The inclusion of enterprise expenses in the calculation of taxable amounts should be carried out on the basis of economic feasibility. At the same time, not a single legislative act contains a clear concept of justification for expenses. The criterion is evaluative in nature, which gives rise to a number of questions and controversial situations during tax audits. The article will tell you how to avoid economically unjustified expenses and claims from fiscal authorities.

Question: Is the counterparty’s absence of expenses characteristic of its type of activity (including general business expenses) a sign that the taxpayer has received an unjustified tax benefit under VAT (Article 54.1, clauses 1, 2 of Article 171 of the Tax Code of the Russian Federation)? View answer

What expenses are unreasonable?

According to Art. 252 of the Tax Code of the Russian Federation, the following expenses can be included in tax calculations:

- economically justified;

- documented;

- expressed in monetary terms.

The norms of this article are related to the norms of Art. 346.16 of the Tax Code of the Russian Federation, therefore, the criteria apply to both calculations for income tax and simplified tax.

Question: Is it possible to deduct VAT if income tax expenses are economically unjustified (clauses 1, 2, Article 171 of the Tax Code of the Russian Federation)? View answer

In practice, it follows from the above that the Federal Tax Service has the right not to recognize certain expenses as economically justified, despite the absence of strict prohibitions in the legislation on the inclusion of certain types of expenses in calculations:

- Costs, according to the law, that are not related to the economic activity carried out by the taxpayer.

- Costs of paying for the services of consultants, auditors, lawyers, advertising agencies without detailing the work performed and the use of this work in business activities.

- Material costs not provided for by production technology or used in excess of technological standards.

- Inventory and materials (works, services) purchased at prices above average market prices for similar product items.

- Inventory materials used in the production of products that are subsequently sold at prices below the cost of inventory materials. The same applies to works and services.

- Costs that are not associated with the organization's receipt of income or with the intention of receiving it.

- Expenses incurred outside the scope of activities aimed at generating income, not having the purpose of generating income (reducing losses), and inflated compared to standard indicators are not considered economically justified.

How are economically unjustified expenses made for the purpose of tax evasion identified?

Important! The taxpayer is obliged to structure his document flow in such a way that it is clear from concluded contracts, primary documents, accounting registers, supporting and reference documents which goods, works and services were subsequently included in the tax calculation and for what purpose certain costs were incurred. When checking, the Federal Tax Service will, first of all, pay attention to their connection with business activities.

Cost write-off act

The act in question is intended to certify the fact that the PR was committed by authorized persons. Most often, they are members of a special commission from among representatives of the company that carried out the PR.

The relevant act may contain:

- date, name of the document (for example, “Act for writing off expenses as part of a business breakfast”);

- a list of commission members certifying the fact that the company has committed PR;

- a list of expense items indicating the actual amounts corresponding to them, which are confirmed by the commission (this block may be identical to that reflected in the previous document - the report);

- the total amount of actual expenses for the event, which is confirmed by the commission - similarly as in the report;

- the commission’s conclusion on the validity of the expenses in the specified list;

- the conclusion of the commission on the write-off of the relevant expenses as expenses of the category that is determined within the framework of accounting (most often these are “other expenses” in accordance with clause 8 of PBU 10/99).

- Full names, positions of commission members, their signatures.

How to identify and minimize unreasonable expenses

Identifying unreasonable expenses of an organization is a priority goal of its management. Timely measures will help not only to avoid problems during tax audits, but also to discover internal reserves that allow you to generate more income and save resources. As a rule, they start with an internal audit, during which a continuous or selective method is used to check whether the costs correspond to:

- production technology, the nature of economic activity in essence;

- standards established by internal documents of the organization or the legislation of the Russian Federation (norms for writing off fuel and lubricants, travel expenses, production costs based on internal calculations of the economic service, etc.);

- criterion of economic feasibility.

Supporting and other documents are checked, reflecting costs, correctness of execution, availability of necessary details (to avoid claims during inspections, etc.).

Before signing an agreement with a counterparty that involves expenses, it is necessary to calculate its economic consequences. Based on the data received, the manager makes a decision whether to consider future costs justified or not. Thus, if the Federal Tax Service refuses to refund a large amount of VAT, then engaging a professional consultant with a fee significantly lower than the disputed amount will be economically justified. At the same time, conducting marketing surveys of potential consumers, if the company does not have problems with selling products, cannot be called justified, since their economic benefits cannot be assessed.

As a rule, it is not possible to completely avoid economically unjustified expenses, even in the part limited by the articles of the Tax Code of the Russian Federation.

Internal limits on such expenses should be established and compliance with them should be monitored:

- travel expenses, travel taking into account the status and categories of employees;

- entertainment expenses, similar to the previous paragraph;

- expenses for gifts for holidays and anniversaries;

- expenses of cultural events.

Estimate

This document, used to confirm the PR, may contain:

- a block reflecting the fact of approval of the document by the director;

- date of document preparation;

- name of the document (for example, “Estimate of entertainment expenses for a business breakfast”);

- information about the planned location of the event;

- data on the planned number of event participants in one status or another (organizers, invitees, representatives of the company, its partners);

- a list of PR items indicating the corresponding planned amounts;

- the total amount of expected PR within the event;

- Full name and signature of the chief accountant of the company;

- Full name, position of the head of the company and his signature.

Justification of expenses and tax control

When carrying out tax audits, employees of the Federal Tax Service are often guided by the principle that the taxpayer is required to prove the validity of expenses. In doing so, they refer to Art. 64 of the Arbitration Procedural Code of the Russian Federation, provisions of the Tax Code of the Russian Federation, justifying my opinion as follows:

- Based on the norms of the Tax Code, the taxpayer forms the tax base independently;

- Based on the rules of the APC, the taxpayer is not relieved of the obligation to prove his claims with facts that form the basis of the claims.

However, such a position is at least controversial, and essentially incorrect. In the same APC Art. 200-5 directly contains an indication of the obligation of the Federal Tax Service to provide evidence of the unreasonableness of the organization’s expenses.

Important! If there is a suspicion of artificially inflated prices, tax authorities use Art. 40-3 Tax Code of the Russian Federation. The established standard is no more than 20% deviation from market prices for similar items of goods, works, and services. The rate of entertainment expenses is no more than 4% of labor costs during the year (Article 264-2 of the Tax Code of the Russian Federation).

Cash expenditure report

The corresponding report in its structure can be a logical continuation of the previous source - the estimate. That is, it will contain:

- date of preparation, name of the document (for example, “Report on entertainment expenses during a business breakfast”);

- information about the actual number of event participants in one status or another;

- information about the actual location of the event;

- a list of expense items indicating the actual amounts corresponding to them;

- the total amount of actual PR within the event;

- Full name, position and signatures of the employees responsible for drawing up the report.

Reflection of unreasonable expenses in accounting

Let's consider an example: an organization participates in a charity program by transferring contributions in the amount of 175,000.00 rubles. From the point of view of tax legislation, such expenses will be unjustified, since they do not lead to income (Article 270-16.34 of the Tax Code of the Russian Federation). An attempt to include them in the calculation of the tax base in order to reduce it may lead to the application of penalties against the organization.

In accounting, charitable contributions are reflected in account 91:

- Dt 91/2 Kt 76 - 175,000.00 rub. — reflects the amount of the charitable contribution.

- Dt 76 Kt - 51.50 - 175000.00 rub. — a charitable contribution is transferred.

- Dt 99/PNO Kt 68/Income tax - RUB 35,000.00. — a permanent tax liability is reflected (175,000.00*20%= 35,000.00).

Important! If an organization has incurred a loss as a result of its activities, this cannot serve as a basis for recognizing expenses as economically unjustified. Article 252 of the Tax Code of the Russian Federation does not justify costs based on the results of the activities of an economic entity. Likewise, costs aimed at reducing losses are justified (see letter of the Ministry of Finance No. 03-03-04/4/69 dated 10/27/05).

The determining factor is the focus on generating income, and not the result of economic activity during the period of expenditure.

Main

- The justification of expenses is determined by the organization.

- The expenses incurred must be primarily aimed at generating profit within the scope of the type of activity declared by the organization.

- Costs that do not meet this requirement, as well as those incurred in excess of the norms established by law, are economically unjustified. They cannot be included in tax calculations and reduce the tax base.

- Control of unreasonable expenses and expenses that may be recognized by the Federal Tax Service as unreasonable is carried out by the management of the organization.

- During a tax audit, the burden of proof of the unreasonableness of the taxpayer's expenses rests with the fiscal authorities.

Director's order about the event

Such an order must contain:

- date, number of the document;

- name of the document (for example, “On holding a business breakfast”);

- name of the business entity;

- a text block with the rationale for holding the event (with the phrase “For the purpose”);

- a text block of an operative nature (“I order”), which reflects the list of tasks assigned to responsible persons as part of the event, as well as a list of relevant persons;

- Full name, position of the head of the organization, his signature.

Results

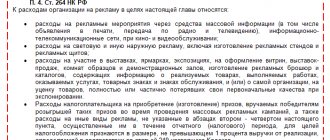

PR determined in accordance with paragraph 2 of Art. 264 of the Tax Code of the Russian Federation, can be used by a company to reduce the tax base within the established limits. To do this they must be confirmed.

You can find other useful information about PR in the article “How are entertainment expenses correctly reflected in tax accounting?”

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Cargo transportation

The fact of concluding a contract for the carriage of goods is confirmed by a waybill drawn up strictly in accordance with the form approved by Decree of the Government of the Russian Federation dated April 15, 2011 No. 272 (letter of the Ministry of Finance dated August 28, 2021 No. 03-03-06/1/61110).

The consignment note in the TORG-12 form is not suitable for this. It does not indicate the delivery of the goods, but only its delivery and acceptance (letter of the Ministry of Finance dated December 21, 2021 No. 03-03-06/1/85703).

If the bill of lading does not contain the total cost of transportation, in addition to it, a primary document should be drawn up in which it is defined. Such a document may be a UPD (letter of the Federal Tax Service dated August 10, 2021 No. AS-4-15/ [email protected] ).

If you don’t have a waybill, you won’t be able to write off transportation costs.

Thus, only if the necessary documents are available and executed in accordance with all the rules, expenses under the relevant agreement can be taken into account as expenses when taxing profits.

Event program

Many companies prefer to supplement the set of documents we reviewed with a program for an official event.

This source may include:

- name (for example, “Business Breakfast Program”);

- wording reflecting the purpose of the official event;

- date or period, location of the event;

- lists of event participants with one or another status;

- lists of partner organizations or individuals to whom the business entity plans to contact in order to obtain translation, transport and other services.

- Full name, position, signatures of persons responsible for the event.