During its work, any business entity (individual entrepreneur or LLC) acquires a huge number of documents: registration, accounting, reporting, personnel, permits, supporting and confirming documents. And although this is the 21st century, and electronic document management has long been integrated into business practice, documents in paper format are still an irreplaceable value. The shelf life of some of them is 75 years, as they say, manuscripts do not burn.

We are, of course, not concerned about the historical value of the organization’s documents, but about the fact that the lack of the necessary papers, especially for accounting and personnel, can create difficulties when passing inspections and lead to financial sanctions, in other words, fines. To avoid financial losses, we advise you to check the complete set of all necessary documents from time to time or entrust this check to specialists:

Free business audit

The obligation to collect and store documents of an organization is established by Law No. 125-FZ of October 22, 2004 “On Archival Affairs in the Russian Federation.” According to it, organizations and individual entrepreneurs are obliged to ensure the safety of archival documents, including personnel documents. The list of archival documents is given in the Order of the Federal Archive of the Russian Federation dated December 20, 2021 N 236, it consists of 12 sections and contains 657 items.

Not all of them are related to entrepreneurial activity, so we suggest that you check your documentary baggage with the necessary minimum that organizations and individual entrepreneurs must have.

Registration documents of organizations and individual entrepreneurs

Let's start with the documents with which, in fact, the life of a legal entity begins or the acquisition of individual entrepreneur status by an individual. The list of registration documents for an organization is noticeably larger than for an individual entrepreneur:

- Charter of a limited liability company. To date, this is the only constituent document for an LLC. If changes have been made to the charter, it is advisable to store its previous editions with the note “invalid due to the adoption of a new edition of the charter dated ___.”

- Minutes of the general meeting of founders or the decision of the sole participant to create an LLC. Everything is clear here - this document is an expression of the will of the founders to create a legal entity.

- List of LLC participants. The list must contain current information about each participant (passport data of an individual or organization data), the size and value of each participant’s share, information about its payment. If there are shares owned by the company itself, then information about them is also indicated.

- Certificate of state registration of a legal entity or individual entrepreneur (issued until 2021).

- Certificate of registration with the tax authority (for individual entrepreneurs and LLCs).

- Entry sheet in the Unified State Register of Legal Entities (for LLC) or in the Unified State Register of Individual Entrepreneurs (for individual entrepreneurs). As for extracts from the Unified State Register of Legal Entities (USRIP), there is no need to store them. Usually a bank, notary, counterparties, etc. They request an extract that is no more than a month old, so if necessary, you need to get it again each time.

- Letter with information about statistics codes (for individual entrepreneurs and LLCs). You can obtain this information without contacting the statistical authorities personally, but through a form on the official website of Rosstat. You can find your statistics codes with our help. Just print a page from the site with your codes. Banks also accept such a document, but if you wish, you can also receive an official document with the seal of regional statistical authorities.

Documents of the organization confirming its legal address

When opening a bank account, the bank will require from the client organization “information about the presence or absence at its location of a legal entity and its permanent management body.” The following documents (optional) can serve as confirmation of the organization’s legal address:

- Certificate of ownership of the premises in which the LLC is located (if the owner is the founder);

- The lease agreement and the acceptance and transfer certificate of the premises, as well as a copy of the certificate of ownership of the premises, certified by the lessor;

- The owner’s consent to register an LLC at the home address and a copy of the certificate of ownership of the premises.

Such documents are also requested by tax authorities (during the initial registration of an LLC and subsequent changes to the Unified State Register of Legal Entities) and licensing authorities. For individual entrepreneurs, there are no special documents confirming his address. A copy of the registration in the passport is enough.

Permitting documents of organizations and individual entrepreneurs for certain types of activities

This refers to those types of activities that require additional documents from government services:

- Licenses for licensed types of activities;

- SRO approvals (for construction companies);

- Confirmation that you have submitted a notice of commencement of activity (in the cases specified in Article 8 of Law No. 294-FZ of December 26, 2008);

- Permits from the SES and the State Fire Service (for shops, catering establishments and hotels);

- Certificates issued for your products or services, etc.

Accounting and reporting documents of organizations and individual entrepreneurs

Accounting and reporting can be accounting and tax. You can find out how one differs from the other in this article. Here we will limit ourselves to the fact that accounting is mandatory only for organizations, and tax accounting is carried out by all taxpayers (including LLCs and individual entrepreneurs). Based on this, the list of documents of the organization is much more significant than that of an individual entrepreneur, due to the financial statements.

The organization's accounting documents include:

- Accounting registers (general ledger, order journals, memorial orders, account transaction journals, turnover and accumulative statements, accounting books, inventory lists, etc.);

- Accounting statements (balance sheets, profit and loss statements, explanatory notes);

- Working chart of accounts;

- Accounting policy;

- Correspondence on accounting issues.

Documents related to tax accounting (which are maintained by both organizations and individual entrepreneurs) include:

- Tax returns;

- Books of accounting of income and expenses;

- Invoices;

- Purchase books and sales books;

- Documents confirming the tax loss, the amount of which has been carried forward to future periods;

- Acts of reconciliation with the Federal Tax Service and certificates of the status of settlements with the budget.

Primary documents record the fact of business transactions and are the basis for accounting and tax accounting:

- Cash documents and books;

- Bank documents;

- Warrants, timesheets;

- Invoices;

- Expense reports;

- Acts on acceptance and delivery of property and services;

- Acts on write-off of inventory items;

- Receipts, etc.

Agreements and documents confirming their execution:

- Treaties, agreements, contracts, invoice agreements;

- Protocols of disagreements under contracts;

- Correspondence, calculations, certificates, conclusions to contracts and agreements;

- Transaction passport;

- Liability agreements;

- Correspondence regarding accounts receivable/payable;

- Documents on acceptance of completed work (acts, certificates, invoices).

Documents on cash register equipment:

- Cash register passport;

- Cash register registration card;

- Journal of the cashier of the operator;

- Service agreement with the service center;

- Used control tapes;

- Fiscal memory drives, etc.

About business

Accounting and tax accounting documents are documentary evidence of the organization’s income and expenses, therefore the business entity is obliged to organize their proper storage, and subsequently timely destruction. This is only possible if the storage periods and document destruction procedures are observed.

Archival storage, as well as timely destruction of accounting documents, is a pressing task for many accountants. The basis for the correct destruction of documents is knowledge of the legal requirements regarding the procedure and terms of storage of accounting documentation. Please note that in accordance with Art. 5 of the Federal Law of October 22, 2004 N 125-FZ “On Archival Affairs in the Russian Federation”, archival documents include all documents, regardless of the type of their medium. This means that document storage applies to both paper and electronic documents. The general procedure for storing documents is regulated by the following main documents: 1) Federal Law of October 22, 2004 N 125-FZ “On Archiving in the Russian Federation”; 2) The basic rules for the operation of the organization’s archives, approved by the Decision of the Federal Archive of 02/06/2002 (important: the basic rules do not regulate the storage period of documents); 3) A list of standard management archival documents generated in the process of activities of state bodies, local governments and organizations, indicating storage periods, approved. By Order of the Ministry of Culture of Russia dated August 25, 2010 N 558; 4) Regulations on documents and document flow in accounting, approved. By Order of the USSR Ministry of Finance dated July 29, 1983 N 105. The obligation to store documents generated in the activities of open and closed joint-stock companies is established by the Regulations on the procedure and terms of storage of documents of joint-stock companies, approved. Resolution of the Federal Commission for the Securities Market dated July 16, 2003 N 03-33/ps. Limited liability companies, accordingly, are guided by the Federal Law of 02/08/1998 N 14-FZ “On Limited Liability Companies”. When determining specific storage periods for accounting documentation, organizations are guided by the List of standard management archival documents generated in the process of activities of state bodies, local governments and organizations, indicating storage periods, approved. Order of the Ministry of Culture of Russia dated August 25, 2010 N 558. This List includes standard management archival documents generated in the process of activities of state bodies, local governments and organizations in the implementation of the same type (common to all or the majority) management functions, regardless of the form of ownership, with indicating storage periods. It contains documents grouped into sections, compiled when documenting the facts of the economic life of organizations, and instructions for its use. Among the sections highlighted in the List, in particular, there is section. 4 “Accounting and Reporting”, containing subsections 4.1 “Accounting and Reporting” and 4.2 “Statistical Accounting and Reporting”. The Tax Code of the Russian Federation obliges taxpayers to ensure the safety of accounting, tax accounting data and other documents necessary for the calculation and payment of taxes for four years. This also applies to documents confirming the receipt of income, the incurrence of expenses, as well as the payment (withholding) of taxes. Four years is the general storage period, since for some types of documents tax legislation establishes special storage periods. For example, this applies to documents confirming the amount of loss received by the taxpayer. The Tax Code of the Russian Federation establishes that such documents are retained by the taxpayer for the entire period when he reduces the tax base of the current tax period by the amounts of previously received losses. The Tax Code of the Russian Federation gives the taxpayer the right to carry forward a loss for ten years following the tax period in which the loss was incurred, due to which documents confirming the amount of the loss must be retained by the taxpayer for ten years. Accounting and tax records must be retained for a period of five years.

On January 1, 2013, the Federal Law of December 6, 2011 N 402-FZ “On Accounting” came into force, in Art. 29 of which it is stated that primary accounting documents, accounting registers, accounting (financial) statements are subject to storage by an economic entity for periods established in accordance with the rules for organizing state archival affairs, but not less than five years after the reporting year. The storage period for documents is calculated from January 1 of the year following the year in which they were completed. So, for example, the organization will begin to calculate the storage period of files completed in 2010 only from January 1, 2011. We especially draw attention to the fact that it is possible to destroy documents whose storage periods have expired only if the period to to which they refer has already been verified. To automatically determine the storage periods for accounting documents, we recommend using the free service “Archivist Online”, which searches for documents using three main lists, including the List of Standard Management Archive Documents, approved. By order of the Ministry of Culture of Russia dated August 25, 2010.

Responsibility for improper storage of accounting documents

First of all, the manager is responsible for organizing the storage of organization documents, including primary accounting documents. The chief accountant of the institution is also responsible for the safety of primary accounting documents, accounting registers and financial statements. Documentation may be lost as a result of natural disasters or illegal actions of third parties. If documents are lost as a result of someone’s unlawful actions (for example, theft), then this fact must be confirmed by law enforcement agencies. Loss of documents as a result of natural disasters is also documented by the relevant authorities. In the event of a fire, this may be a certificate from the fire inspection authorities. In case of loss of primary accounting documents, the head of the organization, in accordance with clause 6.8 of the Regulations on Documents and Document Flow, appoints by order a commission to investigate the causes of the loss. The absence of primary documents justifying the completion of any business transaction, in accordance with Art. 120 of the Tax Code of the Russian Federation refers to gross violations of the rules for accounting for income and expenses, which means: the absence of primary documents, or invoices, or accounting registers; systematic (twice or more times during a calendar year) untimely or incorrect reflection in the accounting accounts and in the reporting of business transactions of funds, tangible assets, intangible assets and financial investments of the taxpayer. For violation of the procedure and terms of storage of accounting documents, administrative liability is provided - a fine for officials will range from 2,000 rubles. up to 3000 rub. (Article 15.11 of the Code of the Russian Federation on Administrative Offenses). The absence of primary documents, invoices, and accounting registers is a tax offense. Responsibility for it is provided for in Art. 120 Tax Code of the Russian Federation. The minimum fine under this article is 5,000 rubles. The chief accountant is responsible for the safety of documents. It is he who has the right to make a decision on issuing such documents to employees of structural divisions of the enterprise. As for liability for failure to comply with the rules for storing accounting documents, it can be both administrative and tax. As mentioned above, the absence of primary documents and accounting registers is a gross violation of the rules for accounting for income, expenses, and taxable items and entails a fine of 5,000 to 15,000 rubles. (Article 120 of the Tax Code of the Russian Federation). An administrative fine in this case can be imposed both for violation of archival requirements for storing documents (Article 13.20 of the Code of Administrative Offenses of the Russian Federation - 300 - 500 rubles), and for a gross violation of accounting rules, if due to the lack of documents the accounting statements are distorted (Article 15.11 Code of Administrative Offenses of the Russian Federation - 2000 - 3000 thousand rubles). Destruction of documents without observing their storage periods is illegal and entails administrative liability. In accordance with Art. 13.20 of the Code of Administrative Offenses of the Russian Federation establishes administrative sanctions for violation of the rules of storage, acquisition, accounting or use of documents in the form of a warning or the imposition of an administrative fine.

Destruction of accounting documents and methods of their disposal

The procedure for destroying accounting documents is unified and consists of several stages: conducting an examination of the value; drawing up an act on the allocation of cases for destruction; physical destruction of documents and drawing up a corresponding act. The process of document destruction is fixed by law.

The allocation of files for destruction is regulated by: - Federal Law of October 22, 2004 N 125-FZ “On Archival Affairs in the Russian Federation”; — Federal Law of December 29, 1994 N 77-FZ “On the mandatory copy of documents of organizations and commercial organizations indicating storage periods”; — GOST 7.50-2002 “Conservation of documents” (introduced by Decree of the State Standard of Russia dated 06/05/2002 N 232-st).

Examination of the value of documents

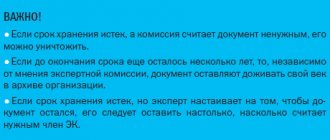

In accordance with clause 1.1 of the Model Regulations on the permanent expert commission of an institution, organization, enterprise, approved. By Order of the Federal Archive of January 19, 1995 No. 2, the organization creates a permanent expert commission to examine the value of documents created in the process of the organization’s activities, select and prepare them for transfer to state storage in archives.

Storage and disposal methods of accounting documents

It includes the most qualified specialists from all existing structural divisions of the company, who can assess the historical and practical value of certain types of documents. The composition of the expert commission is approved by the head of the organization. It is the expert commission in the organization that deals with the selection of documents for permanent and temporary storage, and it also makes decisions on the destruction of documents whose storage periods have expired. One of the leaders of the organization, who is in charge of office work and archives, is appointed as the chairman of the expert commission. This expert commission conducts an examination of the value of documents. Value examination is the study of documents based on criteria of their practical value in order to determine storage periods, to select them for permanent storage and to allocate documents with expired storage periods for destruction; is held annually. An examination of the value of documents is carried out through a page-by-page review of cases. It is unacceptable to determine the retention period of files based solely on the titles. Case inventories are compiled for documents of permanent storage, for personnel and temporary (over 10 years) storage, selected for further storage. Cases allocated for destruction are included in the Act on the allocation for destruction of documents that are not subject to storage (Appendix 4 to clause 2.4.1 of the Basic Rules for the Operation of Organizational Archives). The act of allocation for destruction is approved by the head of the organization. The procedure for conducting an examination of the value of documents is defined in the Basic Rules for the Operation of Archives of Organizations (Chapter 2 “Examination of the Value of Documents”). Based on the results of the examination of documents, the expert commission should organize a procedure for the destruction of documents whose storage period has expired. The principles of physical destruction of documents are established in clause 9.9 of the National Standard of the Russian Federation “System of standards for information, library and publishing. Document management. General requirements. GOST R ISO 15489-1-2007", approved. By Order of Rostekhregulirovaniya dated March 12, 2007 N 28-Art.

Destruction of documents upon liquidation of an organization

According to the Federal Law of October 22, 2004 N 125-FZ “On Archival Affairs in the Russian Federation”, during the liquidation of non-governmental organizations, archival documents, documents on personnel, as well as archival documents formed in the process of their activities and included in the Archive Fund of the Russian Federation, are included in the Archive Fund of the Russian Federation. whose temporary storage has not expired are transferred by the liquidation commission in an orderly state for storage to the appropriate state or municipal archive on the basis of an agreement between the liquidation commission and the state or municipal archive. At the same time, the liquidation commission organizes the organization of archival documents of the liquidated organization. Consequently, if the storage period for documents has not expired, the liquidation commission must organize their ordering and transfer to the state or municipal archive under the appropriate agreement. If the organization is not the source of acquisition of state and municipal archives, then the destruction of documents is carried out without coordination with the archival authorities. In organizations that do not transfer documents to the state archive, documents subject to destruction are determined only after drawing up annual sections of inventories of permanent storage cases, and for personnel - only after approval by the head of the organization. Regardless of whether the organization is the source of acquisition of state archives or not, the allocation of cases for destruction can be carried out by a specialized (archival) company. This approach allows you to: — minimize the risk of erroneous (illegal) selection of documents for destruction or delegate it to a third party; — reduce non-core workload on the accountant; — significantly increase the efficiency of identifying cases for destruction; — prepare an act on the selection of cases for destruction in strict accordance with the law. The destruction of documents with expired storage periods must be documented in an act prepared by an expert commission and approved by the head of the organization. The act has a unified form (Appendix 4 to clause 2.4.1 of the Basic Rules for the Operation of Archives of Organizations). The act of allocating cases for destruction includes a list of documents intended for destruction, indicating general headings, as well as their number. The act indicates in accordance with which regulatory document (and article) the destruction is carried out.

Such documents may be a List of standard management documents generated in the activities of organizations, indicating storage periods, approved. Federal Archive Service of Russia 08/25/2010 (or earlier - approved 10/06/2000 - for cases generated during the period of validity of this List), industry lists and lists of scientific and technical documents or federal law. The act must indicate the years for which the documents were selected. At the end of the act of destruction, an entry may be made confirming the approval of the inventory of the personnel of the organization for all years specified in the act. An act on the allocation of documents for destruction is drawn up in the organization only after complete scientific and technical processing of the documents. It is important to remember that documents are destroyed only if an audit is carried out during the specified period. If the period covered by the documents has not been revised, they cannot be destroyed. The beginning of the document storage period is considered to be January 1 of the year following the year in which they were completed by office work (contracts are considered completed by office work only after the expiration of their validity period). For example, the calculation of the storage period for files compiled in 2012 begins on January 1, 2013. After the documents are selected for destruction and the corresponding act is drawn up, they are sent for destruction. An organization can destroy documents on its own or contact an appropriate organization that can ensure the disposal of documents with the required level of security. The destruction method depends on the industry specifics and the organization’s document destruction practices, as well as on the financial capabilities of the company. The main methods for disposing of expired documents are shredding, burning and on-site destruction of documents. After the destruction of documents, a certificate of the appropriate sample is drawn up.

Personnel documents of the organization and individual entrepreneur

Personnel documents are under special attention of tax authorities, funds (PFR, MHIF, Social Insurance Fund) and labor inspectorate (LIT). Individual employers have the same responsibilities as organizational employers with regard to maintaining personnel records.

We provide a list of personnel documents for organizations and individual entrepreneurs that every employer must have.

- Inner order rules

- Regulations on the protection of personal data of employees

- Staffing table

- Employment contract with each employee

- Employee personal card (form T-2)

- Work books of employees (if the employee is registered at the main place of work)

- Book of movement of work books and inserts in them

- All documents related to the calculation and payment of salaries and other payments to employees

- Labor protection instructions for positions (professions)

- Time sheet and calculation of wages

- Briefing log (familiarization with instructions)

- Vacation schedule

- Orders and instructions of the head of personnel

- Job descriptions for each position (if the contract contains a link to the instructions)

- Regulations on remuneration and bonuses for employees (if this is not specified in the contract)

- Regulations on certification of employees (if certification is carried out)

- Provision on trade secrets (if there is such a provision in the contract)

- Agreement on full financial responsibility (not for all employees)

- Shift schedule (if there is shift work)

- Collective agreement (if such an agreement has been concluded)

- Documents on certification or assessment of working conditions of workplaces

- Documents on labor protection

- Journals and books of personnel records (employment contracts, orders, personal files, travel certificates, military records, etc.).

The procedure for destroying documents is regulated by:

- Federal Law of 02/08/1998 N 14-FZ “On Limited Liability Companies” (Article 50); Federal Law of November 21, 1996 N 129-FZ “On Accounting” (Article 17); Federal Law of October 22, 2004 N 125-FZ “On Archival Affairs in the Russian Federation”;

- List of standard management documents generated in the activities of organizations, indicating storage periods, approved by the Federal Archive on October 6, 2000 (hereinafter referred to as the List of standard documents);

- Basic rules for the work of archives of organizations (approved by the Decision of the Board of Rosarkhiv dated 02/06/2002).

- Tax Code of the Russian Federation.

The procedure for destroying documents is as follows:

First of all, it is necessary to carry out an examination of documents and identify documents of permanent, temporary storage and documents that are not subject to storage (i.e. those that must be destroyed). Based on the results of the examination of the value of documents in the organization, inventories of permanent, temporary (over 10 years) storage and personnel records are drawn up, as well as acts on the allocation for destruction of files that are not subject to storage (clause 2.4.1 of the Basic Rules for the Operation of Archives of Organizations). Folders with documents (cases) that are subject to destruction are transferred for processing (disposal). The transfer of cases is formalized by an invoice, in which it is necessary to indicate the date of transfer of documents, the number of cases to be handed over and the weight of the waste paper. Loading and removal for disposal are carried out under the supervision of an employee responsible for ensuring the safety of documents in the organization. This procedure is provided for in clause 2.4.7 of the Basic Rules for the Operation of Organizational Archives. Ultimately, the expert commission must fix the correct procedure for destroying documents.

Storage periods for organizational and individual documents

Typically, the storage of documents is carried out by an accountant, human resources specialist, lawyer, and secretary. It’s good when there are several employees, and you can entrust one of them with maintaining and storing all this documentation.

And yet, even if the business is small, and the owner does not have time to devote a lot of time to this issue, it is necessary to think about the safety of documents. Here are the storage periods for the main groups of organizational and individual documents (see the List for the full list):

| DOCUMENTATION | STORAGE LIFE |

| Registration documents | constantly |

| Licenses and certificates of conformity | constantly |

| Annual financial statements | constantly |

| Accounting quarterly reporting | 5 years |

| Monthly accounting reports | 1 year |

| Accounting registers, working chart of accounts, accounting policies, correspondence on accounting issues | 5 years |

| Primary accounting documents, books and journals | 5 years |

| Accounting and tax accounting data for the calculation and payment of taxes, documents confirming income and expenses, as well as payment (withholding) of taxes | 4 years |

| Tax returns | 5 years |

| KUDiR for simplified tax system | constantly |

| Annual pay slips to the Social Insurance Fund | constantly |

| Quarterly payslips in the Social Insurance Fund | 5 years |

| Declarations and calculations for insurance contributions for pension insurance | 5 years |

| Agreements and documents related to them (except for leasing and collateral) | 5 years |

| Documents related to CCP | 5 years |

| Occupational safety documents | 5 years |

| Employment contracts | 75 years old |

| Personal files of the organization's leaders | constantly |

| Personal files of employees | 75 years old |

| Personal cards of employees | 75 years old |

| Documents of persons not hired (forms, applications, resumes) | 3 years |

| Original personal documents of employees (work books, diplomas, certificates) | on demand, and unclaimed - 75 years |

| Books, magazines, personnel records cards | 75 years old |

List of documents that need to be stored

The requirement to store accounting documents for periods established in accordance with the rules for organizing state archival affairs, but not less than 5 years after the reporting year, is enshrined in Art.

29 of the Law “On Accounting” dated December 6, 2011 No. 402-FZ. At the same time, the rules of archival affairs mean, first of all, the list of documents and their storage periods approved by Rosarkhiv (order No. 236 dated December 20, 2019, entered into force on February 18, 2020). The storage period for tax documents, reporting and annexes (additions) to it is also specified in the Tax Code. In particular, in Art. 23 of the Tax Code of the Russian Federation states that documents (tax and accounting) on the basis of which taxes were calculated should be stored for at least 4 years.

Important! ConsultantPlus warns The absence of documents necessary for the calculation and payment of taxes may result in prosecution for gross violation of the rules for accounting for income and (or) expenses and (or) objects of taxation established by clause 1 or clause 2 of Art. 120 Tax Code of the Russian Federation. And if the tax base is distorted, you face... Read more about liability in K+. Trial access is free.

A number of federal laws also contain clear instructions on the list of documents that must be retained for a certain period of time (or for a long period of time). So, in paragraph 1 of Art. 50 of the Law “On LLC” dated 02/08/1998 No. 14-FZ (hereinafter referred to as the Law on LLC) states that it is mandatory to preserve accounting documents among the constituent documentation:

- confirming the rights of the LLC to the property listed on its balance sheet;

- internal documentation of the business entity;

- documents on the issue of securities;

- other documentation, the need for storage of which is stipulated by federal laws, the charter of the economic company, and local regulations of the company.

In paragraph 1 of Art. 89 of the Law “On JSC” dated December 26, 1995 No. 208-FZ (hereinafter referred to as the Law on JSC) it is stated that among the mandatory storage of constituent documents the following accounting documentation is mentioned:

- documents confirming the company’s rights to assets that are listed on its balance sheet;

- all internal documentation;

- annual reports and other accounting documents;

- accounting documents;

- other documentation, the mandatory preservation of which is specified in the charter and/or local regulations.

You will find more information about what types of accounting documents are in the article “Unified forms of primary documents (list)”.

Where to store documents of the organization and individual entrepreneurs?

If there are few documents, then the easiest way is to create your own archive - store them in a safe (fireproof cabinet) or allocate a separate room for the archive. The law does not provide specific requirements for the design of the archive; the main thing is that it fulfill its function of collecting and storing documents.

Documents of the last three years, as well as those that are constantly required in work (most often, registration) constitute the so-called operational archive, therefore they are not stored for long-term storage. Documents stored for no more than five years, upon expiration of the storage period, must be destroyed by burning or cutting in a shredder.

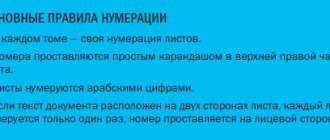

Other documents with a shelf life of more than five years must be deposited. To do this, they are filed in volumes with no more than 250 sheets in one volume. Each sheet of the volume is numbered, and an internal inventory and cover are drawn up. Documents can also be transferred for safekeeping to specialized archival organizations, but this makes sense if there are a large number of them.

Civil liability

Civil liability for violation of archival legislation is compensatory in nature. In other words, the person who is guilty, for example, of the loss or damage of documents, is obliged to compensate for the damage caused.

Most often, punishment is limited to a material penalty in the form of payment of a penalty or fine. However, in case of serious violations, for example, failure to comply with the rules for storing especially valuable documents, the latter can be confiscated by a court decision in accordance with Art. 240 Civil Code of the Russian Federation.

Responsibility for the safety of documents of the organization and individual entrepreneurs

It is necessary to store the above documents, first of all, in the interests of the businessman himself, because their absence makes it very difficult (or even impossible) for entrepreneurial activity. But penalties, in the form of fines, are also provided for by law.

Thus, for the absence of primary documents for one tax period, a fine of 10 thousand rubles is imposed on officials, and if this results in an underestimation of the tax base, then the fine will be at least 40 thousand rubles.

What to do if documents are lost? Lost registration documents (certificates of state registration and tax registration) or the Charter can be restored by contacting the tax office with an application to issue a duplicate certificate or a copy of the Charter.

If the accounting or personnel documents of an organization or individual entrepreneur are lost, a commission should be created to investigate the reasons. The fact of document theft must be confirmed by a police certificate; natural disasters - a certificate from the Ministry of Emergency Situations; flooding - a certificate from the Housing Office, etc.

Next, documents whose storage period has not expired will need to be restored. For documents related to the calculation and payment of taxes, you must contact the tax office, and for payment of contributions, respectively, to the funds. You can obtain copies of account statements and copies of payment documents from the bank. You can contact your counterparties with a request to send copies of contracts, acts, delivery notes, and invoices.

Features of storing various accounting documents

The rules for storing accounting documentation applied at the enterprise in accordance with current legislation should be prescribed in a separate local act. For such purposes, the provision on archiving documents is suitable.

In accordance with the adoption of a number of norms in domestic legislation, enterprises can use documentation in electronic form. Primary documentation can be stored in this form on the basis of Art. 9 of the Law on Accounting, accounting registers - Art. 314 of the Tax Code of the Russian Federation and tax reporting transmitted via electronic communication.

Electronic documents must be certified with a digital signature - this is stated in the letter of the Ministry of Finance dated August 22, 2012 No. 03-02-07/1-202. But if a request is received from the inspector to provide such documentation in printed form, it must be printed by the taxpayer and certified in accordance with all the rules. The storage periods for electronic documentation are the same as for analogues in printed form.

Information on storing personnel documentation is contained in the article “What is the storage period for personnel documents in an organization?”