There are a lot of non-cash payments going on in Russia these days. They have become common practice. This includes payment from a current or card account online, and transfer of funds directly from a mobile phone. But payment orders occupy a special place in the mechanism for sending money. Throughout Russia, this calculation method is used very actively. But this does not exempt you from complying with strict requirements when filling out a payment form. In particular, such details as the checkpoint in the 2021 payment order.

Payment

Based on the prescription of paragraph 1 of Article 863 of the Civil Code of the Russian Federation, the payment order acts as a written order sent to the bank by the owner of the funds. According to the contents of the payment order, the credit institution transfers the money to the recipient’s account.

The payment order did not appear by itself, but was developed by the Central Bank of Russia on the basis of Regulation No. 383-P of June 19, 2012. The approved form of this form requires that all mandatory details be included in it. Including KPP - the code for the reason for registering the enterprise for tax purposes.

Simply put, everything must be filled out in the same way as the Central Bank of Russia explains in its regulations.

This Regulation contains Appendix No. 3, which states that the code in question in the payment form should be displayed in the following lines:

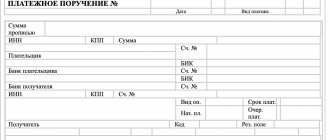

- field 103 is intended to enter into it the checkpoint of the person who is to receive the funds;

- field 102 is used to indicate in it the code by which the source of payment - the obligated person - is registered in tax records.

Together with the TIN of legal entities, the checkpoint attribute is used to display information regarding the basis for tax accounting of the company.

The reason code in the payment order must consist of 9 digits. They give the following information:

| Decoding checkpoint | |

| Number order | What does it mean |

| First two | Russia region number |

| 3rd and 4th | Tax authority number |

| 5th and 6th | Shows registration code number |

| remaining 3 digits | Record number |

Features of registration of taxes and fees

The most common problem is filling out the details of orders for payments to the budget (transfer of taxes, fees and other mandatory transfers). Errors in such documents lead to incorrect reflection in the taxpayer’s card to the Federal Tax Service.

In addition to the generally accepted details described above, fields 101–109 must be additionally filled in in tax transfers. The rules for filling them out are established by the Ministry of Finance (Order 107n dated November 12, 2013).

Details of payments to the budget

| Field | Name | The most common indicators |

| 101 | Payer status | 01 - payer legal entity 09 – individual entrepreneur 02 - tax agent 08 - other transfers to the budget (contributions from accidents to the Social Insurance Fund) |

| 102 | Payer checkpoint | |

| 103 | Recipient's checkpoint | Checkpoint of the authority to which the transfer is made |

| 104 | KBK | Budget classification code corresponding to the payment being paid |

| 105 | OKTMO | At the payer's location |

| 106 | Basis of payment | TP - transfer by term; ZD - payment of debt voluntarily; TR - debt on demand; AP - transfer according to the inspection report |

| 107 | Payment period | For current transfers, it is indicated in the format depending on the frequency of payment:

To pay a debt - the date of the request. 0 - in other cases |

| 108 | Document Number | Request or review decision number. 0 - in other cases |

| 109 | Document date | Date of the review request or decision. 0 - in other cases |

Filling rules

Appendix No. 1 of Regulation No. 383-P explains that in the case of transfers of money to the budget, each “Checkpoint” field in the payment order must be correctly filled out.

In particular, you must enter the following data:

- purpose and purpose of payment;

- information about the payer who is transferring the money, along with his checkpoint;

- the addressee who will receive the corresponding amounts, with his checkpoint displayed on the payment slip.

These same positions must be filled when money is transferred to private companies. That is, which are not related to the budget system of the Russian Federation.

Also see “Checkpoint of a separate unit: how to find out and receive.”

What can result from an error in the checkpoint in a payment order? It is important to note that fields 102 and 103 of this document are filled out in strict compliance with the registration reason code assigned to the sender and recipient of the money. Other information in these fields that does not reflect reality indicates erroneous data in the payment.

In such a situation, the Ministry of Finance of Russia indicates that an erroneous or missing checkpoint of the recipient in the payment order gives grounds to classify the entire transfer amount as a group of unknown receipts (based on clause 14 of the Procedure approved on December 18, 2013 No. 125n).

Thus, the answer to the question about the obligatory checkpoint in the payment becomes clear. Yes! Otherwise, the money simply won’t arrive. The sender must indicate it if:

- transfers funds to the budget system (writes his reason code in field 103 of this payment order);

- the money is addressed to a person not from the public sector (the law still obliges him to enter his checkpoint on the payment form).

Payment details in the 2021 payment order

The third important block is payment information. This indicates the amount of the payment, for what purpose it is being made, and what the payment is for.

Table 3

| Field no. | Name | Decoding |

| 5 | Payment type | This field is filled in according to the rules established by the sender's bank. When generating an electronic payment, the code set by the bank is indicated. If there are no requirements, then leave the field blank. |

| 6 | Suma in cuirsive | Explanation of the amount in words. Kopecks are indicated by numbers; if there are no kopecks, then 00 is entered. For example: “One thousand five hundred rubles 00 kopecks.” |

| 7 | Sum | Here you need to indicate the amount in numbers. Kopecks are written with a “=” or “-” sign. For example: "1500 = 00". |

| 18 | Type of operation | The transaction code is indicated here in accordance with accounting rules. For a payment order - “01”. There are other codes for other types of transactions. |

| 21 | Outline of boards | In accordance with Article 855 of the Civil Code, there is a sequence of payments. The priority depends on the sufficient availability of money in the current account. If there is not enough money, then priority is applied. First of all, funds are written off under executive documents - alimony and compensation for harm to health, secondly - remuneration for labor obligations, third for wages and tax payments, fourth - for other executive documents and fifth - other payments as they are received. . |

| 22 | Code | Unique payment identifier. It is affixed if it was assigned by the sender. If it is not there, then “0” is entered in the field. |

| 24 | Purpose of payment | This field is required. It indicates on what basis the payment is made (date and number of the invoice, agreement or other basis), and indicates the name of the product or service for which the payment is made. The payment is also noted with VAT or without VAT and its amount in numbers if the payment includes VAT. |

Filling out a payment order is not difficult using the “My Business” online service. The service automatically calculates taxes and contributions and generates payments. Thanks to the integration of the service with banks, you can make any payments in a few clicks. You can try the service absolutely free right now.

Try for free

What errors in a payment order can be corrected by clarifying the payment?

Errors in instructions can be corrected, although not all of them. In the table we will show which data can be clarified and which cannot.

Table. What errors in the payment can be clarified

| Cannot be specified | Can you clarify? |

|

|

Just two errors in a document cannot be corrected. This is an incorrect Treasury number and beneficiary bank name. Therefore, the company will have to re-introduce the payment to the budget and return the erroneous transfer upon application.

If mistakes were made in the recipient’s KBK, INN or KPP, the tax authorities will first send a notification to the Treasury. And based on the results of the department’s response, they will inform the company about the results of the clarifications. In total, they are given 10 working days for this.

Most often, errors occur in the KBK. And this is quite understandable. After all, even a typo in one number is already an unreliable detail. For example, instead of BCC for contributions, they wrote down for personal income tax - 182 1 01 02010 01 1000 110. Then, correctly, enter the code - 182 1 0200 160.

Companies also make mistakes in the TIN/KPP of the payer and recipient of money, status in field 101, purpose of payment, etc. These shortcomings can be corrected, the Federal Tax Service and the Pension Fund reported this in a joint letter dated 06.06.2017 No. 3N-4-22/10626a/ NP-30-26/8158.

Results

Formation of a payment order for the payment of tax to the budget requires increased care.

Errors made in indicating the recipient's bank and Federal Treasury account number lead to the fact that the tax is considered unpaid and will have to be paid again. And if the tax is repaid after the deadline for its payment has expired, then financial sanctions may also be imposed on the payer. Other errors in filling out a tax payment order do not entail financial losses and can be corrected by submitting an application to clarify the payment. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

How to fill out field 102

The tax authorities do not assign the code in question to individual entrepreneurs. Therefore, the entrepreneur is not required to fill out field 102 in the payment slip. On the other hand, the payment order should not have empty fields. And it is even more unacceptable to arbitrarily fill in those columns whose meaning is unclear to the payer. In this regard, merchants do not leave field 102 empty (!), but put “0” (zero) in it.

With this method of filling out, the banking institution should not make any claims to the procedure for issuing the payment form.

Also see “Checkpoint of a separate unit: how to find out and receive.”

Read also

02.01.2019

Is it possible to divide the amount by checkpoint when clarifying the payment?

Quote (LETTER dated October 14, 2021 N BS-4-11 / [email protected] ): The Federal Tax Service reviewed the letter on the issue of transferring personal income tax on the income of employees of a separate division and reports the following. In accordance with paragraph 7 of Article 226 of the Tax Code of the Russian Federation (hereinafter referred to as the Code), tax agents - Russian organizations with separate divisions are required to transfer calculated and withheld tax amounts both at their location and at the location of each of their separate divisions. The amount of tax payable to the budget at the location of the separate division is determined based on the amount of income subject to taxation accrued and paid to the employees of these separate divisions. In accordance with paragraph 1 of Article 83 of the Code, for the purpose of tax control, organizations are subject to registration with the tax authorities at the location of the organization, the location of its separate divisions, as well as at the location of the real estate and vehicles owned by them and on other grounds provided for Code. Organizations that include separate divisions located on the territory of the Russian Federation are subject to registration with the tax authorities at the location of each of their separate divisions. A separate subdivision means any territorially separate subdivision, at the location of which stationary workplaces are equipped. Recognition of a separate division of an organization as such is carried out regardless of whether its creation is reflected or not reflected in the constituent or other organizational and administrative documents of the organization, and on the powers vested in the specified division. In this case, a workplace is considered stationary if it is created for a period of more than one month (clause 2 of Article 11 of the Code). According to paragraphs 3 and 4 of Article 83 of the Code: registration of a Russian organization with the tax authority at the location of the branch or representative office is carried out on the basis of information from the Unified State Register of Legal Entities (USRLE); registration of a Russian organization with the tax authority at the location of its separate division (with the exception of a branch, representative office) is carried out on the basis of information from messages submitted by the Russian organization in accordance with subparagraph 3 of paragraph 2 of Article 23 of the Code. In accordance with paragraph 4 of Article 83 of the Code, if several separate divisions of an organization are located in one municipality, the federal cities of Moscow, St. Petersburg, Sevastopol in territories under the jurisdiction of different tax authorities, the organization can be registered by the tax authority according to the location of one of its separate divisions, determined by this organization independently. The organization indicates information about the choice of tax authority in the notification submitted (sent) by the Russian organization to the tax authority at its location. When registering a Russian organization at the location of each of its separate divisions (including in the tax authority selected by the organization in the prescribed manner for each of its separate divisions), a code for the reason for registration (hereinafter referred to as KPP) is assigned (clause 7 of the Procedure and Conditions for Assignment, application, as well as changes in the taxpayer identification number, approved by order of the Federal Tax Service of Russia dated June 29, 2012 N ММВ-7-6 / [email protected] ). The checkpoint assigned to the organization is indicated in the notice of registration in form N 1-3-Accounting, approved by order of the Federal Tax Service of Russia dated 08/11/2011 N YAK-7-6 / [email protected] Features of registration of banks at the location of their separate divisions ( including branches, representative offices) are not provided for by the Code. If each separate division of an organization located in Moscow, St. Petersburg, Sevastopol is assigned a separate checkpoint, a payment order indicating the corresponding separate division of the checkpoint for the transfer of personal income tax must be issued for each such separate division, including in the case when registration of several separate divisions in accordance with paragraph 4 of Article 83 of the Code is carried out at the location of one of them. Acting State Advisor of the Russian Federation, 2nd class S.L. BONDARCHUK

When is tax considered unpaid?

In accordance with sub. 4 p. 4 art. 45 of the Tax Code of the Russian Federation, if the recipient’s account and (or) the name of the bank of the Federal Treasury Department (UFK) is incorrectly indicated in the payment order, the payment is not received into the budget of the Russian Federation or is not credited to the corresponding account of the Federal Treasury. In this case, the taxpayer’s obligation to pay the tax is considered not fulfilled, and it must be transferred again. You must also pay penalties for late payment of taxes. This is the position of the tax department, set out in letters of the Federal Tax Service of Russia dated 09/04/2015 No. ZN-4-1/ [email protected] , dated 03/31/2015 No. ZN-4-1/ [email protected] , dated 09/06/2013 No. ZN-3 -1/3228 and dated 09/12/2011 No. ЗН-4-1/ [email protected]

Read about what actions in such a situation need to be taken in order for the tax to be paid in the articles:

- “What to do if there is an error in the UFK details?”;

- “We made a mistake in the UFK invoice - we didn’t pay the tax.”

The obligation to transfer tax will not be recognized as fulfilled also in the case where errors in indicating the name of the bank or UFC account in the payment order were made due to the fault of the bank. Penalties will be presented to the taxpayer (letter of the Federal Tax Service of Russia dated September 2, 2013 No. ZN-2-1/ [email protected] ). But in such a situation, the taxpayer may demand compensation from the bank for losses incurred (paragraph 9, article 12, article 15 of the Civil Code of the Russian Federation).

At the same time, some courts recognize the tax paid if the UFK account is incorrectly indicated in the payment order. For example, the Federal Antimonopoly Service of the Moscow District, in Resolution No. A40-42830/11-99-191 dated 04/03/2012, recognized that the tax was received into the budget, despite the presence in the payment order of an error in indicating the UFK account.

By the way, the ability to clarify an incorrect account of the Federal Tax Service will soon be directly enshrined in the Tax Code of the Russian Federation.