A number of professions are closely related to the need for employees to perform their labor functions away from their permanent place of work.

The duration of such business trips is determined by management in compliance with the duration limit established by law - sufficiency to complete the established task (Article 72.1 of the Labor Code of the Russian Federation).

Business trips that begin in one month and continue into the next are called rolling and have some features in making payments for them.

How to pay if the trip goes to the next month?

Consequently, Article 167 of the Labor Code of Russia and paragraph 9 of Regulation No. 749 of the Government of the Russian Federation of October 13, 2008, payment to an employee for time spent on a business trip is made according to his average earnings, calculated in accordance with Regulation No. 922, approved by the Government of Russia.

Paragraph 4 of the above-mentioned Regulation No. 922 establishes the procedure for calculating average earnings: all payments provided for in the specified act for the 12 calendar months that precede the period for which the employee must maintain the average salary are taken into account.

That is, if a business trip begins on October 15, 2021, and ends on November 6, 2021, the average earnings are calculated on October 15 - the billing period from year to year. The amount received will be considered average earnings for the entire duration of the business trip.

Local acts of the enterprise (organization) may establish an additional payment up to the salary of employees who were on a business trip.

This is necessary due to the fact that the average earnings for all days of a business trip are less than the payment that would be due to such an employee if he remained at a permanent place of work.

When is payment due?

Articles 8 and 9 of the Labor Code of Russia establish the obligations of employers to maintain for all employees the circle of guarantees provided for by this regulatory legal act.

The Labor Code of the Russian Federation establishes the provision that wages must be paid to employees at least twice a month.

It does not matter whether the employee is on a business trip or is at a permanent place of work.

The average earnings due to each posted worker are equal to wages and must be accrued to employees on the days of payments established by the collective labor agreement.

Payroll for a seconded employee during a moving business trip is calculated in two parts. The average salary for a business trip for all days of the month in which it began should be given to the employee on the day the salary for that month is calculated.

Accordingly, for all remaining days - on the day of payment of wages for the month in which the business trip was completed.

Calculation of average earnings

A distinctive feature of calculating average earnings for a moving business trip is the presence of two calculation periods: for the month in which the employee went on a business trip and for the month in which he returned from it.

Business travel days are paid according to each billing period.

The following payments for the corresponding billing period are taken into account:

- Accrued salaries or tariff rates;

- Piece wages;

- Remuneration received in non-monetary form;

- Commission remuneration;

- Salary as a percentage of revenue;

- Maintenance of municipal employees;

- Remuneration for citizens who hold government positions in the Russian Federation;

- Salaries of teachers (teachers) for the excess number of hours worked;

- Royalties and royalties of cultural workers;

- Salary calculated for the previous calendar year, determined by the payment system;

- Additional payments that are made in accordance with special working conditions;

- Remuneration for teachers (teachers) who conduct classroom management;

- Rewards, bonuses;

- Other types of cash accruals that are provided by a specific employer.

Any social charges, as well as irregular payments, are not taken into account.

Example

Initial data:

The employee was posted from year to year. The calculation period for which the average daily earnings will be determined: from November 2017 to October 2021 and from December 2021 to November 2021.

The amount of wages for the specified first period, including bonuses, allowances and indexation is 530,000 Russian rubles, and the number of days worked, noted in the accounting report card, is 246. Business trip working days for November 2021 is 5.

The salary for the second of the two periods indicated above is 520,000 Russian rubles, days worked - 248. Working days spent on a business trip is equal to 1.

Calculation:

We calculate wages during a business trip:

First billing period: 530,000/246 * 5 = 2154.47 * 5 days = 10,772.36 Russian rubles.

Second billing period: 520,000/248 * 1 = 2096.77 * 1 day = 2096.77 Russian rubles.

Average earnings for the entire period of the business trip: 10,772.36 + 2096.77 = 12869.13 Russian rubles.

conclusions

A business trip that begins in one month and ends in the next is considered a rolling trip.

Due to the peculiarities of payment for the time spent by employees on business trips, the average earnings of posted workers are calculated in two calculation periods corresponding to the start date of the business trip and the first day of the month to which part of such a work trip began.

Remuneration for employees assigned to perform their labor functions at another enterprise (organization) is made on the days of payment of wages to all employees, as provided for in the collective labor agreement.

Calculation of travel allowances

Funds issued on account to an employee during business trips abroad can be either in Russian rubles or in the currency of the country where the employee is sent. After arrival, recalculation is made at the National Bank rate. There are also a number of nuances when traveling for different periods.

One day business trip

Since the minimum duration of a business trip is not established by law, the employer has the right to send an employee to another locality for one day. If the connection with economic activity is confirmed, such a trip is recognized as a business trip with payment for travel.

The nuances compared to the usual ones are that for a one-day business trip, daily allowances within Russia are not provided, and for an overseas trip - no more than 50% of the amounts established by local documents.

Formally, it turns out that the company cannot pay compensation without being subject to personal income tax and social contributions. The recommendation is to create a clause in internal documents that explains the employee’s lack of economic benefit, thereby avoiding personal income tax. Indirect confirmation in support of this position is the letter of the Ministry of Finance of the Russian Federation dated No. 03-04-07/6189.

Business trip exceeding daily allowance

An enterprise, by means of an internal administrative document, has the right to standardize the amount of daily allowance, both downward and upward. The specific amount is fixed in the employment contract with the employee and can be differentiated among employees.

For example, an employee went on a business trip to, and arrived at, the daily allowance according to the internal regulations is 900 rubles. Then:

- The number of days is 10, since they are included in the calculation.

- Daily allowance exceeding the limit: (900-700)*10=2000 rubles;

- Personal income tax: 2000*0.13=260 rubles.

In addition to personal income tax, it is necessary to accrue taxes on daily allowances in excess of the limit to social funds except for injuries, and not include them in expenses that form taxable profit.

To fully calculate travel allowances, you need to add documented expenses associated with financial and economic activities.

Rotating business trip

In practice, situations often arise when an employee goes on a business trip in one month and returns in another reporting period. If the trip goes to the next month, how to pay for the business trip, when and in what amount should it be included in expenses? Are there any restrictions on paying an advance? – questions that arise for accountants.

Example: For example, a production worker left for a neighboring locality, but arrived in accordance with the order. He presented a transport ticket for departure in the amount of 1,500 rubles excluding VAT and for entry in the amount of 1,400 rubles, and a hotel bill in the amount of 5,000 rubles. he was given an advance in the amount of 6,000 rubles in cash. The daily allowance is 500 rubles according to the employment contract. The report was provided by .

The accounting entries are shown in the table:

Travel and daily allowances

developer 9 — 07/13/05 — 10:37 (7) Yes, there are such situations, but we don’t have large enough business trips, and the salary is dumped on cards. Gena 10 - 07/13/05 - 11:28 then make TWO payment dockets according to the average Advertising space is empty List of forum topics Forum Territory 1C Advertising space is empty Advertising space is empty Automate routine operations with 1C databases through the batch mode of the configurator. Important

ATTENTION!

If you have lost the message input window, press Ctrl-F5 or Ctrl-R or the Refresh button in your browser. The thread has been archived. Adding messages is not possible. But you can create a new thread and they will definitely answer you! More than 2000 people visit the Magic Forum every hour. New accounting", 2006, N 10Question: An employee of the organization was sent to the official

How to calculate travel allowances in 2021

All posted workers are guaranteed reimbursement of expenses based on Ch. 24 of the Labor Code of the Russian Federation. For commercial organizations and individual entrepreneurs, the legislation establishes only general recommendations, while for public sector institutions strict standards apply (Government Decree No. 916 dated and No. 749 dated).

Travel expenses include:

- expenses for travel to and from the place of business travel;

- living expenses;

- additional expenses for accommodation (per diem);

- average earnings;

- other expenses permitted by the employer.

What is considered a business trip?

The concept of a business trip is deciphered quite simply: it is the departure of an employee by order of his superiors to other localities to carry out any assignments for a strictly defined period.

At the same time, the employee of the enterprise retains his workplace during his absence from his permanent place of work, as well as his average salary.

In addition, the organization is obliged to reimburse all expenses associated with the business trip.

What documents confirm travel expenses for travel using an electronic ticket ?

Legislative regulation

According to the Labor Code (LC) of Russia (Article 166), a business trip is a trip by an employee, by order of the employer, to another locality to perform a specific individual task for a certain period (concluding contracts, escorting cargo, participating in seminars and symposiums, checking the activities of subordinate organizations). If the specific work is of a traveling nature (geologists, truck drivers, shift work), then the trip does not qualify as a business trip.

The Labor Code of the Russian Federation guarantees reimbursement of travel expenses (Article 167), and regulates the list (Article 168):

- Payment for travel in the presence of supporting documents for actual expenses not exceeding the cost:

- by rail - a compartment car of a passenger or fast train;

- by plane - economy class cabin;

- by motor transport – means of transport for public use, with the exception of taxis.

- Expenses for renting premises - an invoice from the hotel containing the details:

- name of the organization or individual indicating the relevant individual data;

- information about the room provided and the range of services (if meals are included, it must be written on a separate line);

- prices per day, number of days and total cost.

- Per diem – expenses reimbursed by an enterprise or entrepreneur for each full or partial calendar day of travel, regardless of the operating mode, including weekends, holidays and travel time. According to Article 217 of the Tax Code of the Russian Federation in 2021, in order to avoid personal income tax, the accrual of daily allowances cannot exceed:

- within the Russian Federation – 700 rubles;

- in the near and far abroad – 2500 rubles.

The enterprise has the right to fix any amount of daily allowance in local internal documents, however, personal income tax must be withheld from the excess amount and contributions to the pension fund and social insurance fund must be calculated, as well as excluded from expenses that reduce taxable profit.

Payment procedure and payment date for business trips

In the Business trip , it is enough to correctly fill out the payment order for the business trip ( With salary , With advance payment or During the interpayment period ) so that the program automatically fills out payment forms correctly.

Income in the form of payment during a business trip for personal income tax purposes is accounted for using code 2000 Remuneration for the performance of labor or other duties; salary and other taxable payments to military personnel and equivalent persons. The date of receipt of this income is defined in the program as the last day of the accrual month, so filling out the Payment Date in the Business Trip is not as important as, for example, in the Sick Leave or Vacation .

Is it possible to calculate not the average earnings, but the salary during a business trip?

When sending an employee on a business trip, the employer is obliged to pay him the average salary for all working days at his place of permanent work that fall during the business trip <1>.

But some accountants, in order not to make unnecessary calculations, pay seconded workers a salary instead of average earnings. Is it possible to pay for a business trip this way?

<1> Article 167 of the Labor Code of the Russian Federation; clause 9 of the Regulations on the specifics of sending employees on business trips, approved. Decree of the Government of the Russian Federation No. 749.

Average earnings: determining the billing period in difficult situations

The article from the magazine “MAIN BOOK” is current as of October 7, 2011.

Contents of the magazine No. 20 for 2011 M.N. Naumchuk, accountant

As a general rule, the calculation period for determining the average earnings retained by an employee during his stay, for example, on a business trip or for a medical examination, consists of 12 calendar months preceding this period. 139 Labor Code of the Russian Federation; clause 4 of the Regulations on the specifics of calculating average wages, approved. Decree of the Government of the Russian Federation dated December 24, 2007 No. 922. And if the beginning and end of the period for which the average earnings need to be paid fall within the same calendar month, then there are no problems with the calculation. Questions arise when the beginning and end of this period fall in different months.

For example, a business trip begins on August 29 and ends on September 9, 2011. Is it possible to take one pay period from August 1, 2010 to July 31, 2011 to calculate average earnings for all this time? Or you need to separately determine the average earnings saved during a business trip:

- from August 29 to August 31 with a billing period from August 1, 2010 to July 31, 2011;

- from September 1 to September 9 with a billing period from September 1, 2010 to August 31, 2011?

* * *

Most often, business trips are paid based on salary in order to make fewer calculations. But it's not right. The average earnings will have to be calculated in any case. Otherwise, you may commit a violation for which you may be fined. If you pay for a business trip based on average earnings, there will be no violation on your part, even if the salary turns out to be higher.

<8> Article 25 255 Tax Code of the Russian Federation; Letter of the Ministry of Finance of Russia dated N 03-03-06/1/208. <9> Clause 1 of Art. 210 Tax Code of the Russian Federation; Part 1 Art. 7 of the Federal Law No. 212-FZ “On Insurance Premiums...”; clause 3 of the Rules for the accrual, accounting and expenditure of funds for the implementation of compulsory social insurance against industrial accidents and occupational diseases, approved.

Reflection of the amount of payment for a business trip in accounting

By default, the amount of payment for a business trip is included in the same method of reflection as the employee’s main salary.

If a business trip needs to be attributed to another reflection method, then the reflection method for a specific trip can be overridden - the choice of reflection method is made in the Business trip on the Additional :

Did the article help?

Get another secret bonus and full access to the BukhExpert8 help system for 14 days free of charge

Related publications

- How can I set up accrual for work on holidays and weekends so that the amounts accrued for working on a day off while on a business trip are not included in the calculation of the average? ...

- Income in kind using the example of daily allowances above the norm...

- When the resort fee increases the daily allowance by Federal Law of July 29, 2017 N 214-FZ as part of an experiment on...

- The Ministry of Labor explained the nuances of granting regular leave during a long-term business trip. The employer contacted the Ministry of Labor for clarification on how to apply for…

Average earnings during a business trip: we calculate without errors

Tickets for the use of taxi services as travel expenses can only be accepted if other modes of transport are not available. The question is relevant for small settlements.

A list of restrictions has been established for federal public sector employees; it is presented in paragraph 2 of Resolution No. 916.

The situation is similar with living expenses (renting residential premises). Payment is made for actually incurred and confirmed expenses. In order to save money, the institution may set a limit on the cost of accommodation per 1 day. As, for example, it is established for federal civil servants - no more than 550 rubles. The law allows payment of excess costs by saving money on this expense item, but an order from the manager is required.

When calculating daily allowances for business trips in 2021, no maximum or minimum limit has been established, that is, the payment for one day on a business trip can be either 5 rubles or 10,000 rubles. Article 217 of the Tax Code of the Russian Federation establishes the maximum values for payments that are not subject to taxation: in Russia - 700 rubles per day and 2,500 rubles when traveling abroad. If the daily allowance in an organization exceeds the approved norms, then insurance premiums should be charged on the difference and personal income tax should be withheld.

For federal government employees, a daily allowance limit is set at 100 rubles per day.

Determine the average earnings for calculating travel allowances according to the rules:

- To calculate the average salary, take into account accrual data for the previous 12 calendar months. If the employee has not yet worked for one year, then make calculations for the period actually worked (Article 139 of the Labor Code of the Russian Federation).

- Exclude from the total number of days periods spent on sick leave, maternity leave or child care. Details about which periods to exclude are given in paragraph 5 of Resolution No. 922.

- From your total earnings, exclude accruals for sick leave, benefits, and parental leave. Accruals for a previous business trip should be included in the calculation.

We divide the resulting amount of total earnings by the days actually worked to obtain the average daily wage. Now we multiply the resulting figure by the number of days spent on a business trip.

When calculating vacation pay, be sure to take into account the payment of average earnings for a business trip, since the employee worked (performed a job assignment). If we exclude travel payments from the calculation, the vacation pay will be less than if the employee did not travel anywhere. The posted employee retains his place of work (position), as well as his average earnings for the period of his stay on the trip, as stated in Article 167 of the Labor Code of the Russian Federation.

Transferable business trip in which month to accrue?

The concept of “travel allowance” is explained in Article 167 of the Labor Code of the Russian Federation.

The procedure for compensation of costs in commercial organizations is determined by a collective agreement or local regulatory act (LNA), taking into account current legislation. For employees of federal government institutions there is a special document - Decree of the Government of the Russian Federation of October 12, 2013 No. 916.

For employees of regional authorities, employees of municipal and state institutions, similar legal acts of local governments apply.

An online travel allowance calculator in 2021 will help you easily and effortlessly calculate the required amount to be paid. Below we will give an example of how to calculate without using an online calculator. In the meantime, step-by-step instructions will help you use a simple tool for calculating travel allowances in 2021.

Step 1

Enter the amount of earnings for the year preceding the business trip into the top line of the online calculator. It is important that it is not the previous calendar year that is taken into account, but rather the period of 12 months preceding the trip.

It would seem that the easiest way is to multiply the employee’s salary by 12. However, you need to remember an important nuance. If an employee had sick leave, he could receive a smaller amount of wages. Or, on the contrary, you can earn more due to bonuses in any month.

The exact amount of earnings is entered, taking into account such moments.

Let's assume that an employee's salary is 20,000 rubles. per month (no bonuses are provided), however, due to the fact that he was on sick leave, he received instead of 20,000 × 12 = 240,000 rubles, 228,000 rubles. To calculate, enter this value into the top line of the calculator.

Step 2

In the second line, enter the number of days the employee worked this year. Let’s say that due to sick leave he worked 228 days in the year preceding the trip.

Step 3

We indicate in the third line the number of days of the business trip.

Step 4

In the fourth line we enter the amount of daily allowance, which is established by the local regulations of your organization. Let's say 700 rubles. (since the amount exceeding this limit will need to withhold personal income tax and transfer insurance premiums).

Bottom line

The online calculator for calculating travel allowances in 2021 provides the final values using a simple formula, which we will look at in more detail below using an example. Here is the formula for calculating travel allowances, which is used in the calculator:

The online calculator will also show separately the amount of daily allowance to be issued and the amount of average daily earnings, but first of all it will show the amount of travel allowance that you must give to the employee before the trip.

Calculation of travel allowances in 2021 with examples

You can calculate travel allowances in 2021 without an online calculator. For this you will need:

- clarify the amount of daily allowance;

- determine average earnings for calculating travel allowances;

- add up the resulting numbers.

Let's start with something simple - calculating daily allowances for business trips in 2021. Employers have the right to determine this amount at their discretion; the law does not limit it.

The total amount of daily allowance is the product of the number of business trip days by the amount of compensation indicated in the LNA.

It is important to remember: daily allowance exceeding 700 rubles per day for a trip within the Russian Federation and 2,500 rubles for a trip abroad is subject to personal income tax and insurance contributions.

The next stage is calculating the average salary of a business traveler according to the norms of Article 139 of the Labor Code of the Russian Federation and Government Decree No. 922 of December 24, 2007. The travel allowance calculator in 2021 will do this itself online. But how to calculate travel allowances in 2021 manually? To do this you should:

- Determine the number of days actually worked by the employee, excluding sick leave, vacation and similar days, one year before the business trip or for the period during which the employee is on staff.

- Calculate the amount that the employee actually received for the time worked, also without taking into account guarantee payments and compensation.

- Calculate average daily earnings by dividing income by the number of days worked.

- Multiply the number of days on a business trip by the average daily earnings, not taking into account weekends and holidays if the person was on vacation at that time. If he worked on these days, payment is made in double amount (based on salary, tariff rate, piece rates) when these hours are above standard, and in single amount - if travel time falls on weekends and holidays (Article 153 of the Labor Code of the Russian Federation and paragraph 9 Decree of the Government of the Russian Federation of October 13, 2008 No. 749).

Features of calculations in non-standard situations

[R=math-calc]

The employee is sent on a business trip on the first working day. In this case, the salary established by the contract and the number of working days in the month are used for calculations.

Source: //kpasnokamsk.ru/vedenie-ip/buhgalteriya-ip/perehodyashhaya-komandirovka-v-kakom-mesyatse-nachislyat.html

How does the online travel allowance calculator work?

Step 1. In the first column of the calculator, indicate the employee’s total earnings for the billing period. You can calculate the amount for more than a month; in this case, do not forget to sum up the salary and other payments to the employee.

Step 2. Indicate in days how many days the employee worked during the pay period and how long he was on a business trip.

Step 3. Enter the amount of daily allowance that is established in the organization. This amount must be established by a local act.

Step 4. Click on the Calculate button.

Step 5: The result will be displayed in the table below. In addition to the amount of travel allowances, the calculator will calculate the average daily earnings and the amount of daily allowance.

Overtime work on a business trip

The question of how overtime hours are paid on a business trip is not regulated at the legislative level. Overtime work is considered to be work outside the normal working hours. However, when employees are sent on business, records of the time they worked during the trip are not kept. Consequently, there are no standards for determining normal working hours on a business trip.

The issue also concerns forms of payment. After all, during the days of a business trip, an employee receives an average salary. This is a guaranteed type of compensation, but not a type of remuneration. Consequently, the provisions of Article 99 of the Labor Code of the Russian Federation are inapplicable in such a situation. But what should an employer do, since not one of his subordinates will agree to work for free, especially beyond the established standards.

Procedure:

- Set standards. The procedure and amount of overtime payment should be specified in the regulations on business trips. For example, establish that for the first two hours of overtime, payment is 1.5 times the average earnings. For the rest of the overtime work - 2 times the amount. But additional payments may be higher, depending on the financial capabilities of the company.

- Obtain the employee's consent. To do this, send a written notice to the employee with a proposal for overtime work. In your application, be sure to include information about the increased payment. There is no unified proposal form; prepare a document in any form.

- Place an order. Having received the written consent of the subordinate, it is necessary to issue an order to engage in overtime work during the business trip.

- Ensure time is tracked. This is necessary for payment in full. Use a unified form of working time sheet or develop and approve your own, which the employee will fill out to record overtime and overtime.

IMPORTANT!

If duties on a business trip occur at night, then similar actions must be taken. Set the amount of payment in the business trip regulations.

Please note that if travel time falls during the night hours, from 00:00 to 06:00, then no additional payments or surcharges are due. For example, if an employee returns on a night flight, there is no need to pay for night hours.

How are travel allowances calculated?

The employer is obliged to pay the employee's travel expenses in full, subject to the provision of supporting documents. These can be tickets, checks, receipts for the use of any type of transport (river, sea, air, land), except for taxis for budgetary institutions. Tickets for the use of taxi services as travel expenses can only be accepted if other modes of transport are not available. The question is relevant for small settlements.

A list of restrictions has been established for federal public sector employees; it is presented in paragraph 2 of Resolution No. 916.

The situation is similar with living expenses (renting residential premises). Payment is made for actually incurred and confirmed expenses. In order to save money, the institution may set a limit on the cost of accommodation per 1 day. As, for example, it is established for federal civil servants - no more than 550 rubles. The law allows payment of excess costs by saving money on this expense item, but an order from the manager is required.

When calculating daily allowances for business trips in 2021, no maximum or minimum limit has been established, that is, the payment for one day on a business trip can be either 5 rubles or 10,000 rubles. Article 217 of the Tax Code of the Russian Federation establishes the maximum values for payments that are not subject to taxation: in Russia - 700 rubles per day and 2,500 rubles when traveling abroad. If the daily allowance in an organization exceeds the approved norms, then insurance premiums should be charged on the difference and personal income tax should be withheld.

For federal government employees, a daily allowance limit is set at 100 rubles per day.

Determine the average earnings for calculating travel allowances according to the rules:

- To calculate the average salary, take into account accrual data for the previous 12 calendar months. If the employee has not yet worked for one year, then make calculations for the period actually worked (Article If a business trip begins in one month and ends in another 139 of the Labor Code of the Russian Federation).

- Exclude from the total number of days periods spent on sick leave, maternity leave or child care. Details about which periods to exclude are given in paragraph 5 of Resolution No. 922.

- From your total earnings, exclude accruals for sick leave, benefits, and parental leave. Accruals for a previous business trip should be included in the calculation.

We divide the resulting amount of total earnings by the days actually worked to obtain the average daily wage. Now we multiply the resulting figure by the number of days spent on a business trip.

When calculating vacation pay, be sure to take into account the payment of average earnings for a business trip, since the employee worked (performed a job assignment). If we exclude travel payments from the calculation, the vacation pay will be less than if the employee did not travel anywhere. The posted employee retains his place of work (position), as well as his average earnings for the period of his stay on the trip, as stated in Article 167 of the Labor Code of the Russian Federation.

Business trip moves from one month to another calculate

Days and amounts related to payment of sick leave, vacations (including without pay), downtime through no fault of the employee, business trips, etc. are not included. The employee is sent on a business trip for 5 working days from March 1 to March 7, 2021. The calculation period is from March 2021 to February 2021 is 248 days.

The legislator does not give specific explanations, however, according to the logic of the current accounting rules, the following conclusions can be drawn: Average earnings - the same salary that is paid for a certain month on time;

Carrying payments: features of taxation (Fimina N.)

Firstly, the norms of the current labor legislation require payment of vacation pay three days before the start of the vacation. Moreover, as follows from the explanations of Rostrud, in this case calendar days are meant, not working days (Letter dated March 22, 2012 N 428-6-1).

Secondly, the duration of annual leave (not divided into parts) is, as a general rule, almost a month (28 calendar days). Therefore, the likelihood that annual leave will become transferable is quite high. There are two points of view regarding the payment of personal income tax on vacation pay in the case of rolling vacation.

The first of them assumes that for the purposes of calculating personal income tax, it is unacceptable to equate vacation pay with remuneration for work. In accordance with Art. Art. 106 and 107 of the Labor Code of the Russian Federation, vacation is the time during which the employee is free from performing work duties.

Payment for business trips in non-standard situations

This also applies to employees who have summarized working time recording.

This approach was confirmed to us by the Russian Ministry of Health and Social Development.

From authoritative sources Nina Zaurbekovna Kovyazina - Head of the Department of Labor Relations and Remuneration of the Department of Labor Relations of the Ministry of Health and Social Development of Russia “Summarized recording of working time for an employee sent on a business trip is not used; a time sheet is not kept for his working time during a business trip.

Therefore, his work schedule and days off are considered the same as in the organization where he works (see Regulation No. 749). The remuneration of such an employee on a business trip should be no less than the average salary at the main place of work.

Moreover, if a working day in the organization to which he is posted coincides with a day off for such an employee at his main place of work, he does not receive any additional payment for working on a day off.”

Calculation of travel allowances in 2021: average earnings, daily allowance, wages for business trips

At the same time, it is important not only to organize the trip, but also to correctly calculate travel allowances.

- 1 Calculation of travel allowances in 2021

- 1.2 Calculation of daily allowances

- 1.3 Paying sick leave on a business trip

- 1.1.1 Table: determination of average daily earnings for a business trip

- 1.2.1: daily allowance in 2021

- 1.1 Calculation of average earnings

- 1.1.3 Example of calculating average earnings

- 1.1.2 What is not included in the calculation of average earnings

Question: An employee of an organization is sent on a business trip, which begins in one month and ends in the next month. How to pay for days spent on a business trip according to average earnings: immediately for the entire period of the business trip in the month it began, or in proportion to working days in each month (i.e., some days are paid in the month of departure, and some in the month of return)?

(“New Accounting”, 2006, n 10)

Let’s assume that the employee went on a business trip on May 29, 2006, and returned on June 2, 2006. When paying for a business trip, the employee’s average earnings are calculated based on the wages actually accrued to him and the time he actually worked for the 12 months preceding the moment of payment (clause

3 Regulations). When calculating average earnings from the billing period

Travel allowances in 1C 8.3 ZUP

:

Rice.

2. “Business trip” in the personnel contour If the company maintains a staffing table, then when conducting a business trip on the “Main” tab, you must indicate the attribute “Free up the rate for the period of the business trip.” When specifying the attribute “Part-time/intra-shift business trip”, the field for indicating the hours of intra-shift business trip and the preempted planned type of time becomes active (Fig. 3):

Rice.

3. Intra-shift business trip If it is necessary to indicate in the employee’s PFR experience the fact that he worked on a business trip in an area with conditions different from the main place of work, then on the “PFR Experience” tab their value for the period of the business trip should be indicated (Fig. 4)

Average earnings on temporary business trips

In this case, they take into account (p.

9 Regulations on business trips): - working days spent at the destination; — working days on the way, incl.

9 Regulations on average earnings). The billing period is the 12 months preceding the month the business trip begins.

Calculation of average earnings during a business trip

Next, you need to determine the average daily earnings for calculating travel allowances using the formula:

Read about payments taken into account when calculating average earnings.

As for the days worked by the employee, these are all those days when he actually performed his job duties.

Thus, days worked do not include periods of vacation, temporary disability, downtime through no fault of the employee, etc. (). Knowing the average daily earnings, you can proceed to calculating the average earnings during a business trip. The total amount for the trip is calculated as follows ():

It happens that the amount of average earnings for calculating a business trip turns out to be less than the amount of the salary established for the employee.

Expenses for a “rolling” business trip

Excel formula for calculating average earnings: The employee was on a business trip from March 7 to March 13. According to the company's work schedule, this is 5 working days and 2 days off. We must multiply the average earnings by 5. Weekends are paid separately by order (if the person did work on those days). From the first day of employment, the employee goes on a business trip.

He has no actual days worked and no accrued salary. According to the contract, the official salary is set at 30,000 rubles.

Let's calculate the amount of travel allowance: 248 - the number of working days for the previous 12 months according to the production calendar. An employee goes on a business trip from...

That is, some days fall in February, and some in March. The calculation of average earnings for temporary business trips is not clearly stipulated in the legislation. Therefore, the accountant can calculate as it is more convenient for him (without infringing on the interests of the employee). However, for the application of this deferment there are a number of conditions (tax regime, type of activity, presence/absence of employees). So who has the right to work without a cash register until the middle of next year? <...

Home Accounting consultations Average salary Current as of: December 19, 2021 The days an employee is on a business trip, including days on the road and forced stops, are paid according to average earnings (Art.

Labor Code of the Russian Federation). Working days subject to payment are determined according to the work schedule established in the sending organization (clause 9 of the Regulations, approved by Decree of the Government of the Russian Federation No. 749).

In turn, days off are not paid according to the schedule. Let's consider the procedure for calculating the average salary for a business trip. Payment based on average earnings on a business trip Calculation of average earnings on a business trip begins with determining the billing period.

What is required from the employer? Is it necessary to submit to the Pension Fund in advance lists of future pensioners and documents necessary for assigning a pension? Or are the organization’s responsibilities limited to submitting the requested SZV-STAGE form to the Pension Fund for the future pensioner? Representatives of the Pension Fund Branch for Moscow and the Moscow Region told us what the role of the employer is in the process of applying for a pension by an employee. <... When paying for “children’s” sick leave, you will have to be more careful. A certificate of incapacity for caring for a sick child under 7 years of age will be issued for the entire period of illness without any time limits.

But be careful: the procedure for paying for “children’s” sick leave remains the same! <...Online cash register: who can take the time to buy a cash register? Individual business representatives may not use online cash register systems for up to a year. What are the standards for reimbursement of expenses during business trips? For an employee sent on a business trip, the employer fully reimburses expenses (Article 168 of the Labor Code of the Russian Federation) for transport, accommodation and other expenses agreed with the employer. A special type of travel expenses is daily allowances, which are reimbursed according to the standards established by the employer’s local regulations.

At the same time, at the legislative level, limits are set for accepting daily allowances as expenses without charging personal income tax and social contributions (clause 3 of Article 217, clause 2 of Article 422 of the Tax Code of the Russian Federation):

- in the amount of 700 rubles - for business trips around Russia;

- 2500 rubles - for business trips abroad.

The employee receives funds for all types of specified expenses before the business trip in one amount - in the form of an advance. Upon returning from a trip, the employee reports on it.

Working with the “Business Trip” document

If the duration of a business trip is within one month, then payment based on the average for the entire duration of the business trip is accrued using the document Business trip . The same document used to issue the business trip order is used. For a user with a accountant profile, this document displays details that are not visible to HR officers: average earnings, accrued amounts, payment procedure for business trips:

All amounts in the Business Trip are calculated at the input stage by the user with the HR profile, but are not displayed on the form. When a document is opened by a user with a calculator profile, he immediately sees the calculated amounts; all that remains is to check them, approve the document by checking the Calculation approved and carry it out.

If multi-user work is not configured in the program, then the approval checkbox is not displayed in the document form; it is considered that the document is approved immediately when it is submitted.

If the start date of a business trip falls at the beginning of the month (for example, June 5), and the Business Travel was entered before the salary for the previous month was calculated (for example, the order was issued on May 30, the salary for May had not yet been calculated), then in order to take into account the salary employee's average earnings for the last month (May) in the Business Trip will need to be recalculated. To do this, you can use the arrow button:

Expense report accepted

An employee returning from a business trip is required to report within three working days. He must provide the following documents to the accounting department:

- an advance report in which it is necessary to reflect all expenses incurred and funds received in the form of an advance;

- travel certificate, if the organization decides to use this form. Let us remind you that it is not necessary to use this certificate;

- an official task with a note on its completion or an official note explaining the circumstances and reasons for non-fulfillment of the official task;

- documents that confirm the costs incurred. For example, tickets confirm travel expenses, a hotel receipt confirms accommodation expenses, checks and acts confirm other expenses approved by the company’s management.

The accountant checks the entire package of documents, verifies the data of the advance report and supporting documentation, and summarizes the results. Let us remind you that daily allowances for business trips are not subject to mandatory confirmation. You can calculate the number of days you will stay on a trip using the dates from your tickets or travel certificate.

Travel expenses are written off, the posting depends on the purpose of the business trip. For example:

- to complete tasks for the main production, the accountant will make an entry: Dt 20 CT 71;

- for promoting goods and manufactured products - Dt 41 Kt71;

- for the acquisition of property and assets for use NO - Dt 08 Kt 71.

Postings for travel expenses in the budget:

- for costs associated with core activities - Dt 0 109 ХХ 212 Kt 0 208 12 000;

- for costs not related to core activities - Dt 0 401 20 212 Kt 0 208 12 000.

Who can and who cannot be sent on a business trip

By order of management, any employee of the enterprise who has the qualifications and work experience suitable for performing on-site tasks can be sent on official assignments. But there are exceptions.

Women who are expecting the birth of a child or have young children cannot be sent on a business trip; workers under 18 years of age, as well as those caring for sick loved ones or disabled children.

In all these cases, work outside the workplace is possible only with the personal written consent of a specific employee and the absence of medical contraindications.

Question: Where should I submit documents to receive travel expenses, payment for vacation travel, and monetary compensation for rented housing? View answer

Calculation of travel allowances in 2021 with examples

Let's consider controversial situations in calculating costs when sending employees on business trips.

Example 1. Payment of daily allowance.

The specialist went on a business trip in his car. Travel period: September 30 - October 5, 2021 Actual return day - (due to breakdown). How to pay daily allowance?

Payment of daily allowances must be made for all days of travel (holidays, weekends, days of arrival and departure, downtime, delay). Therefore, pay for all days from September 30 to October 8.

Example 2. Payment of average earnings.

The employee is sent on a business trip for 14 calendar days from.

For the period from to:

We calculate the average daily earnings: 415,200.00 / 174 = 2386.21 rubles.

We determine the amount of travel allowances to be paid for the period of the trip: 2386.21 × 14 = 33,406.94 rubles.

The employee was sent on a business trip. The personnel officer filled out all the orders, wrote out the official assignment, and the cashier paid the advance. The posted employee returned and provided the documents to the accountant. We will tell you further how to keep track of travel expenses in 2021 and how to correctly reflect a business transaction in accounting.

>How to reflect an advance on a business trip

Let’s say an employee contacts the institution’s cash desk to receive money for a business trip.

Calculation of travel allowances: cheat sheet for an accountant

Close Every year the SKB Kontur company holds a competition for entrepreneurs, hundreds of businessmen from different cities of Russia take part in it - from Kaliningrad to Vladivostok.

Through the competition, we have created an inspiring collection of business stories told by people who are turning small start-ups into successful companies.

Their experience and advice will be useful to anyone who is thinking about starting their own business.

To start, you need some prerequisites: an idea, some money and, most importantly, the desire to start Fred DeLuca Founder of Subway

Issue No. 21 Vyacheslav Shinkarev November 27, 2021 An accountant quite often has to calculate travel allowances. To make this task easier, we have prepared a convenient cheat sheet.

In it you will find information about the procedure for calculating travel allowances and about such nuances as additional payment before salary, payment for business trips on weekends, and calculation of daily allowances. The billing period is 12 calendar months preceding the month the business trip began, or less if the employee has worked for the company for less than a year.

To calculate travel allowances, only working days are taken into account, and not calendar days, as for calculating vacation pay. Sick leave, vacations, including without pay, business trips, downtime, etc. are excluded from the billing period (see Art. of the Labor Code of the Russian Federation and clause 5 of the Regulations on the specifics of the procedure for calculating the average salary of the Post.

Government of the Russian Federation). Petrova A.A. has been working since 02/10/2006, on 02/25/2014 she was sent on a business trip for 5 days. There are a total of 247 working days in the billing period (from February 2013 to January 2014). There were excluded periods: in August the sick leave period accounted for 8 working days, and in September the annual paid leave period accounted for 14 working days.

Then 247 – 8 – 14 = 225 days actually worked.

Here and below, calculations in the examples are given rounded to two decimal places. Fill out and submit the DAM through Extern: import the data of all employees into section 3 in one click, use filters and mass operations. Free for 3 months. The calculation of average earnings includes all payments that are provided for by the wage system, except for sick leave, vacation pay, financial assistance and other social payments (see.

2 and 3 Regulations on the specifics of the procedure for calculating average wages Post. Government of the Russian Federation). For information on the specifics of accounting for various bonuses, see also in paragraph.

15. If before or during an employee’s business trip there was an increase in salaries (tariff rates) for the organization (division) as a whole, it is necessary to index the average earnings to calculate travel allowances (see clause 16 of the Regulations on the specifics of the procedure for calculating the average salary of the Permanent Government of the Russian Federation ). Accrual of Popova A.

A. for all months except August and September - 40,000, in August - 26,086.96 rubles, in September - 12,000 rubles. Total for the billing period: (40,000 rubles × 10 months) + 26,086.96 rubles + 12,000 rubles = 438,086.96 rubles. We divide earnings for the billing period by the number of days actually worked in the billing period.

Then we multiply the resulting number by the number of days spent on a business trip.

Business trips are subject to personal income tax. (438,086.96 / 225) × 5 = 9,735.27 rubles of travel allowance must be paid to A.A. Popova. The employee will be charged personal income tax for this amount. If the payment for travel allowances based on average earnings is significantly less than the salary that the employee would have received if he had not been sent on a business trip, an additional payment can be made up to the actual earnings.

If such an additional payment is provided for by an employment or collective agreement or a local regulatory act, the tax base for income tax can be reduced by it (see paragraph 25 of Article 25 of the Tax Code of the Russian Federation and letters from the Ministry of Finance and).

However, you should always calculate travel allowances based on average earnings, and then compare them with the salary, so as not to worsen the situation of the employee if it is more profitable for him to receive average earnings.

If the days of a business trip coincide with days when the employee has a scheduled weekend, and he did not work on these days, payment is made not according to average earnings, but according to the rules for payment on a day off. If the employee was not involved in work on these days, then they are not paid.

And if an employee was involved in work on a business trip on a day off or was on the road, the average earnings for such days are not saved. Weekends are paid at least double or single, but with the right to “take off” the day off afterwards (see.

Art. and Labor Code of the Russian Federation). When calculating double payment, you need to focus on the employee’s remuneration system used (see.

letters from the Ministry of Finance and). Prepare and submit a zero calculation for insurance premiums through Extern. 3 months free. For each day of being on a business trip, including weekends and non-working holidays, as well as for days on the road, including during a forced stopover, the employee is paid daily allowances (Clause 1. Regulations on the specifics of sending employees on business trips, approved

Decree of the Government of the Russian Federation). The employee does not have to report on daily allowance (see letters from the Ministry of Finance,). The amount of daily allowance is established by the organization and enshrined in a collective agreement or local regulation (Art.

Labor Code of the Russian Federation). Expenses for the payment of daily allowances are taken into account when taxing profits without restrictions. Payment of daily allowances is exempt from personal income tax within the framework of the following standards: 700 rubles for each day of a business trip within the country and 2,500 rubles outside the country. Share , Issue No. 21, March 2014 Changes in the compulsory pension insurance system Vyacheslav Shinkarev Pavel Menshikov Anna Trestvyatskaya Alexey Krainev Irina Vasilyeva Alexander Lavrov Elena Kulakova Load more

Business trip moving to the next month calculation of the average

Added after 1 minute 44 seconds:

If the amount of OPV and personal income tax must be withheld from the daily allowance, then 1251 remains unclosed for the amount of deductions.

ilyasdayo says:

What wiring will show this?

ilyasdayo says:

. Answer: Dt 3350-Kt 3220 - 5 193 3.Dt 3350-Kt 3120 - 4 674 4.Dt 7210-Kt 3150,3210 - 5 141

ilyasdayo says:

If the amount of OPV and personal income tax must be withheld from the daily allowance, then 1251 remains unclosed for the amount of deductions.

account 1251 will close because

ilyasdayo says:

Dt 3350-Kt 1251- 51 930

. Since accrued income for St. 40 is added to the accrued salary for these days, then OPV and personal income tax are deducted from the total amount. With uv.

ilyasdayo says:

Did I understand correctly?

Yes. With uv.

Support

Counting business trip days

To calculate the exact number of days on a work trip, you will need round-trip tickets, a calendar and a calculator (if the business trip is long).

The first thing an employee needs to know is that business trip days are considered to be a full day spent by the employee on the road and in the city where he was sent to perform tasks. The days of departure and return of the employee are also added to them. Regardless of what time the business traveler left, this day will be counted as a full day.

If an employee returns from a trip at the beginning of the first night, the employer does not have the right to force him to come to the office in the morning of the same day.

Calculation example

Travelers Eduard Antipovich was sent on business for 20 calendar days in April 2021.

Its calculated data for the period February 2021 – March 2021:

| Indicators | Periods, days | Charges, rubles |

| Total number of days | 254 | 900 000,00 |

| Sick leave | 41 | 150 000,00 |

| Annual leave | 28 | 90 000,00 |

| Total | 185 | 660 000,00 |

Average daily earnings: 660,000 / 185 = 3,567.57 rubles.

Payment for a business trip based on average earnings: 3567.57 × 20 days. = 71,351.40 rubles.

For information about which accounting entries to reflect these transactions in accounting, read the article “How to keep records of travel expenses in a budget organization.”

Documenting

A local internal document recommended for enterprises and entrepreneurs by leading editors and auditors is the developed “Regulations on Business Travel”. In the document, it is important to specify the amount of daily allowance, document flow, how many days before the trip travel allowances are issued in part of the advance. Formally, an advance for the purchase of transport tickets can be issued immediately after the order is created.

Starting from the travel certificate, the official assignment and the travel report are optional documents. The trip is regulated by the manager’s order and the advance report, which requires close attention and clarity when processing.

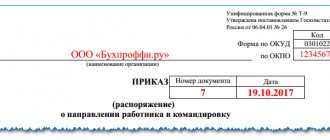

Business trip order

Documentation of a business trip begins with the execution of an order from the head of the enterprise, including:

- Full name and position of the employee;

- purpose of the trip;

- travel duration;

- locality;

- problems that need to be solved.

- An employer violates an employment contract: what should an employee do, how to sue

Based on the order, accounting considers travel days by number, issues daily allowances for them and pays the estimated costs of purchasing transport documents.

If a delay is necessary, the manager creates an additional order to extend the duration of the trip.

Advance report

Reflection of expenses in accounting, payment for a business trip and final payment to the accountable person are made on the basis of an advance report, which is submitted to the accounting department within 3 working days after arrival. Attached to the report are the accompanying documents:

- transport tickets;

- invoices, checks and receipts;

- commission fees;

- fee for obtaining documentation;

- currency exchange costs;

- luggage transportation and payment for luggage storage;

- residence documents;

- a copy of the international passport with border crossing marks;

- waybills when traveling by road and receipts from gas stations.

After the report is checked by the accountant and approved by the manager, the overexpenditure of funds is returned to the enterprise's cash desk, and the debt is paid to the employee. If the business trip is a moving one, in which month the expenses should be accrued and reflected in accounting is evidenced by the date of approval of the report, which forms the accounting entries.

What payment is guaranteed by law?

If an employee goes on a business trip, the employer, that is, the head of a budgetary institution, must provide such a specialist with compensation for his expenses.

Such expenses are associated not only with the purchase of tickets or renting a hotel room. Additionally, the payment for a business trip includes expenses that are aimed at compensating for the inconveniences associated with living outside the place of the main residence, that is, daily allowances. This is not a definitive list of guarantees. According to Article 168 of the Labor Code of the Russian Federation, the employer must guarantee the preservation of the workplace and payment according to the average earnings of the business trip.

Composition of travel expenses:

- Average salary for days spent on a business trip. Calculated based on the average for the 12 months preceding the month of business trip.

- Daily allowance. The organization must have a limit for payment. There are no legal restrictions; the size depends on the financial capabilities of the enterprise. The amount depends on the number of days of the business trip.

- Fare. Includes payment for tickets, commissions, insurance, and other types of expenses. For example, compensation for fuel and lubricants for an employee using a personal car on a business trip.

- Living expenses. It is acceptable to include payment for a hotel room, payment for a bed or room in a dormitory, or payment for renting an apartment on a daily basis.

- Other expenses agreed with the employer. For example, an employee uses personal transport for a work trip. The cost of maintaining the car while on the road can be paid by the employer.

IMPORTANT!

Not all trips and trips of specialists can be classified as business trips. The article “Which trips are considered a business trip” will help you understand the situation.

How to correctly reflect daily allowances beyond 40 days? What kind of postings?

danna123 says:

Daily allowances over 40 days are subject to personal income tax SN CO OPV. What steps should I take? and how to properly prepare an advance report?

I offer: 1.Dt 1251-Kt 1010,1030. 1.Dt 7210-Kt 1251-Advance report (40 days). 2.Dt 7210-Kt 3350-Table (daily allowance*number of days over 40 days: 0.81). 3.Dt 3350-Kt 3220. 4.Dt 3350-Kt 3120. 5.Dt 7210-Kt 3150,3210. 6.Dt 3350-Kt 1251-Withholding the amount of daily allowance in excess of 40 days. With uv.

esiphi says:

6.Dt 3350-Kt 1251-Withholding the amount of daily allowance in excess of 40 days.

This wiring, in my opinion, is superfluous. If we do not pay the employee these daily allowances, then why accrue them and withhold taxes from them?

Avail says:

This wiring, in my opinion, is superfluous.

I didn’t quite write it right, the posting is needed to close 3350, but it’s probably better to include it in the expense report.

esiphi says:

1.Dt 1251-Kt 1010,1030. 1.Dt 7210-Kt 1251-Advance report (40 days). 2.Dt 7210-Kt 3350-Table (daily allowance*number of days over 40 days: 0.81). 3.Dt 3350-Kt 3220. 4.Dt 3350-Kt 3120. 5.Dt 7210-Kt 3150,3210.

in this situation, daily allowances in excess of the norm will be reflected in account 3350 Salaries to employees, and daily allowances are not the employee’s income, but an expense of the enterprise - compensation for business trips. What should I do? This amount should not be in the payroll.

Added after 1 minute 19 seconds:

In 1C, with such postings, will it “sit” correctly or does something else need to be done?

danna123 says:

and per diem is not an employee’s income

Article 155 of the Tax Code says:

3. The following are not considered as income of an individual: ... for a business trip within the Republic of Kazakhstan - daily allowance not exceeding 6 times the monthly calculation index, ...

therefore, what is higher is income

When average earnings are less than salary

When calculating the average earnings, in addition to the salary, in particular, bonuses and salary increases in the organization during the billing period and after it are taken into account <5>. As a rule, such payments occur per year. Therefore, the average earnings will be higher than the salary. But in the case of an individual salary increase, most likely the salary will be higher than the average earnings.

Attention! Even if you pay for a business trip based on your salary, you will have to calculate your average earnings.

And even in a situation where during the entire billing period the employee’s salary was equal to the salary (that is, there were no additional payments, bonuses, etc.), the average earnings will be greater than the salary. The only exception to this rule is when the business trip falls in months with 20 working days or less, since in 2009 and 2010. the average monthly number of working days, taking into account which average earnings are calculated, is 20.75 (249 days / 12 months). This means that the cost of a working day, calculated based on salary, will be higher in such months. This year it is January, February and May.

Therefore, if you make an additional payment before your salary so that employees do not lose money, you only need to pay extra if the business trip falls within these months.

Example. Comparison of average earnings and salary for business trip in January 2010

Condition

The employee was sent on a business trip from January 12 to January 14, 2010.

The employee's salary is 10,000 rubles.

The organization operates on a five-day work week. In January 2010, according to the production calendar, there are 15 working days.

The employee worked the entire pay period (January - December 2009).

In the organization, the regulation on remuneration stipulates that travel time is paid based on salary if the average earnings are less than the salary.

Solution

- We calculate the average daily earnings of an employee for the billing period:

(RUB 10,000 x 12 months) / 249 days = 481.93 rub.

- We calculate the daily part of the employee’s salary for January 2010:

10,000 rub. / 15 days = 666.67 rub.

- We pay for working days of a business trip based on salary, since the daily part of the salary is more than the average daily earnings:

RUB 666.67 x 3 days = 2000.01 rub.

Example. Comparison of average earnings and salary for business trip in June 2010

Condition

The employee was sent on a business trip from June 21 to June 23, 2010.

The employee's salary is 10,000 rubles.

The organization operates on a five-day work week. In June 2010, according to the production calendar, there were 21 working days.

The employee worked the entire billing period (June 2009 - May 2010).

In the organization, the regulation on remuneration stipulates that travel time is paid based on salary if the average earnings are less than the salary.

Solution

- We calculate the average daily earnings of an employee for the billing period:

(RUB 10,000 x 12 months) / 249 days = 481.93 rub.

- We calculate the daily part of the employee’s salary for June 2010:

10,000 rub. / 21 days = 476.19 rub.

- We pay for working days of a business trip based on average earnings, since the daily part of the salary is less than the average daily earnings:

RUR 481.93 x 3 days = 1445.79 rub.

<5> Article 139 of the Labor Code of the Russian Federation; pp. 2, 9, 15, 16 Regulations on the specifics of the procedure for calculating average wages, approved. Decree of the Government of the Russian Federation No. 922.

Answer

If a business trip begins in one month and ends in another, the accountant has questions about how to determine average earnings, calculate personal income tax and contributions, and take into account expenses when calculating income tax. Let's look at each question separately.

During the business trip, the employee retains his average salary (Article 167 of the Labor Code of the Russian Federation). It replaces wages for working days missed due to a business trip. It is impossible to pay an employee a regular salary during a business trip (letter of Rostrud dated 02/05/2007 No. 275-6-0). Average earnings are part of wages. Therefore, if a business trip began in one month and ended in another, distribute the payment for the duration of the business trip by month.

How many times to calculate average earnings

Calculate your average earnings once as of the day the business trip starts. Do not recalculate your average earnings every month. One business trip - one case, in connection with which the average earnings are maintained (Figure 1 below).

SCHEME. ONE TRANSITIONAL TRANSMISSION

If an employee returned from a business trip in one month and then left for the next, calculate the new average earnings for the second business trip (Figure 2 below).

SCHEME. TWO BUSINESS TOURS

When to pay the average salary for a business trip

The accountant calculates the average salary based on the report card data. In most companies, the timesheet is closed once - on the last day of the month, but payments are made twice a month (Part 6 of Article 136 of the Labor Code of the Russian Federation).

Determine the amount of the advance according to the rules established by local regulations. Take into account the time during which the employee was released from work in the first half of the month. Travel days are counted as time worked. The employee is entitled to a regular advance payment.

At the end of the month, calculate the salary for the days worked, the average earnings for the days missed due to a business trip. When paying, withhold personal income tax and the advance payment.

EXAMPLE

Average earnings during a business trip

On July 31, 2021, A.S. Kondratiev went on a business trip. The duration of the business trip is four days (from July 31 to August 3). The employee's official salary is 36,000 rubles.

In the billing period from 07/01/2017 to 06/30/2017, the employee worked fully for 11 months. In September 2021, he was on vacation for 20 working days. For the time worked this month, the employee was accrued RUB 3,272.73.

The company’s local regulations establish that the advance is paid in the amount accrued for the time actually worked in the first half of the month, taking into account a coefficient of 0.87. Payment deadlines are the 20th and 5th.

The employee does not have rights to deductions for personal income tax.

How to calculate average earnings for a business trip and when to pay?

Solution

The accountant will calculate the average daily earnings once as of the start date of the business trip - July 31, 2021. The billing period is from 07/01/2017 to 06/30/2017. It has 248 working days. The average daily earnings will be 1,751.2 rubles. .

Charges and payments for July

On July 20, the employee received an advance in the amount of RUB 14,914.29. (RUB 36,000: 21 work days × 10 work days × 0.87).

On July 31, the accountant accrued to the employee:

- salary for days worked - 34,285.71 rubles. (RUB 36,000: 21 work days × 20 work days);

- average earnings for one day - 1751.2 rubles. (RUB 1,751.2 × 1 work day).

The total amount of accruals is RUB 36,036.91. (RUB 34,285.71 + RUB 1,751.20).

On August 4, the employee received, minus personal income tax and advance payment, 16,437.62 rubles. (RUB 36,036.91 – RUB 36,036.91 × 13% – RUB 14,914.29).

Charges and payments for August

On August 18, the employee received an advance payment of 14,979.13 rubles. (RUB 36,000: 23 work days × 11 work days × 0.87). The accountant calculated this amount according to general rules.

On August 31, the accountant accrued to the employee:

— salary for days worked — 31,304.35 rubles. (RUB 36,000: 23 work days × 20 work days);

— average earnings for 3 days of a business trip — 5253.6 rubles. (RUB 1,751.2 × 3 working days).

The total amount of accruals is RUB 36,557.95. (RUB 31,304.35 + RUB 5,253.6).

On September 5, the employee will receive, minus personal income tax and advance payment, 16,825.82 rubles. (RUB 36,557.95 – RUB 36,557.95 × 13% – RUB 14,979.13).

Subscription to "Salary" - pay for six months, and read for 12 months!

Annual subscription to “Salary” at the price of half a year. Pay your bill with gift months. Or pay by card on our website.