There are now fewer and fewer entrepreneurs and accountants who fill out declarations manually, because accounting programs and online services allow you to do this in one click. But if you are one of the Old Believers, you like to fill out everything manually and are not ready to delegate to anyone the filling out of the declaration under the simplified tax system for 2021, then here are complete instructions from the “My Business” service.

First, let's talk about the deadlines for submitting the declaration. If you have a limited liability company (LLC), then you need to submit the declaration no later than March 31. And if you have the status of an individual entrepreneur, then get ready to submit your reports by April 30.

Now let's move on to a more complex topic - the formation of the declaration itself.

To prepare the report, you will need the following data:

- about income and expenses for the reporting year (if you use the simplified tax system “Income”, then only about income). They can be taken from KUDiR or from a bank statement, if all income and expense transactions in the reporting year passed only through a current account.

- about insurance premiums paid in the reporting year.

Reports for 2021 must be submitted in the form approved by Order of the Federal Tax Service of Russia No. ММВ-7-3/99 dated 02/26/2016. In 2019, nothing has changed in the rules for filling out the declaration.

Important! If you like to work the old fashioned way and have not yet forgotten how to write with a pen, take only black, blue or purple ink and do not use a stroke - this is prohibited.

If you are an advanced PC user, then when filling out, use the Courier New font with a height of 16-18 points. Fill out text fields with printed capital letters, indicate one character in one familiar place, and fill in empty familiar spaces with dashes.

The declaration consists of sections:

- title page - fill out everything;

- 1.1, 2.1.1., 2.1.2 – for the “Revenue” object;

- 1.2, 2.2 – for the object “Income minus expenses”.

Please note that the form contains line-by-line explanations, from which you can see where you need to take the data from, what to add or subtract with what. Fill in the fields from left to right, starting from the leftmost cell.

Here you fill in the details of the individual entrepreneur/LLC and the tax authority.

If you have a non-standard situation, a list of codes for filling out the title page is in the ninth section of the “Procedure for filling out the declaration.”

What to include in the title page fields of a standard annual report:

| Field name | What information to enter |

| TIN | TIN of an entrepreneur or organization. |

| checkpoint | Organizations enter their checkpoints, entrepreneurs put dashes. |

| Correction number | “0 — -” if this is the first version of the declaration, “001” if the first adjustment, etc. |

| Taxable period | "34" for annual declaration. |

| Reporting year | “2018” if the report is for 2021. |

| Provided to the tax authority (code) | The Federal Tax Service code where the individual entrepreneur or LLC is registered, for example, “1651”. |

| Location code | “120” for entrepreneurs, “210” for organizations. |

| Code of type of economic activity according to OKVED | The code of the main activity indicated in the registration documents, for example, “36.13”. |

| Reorganization form, liquidation (code) | In general, do not fill in, put a dash. This field is intended only for companies undergoing reorganization or liquidation. |

| TIN/KPP of the reorganized organization | In general, they don’t fill it out either. |

| Contact phone number | Telephone number of an individual entrepreneur or organization. |

In the lower left block, enter code “1” if you submit the declaration yourself, and “2” if through a representative. Please enter your full name below. the head of the organization, if you have an LLC. Individual entrepreneurs put dashes in this field.

This is what a completed title page for an individual entrepreneur looks like:

Start filling out from section 2.1.1, because section 2.1 contains summary data and should be completed last.

Filing a declaration under the simplified tax system in 2021

The developed declaration form for “simplified” is essentially a calculation of the tax payable to the budget, and therefore must be completed and submitted to the Federal Tax Service within the established time frame. The frequency of submitting the form is once a year, but the deadlines depend on the organizational form: companies using the simplified tax system are required to report no later than March 31 of the year following the reporting year (due to the coincidence with a holiday, the reporting deadline for 2021 is 04/01/2019 .), for individual entrepreneurs the deadline is no later than April 30.

Tax payment is made by quarterly transfer of advance payments (for 1 quarter, half a year, 9 months). These calculations are not declared, they are taken into account in the annual document drawn up, and then the final amount of tax payable is calculated based on the results of work for the year.

Read also: Insurance premiums for the simplified tax system in 2021

Results

Mandatory annual reporting for any simplified tax system is the simplified taxation system (STS) declaration. LLCs always, and individual entrepreneurs if they have hired employees, must submit reports related to the presence of such employees and the payment of income to them. The LLC, in addition, has the obligation to submit accounting reports and (if there are grounds for assessment) - declarations for property tax, calculated from the cadastral value, land and transport taxes.

Sources: Tax Code of the Russian Federation

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Declaration under the simplified tax system for 2021

The document form was approved by order of the Federal Tax Service dated February 26, 2016 No. ММВ-7-3/99 and is still relevant. The simplified taxation system is used in two “modifications”, depending on the selected tax object:

- simplified tax system “Income” with a tax of 6% of the income received during the year on the simplified tax system;

- STS “Income minus expenses” with a tax of 15% of the difference between income and expenses.

This division is also reflected in filling out the declaration. The form is universal and contains sheets for both types of simplified taxation system, but depending on the option used, different pages are filled out:

- “Simplers” on the simplified tax system “Income” draw up the title page and sections 1.1, 2.1.1, 2.1.2 (when paying the trade fee) and 3 (if there were targeted income).

- For the simplified tax system “Income minus expenses”, sections 1.2, 2.2 and 3 are provided.

Only completed sheets should be included in the declaration, numbering them consecutively.

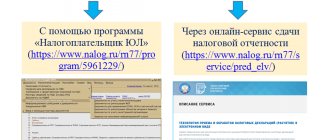

Where and in what form is the declaration sent?

The declaration is sent to the inspectorate at the place of residence of the individual entrepreneur or the location of the company. This can be done in three ways: in person, by mail or via the Internet. The third option is the most convenient for the payer. Through the Federal Tax Service website you can fill out the simplified tax system declaration online - 2018 for free. However, most often declarations are sent using services from electronic document management operators with whom an agreement is concluded. In both cases, such reporting will need to be signed electronically by an authorized person. Most often, this is the head of the company or the entrepreneur himself.

One of the online reporting services is Kontur.Extern, with the help of which entrepreneurs can create and submit a simplified tax return according to the simplified tax system. Kontur.Extern helps with filling out the form and checks it for errors before sending, and then shows the current status of the declaration.

Filling out a declaration according to the simplified tax system

We will briefly list all the details that need to be filled in by the “simplified” and will focus on calculating the tax and reflecting its amount in the document.

The title page contains information about the declarant. The TIN of companies contains 10 categories, individual entrepreneur – 12. The checkpoint is assigned only to legal entities, so the entrepreneur crosses out this field.

The title of the report is followed by the number of the adjustment - the primary report is “0”, the clarifying report is in numerical order, for example, the first adjusting report is numbered as “1”, the second – “2”, etc.

The period code for the declaration for the year is “34”; the same line indicates the year for which the report is being submitted. Below is the number of the Federal Tax Service Inspectorate, and on the right is encrypted its location, for example, code “120” indicates that the report is sent to the Federal Tax Service Inspectorate at the place of residence of the individual entrepreneur, and “210” - at the location of the company.

Next, indicate the name of the company or full name of the entrepreneur, the code of the main type of activity according to OKVED. If the company was reorganized, then in the following fields indicate its form before the transformation and the details of the former organization. Be sure to record the contact telephone number of the declarant, the number of sheets making up the declaration, as well as the number of sheets of documents attached to it, if any.

The lower third of the title page on the left is filled in by the declarant. It reflects information about who certifies the information specified in the declaration (“1” is the payer himself, “2” is his representative), the right part is intended for marks from the Federal Tax Service.

Having filled out the title, they proceed to the preparation of sections of the declaration, which, as we mentioned, are filled out in different ways and this depends on the form of the special regime applied.

Read also: Do I need to submit KUDIR to the tax office in 2021?

OKVED

In the field “Code of the type of economic activity according to the OKVED classifier”, indicate the code of the type of entrepreneurial activity. This code can be viewed in the extract from the Unified State Register of Legal Entities (USRIP), which is issued by the Federal Tax Service. If there is no such extract, then the code can be determined independently by looking at the OKVED or OKVED 2 classifiers (used in parallel until 2021).

If an organization combines simplified taxation and UTII, on the title page of the declaration indicate the OKVED code of the type of activity in respect of which the simplified taxation is applied (letter of the Ministry of Finance of Russia dated June 9, 2012 No. 03-11-11/186).

Declaration of the simplified tax system 2021: sample filling for the simplified tax system “Income”

Section 1.1 is divided into reporting periods (quarters), in each of them the OKTMO code is indicated (lines 010, 030, 060, 090) at the place of registration of the individual entrepreneur or location of the company. If its value remains unchanged (i.e. the address of activity does not change), only line 010 is allowed to be filled in, the rest are crossed out.

Tax amounts payable by quarter (pages 020, 040, 070, 100) are calculated indicators that are calculated according to a specific algorithm. This involves data on income received, insurance premiums paid and advance payments. Let's look at the calculation of tax and its reflection in the declaration using an example:

summed up the results of work for 2021 and issued a declaration:

| Period | Income in rub. | Insurance premiums listed in rub. | Tax amount (6%) in rub. | An advance payment in rubles was transferred. | ||||

| Amount according to KUDIR | Page in Section 2.1 | Sum | Page in Section 2.1.1 | Sum | Page in Section 2.1.1 | Sum | Page in Section 1.1 | |

| 1 sq. | 620 000 | 110 | 15 500 | 140 | 37 200 | 130 (page 110 x 6%) | 21 700 | 020 (p.130 – p.140) |

| half year | 1 330 000 | 111 | 30 600 | 141 | 79 800 | 131 (page 111 x 6%) | 27 500 | 040 (131 – 141 – 020) |

| 9 months | 1 860 000 | 112 | 45 900 | 142 | 111 600 | 132 (page 112 x 6%) | 16 500 | 070 (132 – 142 – 020 – 040) |

| year | 2 410 000 | 113 | 63 000 | 143 | 144 600 | 133 (page 113 x 6%) | 15 900 | 100 (133 – 143 – 020 – 040 – 070) |

The declaration is filled out based on the credentials. Formula for calculating tax payable:

- in the 1st quarter - the amount of tax 6% of income is reduced by the amount of insurance premiums paid during the reporting period, but not more than 50% (clause 3.1 of Article 346.21 of the Tax Code of the Russian Federation);

— for the following quarters, the calculated indicator is also reduced by the amount of the transferred tax advances.

In the sample declaration completed according to this example, the amount of additional tax paid on the listed advances in 2021 amounted to 15,900 rubles:

Responsibility for late submission

Since the simplified declaration includes information on a number of taxes, fines are charged for each of them (letter of the Ministry of Finance dated November 26, 2007 No. 03-02-07/2-190).

In general cases, the fine is 5% of the tax amount, but not less than 1,000 rubles. Since taxes are zero when filing a simplified declaration, the fine for failure to submit a declaration on time will be equal to 1,000 rubles for each tax (Article 119 of the Tax Code of the Russian Federation).

Also, violation of the deadline for filing a declaration or failure to submit it may entail a fine of 300–500 rubles for an official of the organization (Article 15.5 of the Code of Administrative Offenses of the Russian Federation).

Declaration of the simplified tax system 2021: sample filling for the simplified tax system “Income minus expenses”

With this object, the tax base changes, therefore the tax calculation algorithm will change - costs must be taken into account, and the tax is calculated from the difference between income and expenses. The tax calculation is carried out in section 1.2, and the data necessary for it is entered in section 2.2, where, unlike section 2.1, the amounts of costs incurred are reflected on a quarterly basis.

Let's continue the example, taking the initial data on income from it, adding expenses and applying the simplified tax system 15% of the difference between income and expenses:

| Period | Income in rub. | Expenses in rub. | The tax base | Tax amount (15%) | ||||

| Amount according to KUDIR | Page Section 2.2 | Amount according to KUDIR | Page Section 2.2 | Sum (gr. 2 – gr. 4) | Page Section 2.2 | Sum (gr.6 x 15%) | Page Section 2.2 | |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

| 1 sq. | 620 000 | 210 | 380 000 | 220 | 240 000 | 240 | 36 000 | 270 |

| half. | 1 330 000 | 211 | 720 000 | 221 | 610 000 | 241 | 91 500 | 271 |

| 9 months | 1 860 000 | 212 | 900 000 | 222 | 960 000 | 242 | 144 000 | 272 |

| year | 2 410 000 | 213 | 1 200 000 | 223 | 1 210 000 | 243 | 181 500 | 273 |

Based on the calculations carried out, supported by accounting data, fill out section 1.2: - page 020 = page 270 (advance payment for 1 quarter is listed);

— page 040 = page 271 – page 240 = 55,500 rub. (advance for 2 quarters);

— page 070 = page 272 – page 241 = 52,500 rub. (advance payment for Q3);

— page 100 = page 273 – page 242 = 37,500 rub.

The company must pay an additional simplified tax in the amount of 37,500 rubles. This calculation is presented in section 1.2 of the declaration:

Section 2.2

Section 2.2 is intended to calculate the tax base of organizations and entrepreneurs who pay a single tax on the difference between income and expenses.

On lines 210–213, indicate income for each reporting period: quarter, half-year, nine months, year. Indicate the data on an accrual basis.

If you stopped operating on a simplified basis in the middle of the year, also indicate income for the last reporting period on line 213. For example, if an organization stopped operating on a simplified basis in March, the amount of income received in the first quarter should be indicated on line 210. The same amount is duplicated on line 213, and lines 211–212 are filled in with dashes.

On lines 220–223, indicate expenses for each reporting period on an accrual basis. Upon termination of activities, duplicate the amount of expenses for the last reporting period on line 223.

On line 230, indicate the loss (part of the loss) for previous tax periods, which will reduce the base of the reporting year.

On lines 240–243, indicate the tax base for each reporting period, which is defined as the difference between income and expenses. When calculating the tax base for the year, also subtract the amount of loss indicated on line 230 from income.

If the difference between income and expenses turns out to be negative, indicate the amount of loss on lines 250–253.

On lines 260–263, indicate the tax rate for each reporting period and year. The general rate is 15 percent, while in different regions it can vary from 0 to 15 percent.

On lines 270–273, reflect the calculated amounts of advance payments. The advance payment for this line is calculated as the tax base (lines 240–243) multiplied by the tax rate (lines 260–263).

On line 280, indicate the amount of the minimum tax, that is, the amount of income for the year (line 213), multiplied by 1 percent. It must be paid if the actual tax is less than the minimum or a loss is incurred.

15.png

Let us remind you that the declaration must be submitted to the Federal Tax Service even in the absence of activity and non-receipt of income (if there is no official record of termination of activity in state registers). It is not difficult to fill out a zero declaration under the simplified tax system 2021 - they draw up a title page, listing all the required details of the company and the Federal Tax Service, enter zeros in the calculation sheets (where the amounts should be indicated) and dashes in the remaining fields.

The declaration under the simplified tax system 2021 (form) can be downloaded below.

When to take it

Organizations and entrepreneurs submit simplified tax returns at the end of the year at different times. Thus, organizations are required to submit a declaration no later than March 31, and entrepreneurs no later than April 30 of the year following the reporting year.

During the year, an organization or entrepreneur can re-profile their business and cease the activities for which they applied the simplification. They are required to notify the tax office about this within the next 15 working days. In this case, the single tax declaration must be submitted no later than the 25th day of the month following the one in which the simplified taxation activity was terminated.

This procedure is provided for in Article 346.23 of the Tax Code of the Russian Federation.

If the payer winds down his business altogether (for example, the organization is liquidated and the entrepreneur loses his status), there is no need to notify the inspectorate of the termination of activities on the simplified tax system. In this case, the single tax declaration must be submitted within the usual deadline:

- for organizations - no later than March 31 of the following year;

- for entrepreneurs - no later than April 30 of the following year.

This conclusion follows from the letter of the Federal Tax Service of Russia dated April 29, 2015 No. SA-4-7/7515.

An example of determining the deadline for submitting a declaration under the simplified tax system in case of loss of the right to a special regime

"Alpha" applies a simplified taxation system. In June 2016, the average number of Alpha employees, calculated for the six months, exceeded 100 people. Therefore, from April 1, 2021, Alpha lost the right to use the simplified procedure.

The last day for submitting a declaration to the simplified tax system is July 25, 2021.

An example of determining the deadline for submitting a declaration under the simplified tax system upon termination of activity

On July 10, 2021, Alpha submitted to the tax office a notice of termination of business activities for which the simplified taxation system was applied (form 26.2-8). There has been no activity since July 1st.

The last day for submitting a declaration to the simplified tax system is August 25, 2016.

Situation: is it necessary to submit a zero tax return under the simplified tax system if the organization has switched to a simplified tax system, but is not yet conducting business?

Yes need.

Submitting a declaration to the tax office is the responsibility of all taxpayers (subclause 4, clause 1, article 23 of the Tax Code of the Russian Federation). Tax payers under simplification are organizations, autonomous institutions and entrepreneurs who have submitted an application for the transition to this special regime (clause 1 of Article 346.12 of the Tax Code of the Russian Federation). Thus, if a taxpayer has switched to a simplified tax system, but does not conduct business and does not pay a single tax, he needs to file a declaration. A similar point of view is reflected in letters of the Ministry of Finance of Russia dated November 9, 2007 No. 03-11-05/264 and dated March 31, 2006 No. 03-11-04/2/74.

Instead of a zero declaration for a single tax when simplified, you can submit a single (simplified) declaration. The form of a single (simplified) declaration and the procedure for filling it out were approved by Order of the Ministry of Finance of Russia dated July 10, 2007 No. 62n. In order to file a single (simplified) return, the taxpayer must simultaneously meet two conditions during the tax period, that is, the year. First: there is no object of taxation, that is, income, and if expenses were taken into account when calculating the tax, then they should not exist either. And second: during the year there was no movement of money through current accounts (at the cash desk). This is stated in paragraph 2 of Article 80 of the Tax Code of the Russian Federation.

At the same time, there is no need to submit unified (simplified) declarations quarterly. After all, tax legislation does not oblige payers to submit declarations under the simplified tax system based on the results of reporting periods (clause 1 of article 346.23 of the Tax Code of the Russian Federation). Consequently, such an obligation does not arise in relation to single (simplified) declarations. Similar clarifications are contained in the letter of the Federal Tax Service of Russia dated August 8, 2011 No. AS-4-3/12847.