Invoice is a document according to which the buyer accepts VAT deduction on purchased goods and services. Why an adjustment invoice is needed, in what cases it is issued, and how to properly prepare it and reflect it in tax registers for VAT, we will tell you in our article.

Why an invoice and an adjustment invoice are issued is discussed in Article 169 of the Tax Code of the Russian Federation. Based on them, the buyer of goods and services reduces the amount of value added tax paid to the budget (claims a deduction). Correct execution of these documents allows you to avoid claims from tax authorities. The forms and rules for filling out are established by Government Decree No. 1137 dated December 26, 2011.

Invoice form

The cost of goods has decreased: what documents are needed from the supplier?

The seller (supplier) can reduce the cost of goods after they have been shipped to the buyer.

When this can happen, says the material “What is an adjustment invoice and when is it needed?” .

At the time of making such a decision, the parties to the transaction already have the following set of documents in their hands:

- contract with initial delivery conditions;

- original invoice (PSF);

- primary document for the shipped goods;

- other documents (certificates, technical specifications, etc.).

A decrease in the cost of goods is accompanied by additional documents:

- agreement or other type of consent of the buyer to change the initial terms of the transaction (clause 10 of article 172 of the Tax Code of the Russian Federation);

- adjustment invoice (CSF) for reduction;

- a new primary document on changes in the value of goods containing the necessary details (Article 9 of the Law “On Accounting” dated December 6, 2011 No. 402) - it will serve as the basis for reflecting adjustment transactions in accounting (letter of the Federal Tax Service of Russia dated January 24, 2014 No. ED-4 -15/ [email protected] ).

The absence of these documents may deprive counterparties of the right to deduct VAT under the CSF and leave adjustment accounts unconfirmed.

You can view and download a sample adjustment invoice for reducing the price of goods in ConsultantPlus. Get trial access to the system for free and proceed to the filling example.

From the next section, find out what actions are required in the accounting of the buyer and seller when the CSF appears.

Downward adjustment in the current period in “1C: Accounting 8” (rev. 3.0)

Let's consider an example of how the 1C:Accounting 8 version 3.0 program reflects downward adjustments to acquisitions in the current tax period if input VAT is not accepted for deduction.

Example

Organization LLC "Style" carrying out operations subject to and exempt from VAT:

In addition, in the fourth quarter of 2021, the organization LLC "Style":

The sequence of operations is given in the table. |

Setting up accounting policies

Due to the fact that the organization maintains separate accounting of the submitted VAT amounts when carrying out operations for the sale of goods (works, services), both subject to VAT and exempt from taxation, it is necessary to make appropriate accounting policy settings.

On the VAT tab of the Accounting Policy form (section Main - subsection Settings - Taxes and reports), you should set the checkbox Separate accounting of incoming VAT by accounting methods is maintained.

After making the settings in the tabular part of the documents of the accounting system Receipt (act, invoice), it will be possible to display information about the selected method of accounting for input VAT, which can take the following values:

- Accepted for deduction;

- Included in the price;

- Blocked until confirmation 0%;

- Distributed.

Receipt of goods

Receipt of goods from the seller (operations 2.1 “Accounting for received goods”, 2.2 “Accounting for input VAT”) is registered in the program using the document Receipt (act, invoice) with the transaction type Goods (invoice) (section Purchases - subsection Purchases), fig. 1.

Rice. 1. Reflection in the accounting of goods received

Since the purchased goods are intended for resale, i.e., for carrying out a transaction subject to VAT, the value Accepted for deduction is indicated in the VAT accounting method field in the tabular part of the document.

After posting the document, the following accounting entries are entered into the accounting register:

Debit 41.01 Credit 60.01 - for the cost of goods purchased;

Debit 19.03 Credit 60.01 - for the amount of VAT presented by the seller on purchased goods. In this case, account 19.03 indicates the third sub-account, reflecting the method of accounting for VAT - Accepted for deduction.

An entry with the type of movement Receipt and the event Presented by VAT by the supplier is made in the VAT accumulation register. At the same time, a record is entered with the type of movement Arrival in the accumulation register Separate accounting of VAT. The recording is made to be able to use data on purchased goods in the event of a change in the purpose of their use.

To register a received invoice (operation 2.3 “Registration of a received invoice”), you must enter the number and date of the incoming invoice in the fields Invoice No. and from the document Receipt (act, invoice) (Fig. 1), respectively, and click the button Register. In this case, the document Invoice received will be automatically created (Fig. 2), and a hyperlink to the created invoice will appear in the form of the basis document.

Rice. 2. Invoice received for receipt of goods

The fields of the Invoice document received will be filled in automatically based on information from the Receipt document (act, invoice).

Besides:

- in the Received field the date of registration of the Receipt document (act, invoice) will be entered, which, if necessary, should be replaced with the date of actual receipt of the invoice. If an agreement has been concluded with the seller on the exchange of invoices in electronic form, then the date of sending the electronic invoice file by the EDF operator, indicated in its confirmation, will be entered in the field;

- in the line Base documents there will be a hyperlink to the corresponding receipt document;

- in the Transaction Type Code field the value 01 will be reflected, which corresponds to the acquisition of goods (work, services), property rights in accordance with the Appendix to the order of the Federal Tax Service of Russia dated March 14, 2016 No. ММВ-7-3/ [email protected]

Since the organization maintains separate accounting, in the Invoice received document there is no line with the value Reflect VAT deduction in the purchase book by the date of receipt, i.e. there is no possibility of a simplified application for deduction of input VAT.

An application to deduct the amount of input VAT is made using the routine operation Generating purchase ledger entries (section Operations - subsection Closing the period - Regular VAT operations).

As a result of posting the document Invoice received, a registration entry is made in the Register of Invoices. Despite the fact that since 01/01/2015, taxpayers who are not intermediaries (forwarders, developers) do not keep a log of received and issued invoices, register entries in the Invoice Log are used to store the necessary information about the received invoice.

Adjusting the cost of purchased goods

To reflect operations 3.1 “Adjustment of the cost of goods received”, 3.2 “Adjustment of input VAT”, it is necessary to create a document Adjustment of receipts with the operation type Adjustment as agreed by the parties.

This document can be created based on the document Receipt (act, invoice) (Fig. 1) by clicking the Create based on button. On the Main tab you must specify (Fig. 3):

- in the Document No. and from fields - the number and date of the document serving as the basis for adjusting the cost of purchased goods;

- in the Reflect adjustment field - the value In all accounting sections, since the adjustment is made to the cost indicators.

On the Products tab, you should indicate the adjusted indicators in the line after the change (see Fig. 3). After posting the document Adjustment of receipts, the following accounting entries are entered into the accounting register:

Debit 19.03 Credit 60.01 - REVERSE for the difference in the amount of input VAT;

Debit 41.01 Credit 60.01 - REVERSE for the difference in the cost of purchased goods.

Since before the adjustment, the amount of input VAT was not declared for deduction (the routine operation of Generating purchase ledger entries was not performed), an entry with the type of movement Receipt is made in the VAT register presented to adjust downward the amount of VAT presented by the supplier.

At the same time, a similar adjusting entry with the type of movement Receipt is also entered into the accumulation register Separate accounting for VAT.

To register the received adjustment invoice (operation 3.3 “Registration of the received adjustment invoice”), it is necessary in the Corr. invoice No. and from the Receipt Adjustment document (see Fig. 3), enter the number and date of the incoming adjustment invoice, respectively, and click the Register button.

Rice. 3. Adjustment of the cost of received goods

In this case, the document Adjustment invoice received will be automatically created, and a hyperlink to the created invoice will appear in the form of the basis document.

The fields in the document Adjustment invoice received will be filled in automatically based on information from the document Adjustment of receipts.

Besides:

- in the Received field the date of registration of the Receipt Adjustment document will be entered, which, if necessary, should be replaced with the date of actual receipt of the adjustment invoice. If an agreement has been concluded with the seller on the exchange of invoices in electronic form, then the date of sending the electronic invoice file by the EDF operator, indicated in its confirmation, will be entered in the field;

- in the line Basis documents there will be a hyperlink to the corresponding document for adjusting the receipt;

- in the Operation type code field the value 18 will be reflected, which corresponds to the receipt of an adjustment invoice due to a decrease in the cost of shipped goods, including in the event of a decrease in prices (tariffs) of shipped goods (Appendix to the order of the Federal Tax Service of Russia dated March 14, 2016 No. ММВ-7-3/ [email protected] ).

As a result of posting the document Adjustment Invoice received, an entry will be made in the information register Invoice Journal for storing the necessary information about the received invoice.

Acceptance of completed work

To perform operations 4.1 “Accounting for completed work”, 4.2 “Accounting for input VAT”, you need to create a document Receipt (act, invoice) with the document type Services (act) (section Purchases - subsection Purchases), fig. 4.

Rice. 4. Reflection in accounting of work performed

Since the service for repairing office premises relates to the entire activity of the organization, the amount of VAT claimed by the contractor must be distributed. To do this, in the document Receipt (act, invoice) in the Accounts column of the tabular section, set the VAT accounting method to Distributed.

As a result of posting the document Receipt (act, invoice) the following accounting entries will be entered into the accounting register:

Debit 26 Credit 60.01 - for the cost of repair work performed, amounting to RUB 100,000.00;

Debit 19.04 Credit 60.01 - for the amount of VAT presented by the contractor and amounting to RUB 20,000.00. In this case, account 19.04 will have a third sub-account, reflecting the method of accounting for VAT - Distributed.

Entries with the type of movement Receipt with the event Presented by VAT by the Supplier and with the type of movement Expense with the event VAT are subject to distribution to the amount of VAT presented by the contractor and subject to distribution are entered into the VAT register submitted.

At the same time, for the tax amount written off in the VAT register, an entry is made in the Separate VAT accounting register with the type of movement Receipt.

To register an invoice received from a contractor (operation 4.3 “Registration of a received invoice”), you must enter the number and date of the incoming invoice in the fields Invoice No. and from the document Receipt (act, invoice) (see Fig. 4). invoices and click the Register button. In this case, the document Invoice received will be automatically created (Fig. 5), and a hyperlink to the created invoice will appear in the form of the basis document.

Rice. 5. Invoice received for work performed

As a result of posting the document Invoice received, an entry will be made in the information register Invoice Journal to store the necessary information about the received invoice.

Adjustment of the cost of work performed

To reflect operations 5.1 “Adjustment of the cost of work performed”, 5.2 “Adjustment of input VAT”, it is necessary to create a document Adjustment of receipts with the transaction type Adjustment by agreement of the parties.

This document can be created based on the document Receipt (act, invoice) (Fig. 4) by clicking the Create based on button.

On the Main tab you must specify (Fig. 6):

- in the Document No. and from fields - the number and date of the document serving as the basis for adjusting the cost of work performed;

- in the Reflect adjustment field - the value In all accounting sections, since the adjustment is made to the cost indicators.

Rice. 6. Adjustment of the cost of work performed

On the Services tab, you should indicate the adjusted indicators in the line after the change.

After posting the document Adjustment of receipts, the following accounting entries are entered into the accounting register:

Debit 19.04 Credit 60.01 - REVERSE for the difference in the amount of input VAT;

Debit 26 Credit 60.01 - REVERSE for the difference in the cost of work performed.

According to clause 4.1 of Article 170 of the Tax Code of the Russian Federation, the proportion for the distribution of input VAT is determined based on the cost of goods shipped (work performed, services rendered) and transferred property rights for the tax period.

Since the adjustment to the cost of contract work was made before the end of the current tax period (before performing the routine operations Distribution of VAT and Creation of purchase ledger entries), an entry with the type of movement Receipt is made in the accumulation register Separate VAT accounting to reflect the decrease in the cost of work performed and the amount of input VAT.

To register the received adjustment invoice (operation 5.3 “Registration of the received adjustment invoice”), it is necessary in the Corr. invoice No. and from the Receipt Adjustment document (see Fig. 6), enter the number and date of the incoming adjustment invoice, respectively, and click the Register button. In this case, the document Adjustment invoice received will be automatically created, and a hyperlink to the created invoice will appear in the form of the basis document.

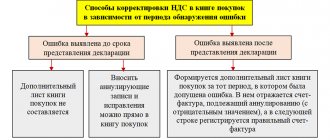

Where are reduction adjustment invoices recorded?

The CSF for reduction is subject to registration by both the seller and the buyer.

Seller's actions

By reducing the cost of shipped goods, the seller:

- draws up a CSF or consolidated CSF;

- transfers data from the KSF (consolidated KSF) to the purchase book (clause 13 of Article 171 of the Tax Code of the Russian Federation);

- takes for deduction the difference between the VAT amount on the PSF and the reduced tax amount calculated after making adjustments.

The seller has the following rules regarding CSF for reduction:

- VAT clarification for the period when the shipment occurred does not need to be submitted;

- It is possible to claim a deduction within 3 years from the date the CSF is set for reduction (clause 10 of Article 172 of the Tax Code of the Russian Federation).

Buyer actions

The buyer upon receipt from the seller of CSF for reduction:

- registers it in the sales book;

- restores the portion of VAT previously accepted for deduction.

He will not have to submit an updated declaration and pay penalties.

Find out how to take into account and use what details to transfer VAT penalties from the article “Under which BCC are VAT penalties paid?”

How not to lose a deduction on an adjustment invoice for a reduction?

The CSF for reduction is a document on the basis of which a taxpayer can claim a VAT deduction. You can use the right to deduction only if the CSF does not contain significant errors.

For example, controllers may refuse a deduction if in the CSF:

- goods not specified in the PSF are listed;

- negative values are indicated (all numbers in the CSF must be positive, even when adjusting the cost of the product downward).

When errors in invoices cannot deprive a deduction, find out from the material “What errors in filling out an invoice are not critical for deducting VAT?”

K+ experts explained in detail how to correct errors in an adjustment invoice. You can find out the procedure by getting free trial access to the system.

Learn about other errors inherent in the CSF that can negatively affect the deduction in the next section.

Making corrections to primary documentation

Invoices are based on source documents (for example, delivery note, etc.). Therefore, the primary documentation needs to be corrected, because... an error has occurred. Errors in primary documents drawn up manually (except for cash and bank documents) are corrected by crossing out the incorrect text and quantity with one line and entering the correct information above the crossed out. Correction of an error is indicated by the inscription “corrected”, signed and dated for correction.

In most cases, the seller issues a statement for the difference along with the adjustment invoice, which will be illegal, because accounting is maintained on the basis of primary documents. The appearance of a price difference is not a business transaction and there is no need to document it with an additional document.

Consolidated adjustment invoice: can it be prepared when the cost of goods decreases?

The supplier may issue a single (consolidated) CSF if adjustments to the cost of goods are needed for several deliveries to one buyer.

This opportunity has been provided for the last 5 years thanks to clause 5.2 of Art. 169 of the Tax Code of the Russian Federation (after the entry into force of the law dated 04/05/2013 No. 39-FZ).

Registration of a consolidated CSF for reduction is possible if:

- the seller agreed with the buyer to reduce the cost of shipped goods;

- the decrease affects several (two or more) deliveries issued with separate primary invoices.

The unified CSF must contain information:

- about all serial numbers and dates of issued PSF;

- on the quantity of goods and their total cost (with and without VAT) for all invoices before and after adjustments;

- the difference between invoice values before and after changes are made.

In the consolidated CSF, errors are also possible that will not allow the taxpayer to claim a tax deduction. The main specific error of this document is the indication in it of data on several buyers (subclause 3, clause 5.2, article 169 of the Tax Code of the Russian Federation). It is also unacceptable in the consolidated CSF to collapse the totals if the cost of some goods decreases and others increases.

Adjustments and corrections

The Rules, approved by the commented resolution No. 1137, clearly distinguish between two concepts: making adjustments and correcting errors.

Adjustments are changes to the original cost made after shipment and by mutual agreement of the supplier and buyer.

Errors should be understood as incorrect information initially indicated on the invoice (for example, incorrect address of the supplier or buyer, someone else's TIN, etc.).

In accordance with this, two algorithms are described in detail. The first is for making, registering and accounting for adjustments. The second is to correct errors. Corrections must be made using adjustment invoices, and errors must be corrected by issuing new copies of invoices indicating the number and date of correction.

For simplicity, we will call the new copy with the corrected errors the corrected invoice. And the original copy, which is not an adjustment, is the original invoice.

Results

A decrease in the cost of goods after their shipment is accompanied by the issuance of an adjustment invoice, which the seller registers in the purchase book, and the buyer in the sales book.

Unified (consolidated) adjustment invoices are registered in the same way. At the same time, they can reflect adjustments for several deliveries to only one buyer - indicating several buyers in a consolidated adjustment invoice will be considered erroneous and may cause a refusal of a tax deduction.

Sources:

- Tax Code of the Russian Federation

- Federal Law of December 6, 2011 N 402-FZ “On Accounting”

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.