Basic information about the document

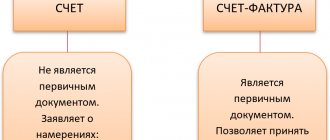

An invoice is the documentary basis for accounting, calculation and deduction of VAT. An invoice is issued by the supplier - the VAT payer - to its customers: companies or entrepreneurs. In other words, any transaction for the sale of goods and services subject to VAT must be accompanied by the preparation of an invoice. For the buyer, this document serves as the basis for reducing his own VAT payable, that is, for a tax deduction.

If the buyer does not pay VAT, the supplier may not issue him invoices. However, to do this, an agreement must be signed between the parties that no invoices will be issued. Suppliers who do not pay VAT are also exempt from the need to prepare this document.

Liquidation of organizations of all forms of ownership, firms, enterprises

The liquidation procedure of an organization is carried out to terminate its work without further transfer of rights and obligations to other persons in the order of succession. Upon completion of the process, creditors do not have the right to demand fulfillment of obligations from the company that caused its closure.

When providing services to support these procedures, Strategy specialists provide professional legal advice, assist in collecting and processing documents, conduct legal reviews, and also register changes in tax structures. They know exactly what to do when liquidating a company, even in the most difficult cases.

Regulatory regulation

The legal basis for the application of the document in question is the Tax Code. Paragraph 3 of Article 169 defines the cases in which an invoice is issued. This includes transactions that are subject to VAT, as well as the export of non-taxable goods from Russia to the territory of the Customs Union.

The document has a specific form, set out in Resolution No. 1137. The same act contains the rules in accordance with which invoices should be filled out. The form of the document and the procedure for filling it out are constantly being improved, and therefore changes are being made to the resolution.

Paper and electronic formats

Today, invoices are generated in the classic form, that is, on paper or in electronic format. Such an invoice, like its paper counterpart, must be drawn up in a strictly prescribed form and contain all the necessary details.

When is an electronic invoice issued? This is possible if the following conditions are met:

- an agreement has been concluded between organizations on the preparation of electronic invoices;

- counterparties have the technical ability to exchange documents in the established format via the Internet.

Otherwise there are no restrictions. An electronic document completely replaces a paper one, provided that it is drawn up in the form and certified with a digital signature.

When is an invoice issued?

Most often, the primary document in question is issued by the seller when carrying out transactions that, in accordance with tax legislation, are subject to VAT. The sale of most goods and services, including gratuitous transfers, is subject to taxation. But there are exceptions - they are listed in Article 149 of the Tax Code of the Russian Federation.

Also, companies and individual entrepreneurs working with VAT are required to generate invoices upon receipt of payment for future shipments. Such documents are usually called advance invoices.

In addition, VAT payers are required to issue invoices when exporting to the EAEU countries.

There are cases when the paper is issued by an entity that does not pay VAT. Such an obligation arises for companies and individual entrepreneurs if they, on their own behalf, sell goods that belong to another organization - a VAT payer. We are talking about mediation activities under commission agreements and the like.

The procedure for issuing a document during implementation

Let's consider a basic example - the seller releases the goods, and the buyer makes payment upon delivery. The invoice is issued within 5 days, starting from when the goods were shipped, services were provided or work was performed.

One copy of the invoice is issued for the supplier himself, the second for the buyer. The document must be registered in the Invoice Journal (hereinafter referred to as the Journal). In addition, the seller makes an entry in the Sales Book and indicates the details of the corresponding invoice. And the buyer, accordingly, makes a similar entry in his Purchase Book.

Submission deadlines

Tax Code of the Russian Federation in paragraph 3 of Art. 168 regulates the period for issuing an invoice, which is 5 calendar days from the date of:

- receiving partial or full payment for the performance of work, services, purchase of products or assignment of rights to property;

- issuing products, providing services, works, vesting rights to property.

Moreover, the five-day period is counted starting from the day following the day of issue of goods, provision of services, work, and vesting of property rights. In Art. 6.1 of the Tax Code of the Russian Federation also stipulates that if the last day of the calculated period falls on a weekend or holiday, then the end of the period is postponed to the next working day that follows this one.

It is possible for the seller to issue an invoice once for all goods sold at the end of a month.

Here, however, it must be taken into account that such a privilege is given to enterprises that operate in areas that produce uninterrupted regular supplies to one counterparty.

When is an advance invoice issued?

If the buyer makes an advance payment for a future delivery, the supplier must also issue an invoice. In this case, it does not matter whether the buyer made the payment in full or in part - the document is issued for the transferred amount. The seller charges VAT on the prepayment received, and the buyer, subject to certain conditions, can claim his input tax as a deduction.

When is an advance invoice issued? The issuance period is 5 days, calculated from the date on which the advance payment was received. The document is taken into account by the supplier in the following order:

- the advance invoice is reflected in the Sales Book;

- when the goods are sold, a shipping invoice, that is, a “real” invoice, is drawn up;

- the shipping document is noted in the Sales Book for the entire amount of delivery;

- at the same time, an entry regarding the advance invoice is made in the Purchase Ledger.

The buyer has a similar document accounting procedure, but with the opposite sign: instead of entries in the Purchase Book, there is a Sales Book, and vice versa. Both the buyer and the seller's documents are also subject to registration in the Journal.

About invoices, invoice journals, purchase and sales books

S.V. Fourth

www.nalogi.com.ru/Russia.html

The invoice is an important formal

a document serving as the basis for accepting the submitted VAT amounts for deduction or reimbursement.

Having an invoice and filling it out correctly is a prerequisite

for deduction or refund of VAT.

Indeed, in accordance with Article 169 of the Tax Code of the Russian Federation, invoices drawn up and issued in violation of the procedure established by paragraphs 5 and 6 of this article of the Tax Code of the Russian Federation cannot be the basis for accepting tax amounts presented to the buyer by the seller for deduction or reimbursement.

Thus, the legislator actually imposed on the buyer

control over the seller in two directions:

1) drawing up an invoice in the prescribed manner;

2) issuing an invoice in the prescribed manner.

Moreover, it is the buyer who is interested in such control, since only his economic interests will be infringed if the tax authority reveals violations of the established procedure.

FORMAL SIGNS OF A CORRECTLY COMPLETED INVOICE

These signs are indicated in the Tax Code of the Russian Federation and in the Rules for maintaining logs of received and issued invoices, purchase books and sales books when calculating value added tax, approved by Decree of the Government of the Russian Federation of December 2, 2000 N 914 “On approval of the Rules for maintaining accounting logs received and issued invoices, purchase books and sales books when calculating value added tax" ( hereinafter referred to as the Rules

):

1) the buyer must have the original

invoices.

- In the letter of the Ministry of Taxes and Taxes of the Russian Federation dated November 23, 1997 N PV-6-03/393 “On invoices” it was noted that in order to prevent unjustified payments from the budget on false invoices, the use of facsimile copies of them (by fax, e-mail and etc.);

all required details must be filled in

invoices established by paragraphs 5 and 6 of Article 169 of the Tax Code of the Russian Federation. This:

- 1) serial number and date of issue of the invoice.

The procedure for numbering invoices (in contrast to the canceled Decree of the Government of the Russian Federation dated July 29, 1996 N 914 “On approval of the Procedure for maintaining invoice journals for value added tax calculations”) is not established by the Rules. Therefore, organizations can number invoices as they wish;

2) name, address and identification numbers of the taxpayer and buyer;

3) name and address of the shipper and consignee.

- The name of the seller, consignor, consignee and buyer, as well as the location of the buyer and seller must be indicated in accordance with their constituent documents

. At the same time, the actual address may be indicated for the consignor (if the seller and the consignor are not the same legal entity), and the postal address may be indicated for the consignee.

In cases where there are no concepts of consignor and consignee (for example, when providing services), a dash is placed in the corresponding lines (letter of the Ministry of Taxation of the Russian Federation dated May 21, 2001 N VG-6-03/404 “On the use of invoices when calculating value added tax price");

4) number of the payment and settlement document.

- It is placed in case of receipt of advance or other payments on account of upcoming deliveries of goods (performance of work, provision of services);

5) name of the goods supplied (shipped) (description of work performed, services provided) and unit of measurement (if it is possible to indicate it);

6) the quantity (volume) of goods (work, services) supplied (shipped) according to the invoice based on the units of measurement adopted for it (if it is possible to indicate them);

7) price (tariff) per unit of measurement (if it is possible to indicate it) under the agreement (contract) excluding tax, and in the case of using state regulated prices (tariffs) that include tax, taking into account the amount of tax;

the cost of goods (work, services) for the entire quantity of goods supplied (shipped) according to the invoice (work performed, services rendered) without tax;

the cost of goods (work, services) for the entire quantity of goods supplied (shipped) according to the invoice (work performed, services rendered) without tax;

9) the amount of excise duty on excisable goods.

- When implementing excisable goods and (or) excisable mineral raw materials

, operations for the implementation of which, in accordance with Article 183 of the Tax Code of the Russian Federation, are exempt from taxation, invoices are issued without allocating the corresponding excise tax amounts. At the same time, the inscription or stamp “Without excise tax” is made on these documents (clause 3 of Article 198 of the Tax Code of the Russian Federation);

For organizations that sell excisable goods, but are not excise taxpayers

, there is no basis for allocating the amount of excise tax in invoices (letter of the Ministry of Taxation of the Russian Federation dated April 10, 2001 N VG-6-03/284);

10) tax rate;

11) the amount of tax presented to the buyer of goods (works, services), determined based on the applicable tax rates.

- When selling goods (works, services), operations for the sale of which in accordance with Article 149 of the Tax Code of the Russian Federation are not subject to taxation (exempt from taxation), as well as when the taxpayer is exempted in accordance with Article 145 of the Tax Code of the Russian Federation from fulfilling the duties of a taxpayer, settlement documents, primary accounting records documents are prepared and invoices are issued without allocating the corresponding tax amounts. In this case, the corresponding inscription or stamp “Without tax (VAT)” is made on these documents (clause 5 of Article 168 of the Tax Code of the Russian Federation);

12) the cost of the total quantity of goods supplied (shipped) according to the invoice (work performed, services rendered), taking into account the amount of tax;

13) country of origin of the goods;

14) number of the cargo customs declaration.

Free lines are subject to mandatory crossing out (clause 2.9 of the Regulations on Documents and Document Flow in Accounting, approved by the USSR Ministry of Finance on July 29, 1983 N 105).

3) the invoice must be signed

manager and chief accountant.

- It is also allowed to sign the invoice to other officials of the organization, but in this case such persons must be listed in the order for the organization.

If the head of an organization, on the basis of subparagraph “d” of paragraph 2 of Article 6 of Federal Law dated November 21, 1996 N 129-FZ “On Accounting,” keeps accounting records personally, then an invoice can be issued without the signature of the chief accountant (resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated July 9 .02 N 58/02).

When issuing an invoice by an individual entrepreneur, the invoice is signed by the individual entrepreneur indicating the details of the certificate of state registration of this individual entrepreneur.

Facsimile imprints of signatures on an invoice are completely unacceptable as they cannot verify the authenticity of the invoice. In addition, this contradicts Article 9 of the Federal Law of November 21, 1996 N 129-FZ “On Accounting”, according to which primary accounting documents must contain personal signatures of persons (and not facsimiles) responsible for the execution of a business transaction and the correctness of its execution.

4) an invoice issued before 01/01/02 must be certified by a seal

organizations. After this date, in connection with the changes made to paragraph 6 of Article 169 of the Tax Code of the Russian Federation, a stamp on the invoice is not mandatory.

5) the invoice should not contain erasures or blots

.

- In accordance with paragraph 29 of the Rules, invoices that have erasures and erasures are not subject to registration in the purchase book and sales book.

Corrections

entered into invoices must be certified by the signature of the manager and the seal of the seller, indicating the date of the correction.

Invoices must be drawn up when performing transactions that are recognized as the object of taxation, including those that are not subject to taxation (exempt from taxation)

. They are not compiled for transactions involving the sale of securities (with the exception of brokerage and intermediary services), as well as by banks, insurance organizations and non-state pension funds for transactions that are not subject to taxation (exempt from taxation) in accordance with Article 149 of the Tax Code of the Russian Federation.

ABOUT THE DEADLINES FOR SUBMISSION OF INVOICES

By virtue of paragraph 3 of Article 168 of the Tax Code of the Russian Federation, invoices are issued no later than five days counting from the date of shipment of goods (performance of work, provision of services).

At the same time, for certain industries associated with continuous long-term supplies to the same buyer (continuous supply of goods and provision of transportation services to the same buyers of electricity, oil, gas; provision of telecommunications services, banking services; daily multiple sales in address of one buyer of bread and bakery products, perishable food products, etc.), it is allowed to draw up invoices in accordance with the terms of the supply agreement concluded between the seller and the buyer of goods (services), acts of reconciliation of completed deliveries and issuance of invoices to buyers simultaneously with payment and settlement documents, but at least once a month and no later than the 5th day of the month following the previous month. It must be borne in mind that the preparation of invoices and their registration in the sales book must be carried out in the tax period in which the sale of these goods (provision of services) took place in accordance with the accounting policy adopted by the organization for tax purposes (letter from the Ministry of Taxes of the Russian Federation dated 05.21.01 N VG-6-03/404 “On the use of invoices when calculating value added tax”).

Mass media (newspapers, magazines) that sell their products to legal entities are allowed to issue invoices to each subscriber once during the period for which the subscription fee is received (month, quarter, half-year, year) - see letter from the Ministry of Finance of the Russian Federation dated August 13. 97 N 04-03-11.

In general, I think we should try to adhere to the following procedure for preparing and providing invoices to customers: 1) an invoice is drawn up at the time of the transaction, and if this is not possible, immediately after its completion; 2) an invoice is issued to the buyer as soon as possible, but no later than the end of the corresponding VAT tax period (in the most extreme case - no later than the 19th day of the month following the tax period) - so that the buyer can legally take VAT into account in the calculations .

In conclusion, it should be noted that there are still cases when organizations, in order to receive an advance payment for goods (products, works, services), issue buyers not an invoice, but an invoice. This is not true, since in this case the invoice should be issued only after receiving the advance payment.

and it is then that it is registered in the sales book (clause 18 of the Rules).

FEATURES OF DRAFTING INVOICES FOR THE EXECUTION OF AGREEMENTS OF DIRECTION, COMMISSION OR AGENCY AGREEMENT

These features are given in the letter of the Ministry of Taxes of the Russian Federation dated May 21, 2001 N VG-6-03/404 “On the use of invoices when calculating value added tax.” Namely:

1. When selling goods (works, services) under an agency agreement

the invoice on behalf of the principal is issued in the name of the buyer.

2. When implemented by an intermediary acting on his own behalf

, goods (works, services) of the principal, principal, the invoice is issued by the intermediary in two copies

on its own behalf

.

- The number of the specified invoice is assigned by the intermediary in accordance with the chronology of invoices issued by him. One copy is handed over to the buyer, the second is filed in the journal of issued invoices without registering it in the sales book. The principal (principal) issues an invoice in the name of the intermediary with numbering in accordance with the chronology of invoices issued by the principal (principal). This invoice is not recorded in the intermediary's purchase book.

The indicators of the invoice issued by the intermediary to the buyer are reflected in the invoice issued by the principal (principal) to the intermediary and registered in the sales book of the principal (principal).

3. The intermediary issues a separate invoice to the principal, principal, and principal for the amount of his remuneration

under a commission agreement, commission agreement, agency agreement. This invoice is registered in the prescribed manner with the attorney, commission agent, and agent in the sales book, and with the principal, principal, and principal in the purchase book.

4. When purchasing goods (works, services) through an attorney (agent)

The basis for the principal (principal) to deduct value added tax on purchased goods (works, services) is an invoice issued by the seller in the name of the principal (principal).

5. If the invoice is issued by the seller in the name of the commission agent (agent), then the principal (principal) has the basis for deducting value added tax

is the invoice received from the intermediary. An invoice is issued by the intermediary to the principal, the principal, reflecting the indicators from the invoice issued by the seller to the intermediary. Both invoices from the intermediary are not recorded in the purchase book and the sales book.

- The commission agent and the agent can indicate the amount of intermediary remuneration in one invoice with the cost of goods (work, services) on separate lines indicating the corresponding VAT amounts.

When an intermediary sells on his own behalf to one buyer goods (works, services) of the principal or principal simultaneously with the sale of his own goods (works, services) to this buyer

the intermediary can issue a single invoice for the specified goods (work, services).

FEATURES OF COMPLETION OF INVOICES BY ORGANIZATIONS WITH SEPARATE STRUCTURAL DIVISIONS

These features are given in the letter of the Ministry of Taxes of the Russian Federation dated May 21, 2001 N VG-6-03/404 “On the use of invoices when calculating value added tax”:

1) invoices for goods shipped (work performed, services rendered) are issued to customers directly by separate structural divisions. In this case, invoices must be certified by the signatures of persons authorized to do so by order of the organization, as well as the seal of a separate division (until 01/01/02);

2) invoices are numbered in ascending order for the organization as a whole. It is possible to both reserve numbers as they are selected, and assign composite numbers with the index of a separate division;

3) journals of received and issued invoices, purchase books and sales books are maintained by structural divisions in the form of sections of unified accounting journals, unified purchase and sales books of the organization;

4) for the reporting tax period, the specified sections of the books of purchases and sales are presented as separate divisions for the registration of unified books of purchases and sales of the taxpayer and the preparation of value added tax declarations.

FEATURES OF PREPARATION OF SOME OTHER INVOICES

1. When selling an enterprise as a whole as a property complex, a consolidated invoice is drawn up in the manner established by paragraph 4 of Article 158 of the Tax Code of the Russian Federation.

2. If taxpayers exempt from performing duties related to the calculation and payment of tax in accordance with Article 145 of the Tax Code of the Russian Federation or taxpayers applying exemption from taxation of transactions provided for in Article 149 of the Tax Code of the Russian Federation issue an invoice to the buyer with the allocation of VAT, then they will have to pay to the budget the amount of VAT indicated in the corresponding invoice (clause 5 of Article 173 of the Tax Code of the Russian Federation).

3. In the case of shipment to the buyer of a large number of items of goods for which invoices and specifications are issued, column 1 of the invoice can be drawn up in the form of a register of these documents indicating the necessary details and attaching them to the invoice. This is what the Department of Tax Administration of the Russian Federation for Moscow thinks (letter dated November 14, 2001 N 02-11/52362).

4. Tenants of state (or municipal) property draw up an invoice in one copy marked “rent of state (or municipal) property.” The compiled invoice is registered in the sales book at the time of actual transfer of rent and value added tax to the budget. In the purchase book, an invoice is recorded only for that part of the rental payment that is subject to write-off in a given reporting period for production and distribution costs and in the corresponding share for value added tax. This procedure is set out in the letter of the Ministry of Taxes of the Russian Federation dated 02.04.97 N 03-4-09/21 “On the use of invoices for VAT calculations when leasing state and municipal property.”

JOURNALS OF ACCOUNTING OF RECEIVED AND ISSUED INVOICES

The text of the Rules does not define what constitutes “log books of received and issued invoices.” Since these “logs” store

invoices (clause 1 of the Rules), then we can assume that these are ordinary files of invoices.

In this case, from paragraph 2 of the Rules it follows that buyers must file invoices as they are received from sellers, and sellers must file them in chronological order

.

And there should be two folders: for received and issued invoices. In this case, the log of received invoices should contain only originals

, and the log of issued invoices should contain

second copies

of invoices.

By virtue of paragraph 6 of the Rules, the journals for recording received and issued invoices must be bound together and their pages numbered. Obviously, this should be done after the end of a tax period* (and certainly before a tax audit). Unlike the purchase book and sales book, these journals do not have to be sealed, since this is not established by the Rules.

____

*Depending on the number of invoices - monthly, quarterly or annually.

PURCHASE BOOK AND SALES BOOK

Both books must be bound, the pages numbered and sealed. This is done before opening the book.

If there are a large number of buyers or sellers, it is allowed to maintain a purchase book and a sales book using a computer. In this case, a new book is created for each tax period, since in accordance with paragraph 28 of the Rules, after the expiration of the tax period, but no later than the 20th day of the month following the tax period (month, quarter), the purchase book and the sales book are printed, the pages are numbered, laced and sealed.

Clause 19 of the Rules states that in the sales book

invoices are registered, issued in one copy by the recipient of financial assistance, funds to replenish special-purpose funds, to increase income or otherwise related to payment for goods (performance of work, provision of services), interest on bills, interest on a trade loan in part, exceeding the interest rate calculated in accordance with the refinancing rate of the Central Bank of the Russian Federation, insurance payments under insurance contracts for the risk of non-fulfillment of contractual obligations. When applying this clause, it is necessary to take into account that these amounts, in accordance with Article 162 of the Tax Code of the Russian Federation, must be associated with settlements for payment for goods (work, services).

In the sales book

There is column 9 “P/n from the purchase book”. However, the data in this column may not be enough to correctly identify previously purchased goods (works, services). For example, if the purchase related to previous years. Obviously, in this case, additional information will have to be entered in column 9. However, the best way out, I think, would be to introduce a new right-most “Notes” column in both books. In this column you could make any entries that would make working with books easier. As a matter of fact, no one is preventing enterprises from introducing such a column on their own.

ORGANIZATIONAL EVENTS

1. If the head of an organization wants, in accordance with paragraph 6 of Article 169 of the Tax Code of the Russian Federation, officials of the organization (including separate divisions) to receive the legal right to sign invoices, then he must issue a corresponding order or issue a power of attorney.

2. The manager, by order, may entrust to a person authorized by him control over the correct maintenance of the purchase book and sales book (clauses 15 and 27 of the Rules).

3. The records of purchases and sales must be preserved for a full period of 5 years from the date of last entry.

4. The procedure for preparing invoices, books of purchases and sales in separate divisions must be reflected in the accounting policy of the organization for tax purposes (letter of the Ministry of Taxes of the Russian Federation dated May 21, 2001 N VG-6-03/404 “On the use of invoices in settlements for value added tax").

______________

Write a letter to the author.

c Website of Russian Taxpayers (new edition of the article), 10.17.2002. c Magazine “Taxes and Payments”, 2001, N 1. — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — Index 73869 according to the “Newspapers, Magazines” catalog (Rospechat). Subscribe at any post office. Internet subscription: www.nalogi.com.ru/Russia.html — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — —

When an intermediary issues an invoice

Let us separately mention the peculiarities of working with invoices of commission agents and other intermediaries (agents, forwarders, attorneys). When selling the goods of the principal with VAT on his own behalf, the commission agent must draw up an invoice and highlight the amount of tax in it. This will allow the buyer to claim their input tax as a deduction. Moreover, an invoice should also be issued if the commission agent himself does not pay VAT, for example, being on a simplified taxation system. The fact is that in this case, the commission agent, being an intermediary between the buyer and the owner of the goods, actually takes on the latter’s function in calculating VAT and drawing up documents.

The commission agent registers the exposed document only in the Journal. The second copy is intended for the buyer. The commission agent transfers the document details to the principal, and he issues an invoice to the intermediary himself. In this case, the document must have the same number that the commission agent assigned to it. He notes the received invoice in the Journal.

If a commission agent buys goods from a third party for a VAT payer, he re-issues an invoice issued by the seller to his address. In this case, the received and issued invoices should also be recorded in the Journal without being reflected in the Books.

If the displayed document needs to be changed

In practice, it often happens that changes have to be made to documents. For example, there was a shortage of goods or its price changed. This is also required when an error is found in the invoice.

To change the information in the issued document, corrected and adjustment invoices are drawn up. The first is simply a new version of the document that contains the correct information. The corrected invoice is issued within three years from the period of issue of the original document. This is due to the right of the buyer to claim input tax deduction within a specified period. The corrected document exists independently and completely replaces the one in which the incorrect data was indicated. It is issued in cases where it is necessary to correct an error that did not lead to a change in the amount. For example, the supplier incorrectly indicated the buyer's name or tax rate. If incorrect information in the invoice does not make deduction impossible, then a corrected document does not need to be drawn up.

In what cases is a correction invoice issued? When the transaction amount is adjusted, for example, due to a change in the cost of the product. In this case, an agreement must be concluded between the parties to change the amount (annex to the agreement, act, decision). The adjustment document is drawn up for the amount of changes and is an addition to the original one.

It happens that the supplier sold several batches of goods to one buyer and issued a separate invoice for each. However, it happened that the amount in all deliveries needed to be changed. How many invoices are issued for adjustments? In this situation, there is no need to draw up several documents - the seller can draw up one for all changes addressed to this buyer.

Accounting info

This situation may occur when the buyer has made an advance payment and asks the seller to draw up documents. If the seller meets the buyer halfway, then he provides a disservice to his client, since in this case one of the necessary conditions for the deduction is not met - the service has not yet been provided, therefore, VAT cannot be claimed for deduction in the current tax period, and only after registration. During an audit, tax authorities may notice such a discrepancy, which will cause additional penalties and sanctions.

If the invoice date coincides with the shipment date, then this option is the most preferable for both the seller and the buyer, since both primary documents (invoices, certificates of work performed) and invoices have the same number, which does not cause disagreements when reconciliation between counterparties, and there are also no claims from the tax authorities. This is ideal. However, in practice this ideal state of affairs is often not observed.

Violation of rules and responsibility

What are the risks for a company or individual entrepreneur for violations related to the described document? The law stipulates the deadlines for issuing an invoice, but does not provide for direct liability for exceeding them. But the absence of an invoice is regarded as a serious flaw in accounting. Absence means failure to issue a document in the quarter in which the transaction took place.

For this, the taxpayer may be punished in accordance with Article 120 of the Tax Code of the Russian Federation. If this violation is detected for the first time, the organization may receive penalties in the amount of 10 thousand rubles. If the absence of invoices is revealed in several quarters, the amount of the fine will triple. And in the case where this violation led to an understatement of tax, the fine will be 1/5 of the amount of the underpayment, but not less than 40 thousand rubles.

It must be said that it is quite difficult to “forget” about an invoice when selling a product or service. Even if this happens, the buyer will definitely remind him of the need to draw up a document, because without it he will not be able to deduct VAT. With an invoice for an advance payment, everything is different. Buyers do not always claim VAT deduction from the advance payment, so they do not ask for an invoice. In such a situation, some accountants do not consider it necessary to issue them. They reason like this: receipt of the advance and shipment occur in the same quarter (in most cases), so why issue an interim document? However, the Federal Tax Service considers this a violation if more than five days pass between the receipt of the advance payment and the shipment of the goods.

Subjective opinion

“The letters from the Ministry of Finance are primarily explanatory comments, but in no way legal or by-laws. To be guided by the opinion of officials in this matter or by one’s own considerations is a personal matter for each taxpayer. Moreover, the letter of the Ministry of Finance dated 08/26/2010 No. 03−07−11/370 is outdated: it has no relation to the current edition of the Tax Code, since the text of the letter contains a direct reference to the edition of the code valid until 01/01/2010,” explains Tamara Mokeeva.

Finally, in the same letter, the Ministry of Finance itself notifies that “the opinion provided is of an informational and explanatory nature and does not prevent one from being guided by the norms of legislation on taxes and fees in an understanding that differs from the interpretation set out in this letter.”

Why is it important to follow the design?

The document to which this article is devoted is necessary for the buyer to claim VAT deduction. If critical errors are made in it, the tax service will not recognize the deduction. This means that the company will have to pay additional taxes, and in the worst case, also pay a fine. Therefore, when receiving an invoice, it is important to carefully check its basic details.

To be fair, we note that not every mistake will result in a denial of the deduction. There are a number of transaction parameters that must be identified by the invoice, namely:

- buyer and seller;

- object of the contract;

- cost of goods (services) or advance payment amount;

- VAT rate and amount.

If the specified parameters are determined from the invoice, then a deduction can be claimed on it, despite other errors. Having received a refusal from the Federal Tax Service, the taxpayer can safely go to court. However, if the supplier made an error when generating the invoice, for example, in the cost of the goods or the amount of tax, then the buyer may not count on VAT preferences.

So, an invoice is very important for calculating VAT from the supplier and deducting its incoming part from the buyer. It is necessary to monitor the current form of the document, because it changes periodically. And it is extremely important to follow the procedure and deadlines for its preparation, as well as to avoid critical errors that will lead to non-recognition of the deduction from the buyer.