taxpayer to the owner of the toll raw materials (materials) are attributed by the owner of the toll raw materials (materials) to the cost of excisable goods produced from the specified raw materials (materials).

If operations with petroleum products recognized as an object of taxation are carried out by the taxpayer through its separate divisions located on the territory of one constituent entity of the Russian Federation and on the same territory as the head division, then in accordance with Article 204 of the Tax Code of the Russian Federation, the amount of excise tax can be paid by the taxpayer centrally at the location of the head office. divisions.

Procedure and deadlines for paying excise taxes

An enterprise carrying out operations for the sale of excisable goods determines the amount of tax based on the results of each tax period minus allowed tax deductions.

When selling (transferring) excisable goods, if the date of their sale (transfer) is determined as the day of payment, excise tax is paid based on the actual sales for the expired tax period no later than the 25th day of the month following the reporting month.

Payment of excise tax when carrying out transactions recognized as an object of taxation in relation to petroleum products is made no later than the 25th day of the month following the expired tax period, with the exception of:

Organizations that only have a wholesale sales certificate pay excise duty no later than the 25th day of the second month following the expired tax period.

Organizations that only have a retail sales certificate pay excise tax no later than the 10th day of the month following the expired tax period. The tax return is submitted to the tax authorities within the same time frame.

Payment of excise tax on the sale (transfer) of ethyl alcohol, alcohol-containing products, alcoholic products, beer, tobacco products, passenger cars and motorcycles with an engine power over 112.5 kW (150 hp) is made based on the actual sale (transfer) for the past tax period in equal shares:

- no later than the 25th day of the month following the reporting month and

- no later than the 15th day of the second month following the reporting month;

Payment of excise tax on the sale (transfer) of alcoholic beverages from excise warehouses of wholesale organizations is made based on the actual sale (transfer) for the expired tax period:

- no later than the 25th day of the reporting month (advance payment) - for alcoholic products sold from the 1st to the 15th day inclusive of the reporting month;

- no later than the 15th day of the month following the reporting month - for alcoholic products sold from the 16th to the last day of the reporting month.

The tax on excisable goods is paid at the place of production of such goods, and on alcoholic products - at the place of their sale from excise warehouses. The taxpayer is obliged to submit a tax return to the tax authority at the place of his registration as a taxpayer no later than the last day of the month following the reporting month.

When carrying out transactions with petroleum products, the payment of the tax amount is made by the taxpayer at the location of the taxpayer, as well as at the location of each of its separate divisions based on the share of the tax attributable to these separate divisions.

Excise taxes are one of the few levers of influence of the state on the economic processes taking place in society. Improving taxation in the field of excise taxes is one of the most important conditions for improving the economic situation and replenishing the federal and regional budgets.

Tax base for tobacco products

When selling cigarettes and cigarettes, the tax base consists of two parts and is defined as:

- the volume of goods sold (transferred) in kind – for the application of a fixed tax rate;

- the estimated value of these goods is for the application of the ad valorem tax rate.

This procedure is provided for in paragraph 2 of Article 187 and Article 193 of the Tax Code of the Russian Federation.

To determine the estimated cost of cigarettes or cigarettes, use the following formula:

| Estimated cost of goods sold (transferred) | = | Maximum retail price indicated on a pack of cigarettes or cigarettes | × | Number of cigarettes or cigarettes sold or transferred during the tax period (in packs) |

Minimum and maximum retail price

The organization does not have the right to sell tobacco products at a price below the minimum retail price and above the maximum (Clause 5, Article 13 of Law No. 15-FZ of February 23, 2013).

The maximum retail price is the price above which a pack of cigarettes or cigarettes cannot be sold to end consumers. This price must be indicated on the package. This is stated in paragraph 2 of Article 187.1 of the Tax Code of the Russian Federation.

The maximum retail price is set independently by the manufacturer for each brand (name) of cigarettes and cigarettes. Therefore, using the above formula, you need to determine the estimated cost for each brand (each name) of sold cigarettes or cigarettes. And then, if the excise tax rate on them is the same, add the resulting values to determine the final estimated cost. This follows from the provisions of Article 187 of the Tax Code of the Russian Federation.

Information from manufacturers on maximum retail prices for tobacco products is published on the official website of the Federal Tax Service of Russia.

The minimum retail price is 75 percent of the maximum retail price established by the manufacturer (clause 3 of article 13 of the Law of February 23, 2013 No. 15-FZ).

Situation: can an organization set different maximum retail prices for cigarettes of the same name? Cigarettes are sold in different regions, and the costs of their sale differ.

Yes, it can, if cigarettes of the same name, which are sold in different regions of Russia, are classified as different brands.

The maximum retail price, which must be indicated on a pack of cigarettes or cigarettes, is set by tobacco product manufacturers separately for each brand (clause 2 of Article 187.1 of the Tax Code of the Russian Federation). In this case, a brand is understood as an assortment position of tobacco products that differs from other brands in at least one of the following characteristics:

- Name;

- recipe;

- dimensions;

- presence or absence of a filter;

- package.

For example, cigarettes intended for sale in the Far North may differ from cigarettes of the same name sold in other regions in the color of the packaging. Changing packaging gives manufacturers the right to classify cigarettes of the same name as different brands. As a result, set different maximum retail prices for them.

Similar explanations are contained in the letter of the Ministry of Finance of Russia dated January 20, 2009 No. 03-07-06/4.

Attention: for the sale of cigarettes and cigarettes at a price exceeding the maximum retail price indicated on each package (pack), administrative liability is provided:

- for officials – a fine of 50,000 rubles. or disqualification for up to three years;

- for legal entities - a fine of two times the amount of excess revenue received as a result of the sale of cigarettes or cigarettes at a price higher than that indicated on the pack. Excess revenue received is determined for the entire period of sale of such goods, but not more than for 1 year (Part 1 of Article 14.6 of the Code of Administrative Offenses of the Russian Federation).

Investment tax deduction

From January 1, 2021, the list of organizations that can qualify for an investment deduction has been expanded (Article 286.1 of the Tax Code of the Russian Federation):

- organizations are allowed to reduce their income tax by the amount of donations made to state and municipal institutions operating in the field of culture . The benefit also includes transfers from non-profit organizations aimed at generating endowment capital to support cultural institutions. The maximum deduction amount is 100% (clause 3, clause 2, article 286.1 of the Tax Code of the Russian Federation);

- the right to apply the deduction and the procedure for receiving it is established by the subject of the Russian Federation independently (clause 6 of Article 286.1 of the Tax Code of the Russian Federation).

Registration of minimum and maximum prices

To establish the minimum and maximum retail prices, the manufacturer must submit to the tax office at the place of registration (customs authority at the place of declaration) a notification of the minimum and maximum retail prices for tobacco products.

The notification form for tax inspectorates (in relation to tobacco products produced in Russia), as well as the electronic format and procedure for filling out the form, were approved by Order of the Federal Tax Service of Russia dated March 28, 2014 No. ММВ-7-3/120.

The notification form for customs (for imported tobacco products) is not currently approved.

The notification must be submitted no later than 10 calendar days before the start of the tax period, starting from which the maximum retail prices indicated in the notification will be applied to the packaging.

The organization has the right to change the maximum retail price of cigarettes or cigarettes. To do this, you need to submit a new notification. The maximum retail prices indicated therein must be indicated on packs from the first day of the month following the date of submission of the notification, but not earlier than the expiration of the minimum validity period of the previous notification.

If an organization, by the beginning of the month from which new maximum retail prices are applied to packs, has unsold balances of cigarettes, then a situation may arise when tobacco products of the same name with different maximum retail prices are sold during the tax period. In such a case, the estimated value is determined in relation to each maximum retail price. Then the total estimated cost of sold cigarettes or cigarettes of this brand is determined.

This procedure follows from the provisions of Article 187.1 of the Tax Code of the Russian Federation.

Tax period for excise taxes

The tax period for excise taxes is recognized as only 30 days of one month for almost all taxpayers. Companies operating in three product categories enjoy a special deadline for paying excise duty:

- processing straight-run gasoline, denatured alcohol and middle distillate. Make the payment by the 25th day of the third month of the next tax period;

- selling middle distillates to foreign companies in the Russian Federation. The payment deadline is the 25th day of the sixth month of the next tax period;

- selling middle distillates outside the country to foreign organizations. Also, until the 25th of the sixth month.

The remaining companies submit financial declarations and pay excise taxes by the 25th of the next month. Having submitted the report on February 25, payment must be made by March 25. The procedure is repeated monthly. For failure to comply with the deadlines of the tax period, the violator will face penalties.

Organizations that produce strong alcoholic drinks pay excise tax in two stages. First, for the volume of raw materials from which they plan to produce alcohol. An advance excise tax is paid for it until the 15th day of the month in which these drinks will be sold. And the final payment is made to the budget before the 25th of the next month.

Become an author

Become an expert

Estimated cost of tobacco products

An example of determining the estimated cost of cigarettes sold. During the tax period, two brands of cigarettes were sold

Alpha LLC produces filter cigarettes of two brands: Balkan and Zvezda.

In July, the organization sold cigarettes of both brands in the following quantities:

- “Balkan” brand – 75,000 cigarettes (3,750 packs);

- “Zvezda” brand – 37,000 cigarettes (1,850 packs).

Packs of Balkan cigarettes sold in July had a maximum retail price of 50 rubles. On packs of Zvezda brand cigarettes – 55 rubles.

To calculate the excise tax, Alpha's accountant determined the estimated cost for each brand of cigarettes sold in July:

- “Balkan” – 3750 packs × 50 rubles. = 187,500 rub.;

- “Star” – 1850 packs × 55 rubles. = 101,750 rub.

There is one excise tax rate for all filter cigarettes. Therefore, the accountant calculated the total estimated cost of filter cigarettes sold in July: RUB 187,500. + 101,750 rub. = 289,250 rub.

An example of determining the estimated cost of cigarettes sold. During the tax period, cigarettes of the same brand were sold with different maximum retail prices

Alpha LLC produces filter cigarettes of one brand. In August, the organization sold 100,000 filter cigarettes (5,000 packs).

From August 1, based on the notice on produced packs of cigarettes, Alpha indicates the maximum retail price of 60 rubles.

During August, Alfa sold both cigarettes produced in August and cigarettes produced in July. In July, Alpha indicated on cigarette packs the maximum retail price of 57 rubles.

The number of cigarettes sold in April that were produced in July is 20,000 pieces (1,000 packs).

The estimated cost of cigarettes with a maximum retail price of 57 rubles. is: – 57 rub. × 1000 packs = 57,000 rub.

The number of cigarettes that were both produced and sold in August was 80,000 pieces (4,000 packs). Their estimated cost is: – 60 rubles. × 4000 packs = 240,000 rub.

Thus, the estimated cost of cigarettes sold by Alfa in August is: - 57,000 rubles. + 240,000 rub. = 297,000 rub.

General procedure for calculating excise tax

Once the tax base is determined, calculate the amount of excise tax.

When selling (transferring) excisable goods for which a fixed rate is established, calculate the excise tax using the formula:

| Excise tax amount (fixed rate) | = | Volume of goods sold (in units of measurement specified in the excise tax rate) | × | Excise tax rate per unit of excise tax measurement |

This procedure is provided for in paragraph 1 of Article 194 of the Tax Code of the Russian Federation.

An example of excise tax calculation for the sale of excisable goods for which fixed excise tax rates are established

Alpha LLC is engaged in the production of alcoholic beverages with a volume fraction of ethyl alcohol of more than 9 percent.

The excise tax rate for alcoholic products with a volume fraction of ethyl alcohol of more than 9 percent is set at 500 rubles. for 1 liter of anhydrous ethyl alcohol contained in excisable goods.

In June, Alpha purchased 200 liters of anhydrous ethyl alcohol for use in production at a cost of 11,800 rubles. (including VAT - 1800 rubles) Previously (in May), the organization transferred to the budget an advance payment of excise tax for purchased alcohol (clause 6 of Article 204 of the Tax Code of the Russian Federation). The amount of the advance payment was 100,000 rubles. (200 l × 500 rubles) (paragraph 5, paragraph 8, article 194 of the Tax Code of the Russian Federation).

Alpha uses the purchased alcohol to produce liqueur with a volume fraction of ethyl alcohol of 14 percent. In June, Alpha produced 2,000 0.7-liter bottles of liqueur. The volume of alcohol used was: 2000 bottles. × 0.7 l × 14% = 196 l.

In July, the finished products were fully sold. The contract price of goods sold is 180,000 rubles. (including VAT - 18% and excise tax).

When calculating the excise tax, the Alpha accountant does not rely on the volume of alcoholic beverages sold, but on the amount of anhydrous ethyl alcohol contained in it.

The amount of excise tax for July will be equal to: 2000 bottles. × 0.7 l × 14% × 500 rub./l = 98,000 rub.

Alpha's accountant made the following entries in accounting (transactions related to the production of finished products are not considered).

In May:

Debit 68 subaccount “Calculations for advance payments of excise duty” Credit 51 – 100,000 rubles. – advance payment of excise tax is transferred (before purchasing alcohol).

In June:

Debit 10 Credit 60 – 10,000 rub. – alcohol is credited;

Debit 19 Credit 60 – 1800 rub. – VAT presented by the alcohol supplier is reflected;

Debit 68 subaccount “Calculations for VAT” Credit 19 – 1800 rub. – accepted for deduction of VAT on alcohol.

In July:

Debit 62 Credit 90-1 – 180,000 rub. – revenue from the sale of liquor is reflected;

Debit 90-3 Credit 68 subaccount “VAT calculations” – 27,457.63 rubles. (RUB 180,000 × 18/118) – VAT is charged on sales proceeds;

Debit 90-4 subaccount “Excise taxes” Credit 68 subaccount “Calculations for excise taxes” - 98,000 rubles. – excise tax is charged on the sale of liquor;

Debit 68 subaccount “Calculations for excise taxes” Credit 68 subaccount “Calculations for advance payments of excise taxes” - 98,000 rubles. – advance payment of excise tax is credited.

The amount of the advance payment of excise tax on alcohol within the amount of excise tax accrued on sold products is accepted by Alpha for deduction (clause 16 of Article 200 of the Tax Code of the Russian Federation). Since the advance payment exceeds the amount of excise tax accrued upon sale, at the end of July Alfa does not pay excise tax to the budget.

The remaining part of the advance payment of excise tax, not accepted for deduction in July (2,000 rubles = 100,000 rubles - 98,000 rubles), will be accepted by the Alpha accountant for deduction in subsequent tax periods in which the purchased ethyl alcohol will be used for the production of liquor - vodka products with a volume fraction of ethyl alcohol of more than 9 percent.

Excise taxes in the tax system of the Russian Federation

Excise tax is levied on organizations and entrepreneurs working with certain types of goods under the Tax Code of the Russian Federation, including when moving across the border (customs) with member countries of the Eurasian Economic Union.

What are the excise tax deductions for wine products ?

Classification characteristics of excise tax:

- federal tax (according to government and management level);

- payment of legal entities and individual entrepreneurs (according to their affiliation with the entities paying it);

- non-targeted payment (funds received from excise taxes are not used to finance strictly defined projects or activities);

- indirect tax (using the withdrawal method);

- non-salary tax calculated and paid by the payer himself (according to the method of taxation);

- a regulatory tax credited to the federal treasury and regional budgets (according to the fullness of use rights).

The purpose of applying the excise tax, in addition to the general one inherent in all taxes - filling the budget, is to regulate, with the help of this premium to the price, the demand for the goods most in demand by the consumer.

How are excise taxes on beer ?