Variables and constants

This is a very popular classification. Costs are allocated based on how they relate to production volume.

Variable costs

Variable costs are all of a company's costs that depend on production volume. That is, the more products you produce, the more costs you will incur. We described these expenses in detail in the article “What are variable costs.”

Variable costs include:

- payment for raw materials;

- purchasing goods for resale;

- costs for delivery of finished products;

- expenses on electricity and fuel;

- third party services required for production;

- piecework wages for production workers and so on.

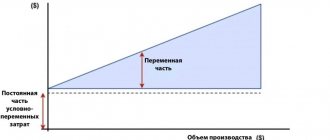

Variable costs are different. Some of them are directly proportional to production output; they are called proportional variables. There are those that grow slower than production volume - degressive costs. On the contrary, there are outputs that are growing faster—progressive ones.

Fixed costs

Fixed costs are contrasted with variable ones. They are in no way dependent on the release. Even if the company does not operate and does not produce anything, costs still arise. For example:

- rent payments;

- salaries of administrative and management personnel;

- depreciation of property;

- part of utility costs;

- costs for banking services, accounting services, auditing, legal advice;

- taxes and contributions from salaries;

- interest on loans;

- entertainment expenses and so on.

We described these costs in detail in the article “What are fixed costs”.

Keep records of exports and imports in the Kontur.Accounting web service. Simple accounting, payroll and reporting in one service

Management accounting and problems of cost classification

Kerimov V.E.

,

Minina E.V.

Published in the issue: Management in Russia and abroad No. 1 / 2002

In economic theory, an approach has been established according to which any commercial enterprise strives to make decisions that would ensure it receives the maximum possible profit. Profit, as a rule, depends mainly on the price of the product and the costs of its production and sale.

The price of products on the market is a consequence of the interaction of supply and demand. Under the influence of the laws of market pricing in conditions of free competition, the price of products cannot be higher or lower at the request of the manufacturer or buyer; it is automatically equalized. Another thing is the costs that form the cost of production. They can increase or decrease depending on the volume of consumed labor and material resources, the level of technology, the organization of production and other factors. Consequently, the manufacturer has many cost-cutting levers that it can use with skillful management.