When making a calculation, the user is obliged to issue a cash receipt or a strict reporting form (SRF) on paper and (or) if the buyer (client) provides the user with a subscriber number or email address before the calculation, send a cash receipt or a strict reporting form in electronic form to the buyer (client) to the provided subscriber number or email address (if it is technically possible to transfer information to the buyer (client) in electronic form to the email address), unless otherwise established by the Federal Law of May 22, 2003 N 54-FZ “On the Application of Control - cash register equipment when making payments in the Russian Federation" (hereinafter referred to as Law No. 54-FZ) (clause 2 of Article 1.2 of Law No. 54-FZ).

Basic rules for storing strict reporting forms

The rules according to which Russian organizations must store BSO are set out in the Regulations on cash settlements without the use of cash registers (hereinafter referred to as the Regulations), approved by Decree of the Government of the Russian Federation No. 359 of 05/06/2008.

Read more about other important provisions of Resolution No. 359 in the article “What applies to strict reporting forms (requirements).”

The traditional method of producing BSO is to contact a printing house (clause 4 of the Regulations). The legislation of the Russian Federation also allows for the issuance of forms when automated systems are used (clause 11 of the Regulations).

As for BSOs produced by printing methods, they should be placed in safes or in special premises of the enterprise, where the safety of the forms is guaranteed. Every day, the place where BSO is stored must be sealed or sealed (clause 16 of the Regulations).

The functions of ensuring the safety of strict reporting forms must be performed by a financially responsible person (hereinafter referred to as the MOL) - an employee of the organization, with whom the employer must sign an agreement on full financial responsibility (clause 14 of the Regulations).

The MOL begins to perform its functions from the moment the BSO becomes available to the organization (for example, from a printing house). His tasks at the time of receipt of the forms are to:

- check the number of forms, their series and numbers with the data specified in the accompanying documents;

- issue an act of acceptance of forms;

- enter information about the accepted forms into the book of strict reporting forms.

All three actions of the MOL must be carried out in the presence of a commission, which is created on the basis of an order from the head of the company (clause 15 of the Regulations).

As a BSO accounting book (or the basis for its creation), commercial companies can use a form corresponding to number 0504045 according to OKUD. For state and municipal organizations, its use is mandatory (Order of the Ministry of Finance of the Russian Federation No. 52n dated March 30, 2015).

The acceptance certificate (a little later we will look at the basis on which form it should be drawn up) must be signed by all members of the commission. It must also be approved by the supervisor. The book of records of strict reporting forms should be stitched and numbered. It must be signed by the head of the company, the chief accountant, and also sealed.

You can learn about filling out the book from the article “How to fill out the book of strict reporting forms.”

Documentary reflection of the presence of BSO

The standards for maintaining strict reporting forms are prescribed in the relevant provisions of the Government of the Russian Federation. They state that the organization is obliged to keep BSO accounting logs, where their number is recorded. The template for preparing such documents is not established by law, therefore a legal entity has the right to choose the format that is convenient for it. The journal must meet three main characteristics:

- presence of page numbers;

- sheet stitching;

- presence of the director's signature and seal of the legal entity.

When starting a journal, the organization issues an act regarding the rules for filling it out. This document specifies the full name of the employee responsible for the use and safety of the BSO.

Storing forms using automated systems

The “innovative” scenario for manufacturing BSO - using automated systems (AS) - significantly simplifies the task of organizing the storage of forms for the company’s management. If the corresponding system meets the criteria contained in clause 11 of the Regulations (is protected from unauthorized access, identifies and records transactions with BSO for five years or more, stores data on the form in memory), then there is no need to carry out the above procedures, because:

- BSO from a third party is not accepted;

- copies of the BSO remain in the memory of the computer and other devices as part of the system;

- Suppliers of modern AS for organizing the circulation of BSO, as a rule, include in the software package solutions that allow you to maintain a book of records of strict reporting forms in electronic form.

At the same time, once printed using AS, but for one reason or another damaged, BSOs should, like those created by printing, be stored in the organization’s safes or in other safe places.

The functions of the MOL in the case of using an automated system are most often assigned to an accountant trained in working with the appropriate software, and less often to a system administrator managing the automated system.

Attention! In connection with the transition to online cash registers, the taxpayer is obliged from 07/01/2018, and in some situations from 07/01/2019, to form a BSO using automated systems for strict reporting forms capable of transmitting information about mutual settlements to the Federal Tax Service online. For more details, see the material “Law on online cash registers - how to apply BSO (nuances)”. The BSO is issued to the buyer on paper or sent by email or to the client’s phone number.

Tax authorities control the completeness of revenue accounting. Find out what rights they have when checking the cash balance in the cash register, the BSO machine and generated forms from the materials of ConsultantPlus experts, having received trial access for free.

Manufacturing of BSO

Strict reporting forms can be produced in two ways: printing or using automated systems. The printed form must contain information about the manufacturer (name, tax identification number, location, order number and year, circulation). When filling out the form, at least one copy of the form must be provided, or it may have tear-off parts.

Generating forms using an automated system currently presents certain difficulties. There is no official explanation of what is considered such a system. The Regulations state that the automated system must:

- have protection from unauthorized access;

- identify, record and save all transactions with BSO for at least 5 years;

- save the number and series of the form.

According to the regulatory authorities, the system must meet the requirements for cash register systems. The computer is not suitable for making forms , because... does not provide protection, recording and storage of information about the form. For questions regarding the use of an automated system for the production of strict reporting forms, the Ministry of Finance recommends contacting the Ministry of Industry and Trade (Letter dated 03/06/09 No. 03-01-15/2-96).

Transfer of forms to the organization's employees

If the calculations in which the BSO is used are carried out not by the MOL, but by another employee of the company, then the transfer of the relevant forms to his disposal is carried out by the financially responsible person on the basis of a written application. Data on issued BSOs are entered by the MOL in the book of records of strict reporting forms.

Copies of the BSO issued to the organization's clients, or the counterfoils of the forms (depending on which specific form of the BSO is used) are transferred by the employees to the financially responsible person. Data about this is also recorded in the BSO accounting book. If any of the previously issued forms is damaged, it is crossed out and then attached to the accounting book.

Normative legal acts

For an accountant, the fundamental regulatory legal acts (RLA) that regulate the accounting of strict reporting forms in budgetary institutions are several instructions:

- instructions for the use of a unified chart of accounts, approved by order of the Ministry of Finance of Russia dated December 1, 2010 No. 157n;

- instructions for using the chart of accounts for budget accounting, approved by order of the Ministry of Finance of Russia dated December 6, 2010 No. 162n;

- instructions for using the chart of accounts for accounting of budgetary institutions, approved by order of the Ministry of Finance of Russia dated December 16, 2010 No. 174n;

- instructions for using the chart of accounts for accounting of autonomous institutions, approved by order of the Ministry of Finance of Russia dated December 23, 2010 No. 183n.

In addition, it is necessary to know industry regulations that regulate the structure of specific forms, the rules for filling them out, recording and storing them. So, if the form of a school certificate is approved by a state body (order of the Ministry of Education and Science of Russia dated August 27, 2013 No. 989 “On approval of samples and descriptions of certificates of basic general and secondary general education and appendices to them”), it should be used. Similar orders apply to documents of higher education, work records, certificates of incapacity for work and other BSO.

Do GMEC protocols have legal force?

Some provisions of the legislation regulating the circulation of BSO are contained in the minutes of the meeting of the State Interdepartmental Expert Commission (GMEC) No. 4/63-2001 dated June 29, 2001. Do they have legal force that applies to all Russian organizations?

Despite the fact that GMEC ceased to exist on 08/09/2004, its decisions, which were made during the period when this institution exercised its powers, are generally binding (letter of the Federal Tax Service of the Russian Federation No. ED-18-2/947 dated 06/17/2014).

So, with regard to the form of the BSO acceptance certificate, you should use the form that corresponds to number 070000 according to OKUD. The order to use this form includes clause 18 of the GMEC protocol No. 4/63-2001.

Similarly, other provisions of the GMEC Protocol No. 4/63-2001 retain legal force. In particular, those that regulate BSO accounting.

Legislative regulation

Clause 2 Art. 2 of Federal Law No. 54 speaks of the possibility of using BSO instead of cash registers when providing services to the population included in the corresponding list of OKUN.

Federal Law No. 290-FZ of July 3, 2021 amended the aforementioned Federal Law No. 54, making the list of services for which payment for the provision can be registered using BSO, without cash register, exhaustive.

In 2008, the government of the Russian Federation updated the regulations on making payments without the use of cash registers (Resolution No. 359 of May 6, 2008). It covers in detail the requirements for this type of documentation, the procedure for settlements with their help, and the features of accounting and disposal. The main changes (compared to previous requirements) are as follows:

- old BSO forms are considered irrelevant and cannot be used;

- entrepreneurs must themselves develop new forms of SSB (except for certain types of activities for which standard ones have been approved);

- The BSO must contain certain details;

- You must indicate typographical information if the BSO was printed in this way.

Accounting for strict reporting forms

BSO turnover is recorded in off-balance sheet account 006, which is called “Strict Reporting Forms”. BSO accounting is carried out through entries reflecting the amount of costs for the production of forms (clause 22 of the minutes of the GMEC meeting No. 4/63-2001). As a rule, these are the postings:

- Dt account 26 “General business expenses”;

- Kt account 60 “Settlements with suppliers and contractors.”

In some cases, BSO accounting involves the creation of subaccounts for account 006. This is possible if the forms capitalized by the accounting department are subsequently issued to other employees who actually manage the BSO (we examined a similar scenario above). In this case, subaccount 006-1 “BSO in accounting”, as well as subaccount 006-2 “BSO from executors” can be formed.

How to correctly write off BSO in accounting and what documents to prepare? The answer to this question was given by 2nd class State Civil Service Advisor I. O. Gorchilina. Get free trial access to the ConsultantPlus system and get acquainted with the official’s point of view.

What it is

A strict reporting form is a fiscal document that, instead of a cash receipt, can be generated for their clients by organizations and individual entrepreneurs engaged in the provision of services to the public.

Until July 1, 2021, organizations and individual entrepreneurs, regardless of the chosen taxation system, had the right not to use a cash register, but instead of cash register receipts, issue their clients with strict reporting forms printed in a typographical manner.

From July 1, 2021 paper forms

cannot be used in place of cash receipts. This is due to the fact that all fiscal documents must be transmitted via the Internet to the Federal Tax Service. Therefore, BSOs should be formed at special BSO-KKT or regular online cash registers. To print them, you need to choose devices whose name contains the letter “F” - they are equipped with a printer.

Paper forms of strict reporting were used as an alternative to checks and made it possible not to purchase a cash register. Now, when they need to be generated on cash registers, the use of BSO does not make sense for most companies and individual entrepreneurs. However, this does not mean that paper forms are completely prohibited. If it is convenient and necessary, you can continue to issue them, but at the same time generate a check at the online cash register.

note

, from July 1, 2021, it is possible to issue printing BSOs

without issuing a check

only in cases where the business is exempt from using cash register equipment, and the law does not require issuing any document with certain details.

Thus, typographic BSO in 2021 can be used at will:

- Individual entrepreneurs without employees from the service sector. For them, there is a deferment for the use of CCP until July 1, 2021. At the same time, they are not obliged to issue any payment documents, but can do this at their own request or at the request of the client;

- other business entities exempt from the use of cash register systems (Article 2 of Law 54-FZ on cash register systems), if they do not have to issue a document with specific details;

- other companies and individual entrepreneurs from the service sector - not instead of, but in addition to the online cash register receipt.

If BSOs are used instead of cash register receipts, they must be generated on a special BSO-KKT or a regular online cash register.

For some types of activities, there are BSO forms developed by the state. Here they are:

- tickets (railway, air, public transport);

- parking services;

- tourist and excursion packages;

- subscriptions and receipts for payment of veterinary services;

- pawn tickets and safety receipts for pawnshop services.

However, from July 1, 2021, the above paper forms are also valid only with the simultaneous generation of a cash receipt. For example, if the buyer is issued a train ticket, the following options are possible:

- The ticket is purchased electronically. The buyer is sent an electronic travel document with the cash receipt details printed on it, including a QR code. Or he is sent an electronic ticket and a separate online cash register receipt in electronic form.

- A paper ticket is purchased. The buyer is issued a standard railway ticket form (approved by the BSO) + an online cash register receipt. Or he is given a standard ticket form, which contains the receipt details, including a QR code.

Companies in the arts and culture sector need to apply SSR

, if they want to receive VAT exemption. It is provided if tickets are sold in the form of an approved document. However, this does not relieve them of the obligation to use online cash register systems. That is, in order not to break the law and receive an exemption from VAT, cultural institutions need to generate a cash receipt and issue a paper ticket (BSO from Order of the Ministry of Culture No. 257). By the way, the ministry has developed a new ticket form, and after approval it will replace the current BSO form.

Criteria for correct numbering of strict reporting forms

An important criterion characterizing the accounting and storage of BSO is the correct numbering of the relevant forms.

The main requirement for a BSO is the presence of a unique 6-digit serial number and a series consisting of 2 letters. At the level of federal legislation, the noted criteria are not fixed, but they are regularly found in departmental legal acts regulating the production of BSO (for example, in the letter of the Ministry of Culture of the Russian Federation No. 2344-01-39/03-E4 dated April 13, 2009). These provisions can be applied by subjects of legal relations in other industries on the principle of legal analogy.

The relevant details of the forms - series, number - will need to be recorded in the marked forms (BSO acceptance certificate, BSO accounting book).

As we noted at the beginning of the article, BSOs must be produced using the printing method or using automated systems. In the first case, the organization, as a rule, orders the production of forms from a third-party contractor who has the necessary printing equipment. If such an order is being made for the first time, then you can start producing BSO with series AA and number 000001. But in subsequent orders, printed forms must begin with the number following the one that was present on the last BSO of the previous edition.

The use of automated systems for issuing forms assumes that the correct numbering of the BSO (in correlation with entering the necessary information into the system registers) will be carried out automatically by the corresponding software.

BSO forms (what applies to them)

Depending on the type of services provided, strict reporting forms may be called differently: receipts, tickets, vouchers, subscriptions, etc. The forms of BSO can also be different.

Organizations and individual entrepreneurs can themselves develop the form of strict reporting form that will be convenient for them to use in their activities, but on the condition that it contains a list of mandatory details

(Article 4.7 of Law 54-FZ).

List of required details of the BSO form

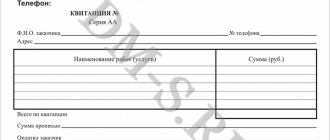

- Title of the document;

- serial number for the shift;

- date, time and place (address) of settlement;

- name of the user organization or last name, first name, patronymic of the individual entrepreneur;

- User's TIN;

- the taxation system used in the calculation;

- calculation attribute (receipt, return of receipt, expense, return of expense);

- name of goods, work, services, payment, payment, their quantity, price per unit taking into account discounts and markups, cost including discounts and markups, indicating the VAT rate (individual entrepreneurs in special modes may not indicate the name and quantity until 02/01/2021);

- the calculation amount indicating the rates and VAT amounts at these rates;

- form of payment (payment in cash and (or) by bank transfer), as well as the amount of payment in cash and (or) by bank transfer;

- position and surname of the person who made the settlement with the buyer;

- registration number of the cash register on which the BSO was formed;

- serial number of the fiscal drive model;

- fiscal sign of the document;

- the address of the website of the authorized body, where the fact of recording this calculation and the authenticity of the fiscal indicator can be verified;

- subscriber number or email address of the buyer (if the BSO is sent electronically to him by phone or email);

- sender's email address;

- serial number of the fiscal document;

- shift number;

- fiscal sign of the message;

- QR code.

Inventory and write-off of BSO

The tasks that the process of storing strict reporting forms includes includes inventory. This procedure involves reconciling existing copies of the BSO, as well as their counterfoils, with the data contained in the book of strict reporting forms. The inventory of BSO must be carried out simultaneously with a similar procedure established in relation to cash at the cash desk (clause 17 of the Regulations).

After five years of storage of forms (including damaged or incomplete ones) in the organization, it is necessary to write off the BSO. This procedure is carried out by drawing up a separate act (you can use the form corresponding to OKUD number 0504816, and for state and municipal structures its use is mandatory). This document is drawn up with the participation of a commission created on the basis of an order from the head of the company.

For more information about the act, see “Act on the write-off of strict reporting forms - sample.”

The structure of modern automated systems, as a rule, contains solutions that make it possible to issue the necessary acts on inventory and write-off of BSO in electronic form. Also, the corresponding systems provide algorithms for excluding decommissioned digital BSOs from hardware registers.

For more information about other types of inventory provided for by the legislation of the Russian Federation, read the article “How to conduct an inventory before annual reporting.”

Inventory of forms

An inventory of BSO is periodically carried out, which makes it possible to identify their shortage or violation of storage rules. The inventory is carried out by a commission, the composition of which is approved by the entrepreneur.

Also, the purpose of the inventory is to destroy strict reporting forms. This is a mandatory procedure upon expiration of the storage period, as well as in relation to damaged or damaged forms.

In this case, a write-off act for the BSO is drawn up.

Back to contents

Results

BSO are equivalent to cash receipts and must be generated using automated systems capable of transmitting information to the Federal Tax Service online. In this case, the forms are also recorded using such systems. Some taxpayers are legally allowed to switch to using online devices from 07/01/2019. Before this, they have the right to use printed forms. The purchase of such forms is carried out on cost accounting accounts (25, 26, 44 - depending on the department), and subsequent accounting is carried out using balance sheet account 006.

Sources:

- Decree of the Government of the Russian Federation No. 359 of 05/06/2008

- minutes of the meeting of the State Interdepartmental Expert Commission (GMEC) No. 4/63-2001 dated June 29, 2001

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Procedure for settlements using BSO

Organizations or individual entrepreneurs providing services to the public have the right to refuse to use cash register systems; in this case, they are required to issue strict reporting forms (SRF) when paying in cash. Whether a type of activity belongs to services to the public is determined in accordance with the All-Russian Classifier of Services to the Population OK 002-93 (OKUN), approved by Resolution of the State Standard of Russia dated June 28, 1993 No. 163. The classifier includes the following types of services: 01 – household services; 02 – passenger transport services; 03 – communication services; 04 – housing and communal services; 05 – services of cultural institutions; 06 – tourist and excursion services; 07 – physical education and sports services; 08 – medical, sanatorium, health, veterinary services; 09 – legal services provided by notaries and lawyers; 10 – banking services; 11 – services in the education system; 12 – trade and catering services, market services; 80 – other services to the population, these include: services for financial intermediation, insurance, services in the field of advertising, home security, etc. The procedure for approving forms of strict reporting forms, equivalent to cash receipts, the procedure for their accounting, storage and destruction is established by the Regulations on carrying out cash payments and (or) payments using payment cards without the use of cash register equipment, approved by Decree of the Government of the Russian Federation dated 05/06/08 No. 359 (hereinafter referred to as the Regulations).

For certain types of services, SSBs are developed and approved by federal executive authorities. If the form has already been developed and approved, then it is necessary to use it. If there is no form, then organizations and individual entrepreneurs have the right to independently develop a BSO form, which must contain all the required details.

Mandatory details of strict reporting forms include:

- document name, six-digit number and series;

- name and legal form of the organization, full name. individual entrepreneur;

- the location of the permanent executive body of the legal entity, in case of its absence - of another body or person having the right to act on behalf of the legal entity without a power of attorney;

- TIN of the organization or individual entrepreneur that issued the document;

- type of service;

- cost of the service in monetary terms;

- amount of payment;

- date of calculation and preparation of the document;

- position, full name of the person responsible for the transaction and the correctness of its execution, his personal signature, seal of the organization;

The organization has the right to determine the appearance of the form, shape, font, color independently, as well as indicate additional details characterizing the specifics of the service provided; artistic design is also allowed (Letters of the Federal Tax Service of Russia for Moscow dated July 12, 2009 No. 17-15/022192, dated March 2 .09 No. 17-15/19792).

Particular attention should be paid to the fact that the BSO is also the primary accounting document on the basis of which transactions with funds are processed; therefore, it must meet the requirements of Art. 9 of the Law of November 21, 1996 No. 129-FZ. Strict reporting forms must be filled out clearly and legibly, without corrections. Damaged forms are crossed out and attached to the form book for the day on which they were filled out.