The role of the primary document in accounting

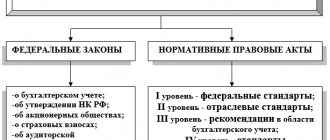

Primary documents are documents with the help of which the company formalizes the economic events that occurred at the enterprise (Clause 1, Article 9 of the Law “On Accounting” dated December 6, 2011 No. 402-FZ).

The first thing that accountants of any organization should clearly understand is that today there is no specific mandatory list of forms for primary accounting documents. Any company determines for itself the forms of primary documents depending on the purpose of their use.

However, for such documents a list of mandatory details is legally established (Clause 2, Article 9 of Law No. 402-FZ).

IMPORTANT! The forms used in accounting must be fixed in the accounting policy of the organization (clause 4 of PBU 21/2008, approved by order of the Ministry of Finance of the Russian Federation dated October 6, 2008 No. 106n).

For information about how long primary documents need to be stored, read the material “What is the period of storage of documents in an organization’s archive?”

Please note that as of October 26, 2020, new sanctions for improper storage of documents apply. Read more about this in ConsultantPlus. Trial access to the system is provided free of charge.

The procedure for transferring accounting documentation and its storage period

Each institution needs to develop and consolidate in its accounting policy a schedule for the turnover of primary accounting documents. As a general rule, it is necessary to reflect the fact of acceptance of the primary accounting register, its processing, storage and filing in the archive.

Accounting employees are responsible for the integrity and safety. The shelf life of financial and economic registers depends on the purpose of a particular form. For example, tax information must be stored for at least four years, and payroll information for an organization’s employees must be stored for at least 75 years.

In the event that the person responsible for safety changes, it is necessary to prepare and sign a corresponding act.

List of possible primary accounting documents

The list of primary accounting documents in 2020-2021 may be as follows:

- Packing list. This is a document that reflects the list of transferred inventory items. The invoice is issued in 2 copies and contains information that is subsequently reflected in the invoice. The invoice is signed by representatives of both parties involved in the transaction and certified by a seal (if the company uses it in its practice).

Read about its most commonly used form in the article “Unified form TORG-12 - form and sample.”

- Record of acceptance. It is drawn up upon completion of certain works (services) to confirm that the result of the work meets the original requirements of the contract.

See a sample of such an act here.

- Primary documents for payment of wages to personnel (for example, pay slips).

For more information about these statements, see the article “Sample of filling out the payroll statement T 49” .

- Documents related to the presence of fixed assets - here the company can draw up such documentation from the list of primary accounting documents:

- Certificate of acceptance and transfer of fixed assets in the OS-1 form - upon receipt or disposal of an object not related to buildings or structures.

For more information about this act, see the material “Unified Form No. OS-1 - Certificate of Acceptance and Transfer of OS” .

- If the fixed asset is a building or structure, then its receipt or disposal is formalized by an act in the OS-1a form.

For more information, see the article “Unified form No. OS-1a - form and sample” .

- The write-off of an asset is formalized by an act in the OS-4 form.

For more details, see the material “Unified Form No. OS-4 - Act on the write-off of an asset” .

- If it is necessary to document the fact of the inventory carried out, an inventory list of the fixed assets is drawn up in the INV-1 form.

For more information about such a primary document, see the article “Unified form No. INV-1 - form and sample” .

- If the inventory was carried out in relation to intangible assets, then the inventory will be compiled according to the INV-1a form.

For more information, see the material “Unified form No. INV-1a - form and sample” .

- A separate group of primary documents are cash documents. These include, in particular, the following list of primary accounting documents for 2020-2021:

- Receipt cash order.

For more information about its preparation, see the article “How is a cash receipt order (PKO) filled out?” .

- Account cash warrant.

For details about it, see the material “Cash expenditure order - form and sample.”

- Payment order.

Read about the rules for preparing this document here.

- Advance report.

Read about what to follow when drawing up such a document in this article.

- The act of offsetting mutual claims.

Read about the specifics of using this document here.

- Accounting information.

For information on the principles of its execution, see the material “Accounting certificate of error correction - sample”.

The above list does not exhaust the entire scope of primary documents used in accounting, and can be expanded depending on the characteristics of the accounting carried out in each specific organization.

You will find a complete list of primary documents in the Directory from ConsultantPlus. Get trial access to the system and proceed to the list.

IMPORTANT! They are not primary accounting documents from the list 2020-2021 - the list was proposed above:

- Agreement . This is a document that stipulates the rights, obligations and responsibilities of the parties involved in the transaction, the terms and procedure for settlement, special conditions, etc. Its data is used when organizing accounting for the analytics of settlements with counterparties, but it itself does not generate accounting transactions.

- Check. This document reflects the amount that the buyer agrees to pay by accepting the supplier's terms. The invoice may contain additional information about the terms of the transaction (terms, payment and delivery procedures, etc.), i.e. it supplements the contract.

- Invoice. This document is drawn up for tax purposes, since on its basis buyers accept for deduction the amounts of VAT presented by suppliers (clause 1 of Article 169 of the Tax Code of the Russian Federation). Thus, in the absence of other documents characterizing a particular transaction, it will be impossible to confirm expenses for this transaction with an invoice (letter of the Ministry of Finance of the Russian Federation dated June 25, 2007 No. 03-03-06/1/392, Federal Tax Service dated March 31, 2006 No. 02-3 -08/31, resolution of the Federal Antimonopoly Service of the East Siberian District dated April 19, 2006 No. A78-4606/05-S2-20/317-F02-1135/06-S1).

It should be borne in mind that the unified forms of primary accounting documents given in the list are not mandatory for use, since since 2013 (after the adoption of Law No. 402-FZ), forms of such forms can be developed independently. But in most cases they continue to be used. Therefore, in 2020–2021, the list of unified forms of primary accounting documents contained in the resolutions of the State Statistics Committee continues to remain relevant.

Planning and reporting documentation

Planning and reporting documentation ensures planning of the organization's activities, which allows you to set goals and calculate resources for development and distribution according to goals and objectives. All planning and reporting documents are compiled for a certain period and include various recorded data. Deviation from planned indicators can be caused by low performance discipline, current market conditions and incorrect planning.

Types of planning and reporting documentation:

- strategy;

- program;

- work plan;

- business plan;

- report.

What information should the forms of primary documents contain?

Despite the fact that there are currently no mandatory primary documents for all forms, the legislator has established requirements for the content of such documents. The list of mandatory details that must be contained in each primary document is given in paragraph 2 of Art. 9 of Law No. 402-FZ. These are, in particular:

- document's name;

- the date on which such document was drawn up;

- information about the person who compiled the document (name of the company or individual entrepreneur);

- the essence of the fact of economic life that was formalized by this document;

- monetary, numerical characteristics, measures of the event that occurred (for example, in what volume, in what units and for what amount were the products sold to customers);

- information about the responsible specialists who documented the event, as well as the signatures of such specialists.

If the primary source does not meet the requirements, the organization may also face tax consequences.

Get free access to K+ and learn about the most common complaints tax authorities have and how to counter them.

For information on how the right to sign is delegated, read the article “Order on the right to sign primary documents - sample.”

Primary documents and accounting registers

How can primary accounting documents be classified?

If the primary document was issued by the company itself, then it can belong either to the group of internal or to the group of external. A document that is drawn up within the company and extends its effect to the compiler company is an internal primary document. If the document was received from the outside (or compiled by the company and issued to the outside), then it will be an external primary document.

The company's internal documents are divided into the following categories:

- Primary administrative documents are those with which a company gives orders to any of its structural units or employees. This category includes company orders, instructions, etc.

- Executive primary documents. In them, the company reflects the fact that a certain economic event has occurred.

- Accounting documents. With their help, the company systematizes and summarizes information contained in other administrative and supporting documents.

After a business event has been documented as a primary document, it is then necessary to reflect the event in the accounting registers. They, in fact, are carriers of ordered information; they accumulate and distribute the characteristics and indicators of business transactions.

The following registers are distinguished by their appearance:

- books;

- cards;

- free sheets.

Based on the method of maintaining the register, the following groups are distinguished:

- Chronological registers. They record the events that happened sequentially - from the first in time to the last.

- Systematic registers. In them, the company classifies completed transactions by economic content (for example, a cash book).

- Combined registers.

According to the criterion of the content of information reflected in the registers, the following are distinguished:

- synthetic registers (for example, a journal order);

- analytical registers (payroll);

- combined registers, in the context of which the company carries out both synthetic and analytical accounting.

For more information about accounting registers, see the article “Accounting registers (forms, samples)” .

Results

At present, there are no mandatory forms and lists of primary accounting documents: any business entity has the right to independently determine for itself the forms of primary documents that it will use in its activities.

At the same time, the most common primary accounting documents are those that have analogues among the unified forms approved by the State Statistics Committee.

After the primary document is drawn up, it is necessary to transfer information from it to the accounting register.

Sources:

- Federal Law of December 6, 2011 N 402-FZ “On Accounting”

- Order of the Ministry of Finance of Russia dated October 6, 2008 N 106n

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Lesson 5 Summary

- An accountant has the right to make an accounting entry only on the basis of a primary document.

- The documentation must be completed correctly using a standard or free form with a mandatory set of details.

- Documents can be signed by the manager, as well as a limited number of persons appointed by order.

- Each document is checked for errors, recorded in a journal, filed in a folder and stored until the expiration date.

- The minimum retention period for most accounting source documents is 5 years.

- You can store documentation in an office in a room with the right conditions or in an archival company.

- Papers with expired shelf life must be destroyed, for which an expert commission is appointed.