A balance sheet asset is one of two parts of equal value containing information about the property of an economic entity. The information is compiled on the basis of reliable accounting records and includes data on tangible and/or intangible objects; existing financial investments; cash/non-cash funds and their equivalents; accounts receivable. Briefly, a balance sheet asset is a kind of inventory of an enterprise’s property, the total result of which is always equal to the liability or sources of funds for financing business activities.

Concept and classification of assets

Assets are the property of an enterprise that should bring profit in the future. In other words, these are financial investments that create constant passive income for the asset holder and increase their value over time. Assets are classified:

- By form of functioning: material: land, structures, finished products, equipment;

- intangible: licenses, copyrights, patents, trademark;

- financial: cash deposits, accounts, debts from individuals and legal entities.

- current assets are property assets used in the current activities of the organization and involved in daily production costs. This group includes cash (in cash, on current and foreign currency accounts), investments in securities (short-term), inventories (raw materials, supplies, inventory, finished products), accounts receivable (if the maturity date is no more than a year), VAT according to acquired values;

- gross - property assets acquired with both own and borrowed capital;

In addition to the main types, there are “hidden” and “imaginary” assets. “Hidden” assets are not reflected when preparing the balance sheet. These may be organizational expenses when creating an enterprise, costs for acquiring a license, training and certification of personnel, improvement of equipment, underestimated residual value of fixed assets and intangible assets due to the use of various methods of depreciation.

“Imaginary” assets, although reflected on the organization’s balance sheet, are in fact absent. It is impossible to obtain significant financial benefits from owning “imaginary” assets, either in the present or in the future. Usually these are funds that have already been written off for a certain time, but for some reason remain not written off. For example, unwritten-off unusable and damaged materials or expired accounts payable.

According to the classification of IFRS (international financial reporting standards), there is another type of assets - excess. These include funds that are not currently needed for the main activities of the organization, for example, an excess amount of equipment in a construction company.

Answers to common questions

Question No. 1: How to reflect in the balance sheet information about the developed computer program that is planned to be implemented?

Answer: Products of electronic computers, as well as software, are intangible assets of the enterprise and are reflected in the asset balance sheet.

Question No. 2: How to competently use borrowed funds in a company’s activities?

Answer: The optimal ratio of the company's founders' own funds and money borrowed is 50/50. As a rule, borrowed funds are used in the field of activity that is aimed at obtaining quick financial results.

Table of potential investments

| Assets | Receiving a profit |

| Bank deposits | Money stored in a bank account (ruble or foreign currency) generates passive income thanks to accrued interest on the investment |

| Business | Money can be invested in a business that will generate income over time |

| Stock | When purchasing shares, the owner can expect to receive dividends from business profits. You can make a profit both from annual income and from the sale of shares |

| Bonds | Purchasing long-term bonds will create a stable source of income for many years. Interest on bonds is accrued once or twice a year |

| Real estate | Investing in real estate is considered the most reliable way to generate passive income. Such a purchase guarantees the owner a constant flow of funds from rent. In addition, the price of real estate increases every year |

| Shares and units in mutual funds (mutual investment funds) | This method is usually used by people who want to quickly and easily invest their capital, without thinking about what and where. For profitable and effective use, the money is placed under the management of professionals who charge a certain percentage for their services. |

| Precious Metals and Collectibles | Investing in gold, silver, paintings, rare coins and other items is one of the best and most reliable ways to invest your savings, as their value is constantly growing |

| Machinery, equipment, transport and more | The owner of these things can receive revenue from their operation |

In addition to the usual sources of income, there are non-standard assets. These can be content sites, YouTube channels, promoted Instagram profiles, VKontakte public pages, photo stocks.

Passives and their varieties

Unlike an asset, a liability is the source of the formation of these assets - capital, as well as reserves. Liabilities also include obligations to the budget and creditors, for example a bank or supplier.

Liabilities include:

- taxes;

- mortgage;

- consumer loans;

- borrowed funds (IOUs, checks, bills, letters of credit);

- movable and immovable property (apartment, car, equipment).

An apartment is one of the controversial points when dividing property into assets and liabilities, since it can fall into two categories at once. For example, renting out an apartment implies receiving passive income, and accordingly is classified as an asset. If the owner personally moves into the apartment or lets his relatives there free of charge, in this case the apartment will be in the role of a liability.

In the production sector, a liability reflects the obligations that an organization has undertaken in the course of doing business. Paying off liabilities results in a decrease in assets. This could be the payment of funds, the provision of services, or the replacement of one obligation with another. Obligations are:

- short-term - current liabilities that must be repaid in the next year from the date of drawing up the balance sheet. This includes accounts payable of the organization itself, for example, debts to employees, lessors, suppliers of raw materials and equipment;

- long-term – financial obligations that require partial repayment over a long period of time. These include deferred liabilities for loans and credits received for a period of more than one year.

All liabilities of the organization are classified into the following categories:

- Imaginary liabilities. They are reflected in tax or accounting records on a certain date to calculate the exact value of net assets, and in fact they are repaid. Timely identification of imaginary liabilities will help prevent double payment, that is, it will preserve the company’s working capital without reducing its value.

- Hidden liabilities are obligations that are actually absent, but, nevertheless, are reflected in the structure of credit, tax and off-budget payments. They can arise when drawing up a balance sheet due to untimely write-off of credit and tax debts in accounting.

- Actual - liabilities that actually exist and are reflected in the balance sheet. The maturity of these liabilities is determined by the date of their repayment, specified in the drawn up agreement. When fulfilling obligations on actual liabilities, the organization always loses part of its own assets. This can be finished products, fixed assets or working capital.

Current liabilities in accounting. balance sheet: composition, line-by-line distribution

So, short-term liabilities are those obligations that are repaid in a period of no more than a year. In the form of an updated balance sheet, they are reflected in Section V. The composition of this section and the line-by-line distribution of liabilities is as follows.

| Borrowed funds | Creditor. debt | Future income periods | Estimated liabilities | Other obligations | Summary of Section V |

| Page 1510 | Page 1520 | Page 1530 | Page 1540 | Page 1550 | Page 1500 |

The total for the entire section (line 1500) or the sum of all completed lines of this section minus line 1520 (accounts payable) is the value of P2 (short-term liabilities). In other words:

When calculating, a question may arise as to where to include future income. Despite the fact that they are formed at the current moment, and the obligations under them are in the short term, they last more than 2 years. That is, we are talking about future income. In this regard, it is assumed that such future income is usually equal to zero, so it does not matter where they are taken into account. Meanwhile, in many services that provide financial analysis services, they are taken into account in long-term liabilities.

Taking into account the above, the above formula may be modified. The calculation can also be done like this:

Another option for calculating P2, in addition to the above lines, includes one more:

Formula 2 is considered the most optimal calculation option. What is important is that there is no separate standard for P2. But it is recognized that a decrease in this indicator is a positive factor.

Balance sheet

The balance sheet is the most important form of corporate reporting, characterizing the financial position of an organization for a certain period of time. Balance sheets are submitted to the tax authorities. Banks study such reports to assess the creditworthiness of the organization, and for shareholders they serve as a financial indicator of the work performed by management.

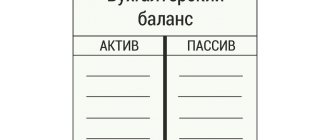

The balance sheet consists of two sections: assets and liabilities. Although these two sections are different, they are still closely related to each other. The slightest changes in one section will affect the other section. Therefore, the total amount of all components of the balance sheet must be the same, that is, in the end, assets and liabilities must always be equal.

The balance sheet is the main source of information for analyzing the production activities of an organization. The planned balance sheet is compiled on the basis of information about all financial flows of the company (including those expressed in foreign currency). It is depicted in the form of a table, where assets are on the left side and liabilities are on the right.

| Balance sheet | |

| Assets | Liabilities |

| Fixed assets and intangible assets (apartments, cars, equipment, computers) | Capital and reserves, earmarked proceeds, treasury shares |

| Inventory | Profit and loss from activities |

| Accounts receivable (cash or inventory that is owed to you) | Short-term obligations to suppliers, budget |

| Cash and short-term investments | Long-term obligations to lenders, banks |

Video on the topic:

Some features of entering data into Section V of the account. balance

Passive buh. The balance sheet is presented in two sections: “Long-term liabilities” (Section IV) and “Short-term liabilities” (Section V). According to the last, fifth section, it is necessary to display information about short-term financial sources attracted by the enterprise. It is recommended to take into account the following features of filling out lines:

- on page 1510, register data using the account. 66 and partially 67 (settlements for short-term and long-term loans, credits);

- on page 1520 indicate the generalized amount of all types of short-term debt (data for accounts 60, 62, 68, 69, 70, 71, 73, 75, 76).

- line 1530 is completed if this accounting object is recognized in accordance with accounting provisions;

- on page 1540 show credit. account balance 96;

- page 1550 is intended to display those types of short-term liabilities that were not included in the previous lines mentioned above;

- page 1500 reproduces the total for all previous lines 1510–1550.

Thus, the total amount of short-term borrowed capital of the enterprise is the result according to section. V, i.e. page 1500. When forming the book. balance sheet and, in particular, section. V, one should also take into account the fact that enterprises autonomously detail the indicators for the relevant items of the generated reports. This right is reserved for all organizations and is justified. So, for example, an enterprise has the right to supplement p. 1520 in section. V in the appropriate lines, detailing, deciphering in this way, this or that indicator.

Personal budget accounting

Assets are a positive cash flow that multiplies capital. Liabilities are negative cash flows that take cash away from equity. In simple and accessible language, an asset is property, a liability is the source of this property. It is necessary to strive to ensure that the income received from assets exceeds the expenses on liabilities. To do this you need:

- Determine the size of your own liabilities, that is, monthly expenses and current needs.

- Distribute expenses. Refuse unnecessary entertainment (restaurants, theaters, clubs) and the purchase of expensive things.

- Determine your own assets with the highest return, that is, everything that brings profit.

- Compare the difference between assets and liabilities. Successful people argue that there should be more assets than liabilities. If they are in equal proportions, the person will balance at the same level.

| Tools | Are an asset | Are a liability |

| Cash | On a bank account | If borrowed from a friend |

| Real estate | For Rent | Used for personal purposes |

| Automobile | Involved in business | Used for personal purposes, incurs expenses or is rented |

| Earth | Rented and generates income | Not used and does not generate income |

| Knowledge | When they bring in income | When they paid for them, but they never brought any income |

Only by correctly distributing assets and liabilities can one achieve material well-being. To put it most simply, assets are everything that generates income, that is, they are positive cash flows that increase capital. Liabilities are everything that money is spent on, negative cash flows, in other words, expenses.

Industrial use

Modern economists and investors interpret the concepts of asset and liability in two ways. The first interpretation defines traditional economic concepts from the field of accounting. The second is used in connection with the development of the topic of personal capital management. Assets and liabilities are everything that forms a company's balance sheet. Company property in any form is considered an asset; liabilities are debt obligations.

Any intangible and tangible property that an enterprise has, as well as rights to property, are assets of the company. Assets are any property of the enterprise, liabilities are the funds at the expense of which the formation of property is carried out. Liabilities are considered to be the capital of an enterprise:

- joint stock;

- borrowed;

- statutory;

- credit.

The assets of the enterprise are classified according to:

- Form of participation in the production process (current and non-current).

- The nature of the functioning (financial, intangible, material).

- Ownership rights (own, leased).

- Source of formation (net, gross).

- Liquidity.

Assets and liabilities reflect the company's balance sheet, which is prepared for a specific period. Balance sheet equilibrium is considered to be their equality. The first ones are arranged in the balance sheet according to increasing liquidity, and the second ones - according to the urgency of involvement in turnover.

Short-term liabilities P2 in formulas for calculating liquidity indicators

Liabilities from group P2 are used in calculating a number of liquidity ratios. In particular, when calculating KTL, KSL, KAL. These are the main ratios of current, urgent and, accordingly, absolute liquidity. Each of them has a specific purpose.

For example, CTL (current ratio), the most famous and often used in financial analysis. It is calculated as follows:

In the said formula there is a group of short-term liabilities P2, as well as P1, A1, A2 and A3. That is, by itself, separately, the P2 indicator indicated in formula 4 is not analyzed, but only participates in the calculation. But without it, calculation and analysis of the KTL value is not possible.

If, based on the calculation results, KTL = 1.5–2, then this will mean compliance with the norm. A KTL value that is less than 1 indicates the enterprise’s inability to pay current obligations on time. There is a destabilization of the financial situation, which, according to the logic of events, implies the presence of significant financial risks for the enterprise.

The remaining liquidity ratios are calculated and analyzed in a similar way. For comparison, the calculation of the CLR (urgent, critical or quick liquidity ratio) is considered below. Using it, you can find out the ability of a particular enterprise to pay current obligations in a difficult financial situation using A1 and A2. Formula for calculating KSL:

This formula uses A1, A2 and P1, P2. That is, there is more than one P2 indicator. The result of calculation with his participation in the situation under consideration must be at least 0.7. If the value of the CFL is less than this minimum, then we can talk about a drop in the solvency of the enterprise. The best result is considered to be a value of KSL = from 0.8 to 1.2.

Types of assets

Assets in the modern investment interpretation are all investments that generate constant (passive) income or increase in value over time: investments that generate constant income, profits from your own business, land, real estate, etc. There are many different assets, the most famous and popular of which are:

| Assets | Description |

| Bank deposits | Funds held in bank accounts from which interest accrues |

| Bonds | Income is generated through coupon payments, which are accrued after a certain time (once every 3 months, 6 months or 12 months). Purchasing long-term bonds creates a constant source of income for a long time. |

| Stock | These securities provide the opportunity to receive two types of income. Firstly, purchasing shares is buying part of a business that will rise in price over time, which means that the price of shares will also rise. Secondly, by purchasing shares that involve the payment of dividends, the owner has the right to expect to receive the company's annual profit, which is proportional to the number of shares purchased |

| Real estate | It is considered the most reliable way to generate income. Investing in the purchase of real estate guarantees a constant flow of cash from rental income. And the price of real estate gets higher over time |

| Mutual funds and other investments | This method of generating income is suitable for those who do not want to think independently about where to invest their capital. In this case, finances are transferred to the management of a team of professionals who have experience in this field and know how to effectively use financial instruments. This contributes to more efficient use of money |

| Borrow money | This will be considered an asset if the money is lent for a reason, but out of financial interest. Otherwise, the debt will be a liability |

| Acquisitions with future appreciation | This is everything that constantly increases in price over time:

|

Types of liabilities

The following are considered liabilities:

- mortgage;

- loans;

- credit cards;

- consumer loan taken for the purchase of expensive items, travel, etc.;

- all property (movable and immovable): apartment, car, household appliances, gadgets, etc. Everything that a person owns and uses in everyday life is considered liabilities;

- unprofitable business, since additional funds will be needed to close it;

- money borrowed. Even if money was lent without interest, it is still a liability, since it must be returned.

To better understand what a passive is, we can consider two examples:

- A man bought an expensive car. It appears to be a valuable purchase and could be considered an asset. However, as soon as the car leaves the showroom, it immediately loses about 20% of its price. The owner will have to pay insurance, buy gasoline, pay for repairs, etc. Consequently, in this situation, the car does not make a profit, but requires additional expenses.

- A man took out a mortgage and bought a house. The banker considers the purchased real estate an asset, and in his own way he is right. But the subtlety is that the house is an asset of the bank, but not the borrower. It makes no difference to the banker what the loan is for: to purchase a house, a yacht, or a luxury car. The bank will own this property until the borrower pays off the entire cost with interest. Thus, the acquired property is a liability.

An asset can become a liability and vice versa

For example, people suddenly moved out of an apartment that the owner had rented out. The owner remains the owner of the apartment and bears the burden of expenses: rent, utilities, repairs, taxes, etc. All this makes him poorer, which means the apartment is considered a liability. But when this apartment is rented again, it will again be a source of income. Therefore, we can conclude: a liability makes a person poorer, and an asset makes a person richer.

Take a look at two more examples:

- It was stated above that purchasing a car is considered a liability. If we assume that the owner of the car decided to work as a taxi driver, the car becomes an asset, since it will generate income;

- real estate (houses and apartments) purchased for rental is an investment and therefore generates profit. Even if we take into account the growth of inflation by 15 -20% per year, the value of real estate grows over time, and such investments bring profit to the owner.

Low-income people tend to spend all their income. All funds are spent on food, utilities, taxes, Internet, communications and entertainment. There is barely enough money until the next salary. A person is forced to borrow money, then pays off his debts, and so on all the time. There are no opportunities to acquire assets.

Middle class people have a lot of expenses equal to a lot of money they earn. These people are accustomed to leading a decent lifestyle and acquire many liabilities: a house, a dacha, a car, etc. Often, to make these acquisitions, they take on debt. It turns out that the higher their income, the higher their expenses. The middle class pays a lot to cover their debts: the more they earn, the more they spend.

Rich, wealthy people are distinguished by the fact that they try to get rid of liabilities and acquire assets. If they really want to buy a liability, they first buy an expensive asset. Wealthy people constantly make sure that their assets always exceed their liabilities.

For example, I wanted to buy a new car. First you need to buy real estate and rent it out, and only after that buy a car. It's safe to say that passive income is created with the help of assets.

Analysis of indicators

Having completed the arithmetic calculations, we move on to analyzing the result obtained. With a positive amount of net assets in the balance sheet, we can conclude that the company is profitable and has high solvency. And, accordingly, the higher the indicator, the more profitable the enterprise.

Negative net assets are an indicator of the low solvency of an enterprise. In other words, a company with a negative NAV will most likely go bankrupt soon; the company will simply have nothing to pay off its debts. However, in such a situation, exceptional circumstances must be taken into account. For example, the company has just been formed and has not yet covered its costs, or the company received a large loan for expansion.

An increase in net assets can be achieved by increasing the authorized, reserve or additional capital or by reducing the founder’s debts to the enterprise.

Maintaining balance

Our world cannot exist without liabilities. People live in houses, drive cars, and enjoy the benefits of life. You need to learn to find a balance, try to ensure that the income received from assets far exceeds expenses. In order for your life to be financially stable, you first need to determine your existing liabilities and monthly expenses, identify unnecessary expenses and decide how to reduce them.

Then evaluate the assets, determine what and how generates income every month. There can be many sources of income. They contribute to the achievement of financial freedom when money works for the person, and not the person for it. Having assets, a person stops working for money. Of course, you can have a country villa as a liability, but this is if the owner is a billionaire and also has factories, oil rigs, a yacht, etc.

It is necessary to take into account that by owning assets you can live in abundance, but for this you need to learn to live within your means. Try not to take out loans, and if you have them, pay them off on time. Credits and loans are monetary bondage, lowering the overall standard of living.

You need to create a step-by-step action plan to increase income and reduce expenses. Buy assets when free funds appear from existing assets. This could be profit from real estate or business, interest from investment activities. A clear understanding of what the actions taken can lead to - a decrease or increase in well-being - is necessary.