The abbreviation KBK stands for budget classification code. In this case, it is necessary to understand what tax is paid under the number 18210101011012100110 KBK. The 2021 interpretation for this code is payment of income tax for organizations that do not belong to the consolidated category of payers.

When filling out a receipt for payment of a fee from the income of an organization, citizens write down the KBK number 18210101011011000110 on the form. This budget classification code means the payment of funds from the calculated fee, which are sent to the federal budget.

Explanation KBK 182 1 0100

Budget classification code is an indicator that determines payments to the budget of government departments. The BCC contains information about the payer, the fee, and indicates the type of payment: penalties, penalties, interest or other budget profit.

The payment documentation contains the number 18210101011011000110 KBK, the decoding of which is regulated by Order of the Ministry of Finance No. 132n dated 06/08/2018 (as amended on 11/30/2018). Cipher content:

- 182 is the administrator code, or the code of the department to which the funds are sent. Government institutions to which payments and contributions are sent are presented in Appendix No. 3 of Order of the Ministry of Finance No. 132n.

- 1 - type of profit to the state budget. So, 1 - tax and non-tax revenues, 2 - gratuitous profit.

- 01 - type of tax. This figure refers to the collection from the income of enterprises.

- 01011 - article and sub-item of budget profit: type of duty and the budget to which the funds are sent. The last two digits “11” are the type of payment.

- 01 is an income element that determines the department’s budget. In this case, the federal budget of the Federal Tax Service.

- 1000 - payment type. The legislation of the Russian Federation provides for payments for collection on the profits of organizations, with the exception of consolidated categories of payers: principal amount - 1000, penalties - 2100, interest - 2200, fines - 3000.

- 110 - type of payment regarding profit or costs. When tax and customs funds are contributed to the budget - 110, when deducted from the budget - 400.

Budget classification codes (BCC) are internal coding necessary, first of all, for the state treasury, where incoming funds are distributed according to them. Entrepreneurs need these codes to comply with the requirements for processing budget payments, especially taxes and contributions to extra-budgetary funds. These codes are indicated depending on the type of payment in field 104 of the payment order.

| Name | Payment | Penalty | Fine |

| Pension contributions to the Federal Tax Service from employee salaries | |||

| Contributions to compulsory pension insurance | 18210202010061010160 | 18210202010062110160 | 18210202010063010160 |

| Contributions to compulsory social insurance from employee salaries to the Federal Tax Service | |||

| Contributions to compulsory social insurance in case of temporary disability and in connection with maternity | 18210202090071010160 | 18210202090072110160 | 18210202090073010160 |

| Contributions to compulsory health insurance from employee salaries to the Federal Tax Service | |||

| Contributions for compulsory health insurance of the working population | 18210202101081013160 | 18210202101082013160 | 18210202101083013160 |

| Contributions for injuries to the Social Insurance Fund | |||

| Contributions for injuries to the Social Insurance Fund | 39310202050071000160 | 39310202050072100160 | 39310202050073000160 |

| Insurance premiums for individual entrepreneurs for themselves | |||

| In the Pension Fund of the Russian Federation (fixed payment and payment from income 1% - a single BCC) | 18210202140061110160 | 18210202140062110160 | 18210202140063010160 |

| In FFOMS | 18210202103081013160 | 18210202103082013160 | 18210202103083013160 |

| Personal income tax (NDFL) on employee salaries | |||

| Personal income tax on income the source of which is a tax agent, with the exception of income in respect of which tax is calculated and paid in accordance with Articles 227, 227.1 and 228 of the Tax Code of the Russian Federation (Salaries / Vacation Pay / Dividends and other payments to employees) | 18210102010011000110 | 18210102010012100110 | 18210102010013000110 |

| Personal income tax on income received by citizens registered as: – entrepreneurs; – private notaries; – other persons engaged in private practice in accordance with Article 227 of the Tax Code of the Russian Federation. | 18210102020011000110 | 18210102020012100110 | 18210102020013000110 |

| Personal income tax on income received by citizens in accordance with Article 228 of the Tax Code of the Russian Federation | 18210102030011000110 | 18210102030012100110 | 18210102030013000110 |

| Personal income tax in the form of fixed advance payments on income received by non-residents employed by citizens on the basis of a patent in accordance with Article 227.1 of the Tax Code of the Russian Federation | 18210102040011000110 | 18210102040012100110 | 18210102040013000110 |

| Value added tax (VAT) | |||

| VAT on goods (work, services) sold in Russia | 18210301000011000110 | 18210301000012100110 | 18210301000013000110 |

| VAT on goods imported into Russia (from the Republics of Belarus and Kazakhstan) | 18210401000011000110 | 18210401000012100110 | 18210401000013000110 |

| VAT on goods imported into Russia (payment administrator - Federal Customs Service of Russia) | 15310401000011000110 | 15310401000012100110 | 15310401000013000110 |

| Income tax | |||

| Income tax credited to the federal budget | 18210101011011000110 | 18210101011012100110 | 18210101011013000110 |

| Profit tax credited to the budgets of constituent entities of the Russian Federation | 18210101012021000110 | 18210101012022100110 | 18210101012023000110 |

| Income tax upon implementation of production sharing agreements concluded before the entry into force of Law No. 225-FZ of December 30, 1995 and which do not provide for special tax rates for crediting the specified tax to the federal budget and the budgets of constituent entities of the Russian Federation | 18210101020011000110 | 18210101020012100110 | 18210101020013000110 |

| Income tax on the income of foreign organizations not related to activities in Russia through a permanent establishment, with the exception of income received in the form of dividends and interest on state and municipal securities | 18210101030011000110 | 18210101030012100110 | 18210101030013000110 |

| Corporate income tax on income in the form of profits of controlled foreign companies | 18210101080011000110 | 18210101080012100110 | 18210101080013000110 |

| Income tax on income received by Russian organizations in the form of dividends from Russian organizations | 18210101040011000110 | 18210101040012100110 | 18210101040013000110 |

| Income tax on income received by foreign organizations in the form of dividends from Russian organizations | 18210101050011000110 | 18210101050012100110 | 18210101050013000110 |

| Income tax on income received by Russian organizations in the form of dividends from foreign organizations | 18210101060011000110 | 18210101060012100110 | 18210101060013000110 |

| Income tax on income received in the form of interest on state and municipal securities | 18210101070011000110 | 18210101070012100110 | 18210101070013000110 |

| Excise taxes | |||

| Excise taxes on ethyl alcohol from food raw materials (except for distillates of wine, grape, fruit, cognac, Calvados, whiskey), produced in Russia | 18210302011011000110 | 18210302011012100110 | 18210302011013000110 |

| Excise taxes on ethyl alcohol from non-food raw materials produced in Russia | 18210302012011000110 | 18210302012012100110 | 18210302012013000110 |

| Excise taxes on ethyl alcohol from food raw materials (wine, grape, fruit, cognac, calvados, whiskey distillates) produced in Russia | 18210302013011000110 | 18210302013012100110 | 18210302013013000110 |

| Excise taxes on alcohol-containing products produced in Russia | 18210302020011000110 | 18210302020012100110 | 18210302020013000110 |

| Excise taxes on tobacco products produced in Russia | 18210302030011000110 | 18210302030012100110 | 18210302030013000110 |

| Excise taxes on motor gasoline produced in Russia | 18210302041011000110 | 18210302041012100110 | 18210302041013000110 |

| Excise taxes on straight-run gasoline produced in Russia | 18210302042011000110 | 18210302042012100110 | 18210302042013000110 |

| Excise taxes on passenger cars and motorcycles produced in Russia | 18210302060011000110 | 18210302060012100110 | 18210302060013000110 |

| Excise taxes on diesel fuel produced in Russia | 18210302070011000110 | 18210302070012100110 | 18210302070013000110 |

| Excise taxes on motor oils for diesel and (or) carburetor (injection) engines produced in Russia | 18210302080011000110 | 18210302080012100110 | 18210302080013000110 |

| Excise taxes on wines, fruit wines, sparkling wines (champagnes), wine drinks made without the addition of rectified ethyl alcohol produced from food raw materials, and (or) alcoholized grape or other fruit must, and (or) wine distillate, and (or) fruit distillate produced in Russia | 18210302090011000110 | 18210302090012100110 | 18210302090013000110 |

| Excise taxes on beer produced in Russia | 18210302100011000110 | 18210302100012100110 | 18210302100013000110 |

| Excise taxes on alcoholic products with a volume fraction of ethyl alcohol over 9 percent (except for beer, wines, fruit wines, sparkling wines (champagnes), wine drinks produced without the addition of rectified ethyl alcohol produced from food raw materials, and (or) alcoholized grape or other fruit must, and (or) wine distillate, and (or) fruit distillate) produced in Russia | 18210302110011000110 | 18210302110012100110 | 18210302110013000110 |

| Excise taxes on alcoholic products with a volume fraction of ethyl alcohol up to 9 percent inclusive (except for beer, wines, fruit wines, sparkling wines (champagne), wine drinks made without the addition of rectified ethyl alcohol produced from food raw materials, and (or) alcoholized grape or other fruit must, and (or) wine distillate, and (or) fruit distillate) produced in Russia | 18210302130011000110 | 18210302130012100110 | 18210302130013000110 |

| Excise taxes on alcoholic products with a volume fraction of ethyl alcohol over 9 percent (except for beer, wines, fruit wines, sparkling wines (champagnes), wine drinks produced without the addition of rectified ethyl alcohol produced from food raw materials, and (or) alcoholized grape or other fruit must, and (or) wine distillate, and (or) fruit distillate), imported into the territory of Russia | 18210402110011000110 | 18210402110012100110 | 18210402110013000110 |

| Excise taxes on household heating fuel produced from diesel fractions of direct distillation and (or) secondary origin, boiling in the temperature range from 280 to 360 degrees Celsius, produced in Russia | 18210302210011000110 | 18210302210012100110 | 18210302210013000110 |

| Organizational property tax | |||

| Tax on property of organizations not included in the Unified Gas Supply System | 18210602010021000110 | 18210602010022100110 | 18210602010023000110 |

| Tax on property of organizations included in the Unified Gas Supply System | 18210602020021000110 | 18210602020022100110 | 18210602020023000110 |

| Land tax | |||

| Land tax levied on taxable objects located within the boundaries of intra-city municipalities of federal cities of Moscow and St. Petersburg | 18210606031031000110 | 18210606031032100110 | 18210606031033000110 |

| Land tax levied on taxable objects located within the boundaries of urban districts | 18210606032041000110 | 18210606032042100110 | 18210606032043000110 |

| Land tax levied on taxable objects located within the boundaries of inter-settlement territories | 18210606033051000110 | 18210606033052100110 | 18210606033053000110 |

| Land tax levied on taxable objects located within the boundaries of rural settlements | 18210606033101000110 | 18210606033102100110 | 18210606033103000110 |

| Land tax for plots within the boundaries of urban settlements | 18210606033131000110 | 18210606033132100110 | 18210606033133000110 |

| Land tax for plots within the boundaries of urban districts with intra-city division | 18210606032111000110 | 18210606032112100110 | 18210606032113000110 |

| Land tax for plots within the boundaries of intracity districts | 18210606032121000110 | 18210606032122100110 | 18210606032123000110 |

| Transport tax | |||

| Transport tax for organizations | 18210604011021000110 | 18210604011022100110 | 18210604011023000110 |

| Transport tax for individuals | 18210604012021000110 | 18210604012022100110 | 18210604012023000110 |

| Single tax simplified taxation system (STS) | |||

| Tax levied on taxpayers who have chosen income as an object of taxation | 18210501011011000110 | 18210501011012100110 | 18210501011013000110 |

| A tax levied on taxpayers who have chosen as an object of taxation income reduced by the amount of expenses | 18210501021011000110 | 18210501021012100110 | 18210501021013000110 |

| Minimum tax | 18210501021011000110 | 18210501021012100110 | 18210501021013000110 |

| Unified tax on imputed income (UTII) | |||

| UTII | 18210502010021000110 | 18210502010022100110 | 18210502010023000110 |

| UTII (for tax periods expired before January 1, 2011) | 18210502020021000110 | 18210502020022100110 | 18210502020023000110 |

| Unified Agricultural Tax (USAT) | |||

| Unified agricultural tax | 18210503010011000110 | 18210503010012100110 | 18210503010013000110 |

| Unified Agricultural Tax (for tax periods expired before January 1, 2011) | 18210503020011000110 | 18210503020012100110 | 18210503020013000110 |

| Water tax | |||

| Water tax | 18210703000011000110 | 18210703000012100110 | 18210703000013000110 |

| Trade fee | |||

| Trade tax in federal cities | 18210505010021000110 | 18210505010022100110 | 18210505010023000110 |

| Additional tariffs in the Pension Fund of Russia | |||

| Contributions for additional pension insurance (Employees from List 1) | 18210202131061020160 | 18210202131062100160 | 18210202131063000160 |

| Contributions for additional pension insurance (Employees from List 2) | 18210202132061020160 | 18210202132062100160 | 18210202132063000160 |

| Contributions for additional pension insurance (Employees from List 1) | 18210202131061010160 | 18210202131062100160 | 18210202131063000160 |

| Contributions for additional pension insurance (Employees from List 2) | 18210202132061010160 | 18210202132062100160 | 18210202132063000160 |

| Income from the provision of paid services | |||

| Fee for providing information contained in the Unified State Register of Taxpayers | 18211301010016000130 | — | — |

| Fee for providing information contained in the Unified State Register of Taxpayers (when applying through multifunctional centers) | 18211301010018000130 | — | — |

| Fee for providing information and documents contained in the Unified State Register of Legal Entities and in the Unified State Register of Individual Entrepreneurs | 18211301020016000130 | — | — |

| Fee for providing information and documents contained in the Unified State Register of Legal Entities and the Unified State Register of Individual Entrepreneurs (when applying through multifunctional centers) | 18211301020018000130 | — | — |

| Fee for providing information from the register of disqualified persons | 18211301190016000130 | — | — |

| Fee for providing information from the register of disqualified persons (when applying through multifunctional centers) | 18211301190018000130 | — | — |

| Government duty | |||

| State duty on cases considered in arbitration courts | 18210801000011000110 | — | — |

| State duty for state registration of a legal entity, individuals as individual entrepreneurs (if the service is provided by tax authorities), changes made to the constituent documents of a legal entity, for state registration of liquidation of a legal entity and other legally significant actions | 18210807010011000110 | — | — |

| State duty for state registration of a legal entity, individuals as individual entrepreneurs (if the service is provided by a multifunctional center) | 18210807010018000110 | — | — |

| State duty for the right to use the names “Russia”, “Russian Federation” and words and phrases formed on their basis in the names of legal entities | 18210807030011000110 | — | — |

| Payments for the use of natural resources | |||

| Payment for emissions of pollutants into the atmospheric air by stationary facilities | 04811201010016000120 or 04811201010017000120 (if the payment administrator is a federal government agency) | — | — |

| Payment for emissions of pollutants into the atmospheric air by mobile objects | 04811201020016000120 or 04811201020017000120 (if the payment administrator is a federal government agency) | — | — |

| Payment for emissions of pollutants into water bodies | 04811201030016000120 or 04811201030017000120 (if the payment administrator is a federal government agency) | — | — |

| Fines and sanctions | |||

| Monetary penalties (fines) for violation of laws on taxes and fees | — | — | 18211603010016000140 |

| Monetary penalties (fines) for violation of legislation on the use of cash register equipment when making cash payments and (or) payments using payment cards | — | — | 18211606000016000140 |

| Monetary penalties (fines) for administrative offenses in the field of taxes and fees provided for by the Code of the Russian Federation on Administrative Offenses | — | — | 18211603030016000140 |

| Monetary penalties (fines) for violation of the procedure for handling cash, conducting cash transactions and failure to fulfill obligations to monitor compliance with the rules for conducting cash transactions | — | — | 18211631000016000140 |

BCC for penalties and fines on corporate income tax to the regional budget

The regional budget is the financing of the constituent entities of the Russian Federation or the contribution of funds to individual constituent entities of the country. In the code structure, when paying tax funds, the budget is determined by the ninth and tenth digits.

Thus, according to Order of the Ministry of Finance No. 132n, financing of the federal treasury is listed under the number “1101”, and replenishment of the subjects – “1202”. At the legislative level, fees payments are determined by type: calculated tax, penalties, fines, interest. For each type of payment there is a corresponding combination of numbers.

KBC for payment of personal income tax fines by individuals

If a citizen fails to pay penalties on income collection, as well as due to other tax violations, the individual is fined. The size of the latter is regulated by the legislation of the Russian Federation. Depending on the severity and type of crime, the amount of the monetary penalty is calculated. In 2021, KBK 18210102030013000110 applies to pay fines. What is the decryption tax? Payment of the amount of monetary penalties (fines) for the corresponding payment, that is, for non-payment of personal income tax or other tax violation regarding personal income tax.

KBK for payment of penalties

When paying a debt in the form of a penalty for collecting profits, enterprises indicate in the payment slip the number 18210101011012100110 KBK, the decoding of which means that this amount finances the federal budget of the Russian Federation.

But if a company accrues penalties in the region of work, then the debt is considered regional. Accordingly, the code classifying the payment of penalties is KBK 18210101012022100110 for duties based on the profitability of those enterprises that are not included in the consolidated category of payers.

What do the set of numbers in KBK mean?

Upon closer examination of the figures contained in the KBK, one can understand what tax in 2021 according to the KBK 18210101011012100110 will be paid by commercial structures, large and small organizations.

So, let's use an example to see what a set of numbers means. Each code for paying a specific payment has twenty digits. Each figure is responsible for itself (Ministry of Finance No. 65n.) When decoding KBK 182 101 01 01101 2100 110 in 2021, you can understand the following:

- 182, this is the tax authority of the Russian Federation. In this case, the Federal Tax Service.

- 101 means income tax.

- If it costs 01, the payment goes to the federal budget (02 goes to the regional budget).

- 01101 denotes income by classification, 01 is an article, 101 is a sub-item of income.

- 2100 indicates the type of payment; if these numbers are indicated, it means that penalties need to be paid.

- Tax income is reflected in figures of 110.

A detailed examination of the set of KBK numbers shows that each group is responsible for a specific regulatory authority, which means the purpose of payment. In payment documents, reflecting a certain BCC for payment of a fee or a fine, a penalty, it is important to enter all the numbers correctly, otherwise the transferred money will not reach the recipient, and you will have to search for it later and write letters to the Treasury.

If tax is paid, if funds are not deposited on time, the company will be subject to a late payment penalty.

Using the BCC in payment documents, taxpayers need to carefully study the normative act and make sure that a particular BCC is correct and relevant for paying a contribution, duty, or tax.

KBC on fines for UTII

A monetary fine may be imposed on the person imputed if he did not submit a UTII declaration in a timely manner, if the tax was calculated incorrectly, as a result of which the base for calculating the tax was underestimated.

The amount of monetary penalty for a declaration not submitted on time is from five to thirty percent of the outstanding tax burden for each month of delay. At the same time, the lower limit of the fine is 1000 rubles.

BCC for payment of a fine for UTII: 182 1 0500 110 (for 2021).

BCC table for UTII in 2021

| Payment type | KBK |

| Single tax UTII | 18210502010021000110 |

| Penalty | 18210502010022100110 |

| Interest | 18210502010022200110 |

| Fines | 18210502010023000110 |

Entering BCC into payment documentation

The current value of the BCC must be entered in field 104 of the order, where you must enter 20 digits corresponding to the current value of the code for the current year.

In addition to the KBK, the payment order must also include the purpose of the payment, briefly explaining the purpose for which the funds are transferred.

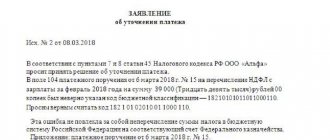

An example of filling out an order when transferring UTII for the second quarter of 2016.

An example of filling out an order when transferring UTII for the second quarter. 2016

Main BCCs used by payers

In addition to income tax, taxpayers must pay insurance premiums and contributions for hired employees. What codes do entrepreneurs and organizations often use?

- Income tax to the regional budget—18210101012021000110.

- Federal fund tax—18210101011011000110.

- Value added tax—18210301000012100110.

- To pay a fine for income tax, indicate - 18210301000013000110.

- Contributions to the Pension Fund for those whose income is more than 300,000—39210202140061200160, less than 300,000—39210202140061100160.

- Contributions to the Pension Fund for employees—39210202010061000160.

- Medical insurance for yourself—39210202103081011160.

- Honey. fear for the employee—39210202101081011160.

- Voluntary contribution to social services fear—39311706020076000180.

These are the main codes where all companies and organizations most often transfer funds. Once again, it is worth remembering that when entering a twenty-digit number into a payment order, you need to be extremely careful. Check that the KBK instructions are correct, otherwise either the operator will not accept the payment, or the money will go to the wrong recipient.

A special field is provided to reflect the BCC in payment orders. It is unchanged, and you won’t have to constantly look for where to add the BCC. To enter the classification code, always use field 104. This is where these numbers are reflected, and in this field you can enter the BCC and leave comments on the payment.

What does the BCC depend on?

In relation to land tax, the BCC depends on where a particular piece of land is located, for which it is necessary to pay it in full or make an advance payment. This rule is regulated by the Order of the Ministry of Finance of Russia dated July 1, 2013. No. 65n.

According to this act, each of the following territories has its own budget classification code:

- intracity municipalities of the cities of Moscow, St. Petersburg and Sevastopol (18210606031031000110);

- urban districts without intra-city division (18210606032041000110);

- urban districts with intracity division (18210606032111000110);

- intracity areas (18210606032121000110);

- inter-settlement territories (18210606033051000110);

- rural settlements (18210606033101000110);

- urban settlements (18210606033131000110).

Detailed instructions on how to rent land are in our material! Who is given a vacated room in a communal apartment first? Find out about it here. Are you looking for a sample apartment exchange agreement? It can be downloaded from this link.

Important points on land tax

Land tax is local, so the budget of the corresponding regional unit must receive it. It must be paid by land owners:

- on the right of ownership;

- those who received them for lifelong use;

- in lifelong inheritable possession.

REFERENCE! This tax does not apply to tenants and those who use land free of charge on a fixed-term basis.

How is land tax calculated?

To determine the tax base, you need to know the following characteristics of the land plot subject to taxation:

- Cadastral value (information is available on the Rosreestr website).

- The owner's share in the rights to this site.

- Ownership coefficient (if the plot has been owned for less than a year).

All this data is multiplied by the tax rate, which depends on the will of the regional authorities.

Notification to individuals

For individuals, the tax authority will calculate everything and send a notification to the place of residence from April to September. You must pay for the notice received before the beginning of October.

ATTENTION! If you find that the tax notice is in error in some way, you need to fill out the application form that will be sent to you along with the notice and send it to the tax office for clarification and recalculation. When the tax office checks everything, it will send you a new notification.

If this document is delayed, lost, or for some other reason does not reach the addressee, do not think that the land tax can be avoided - the law obliges individuals in such cases to independently contact the tax office, unless, of course, you want to get acquainted with fines and penalties .

KBK for UTII

For the imputed tax regime in relation to the payment of a special tax, the BCC is provided for the transfer of the single tax itself, penalties for late payment, as well as various types of fines for violation of the law.

KBK for payment of a special tax of the imputed regime: 182 1 05 02010 02 1000 110 (current for 2021).

According to the specified BCC, not only the calculated special tax payable for the quarter is transferred, but also arrears, tax debt, and recalculation amounts.