Federal Law No. 402 of 06-12-11 “On Accounting” places responsibility for organizing accounting work on the head of the company. At the same time, other regulations contain the concept of managerial responsibility and chief accountant liability, even criminal liability.

What requirements does the law impose on persons responsible for maintaining accounting work in an organization, what should the chief accountant or the person performing his functions do if the requirements of the manager violate the norms and rules of accounting, who bears final and full responsibility for the violations, we will consider in the article .

Question: After the change of general director, the organization was brought to administrative responsibility for violating labor laws due to mistakes made during his work. Is it possible to collect penalties from the former director and bring him to administrative responsibility? View answer

What role does accounting play?

Every company strives to earn maximum profits. But achieving the best result is impossible without an effective and clear distribution of financial flows. For this purpose, a special system is created that provides accurate accounting of business transactions, recording cash flows and inventory items.

The results of proper organization of accounting are as follows:

- cost optimization;

- control of company cash flows;

- extracting maximum efficiency in the distribution of funds;

- easier to analyze reports.

All types of business entities, with the exception of merchants, are required to maintain accounting records. They take into account income and expenses using slightly different methods, which are provided by law.

Also see “Professional standard for an accountant: how and why to apply it.”

Regulatory requirements for the chief accountant

According to the norms of clause 4 stat. 7 of Law No. 402-FZ, increased requirements are imposed on the chief accountant or other employee to whom accounting functions are transferred. In particular, this is the presence of specialized higher education; a certain length of employment in the specialty; no criminal record in the economic sphere. In addition, federal legislation may establish other requirements for the chief accountant.

If an enterprise hires a third party - legal or individual - to keep records, it is first necessary to conclude a contract for services. At the same time, the individual must also have a higher education, practical employment experience and not have a criminal record. A legal entity must have at least one employee on its staff who meets the requirements stated above.

For chief accountants of credit structures and non-credit financial institutions, qualification requirements are approved by the Central Bank of the Russian Federation. To date, no special requirements have been established for chief accountants and ordinary employees of the accounting service of ordinary commercial firms. However, it is better to trust the accounting of your enterprise to an experienced worker and, at a minimum, someone with a higher education in economics or finance.

Procedure

In medium and large organizations, the considered procedure for launching the accounting mechanism is as follows:

- They determine the structural unit and its employees who will deal with accounting issues, as well as control the flow of documents with contractors and suppliers, pay salaries, etc. The range of tasks that will be faced by the chief accountant should also be determined here.

- The responsible person forms the accounting policy rules, documentation procedures, working chart of accounts, mechanism for preparing financial statements, etc.

- Timely and correct preparation of documents and reports for submission to regulatory authorities (IFTS, Rosstat) begins.

Also see “Why is an organization’s accounting policy needed?”

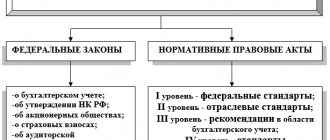

The requirements for accounting are specified in the Federal Law on Accounting No. 402-FZ. The main ones include:

- accounting of business transactions in rubles;

- separate accounting of property owned by the organization;

- maintaining double entries based on the approved chart of accounts;

- reporting in Russian, etc.

A company must keep records from the moment of registration until it is recorded in the Unified State Register of Legal Entities about its liquidation. Otherwise, a large fine or disqualification of officials may be imposed.

Who is required to do accounting?

In accordance with the norms of stat. 6 of Law No. 402-FZ dated December 6, 2011, the obligation to maintain accounting records is assigned to all business entities. Exceptions are provided for:

- Individual entrepreneurs or private practitioners - subject to accounting for income and expense transactions in accordance with legal norms or control of physical indicators (taxable objects) characteristic of certain types of commercial activities.

- SE (separate divisions) of foreign companies - provided that such representative offices or branches, as well as other types of SE, take into account income and expense transactions, taxable objects according to legal requirements.

Accounting begins “at the start” of opening a business, that is, from the date of official state registration with control authorities, and continues until the termination of economic activity as a result of closure or liquidation. In this case, the subject must be excluded from the Unified Register (Unified State Register of Legal Entities or Unified State Register of Legal Entities).

When organizing accounting, some companies have the right to use simplified methods. Such methods, among other things, include the preparation of simplified financial statements. This rule applies to the following types of business:

- Subjects that, according to accepted criteria, belong to the SMP.

- Various NGOs.

- A legal entity with the status of participants in the Skolkovo innovation project.

The following are not entitled to use simplified methods of organizing accounting:

- LCD and housing cooperatives.

- Legal entities required to conduct an annual audit of financial statements.

- Consumer credit cooperatives, including agricultural ones.

- Government agencies.

- Law offices, consultations, and colleges.

- MFO.

- Notary chambers.

- Lawyer consulting.

Consequently, most companies are required to keep accounting records immediately from the moment of establishment. Firms that fail to comply with this regulatory requirement face serious consequences in the form of fines and disqualification of officials. We will tell you more about the sanctions below, but now we will find out which employee should be responsible for the correct organization and maintenance of records.

Reflection of leasing in accounting

Who is responsible for accounting and its organization?

The concepts of “organization” and “maintenance” of accounting must be separated. The head of the company is entirely responsible for the first; for the second, he is also partly the chief accountant. The legislation of the Russian Federation states that accounting and storage of its documents must be organized by the head of the enterprise.

Ministry of Finance: responsible for organizing accounting (clause 6 of order No. 34n dated July 29, 1998).

In practice, accounting functions are usually transferred to the chief accountant. To do this, the manager performs a number of certain formalities:

- documents the accounting system (issues the appropriate order);

- determines the list of responsibilities of the chief accountant and includes them in the job description of this specialist;

- installs the necessary equipment (computers, software, etc.);

- organizes the work process.

Also see “Job description for the chief accountant”.

The chief accountant is obliged to:

- competently formulate an accounting policy taking into account the specifics of the company;

- submit the paper on time. Reporting where needed;

- keep records of funds at the enterprise, etc.

Thus, the chief accountant is responsible for accounting , first of all, in accordance with the law, and then - in accordance with the terms of the employment contract.

Also see: The Most Common Accounting Irregularities.

Criminal liability

The chief accountant is brought to criminal liability in case of evasion of taxes, fees and insurance premiums, or failure to fulfill the duties of a tax agent.

According to the Judicial Department of the Armed Forces of the Russian Federation, a total of 288 persons were convicted of tax crimes in 2021. However, it is difficult to accurately determine the number of accountants involved, since among those convicted there may be not only accountants, but also company managers.

Paragraph 11 of the Resolution of the Plenum of the Supreme Court of the Russian Federation dated November 26, 2019 N 48 “On the practice of application by courts of legislation on liability for tax crimes” states that a mandatory element of the crimes provided for in Article 199 of the Criminal Code of the Russian Federation is a large or especially large amount of unpaid taxes, fees, insurance premiums, determined in accordance with the notes to Article 199 of the Criminal Code of the Russian Federation.

In this article, a large amount is recognized as an amount of taxes, fees, and insurance premiums that exceeds fifteen million rubles over a period of three consecutive financial years, and an especially large amount is an amount that exceeds forty-five million rubles over a period of three consecutive financial years.[ 1]

The consequence of such non-payment should be considered a lack of funds received by the state treasury.