As you know, an entrepreneur must pay to the treasury for a negative impact on the environment. This is stated in the environmental protection law. Previously, the payment of taxes was regulated by regulations of various departments, but now the legislator has come to the uniformity of established standards related to the protection of the environment from pollution.

From January 2021, violators will pay a fee for the following negative impact:

- emissions into the atmosphere from permanently installed sources;

- discharge of pollutants through runoff into water bodies;

- disposal of industrial waste.

In addition, fees will be charged for noise, magnetic and radiation effects, vibration, etc. The new edition establishes standards that provide for acceptable exposure.

It should be noted that the fee will be paid by enterprises and organizations operating on the territory of the Russian Federation, its continental shelf and in the economic zone of the country. Only business entities belonging to the 4th category received exemption from payment (previously the legislation did not establish such a benefit).

Who should pay for environmental pollution?

Please note that the fee for environmental pollution is sometimes called an environmental fee. But this is an incorrect name, since these are two completely different concepts. Only manufacturers and importers of goods subject to recycling must pay the environmental fee. This article will focus specifically on the payment for environmental pollution in 2021.

As mentioned above, both organizations and individual entrepreneurs must pay for the use of objects in their business activities that negatively affect the environment. At the same time, the obligation to pay a fee arises for all businessmen using any of the taxation systems - simplified tax system, UTII, PSN, OSNO or unified agricultural tax.

It should also be taken into account that the obligation to pay for environmental pollution arises regardless of whether the object is owned or not. That is why payment for negative environmental impact in 2021 is mandatory, including for tenants - that is, persons who operate the facility.

You also need to know that individual entrepreneurs and organizations that use objects that have a negative impact on the environment must register with the territorial branch of Rosprirodnadzor. Order No. 554 of the Russian Ministry of Natural Resources dated December 23, 2015 approved the application form for each such facility.

Where is the environmental fee report submitted?

Importers of goods submit a declaration on the number of finished goods and packaging released into circulation on the territory of the Russian Federation, reporting on compliance with waste disposal standards from the use of goods and calculation of the amount of environmental fees to the central office of Rosprirodnadzor.

Manufacturers of goods submit a declaration on the number of finished goods and packaging released into circulation on the territory of the Russian Federation, reporting on compliance with waste disposal standards from the use of goods and calculation of the amount of environmental fees to the territorial body of Rosprirodnadzor in their constituent entity of the Russian Federation.

If a company produces and imports goods simultaneously, a set of documents is submitted to the central office of Rosprirodnadzor.

If there is no waste due to a temporary cessation of activity, then you need to send a letter in any form and submit documents from the tax office about the zero balance.

Who shouldn't pay for environmental pollution?

Naturally, garbage generated during all types of activities by both organizations and individual entrepreneurs pollutes the environment, and you have to pay for it. In this case, it is necessary to distribute responsibility for payments in such a way as to avoid double taxation.

As a general rule, garbage fees are charged when placing production and consumption waste. And here it is important to understand what constitutes waste disposal, because in everyday life, by disposal we mean storing waste in ordinary trash cans.

In a specific case, waste disposal means not just the storage of waste, but its maintenance in special facilities for subsequent disposal, for example, in special landfills or landfills (Article 1 of the Federal Law of June 24, 1998 No. 89-FZ, hereinafter referred to as Law No. 89- Federal Law).

Therefore, if an individual entrepreneur or organization simply throws office or commercial waste into a container standing on the street, and it is already removed by an organization with which an agreement has been concluded for the removal and placement of waste, then there is no need to pay an environmental fee in this case.

According to the Decree of the Government of the Russian Federation of June 12, 2003 No. 344, payment is made only for the disposal of production and consumption waste. Those. The obligation to pay the fee for environmental pollution rests with the organization involved in the removal and disposal of waste. Make sure that the contract concluded with such an organization states that ownership of the garbage passes from your organization to it.

Russian legislation (clause 1 of Article 16.1 of the Law of January 10, 2002 No. 7-FZ) also provides for categories of organizations and individual entrepreneurs that do not pay for environmental pollution. The law covers individual entrepreneurs and organizations that operate at hazardous category IV facilities, where:

- there are no releases of radioactive substances;

- there are no discharges of pollutants generated when using water for industrial needs into sewers, into the environment, into surface and underground water bodies, as well as onto the earth's surface;

- there are stationary sources of pollutant emissions, and their amount does not exceed 10 tons per year;

- There are only non-stationary sources of pollutant emissions.

The concept of stationary and non-stationary sources was first defined by the legislator only in 2014 (Federal Law No. 219-FZ of July 21, 2014). This Law amended 94-FZ “On Environmental Protection”, which is the main law regulating the issues of payment for environmental pollution.

In paragraph 1 a definition appeared:

- stationary source - a source of release, the location of which is determined using a unified state coordinate system or which can be moved by a mobile source;

- mobile source - a vehicle whose engine is a source of emissions during operation.

Also, Law No. 219 Federal Law amended paragraph 1 of Art. 16 of Federal Law No. 7-FZ, which determines that from 01/01/2016, fees for NVOS will be charged only for emissions from stationary sources.

Rosprirodnadzor assigns certain hazard categories when registering objects in the state register. That is, if you do not know the hazard category of your facility, you should contact Rosprirodnadzor to clarify the data.

Please note that the environmental fee and the pollution fee are two different fees!

Features of calculating fees for NVOS

A similar calculation must be made for emissions resulting from the combustion of associated petroleum gas, for discharges into water sources and for fees for waste disposal. More information about reduction factors for waste disposal can be found in Federal Law dated December 29, 2015 N 404-FZ.

Entrepreneurs also have the opportunity to reduce the amount of tax. To do this, it is necessary to take actions throughout the year to reduce NVOS. If these activities are properly documented, they can be used to deduct from the total.

If an entrepreneur decides not to provide a calculation of the fee for the tax assessment at all, then he may face administrative liability. This will be a fine not for the fact that the calculation of the fee for the tax assessment was not provided, because such an article of the Code of Administrative Offenses does not yet exist, but these actions can be qualified as concealment of environmental information. As a result, a fine may be imposed: on officials in the amount of 1,000 to 2,000 rubles, on legal entities - from 10,000 to 20,000 rubles. Paying a fine does not relieve you of the need to provide an estimate of the fee for the tax assessment.

Tariff rates for environmental pollution

The Federal Service for Supervision of Natural Resources or Rosprirodnadzor, on the basis of Decree of the Government of the Russian Federation dated December 29, 2007 No. 995, controls the calculation of fees for negative environmental impacts in 2021 and its timely transfer to the federal budget.

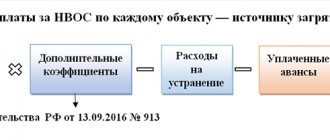

Please note that the old procedure for calculating payment, starting from September 23, 2021, ceased to apply (Resolution of the Government of the Russian Federation of September 13, 2021 No. 913 canceled the resolutions of November 19, 2014 No. 1219 and of June 12, 2003 No. 344 , which contained the calculation rules).

Rates for environmental pollution for 2021 were approved by Decree of the Government of the Russian Federation dated September 13, 2016 N 913, as last amended from 29.06.2018.

Tariff rates are set depending on the categories of pollutant emissions:

- for emissions of pollutants into the air from stationary sources;

- for discharges of pollutants into water bodies;

- for the disposal of production and consumption waste according to their hazard class.

For 2021 , it is proposed to establish a coefficient of 1.08 for the rates of payment for negative impact on the environment.

Table “Tariffs for emissions of pollutants into the air from stationary sources in 2019-2020”

Resolution No. 193 dated September 13, 2016, the latest edition dated June 29, 2018, contains 159 names of pollutants for this category. Here are the most common ones found in production. According to the above resolution, rates for 2021 have been increased by 1.04 compared to 2021.

For 2021, as mentioned above, the Government of the Russian Federation plans to establish a coefficient of 1.08 for the rates of payment for negative impact on the environment. But let’s not rush for now, but wait for the Russian Government’s Decree to be issued establishing the coefficient for 2021. Once the relevant regulations are published, we will update this page with accurate rates for 2021.

While, at the beginning of 2021, the Government has not implemented its plans to create a legislative document, the rates established for 2021 apply.

| Name of pollutant | Rate in rubles (per ton) | Years |

| Nitric acid | 38.064 | 2019 |

| 36.6 | 2018 | |

| Mercury and its compounds (except diethylmercury) | 18973.9 | 2019 |

| 18244.1 | 2018 | |

| Ammonia | 144.4 | 2019 |

| 138.8 | 2018 | |

| Sulfuric acid | 47.2 | 2019 |

| 45.4 | 2018 | |

| Hydrogen sulfide | 713.6 | 2019 |

| 686.2 | 2018 | |

| Benz(a)pyrene | 5691887.4 | 2019 |

| 5472968.7 | 2018 |

Table “Tariffs for emissions of pollutants into water bodies in 2019-2020”

Resolution No. 193 dated September 13, 2016, the latest edition dated June 29, 2018, contains 159 names of pollutants that are released into water bodies. Here are the names of the most frequently encountered ones in production.

| Name of pollutant | Rate in rubles (per ton) | Years |

| Aluminum | 17630.7 | 2019 |

| 18388.3 | 2018 | |

| Beryllium | 1900943.1 | 2019 |

| 1983592.8 | 2018 | |

| Ammonia | 14105.6 | 2019 |

| 14711.7 | 2018 | |

| Benz(a)pyrene | 76495539 | 2019 |

| 73553403 | 2018 |

Table “Tariffs for the disposal of industrial and consumer waste by their hazard class in 2019-2020”

| Waste hazard class | Rate in rubles (per ton) | Years |

| Hazard class I (extremely dangerous) | 4643.7 | 2019-2020 |

| Hazard class II (highly hazardous) | 1990.2 | 2019-2020 |

| III hazard class (moderately dangerous) | 1327 | 2019-2020 |

| IV hazard class (low hazardous) | 663,2 | 2019-2020 |

| Solid municipal waste of hazard class IV (low-hazard) | 194,5 | 2019-2020 |

| Hazard class V (virtually non-hazardous): processing industry | 40.1 | 2019-2020 |

| Hazard class V (virtually non-hazardous): mining industry | 1.1 | 2019-2020 |

| other | 17.3 | 2019-2020 |

From March 17, 2021, new rules for calculating and collecting Fees for Tax Assessments began to work, approved by Decree of the Government of the Russian Federation dated March 3, 2017 No. 255 (hereinafter referred to as the Rules).

Now, for certain cases, formulas have been developed for calculating fees for emissions (discharges) of pollutants and waste disposal, which are valid in 2021:

- in the absence of permits for emissions (discharges) of harmful substances; (clause 17-21 of the Rules);

- in the absence of documents approving waste generation standards and limits on their disposal (clauses 17-21 of the Rules);

- in other cases (clauses 12-16, 22 of the Rules).

If an organization has several facilities, but only part of them belongs to hazard category IV, then payment for pollution will have to be paid for all of the enterprise’s facilities, including category IV.

How is the fee for the tax assessment calculated?

The NVOS declaration form was approved by Order No. 3 of the Ministry of Natural Resources dated January 9, 2017; it can be downloaded on the Ministry of Natural Resources website in the “Documents” section, in the “Official Documents of the Russian Ministry of Natural Resources” tab.

On page 1, fill in the entrepreneur’s details.

On the 2nd page there is a section “Calculation of the amount of payment to be included in the budget.” The 20th line indicates the total amount for all 4 types of IEE. The following lines indicate the amounts for each type separately.

The 40th line shows the amount of emissions into the atmosphere. Detailed calculations must be provided in section 1 of the declaration.

The fee rate per ton for each type of pollutant can be found in Decree of the Government of the Russian Federation dated September 13, 2021 No. 913.

Information is also required on maximum permissible emissions and temporarily agreed upon emissions of pollutants determined by Rosprirodnadzor for the enterprise.

The enterprise itself needs to keep records of emissions into the atmosphere in order to fill in the lines about the amount of emissions within the approved standards (MPE), within the approved temporarily agreed standards (ATS), in excess of the approved standards and temporary standards.

Each limit has its own increasing coefficient: MPE – 1.0, VSV – 5.0, above the limit – 25.0.

Now you need to multiply the coefficient by the corresponding accounting data for the fee rate per ton. By adding up the three amounts, we get the total payment amount for the year.

Payment deadlines for environmental pollution in 2020

The deadline for payment for environmental pollution in 2021, with the exception of small and medium-sized businesses, is no later than the 20th day of the month following the reporting quarter. For the fourth quarter of 2021, payment does not need to be transferred.

Advance payment for each quarter of 2021 = ¼ of the payment amount for the previous year.

Let's give an example. The payment amount for 2021 was 170,000 rubles. Based on paragraph 3 of Article 16.4 of the Law of January 10, 2002 No. 7-FZ, it is necessary to transfer advance payments in this amount within the following terms:

- for the 1st quarter - no later than April 20, 2021 - 42,500 rubles;

- for six months - no later than July 20, 2021 - 42,500 rubles;

- for 9 months - no later than October 20, 2021 - 42,500 rubles.

Based on clause 3 of Art. 16.4 of Law No. 7-FZ of January 10, 2002, the total amount of payment for negative environmental impact for 2021 must be transferred to the budget no later than March 1, 2021.

This payment procedure led to overpayments of tax.

According to amendments to Law No. 7-FZ, which was supposed to come into effect on January 1, 2018, individual entrepreneurs or organizations obligated to pay quarterly fees for NVOS have the right to choose which of three ways to calculate and pay the amount of the quarterly advance payment:

- 1/4 of the amount of the tax assessment fee paid for the previous year.

- 1/4 of the amount of payment for the NEE, calculated on the basis of established standards for permissible emissions, discharges of pollutants, temporarily agreed upon emissions, temporarily agreed upon discharges and limits on the disposal of production and consumption waste.

- Equal to the amount of payment for environmental impact assessment calculated for the actual negative impact on the environment in the past quarter based on industrial environmental control data.

In the declaration of payment for the tax assessment, you will need to indicate which of the three payment and payment methods is chosen by the individual entrepreneur or organization.

And after two years of waiting for these much-needed changes, on December 27, 2019, Federal Law No. 450-FZ was adopted, which amended Article 16.4 of Federal Law No. 7-FZ “On Environmental Protection”.

Article 16.4 of this law looks like this:

Article 16.4. Procedure and deadlines for paying fees for negative environmental impact

Persons obligated to pay a fee have the right to choose one of the following methods for determining the amount of the quarterly advance payment for each type of negative environmental impact for which a fee is charged:

1. In the amount of one-fourth of the amount of the fee for negative impact on the environment payable (taking into account the adjustment of the amount of the fee carried out in accordance with paragraphs 10 - 12.1 of Article 16.3 of this Federal Law) for the previous year.

2. In the amount of one-fourth of the amount of payment for negative impact on the environment, in the calculation of which the payment base is determined based on the volume or mass of emissions of pollutants, discharges of pollutants within the limits of permissible emission standards, permissible discharge standards, temporarily permitted emissions, temporarily permitted discharges, limits on disposal of production and consumption waste.

3. In the amount determined by multiplying the payment base, which is determined on the basis of industrial environmental control data on the volume or weight of emissions of pollutants, discharges of pollutants, or the volume or weight of disposed production and consumption waste in the previous quarter of the current reporting period, by corresponding rates of payment for negative impact on the environment using the coefficients established by Article 16.3 of this Federal Law.”

Therefore, now it is possible to choose the appropriate option and avoid overpaying funds.

Small and medium-sized businesses do not calculate or make advance payments for the tax assessment. For this category of business, a one-time payment deadline has been determined until March 1, 2020 for 2021.

How is the fee for negative environmental impact calculated?

Payment for negative impact on the environment is calculated based on the actual amount of emitted pollutants, discharged pollutants, disposed waste (Article 16.2 of the Federal Law “On Environmental Protection”) for the reporting period.

- Emissions of pollutants are taken into account for each operated source during the reporting period, according to the emissions logbook.

- Discharges of pollutants - according to the wastewater quality logbook. I would like to draw your attention to the fact that if the discharge occurs into centralized wastewater systems, then the payment is made by the organization receiving the wastewater from your enterprise. And you are already paying this organization its expenses.

- Placed waste - according to the waste logbook. Payment is not made for waste accumulated at the enterprise, for waste transferred for recycling or neutralization.

When calculating the negative impact fee, you must take into account the available permitting documentation:

- within the limits of emissions, discharges and above;

- within the limits of temporarily permitted emissions, discharges and above;

- within the limits for the disposal of production and consumption waste and above.

Advance payments in 2021: payment deadlines

The total amount of the 2021 environmental pollution fee, minus advance payments, must be paid by March 1, 2021. Advance payments in 2021 are paid within the following terms:

- for the 1st quarter of 2021 - until April 20, 2021;

- for the first half of 2021 - until July 20, 2021;

- for 9 months 2021 - until October 20, 2021.

And the total amount of the fee for 2021 for environmental pollution, minus advance payments, must be paid before March 1, 2021.

Procedure for paying fees for environmental pollution and BCC in 2021

Payment orders for the transfer of fees for environmental pollution in 2021 should be drawn up in the same way as orders for the payment of taxes (insurance contributions) - that is, according to the general rules. Please note that the payment amount must be transferred to the bank in one payment order to the accounts of the territorial departments of the Federal Treasury. This is stated in the letter of the Ministry of Finance of Russia dated July 24, 2008 No. 03-06-06-04/1.

When filling out payment orders, indicate the KBK of Rosprirodnadzor, which is the administrator of budget revenues in the form of fees for environmental pollution (Appendix 7 to the instructions approved by Order of the Ministry of Finance of Russia dated July 1, 2013 No. 65n).

Thus, in 2021, the BCC for payment is as follows: 048 1 12 010X0 01 6000 120 , where X is the type of environmental pollution.

We present the BCC in table form:

| Payment name | KBK 2021 |

| For releases into water bodies | 048 1 1200 120 |

| For the disposal of production and consumption waste | 048 1 1200 120 |

| For emissions into the atmosphere by stationary objects | 048 1 1200 120 |

| For other types of negative impact on the environment | 048 1 1200 120 |

All current BCCs for 2021 are posted on this page.

In conclusion, we would like to add that if an organization (or individual entrepreneur) does not have objects that have a negative impact on the environment, then they do not need to register with Rosprirodnadzor or pay for garbage.

The material was updated in accordance with current legislation 01/13/2020

Who pays the fee and objects of taxation

The payment applies to individuals and legal entities, including foreign ones, to enterprises, organizations, institutions, individual entrepreneurs who conduct activities in the Russian Federation related to the use of natural resources.

The objects of taxation are stationary objects : objects on the ground that pollute the soil or emit harmful substances into the air; facilities where waste is stored (dump, landfill, storage, etc.).

A fee is charged for each object.

Since January 1, 2015, no payment will be collected for air emissions from vehicles of organizations and individual entrepreneurs.

Based on their impact on the environment, objects are divided into groups:

| Level of negativity | Group |

| significant | 1 |

| moderate | 2 |

| minor | 3 |

| minimum | 4 |

Objects of group 4 are exempt from paying the payment.

This might also be useful:

- Which OKVED code should be indicated in the reporting for 2021?

- Reduced insurance premium rates in 2021

- Deflator coefficient for the simplified tax system for 2021

- Individual entrepreneur insurance premiums for employees in 2021

- Inspection of individual entrepreneurs by the tax inspectorate

- Fixed payments for individual entrepreneurs in 2021 for themselves

Is the information useful? Tell your friends and colleagues

Dear readers! The materials on the TBis.ru website are devoted to typical ways to resolve tax and legal issues, but each case is unique.

If you want to find out how to solve your specific issue, please contact the online consultant form. It's fast and free!

Comments

View all Next »

Ulyana 05/16/2017 at 07:29 # Reply

Thank you for such an informative and at the same time “short” (“no water”) article, everything is clear. this information helped me a lot in my work

ostapx1 05/16/2017 at 14:03 # Reply

It's nice to hear gratitude. Thank you. We are trying.

06/30/2017 at 01:13 pm # Reply

clothing industry

Good afternoon, please tell me, do you need to pay taxes for sewing production for environmental pollution and negative impact on the environment? Thank you very much

07/01/2017 at 14:34 # Reply

Good afternoon. According to (clause 1 of Article 16.1 of the Law of January 10, 2002 No. 7-FZ), you are not a tax payer for environmental pollution and for negative impacts on the environment.

07/20/2017 at 09:49 # Reply

Company.

Good morning! Please tell me whether it is necessary to pay for the negative impact if we only own 2 cars. Thank you!

ostapx1 07/20/2017 at 07:40 pm # Reply

Good afternoon. There is no charge for negative impacts from the use of mobile objects, which are your cars. Explanations are available in the letter of the Ministry of Natural Resources dated July 23, 2015 No. 02-12-44/17039).

07/20/2017 at 10:47 am # Reply

Advance payment

Tell me, if the advance payment for the 2nd quarter of 2021 is paid later than July 20, 2021, will this be a violation?

12/28/2017 at 01:38 pm # Reply

SNT

Hello, please tell me, should SNT pay for the NVOS? We have a waste site, but we only collect it and a specialized organization removes it. We don't store anything...

01/16/2018 at 14:45 # Reply

Good afternoon. According to paragraph 3, clause 5 of the Rules for calculating and collecting Fees for NVOS, approved. fast. Government of the Russian Federation dated March 3, 2017 No. 255, when disposing of solid municipal waste, payers are regional operators and operators involved in such disposal.

01/03/2018 at 14:05 # Reply

OOO

Should I pay a negative impact fee for a retail store?

01/16/2018 at 15:01 # Reply

Good afternoon. The following categories of entrepreneurs who carry out: - emissions of pollutants into the air from stationary sources must pay for the negative impact on the environment; — discharges of pollutants into water bodies; — storage, disposal of production and consumption waste. In all likelihood, you have solid household waste, regarding which Rosprirodnadzor, in its letter dated February 21, 2017 No. AS-06-02-36/3591), explained that entrepreneurs who only have solid municipal waste are not required to pay a fee for pollution .

01/16/2018 at 06:53 # Reply

Hello! We pay Vodokanal for receiving wastewater that exceeds the standards for permissible concentrations of pollutants, should we pay a fee for environmental pollution? Thank you!

01/16/2018 at 15:15 # Reply

Good afternoon. The answer to your question is given in the letter of Rosprirodnadzor dated February 20, 2015 N OD-06-01-31/2606 “On payment for wastewater discharges.” According to Federal Law dated December 29, 2014 N 458-FZ, Part 1, Art. 28 of the Law, which came into force on July 1, 2015, whether to pay the NVOS or not depends on the category of the subscriber. If an organization is subject to rationing, in accordance with Decree of the Government of the Russian Federation dated March 18, 2013 N 230, then it (the organization) must pay fees for the negative impact on the environment directly to the budgets of the budgetary system of the Russian Federation, and not to water supply and utility organizations. For the second non-standardized group of subscribers, Resolution No. 1310 of December 31, 1995 continues to apply, which determines that “executive authorities of the constituent entities of the Russian Federation determine the procedure for collecting fees for the discharge of wastewater and pollutants into the sewerage systems of populated areas from enterprises and organizations that discharge wastewater and pollutants into the sewerage systems of populated areas (hereinafter referred to as subscribers), providing for measures of economic sanctions for damage to the environment, including for exceeding the standards for the discharge of wastewater and pollutants.” Those. in this case, the tariff includes the amount of payment for the NVOS.

01/25/2018 at 01:02 pm # Reply

Good afternoon. Please tell me, we have retail shoe stores, do we need to pay taxes for environmental pollution and negative impact on the environment?

01/25/2018 at 15:36 # Reply

Good afternoon. When carrying out your activities, you must submit a 2-TP waste report by 02/01/2018 for 2021. If your enterprise is a small or medium-sized enterprise, you had to submit the SME report by January 15, 2018. If only solid municipal waste remains from your activities, then no environmental pollution fee is paid. For the negative impact on the environment, environmental users pay a fee; the store is not one of them.

02/08/2018 at 01:16 pm # Reply

cadastral activities.

Good afternoon Does an individual entrepreneur engaged in cadastral activities need to pay taxes for environmental pollution and negative impact on the environment? Thank you!

02/08/2018 at 18:39 # Reply

Good afternoon. If your enterprise is not a natural resource user, then you do not need to pay a fee for negative impact on the environment (the same as for environmental pollution). Individual entrepreneurs and LLCs that operate only at sites of hazard category IV are exempt from paying fees for negative impacts on the environment. Such facilities include: facilities with stationary sources of pollutant emissions, but the amount of emissions does not exceed 10 tons per year; there are no releases of radioactive substances; there are no discharges of pollutants that are formed when water is used for industrial needs, into sewers and into the environment (into surface and underground water bodies, onto the earth's surface). Therefore, your organization does not have to pay an impact fee. You had to provide reports - 2TP waste and SMEs (if you are not a micro-enterprise).

02/10/2018 at 11:57 pm # Reply

Dentistry

Good afternoon, we have a dental office, please tell us, for 2021 we need to submit both a declaration of fees and calculation of fees for negative impact on the environment? Thank you.

02/12/2018 at 05:15 pm # Reply

Good afternoon. The situation with payment for NVOS and the provision of Calculation of fees for NVOS when disposing of medical waste is currently not properly regulated. In the letter of the Ministry of Natural Resources No. 12-50/1025-OG dated February 12, 2015, it is explained that the provisions of the Law on Waste, as well as regulatory legal acts of the Russian Ministry of Natural Resources in the field of waste management, do not apply to medical waste. Therefore, until amendments are made to regulatory legal acts, no fee will be charged for the negative impact on the environment when disposing of medical waste. All that remains is not to miss when these amendments are made.

View all Next »

How to calculate the payment base for pollutants and waste

In accordance with paragraph 1 of Art. 16.2 of Law No. 7-FZ, the payment base for substances and waste corresponds to their volume (or mass) released into the environment within the reporting period. The amount of the base is determined by the payer in accordance with the procedure for environmental control (clause 2 of Article 16.2 of Law No. 7-FZ). The types of pollution that are subject to payment are (Article 16 of Law No. 7-FZ):

- emissions from stationary sources;

- discharges into water bodies;

- waste storage and disposal.

When calculating the base under consideration, the following are taken into account (clause 4 of article 16.2 of law No. 7-FZ):

- standards for permissible pollution;

- standards for temporarily permitted pollution, as well as emissions and discharges that exceed them (including for emergency reasons);

- limits on the placement of pollution and their exceeding.

In accordance with the norms of resolution No. 255:

- emission standards and limits must be calculated separately for each production facility from which emissions occur (these standards can be found by contacting Rosprirodnadzor);

- the enterprise must independently (or with the involvement of experts) calculate the actual volumes of emissions and correlate them with the standards;

- The amount of the fee may be reduced due to:

- deductions representing the amount of costs to reduce the polluting impact on the environment;

- application of incentive coefficients to payment rates.

The fee is calculated by adding:

- the product of standard indicators and the established rate for them;

- the product of emission indicators in excess of standards and the established rate for them.

In some cases, temporary standards—limits—are also taken into account. The product of the indicators of their actual value, its excess and the corresponding rates is added to the amount according to the usual standards.

If the payer is engaged in waste disposal and belongs to the category of large business, then in order to obtain standards he must submit a waste disposal project to Rosprirodnadzor (clause 4 of Article 18 of Law No. 89-FZ, guidelines approved by Order of the Ministry of Natural Resources of Russia dated 05.08.2014 No. 349 ). Small and medium-sized businesses that dispose of waste do not need to develop appropriate projects - they only need to report to the department on activities that involve emissions of harmful substances into the environment (Clause 7, Article 18 of Law No. 89-FZ).

If a company or individual entrepreneur generates waste of hazard classes 1–4, passports must be drawn up for them (Clause 3, Article 14 of Law No. 89-FZ). They must be stored in the payer's archive. Certified copies of such passports with documents confirming the hazard class of the emitted substances are sent to Rosprirodnadzor (clause 7 of the rules established by Decree of the Government of the Russian Federation of August 16, 2013 No. 712).

ConsultantPlus experts explained how to correctly calculate fees for negative environmental impact. If you have access to ConsultantPlus, check whether you have calculated the payment amount correctly. If you don't have access, get a trial online access to the legal system and proceed to the calculation example for free.